4 May, 26

Weekly Crypto Market Wrap: 4 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- U.S. spot BTC ETFs saw ~US$153.8M in inflows; ETH ETFs added ~US$101M

- Robinhood’s Q1 crypto revenue and trading volume fall nearly 50%

- Tether posts over $1 billion Q1 profit as reserve buffer reaches record $8.2 billion

- Ethereum Foundation’s recent ETH sales to Tom Lee’s Bitmine hit $47 million after latest deal

- Coinbase says deal reached on Clarity Act stablecoin yield, clearing path to long-stalled Senate markup

Technicals & Macro

Markets

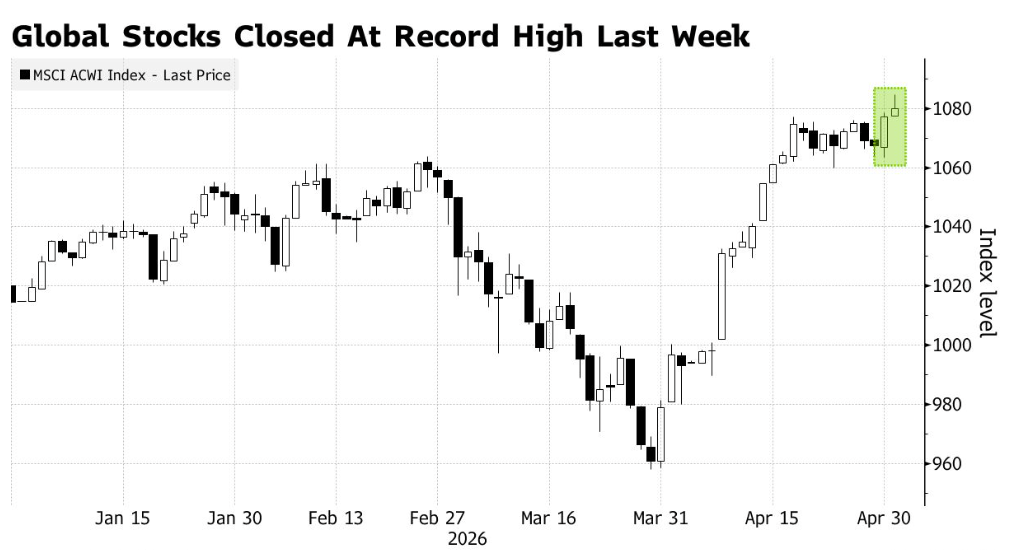

Markets closed April with their strongest monthly performance since 2020. The S&P 500 and Nasdaq both posted fresh all-time highs in a powerful month-end melt-up that has effectively erased every dollar of war-driven underperformance. The S&P 500 closed Friday at 7,230, the Nasdaq broke above 25,000 for the first time ever, and both indices logged a fifth consecutive weekly advance – the longest run since October 2024.

Source: Bloomberg

Three forces converged to drive the rally: a strong Q1 earnings season tracking 18% growth (well above the 14.4% expected at the start of April); continued ceasefire diplomacy with Iran reportedly submitting a fresh agreement proposal via Pakistani mediators on Friday; and a Magnificent Seven earnings cycle that has thoroughly validated the AI infrastructure thesis. Apple jumped 3.3% on Friday after delivering a strong fiscal Q2 beat driven by the iPhone 17 cycle and MacBook Neo demand. Atlassian surged 29.6%, Reddit gained 13.1%, and Salesforce added 4.1% as the software complex caught a bid alongside the chip rally. The casualties were idiosyncratic: Roblox -18.3% on a sharp guidance cut tied to new safety protocols, and Spirit Airlines -60% as a USD$500m government bailout fell apart and the airline prepared to wind down operations.

Source: X.com (@Truflation)

