13 Apr, 26

Weekly Crypto Market Wrap: 13 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- Bitcoin spot ETFs recorded $22.34 million in net inflows last week, marking a significant recovery from the early-month stagnation.

- Coinbase Australia receives the AFSL licence. It can now offer crypto and equity perpetuals to Australians, followed by futures and options.

- Bhutan has sold approximately 70% of its Bitcoin holdings over the last 18 months, reducing its reserves from 13,000 BTC to just 3,954 BTC (worth ~$280 million).

- The HKMA issued its first two stablecoin licenses on April 10, 2026, to HSBC and Anchorpoint Financial (a Standard Chartered-led joint venture).

Technicals & Macro

Markets

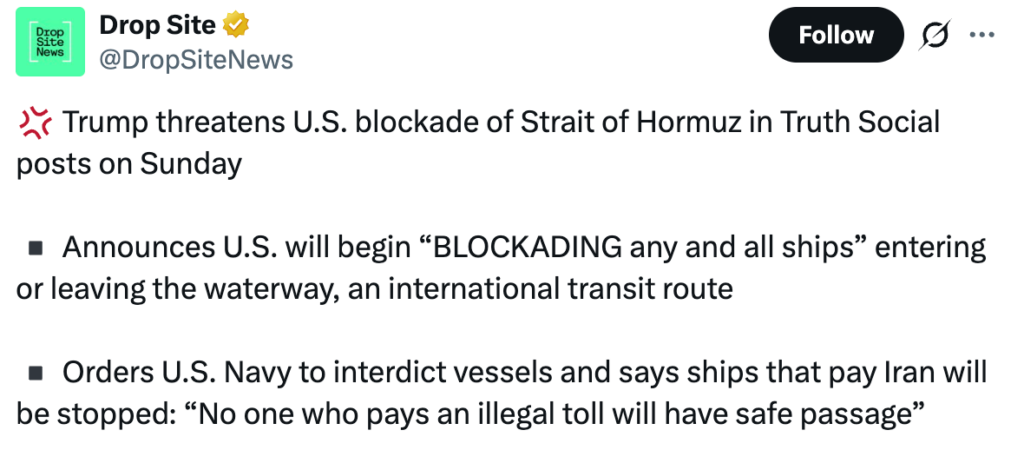

Two narratives collided last week. Through Friday, markets were riding the strongest ‘relief’ rally since November, that is, seven consecutive winning sessions for the S&P500 and the Nasdaq, as a fragile two-week US-Iran ceasefire held and markets began pricing a diplomatic resolution. Then, the weekend happened. VP Vance departed Islamabad without a deal after Iran demanded control of the Strait of Hormuz, war reparations, a Lebanon ceasefire and access to frozen assets (conditions the US rejected as non-starters). Trump responded Sunday by announcing a US naval blockade of the straits, targeting vessels entering or leaving Iranian ports.

Source: X.com @DropSiteNews

This immediately triggered a cross-asset reaction as Monday futures dropped over 1% across the board, and Brent surged 8% back above $103, erasing the prior week’s 12% oil decline in a single session. The ceasefire itself is technically still in place, but the blockade escalation has effectively killed any remaining optimism that a near-term deal was imminent.