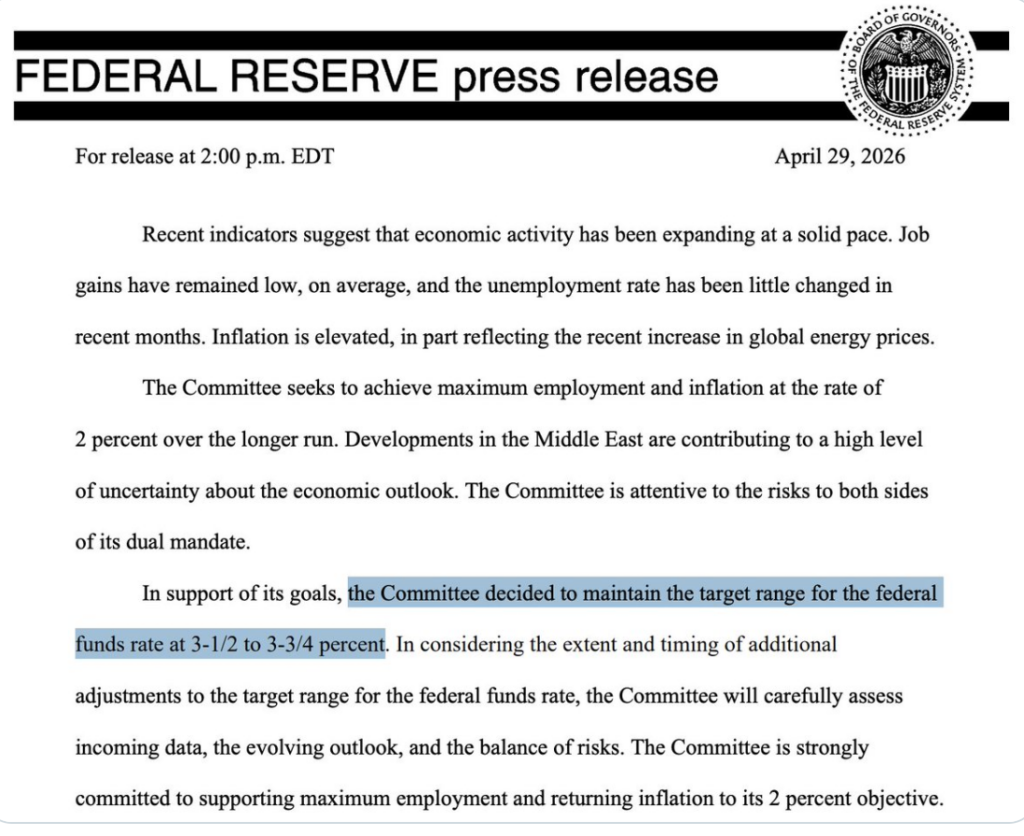

The headline macro event was Wednesday’s FOMC meeting, Powell’s last as Chair, and it was anything but routine. The Fed held rates at 3.50-3.75% as universally expected, but the vote split 8-4, the most dissents since October 1992. Stephen Miran dissented in favour of a 25bp cut. The other three dissenters, Hammack, Kashkari and Logan, voted to hold but opposed the inclusion of an “easing bias” in the statement, signalling they don’t think the committee should be telegraphing future cuts at all. The split is significant because it tells you the FOMC is genuinely divided on whether the war-driven energy shock is transitory or whether it will permanently embed in core inflation. In a separate development that surprised markets, Powell announced he will remain on the Fed Board of Governors after his chairmanship ends on the 15th May, citing concerns about the DOJ renovation probe being reopened. His governor term runs through to January 2028.

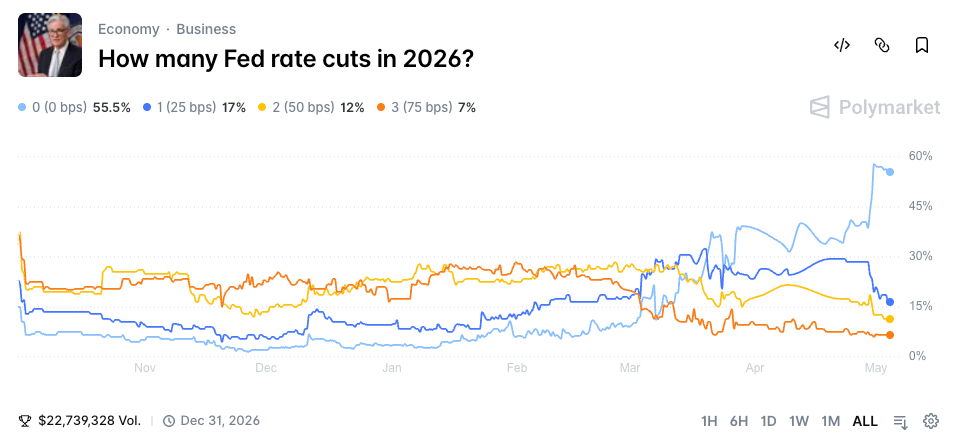

Kevin Warsh’s full Senate confirmation vote is expected the week of 11th May, meaning he will likely chair the June 16-17th FOMC. Importantly, Warsh will take Miran’s seat (not Powell’s), so the immediate dovish-hawkish balance on the committee won’t shift, Powell’s decision to stay effectively neutralises Trump’s ability to stack the Board further. Currently, interest rate futures expect the Federal Funds rate to remain unchanged in 2026, with a single 25bp cut in December 2027.