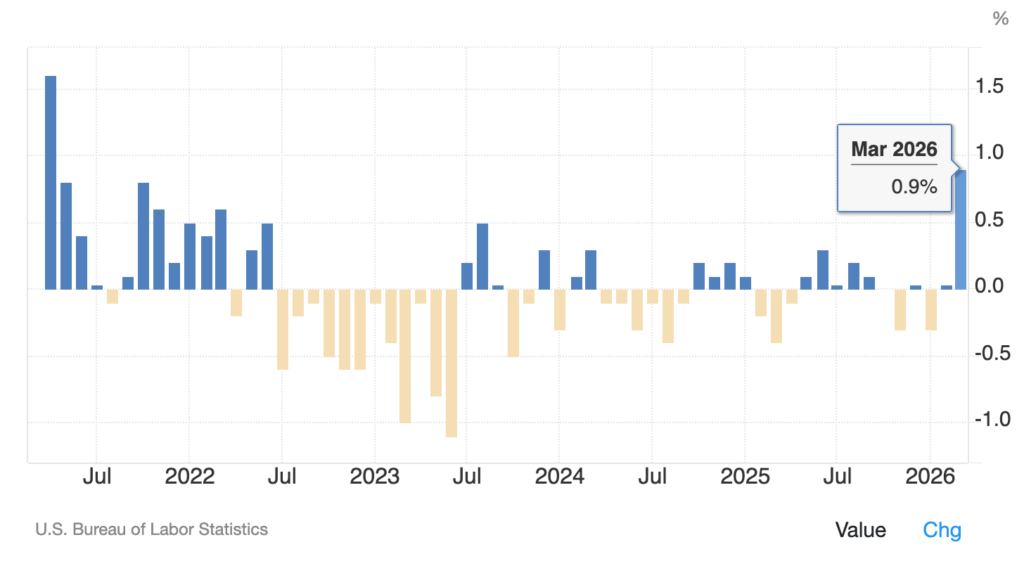

The macro data backdrop was mixed but nonetheless informative. March CPI showed the largest monthly increase in nearly 4 years, driven by the oil shock’s pass-through into energy, transport and food costs.

Markets had briefly been pricing in the possibility of a rate cut later this year during the ceasefire optimism, but that window looks to be closing again.

Source: Bloomberg

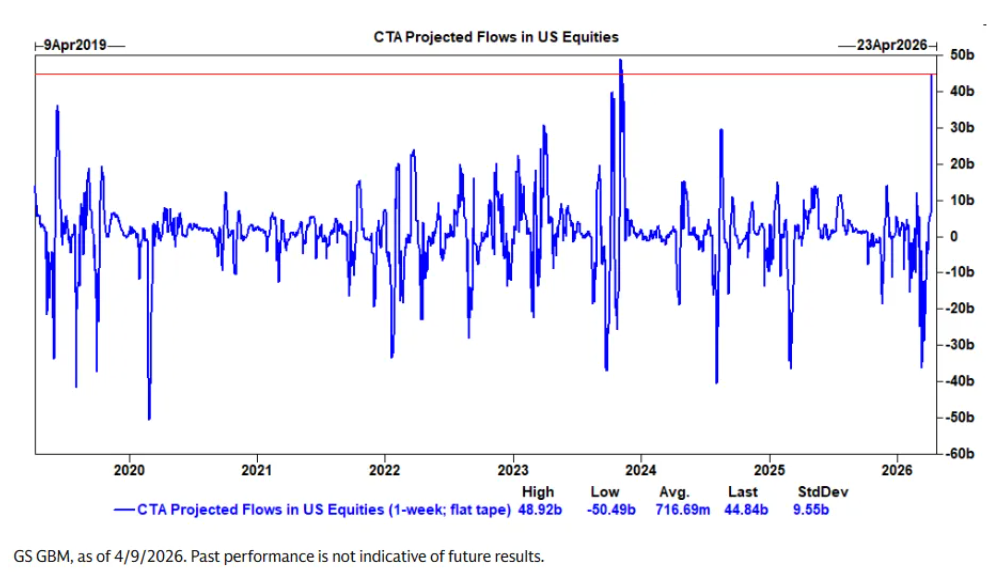

On positioning, desks like Goldman flagged a notable setup: commodity trading advisors (CTAs), the systematic, trend-following funds that trade futures based on momentum signals, are currently short approximately $30B of S&P 500 futures. That’s significant because CTAs generally don’t make discretionary calls; they follow price.

The five-week selloff triggered their algorithms to build a large short position, but the ceasefire rally has now pushed prices above several key momentum thresholds. Goldman’s model suggests that at current levels, CTAs could mechanically buy roughly $34B over the coming week as they cover shorts and flip back to net long, essentially forced buying that would amplify any further upside. It’s a technical tailwind sitting in the background, ready to fire if the market can hold these levels through the blockade noise.