Source: Polymarket

The yield on the 10-year US Government Treasury has settled around 4.34%, up modestly on the week, while the 2-year Treasury yield has held near 4.00%. Despite the FOMC meeting being the dominant event, the rate market reaction was relatively muted. The dot plot wasn’t updated and the dissenters, while dramatic, didn’t change the policy rate. The bigger structural story being that markets continue to price zero cuts for 2026, with the first cut not expected until late 2027, a far cry from the two cuts that were priced in just before the war began. Powell’s decision to stay on as Governor pushes back the potential for the Committee to run more dovish under Warsh, since the Trump administration would prefer to replace him with someone more inclined toward lower rates. The next FOMC meeting is scheduled for June 16-17th, which will be Warsh’s first as Chair and will include updated SEP projections and a new dot plot – likely the most consequential meeting of the year. The April jobs report (released Friday) showed nonfarm payrolls of 178k with unemployment at 4.3%. Neither hot enough to trigger hawkish repricing nor weak enough to bring back cut expectations.

Source: TradingView (BTC/USD)

BTC ended the week at USD$78,711 (up 1.5%) with a Friday close above $78k for the third time in two weeks. The structural picture continues to strengthen even as price action consolidates. April spot Bitcoin ETF inflows hit $2.44B — the strongest monthly figure since October 2025, driven heavily by BlackRock’s IBIT. BTC exchange reserves have fallen to a 7-year low of approximately 2.69 million BTC, with 170,000 BTC moving off exchanges over the past six months as holders shift coins into self-custody and long-term storage. Whale wallets (1,000+ BTC) have grown by 142 addresses over six months to a total of 2,028 – a clean accumulation signal at the high end of the cohort. Tether posted a Q1 profit of USD$1.04B and now holds an USD$8.23B reserve buffer, demonstrating the durability of stablecoin issuer economics through volatile market conditions.

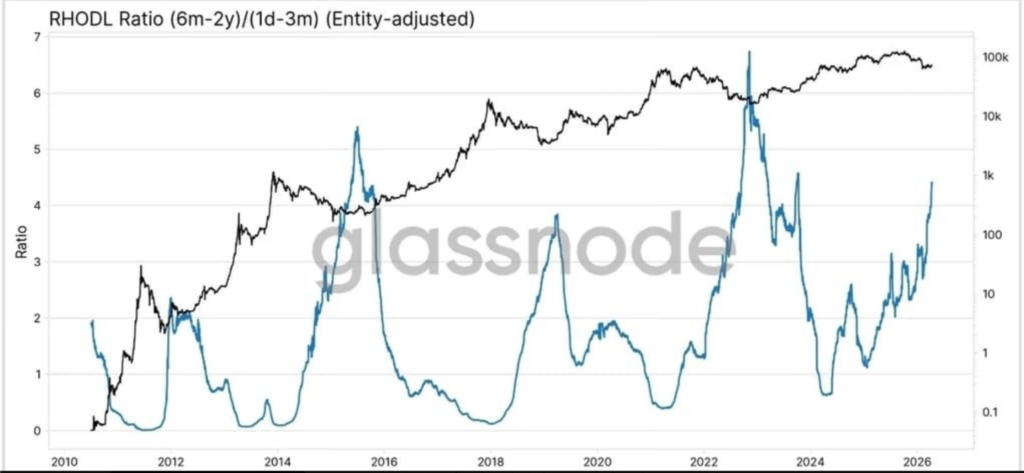

Source: Glassnode

The most striking on-chain signal continues to be Glassnode’s RHODL ratio at 4.5, the third-highest reading in BTC’s history. The only comparable prior readings were at the 2015 cycle bottom (5.0) and the 2022 cycle bottom (7.0), both of which were immediately followed by sustained bull markets.

This ratio measures the balance between coins owned by longer-term holders (those who’ve held for six months to three years) and coins belonging to newer, short-term participants (one day to three months). It helps reveal whether the market is being driven by experienced investors or by fresh speculative demand. When the ratio increases, it usually signals that coins are maturing in the hands of patient holders rather than new buyers flooding in. This pattern tends to appear following significant market downturns, as seen in 2015, 2019, and 2022.

ETH underperformed for the third consecutive week, drifting to USD$2,284 (-1.9% wk) and remaining capped by the persistent $2,400 resistance. ETH funding remains structurally negative across all major venues, reflecting weaker speculative demand and the BTC-led nature of this institutional cycle. The Ethereum Foundation hit its 70,000 ETH staking target via a USD$93m deposit during the week (a meaningful endorsement from inside the project), and Charles Schwab launched spot trading for BTC and ETH, opening a new institutional access channel. Aave V4 went live on mainnet, an important DeFi infrastructure milestone. The CLARITY Act yield compromise text was released Friday, blocking yield offerings that resemble bank deposits but allowing “bona fide” transactions, with Senate Banking Committee markup expected to follow. Standard Chartered cut its BTC year-end target to USD $150k (from USD$300k) citing slower-than-expected ETF absorption. The 2nd May mining difficulty adjustment dropped from 135.59T to ~131.43T, modestly easing miner economics and reducing forced selling pressure.

The broader market asymmetry remains: structural buying is meeting fearful sentiment. While the macro tailwind from ceasefire optimism is building, and the de-leveraged positioning leaves significant room for an upside squeeze if the USD$80k breakout finally clears. The downside scenario, which is a Hormuz re-escalation or a hawkish Warsh confirmation, has been repeatedly absorbed without breaking the USD$75k support that has held through five separate tests since mid-April.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

The past week marked a constructive consolidation phase across the digital asset complex, as a blockbuster Mag 7 earnings season validated AI hyperscaler capex narratives and provided a favourable backdrop that saw broader risk lift to new highs. Flow dynamics on the desk reflected a client base that is still inclined to ‘take profit’ on the recent rally rather than adding: volumes rebalanced materially toward concentration in Bitcoin (BTC) – which saw a net selling skew.

Asset breadth on the desk was the highest observed in some time, with significant two-way altcoin participation in size. Outlier long-tail names included Sonic (S) (which saw heavy net selling); Ripple (XRP) & Solana (SOL) (substantial buying interest) and fiat cross hedging between EUR/AUD.

In a week where flow generally skewed defensive, requests for PAXG remained surprisingly subdued – with interest continuing to fade as gold’s war premium unwinds and forward-looking optimism builds. Meanwhile, trade.xyz‘s SP500, XYZ100 and Oil (WTI/Brent) listings on Hyperliquid’s HIP-3 protocol have affirmed themselves as the currently favoured instruments for macro asset hedging within digital asset infrastructure.

These two-way dynamics suggest that despite the structurally constructive risk backdrop, crypto participation still remains relatively measured; with clients exhibiting a preference towards profit-taking and derisking into yield-bearing structures rather than incremental risk-on directional exposure.

Bitcoin (BTC) consolidated within its well-established range for the week, finding continued value in the USD$74k–80k zone that has anchored price action since the prior breakout. Ethereum (ETH) traded a similar pattern with a softer relative tone as the ETH/BTC cross drifted from 0.03012 BTC to 0.02956 BTC. While the Kelp DAO exploit has been nominally resolved with “DeFi United” – a coalition effort including Consensy, AAVE, LayerZero and more that has now raised over 132,000 ETH (USD$300M+) to restore full rsETH backing in a remarkable display of cross-protocol solidarity; residual sentiment drag still remains evident in the persistent weakness of the cross as ETH continues to digest the episode against a softer relative tape.

In FX, AUD/USD’s run as a leading G10 outperformer extended as the pair opened at 0.7131 and rallied to fresh four-year highs of 0.7228 around Friday’s New York open before closing the week at 0.7201. Wednesday’s headline CPI print of 4.6% confirmed significant oil-driven pass-through into Australia’s domestic inflation report. This week (Tuesday the 5th May at 2:30pm AEST), the Reserve Bank of Australia (RBA) will convene for their May interest rate meeting. Currently, short term futures project a circa 75% chance of a 25bp increase to the Australian cash rate.

Australia’s hawkish monetary policy stance is in divergence to the global backdrop, which saw the BoJ, BoC, ECB, and the FOMC (Powell’s final meeting) all hold rates this past week – a buoy of strength to the AUD/USD pair. On the desk, AUD buying interest has remained. In other pairs, USDC/USDT were primarily offramped to USD while EUR saw significant net selling. NZD and GBP pairs saw mixed participation.

Looking ahead to a packed local calendar: Tuesday’s RBA decision headlines, while on the fiscal policy side, pre-budget commentary surrounding material tax reforms to the CGT discount (potentially extended across all assets, not just property) and negative gearing shape the 12th May Federal Budget. The magnitude of the proposed fiscal changes introduces an additional layer of complexity to the domestic monetary policy equation that the RBA Board will need to weigh alongside the incoming data.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and altcoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Ben Mensah, Trading Analyst

Derivatives Desk

WHOLESALE INVESTORS ONLY

Derivatives markets traded in a relatively contained range this week, with positioning stabilising after the late-April volatility impulse. Aggregate BTC perpetual open interest held broadly steady, suggesting limited incremental leverage entering the system, while price action remained range-bound into the weekend. The absence of meaningful liquidation events points to a well-margined market, with positioning more balanced relative to the earlier dislocations seen through April.

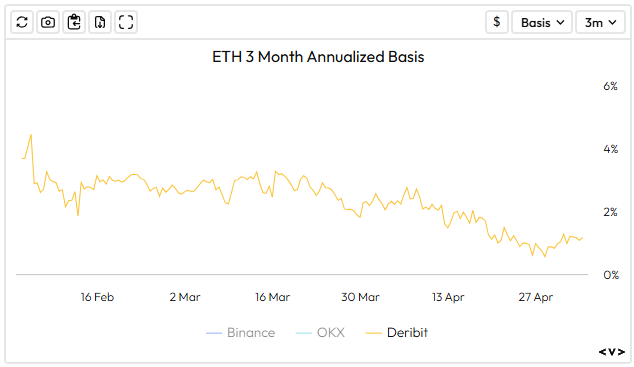

Funding dynamics remained soft throughout the week. BTC perpetual funding traded around flat (plus or minus), indicating a lack of sustained directional conviction and a slight bias toward short positioning at the margin. This contrasts with prior weeks where rallies were accompanied by more aggressive long positioning. ETH funding continued to underperform BTC, reinforcing the ongoing weakness in speculative demand for ETH relative to BTC and keeping the ETH/BTC cross under pressure (to currently trade circa 0.02950 BTC).

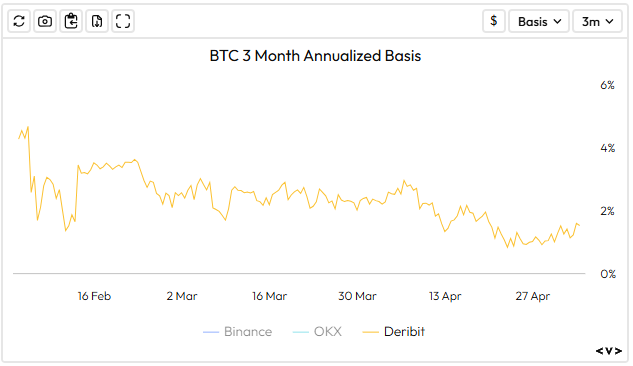

Volatility markets were generally offered. BTC front-end implied volatility drifted lower, with 1-week ATM trading down into the high-30s – relatively flat out to 1-month. The term structure flattened modestly as near-term event premium faded, suggesting reduced demand for short-dated hedging. Skew remains put-biased, (although now marginal), with demand for downside protection less pronounced than prior stress periods. ETH volatility tracked a similar path but maintained a relative premium to BTC, consistent with its higher beta and weaker spot structure.

From a technical perspective, BTC continues to consolidate within a well-defined range, with short term support holding in the mid-USD$70k region and resistance building into USD$80k. ETH remains more fragile, with rallies capped below key resistance and downside support levels being tested more frequently, consistent with the softer funding and volatility profile.

Crypto credit conditions remain stable. There are no visible signs of stress across lending or margin markets, with borrow demand largely functional and tied to liquidity management rather than directional leverage expansion. Haircuts and margin utilisation appear steady, and the lack of funding dislocations or liquidation cascades suggests the system is operating within normal risk parameters. Overall, the derivatives complex reflects a market that is balanced but lacking conviction, with positioning light and volatility subdued as participants await a clearer macro or crypto-native catalyst.

Source: Velo.xyz

What to Watch

Tues: RBA Interest Rate Decision

Wed: ISM Services PMI

FRI: US Non Farm Payrolls, US Unemployment Rate

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 9 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 1 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 25 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.