Source: TigerTrade

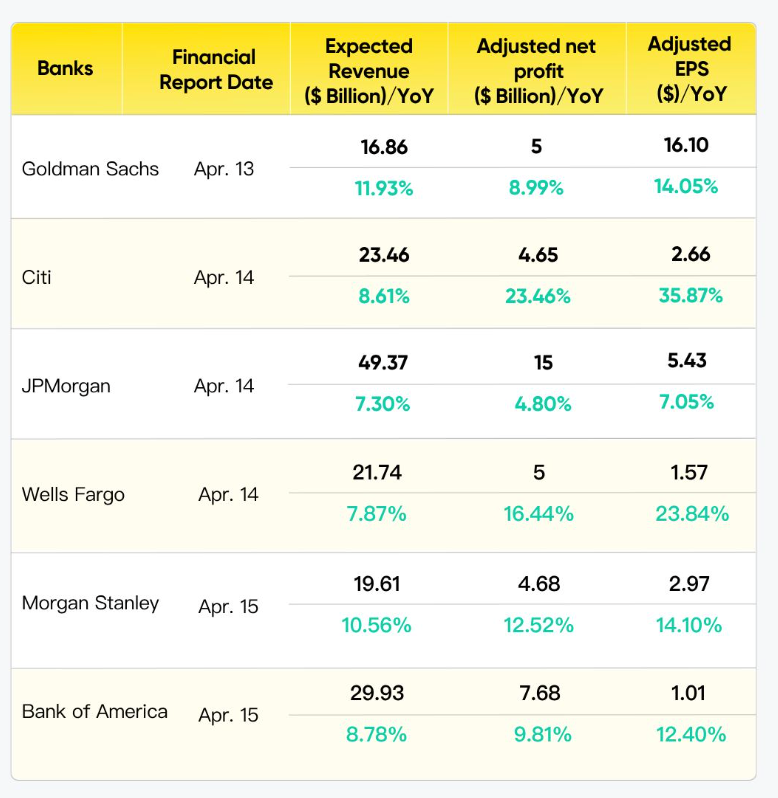

Q1 earnings season begins in earnest this week with Goldman Sachs, JPMorgan, Citigroup, Wells Fargo, Morgan Stanley and Bank of America all reporting. These earnings will show the real corporate test of the war’s impact on margins, credit quality and guidance.

Source: BusinessInsider

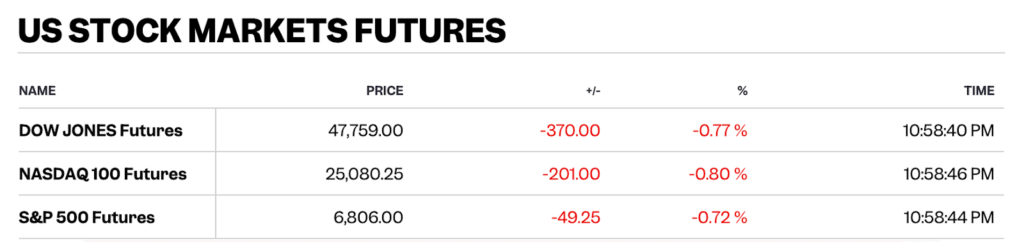

As mentioned, last week U.S. equities saw their best performance since November. The Nasdaq surged 4.7% to USD$22,903, which was mainly semiconductor led (Broadcom +4.7%, Nvidia +2.6% on Friday alone). The Dow added 3.0% and turned positive for 2026 again. Financial stocks underperformed ahead of this week’s earnings deluge. The key stat from the rally: the S&P 500 rode a 7-day winning streak into Friday, its longest since October.

However with Monday’s pre-market reversal, futures down ~1%, threatens to unwind a meaningful portion of these gains at the open.

Source: TradingView

The bond markets declined modestly during the ceasefire-driven rally, with the US10Y settling at 4.32% on Friday, down from 4.44% war-highs. The VIX collapsed to 19.23, its first close below 20 since early March, potentially signalling pricing in de-escalation. However we might expect volatility to rock again as that positioning is yet again exposed with Monday’s blockade announcement likely pushing yields higher on renewed inflation fears and reprice the vol. surface. Markets are still pricing zero rate cuts for 2026 in the base case, with the first full cut not expected until 2027 in several term-structures. Powell’s term is expiring next month on May 15, with the transition to Warsh adding another layer of uncertainty.

Source: Reuters

Oil was a two-fold story within the last 72 hours. Brent fell as low as USD$96 on Friday (lowest since early March) as traders priced ceasefire optimism and the prospect of Hormuz reopening. Iran was even reported to be considering a transit fee system rather than outright closure. Then the blockade announcement sent Brent flying back up 8% on Monday to around USD$103, with WTI trekking back toward USD$96. Saudi Arabia confirmed reduced pipeline and production capacity, making the supply picture even more constrained.

Source: TradingView

The dollar weakened materially during the ceasefire rally. The DXY broke below the key 98.68/76 pivot zone, which is a level that had acted as support since mid-2025, briefly touching the yearly open at 98.23 before stabilising around 98.7. Monday’s blockade reversal will likely bid the USD higher again, testing whether the DXY breakdown was genuine or just a ceasefire-driven head fake.

Crypto

Crypto held firm this week and notably showed meaningful resilience in the face of the kind of headline risk that would have triggered a violent flush in prior cycles. BTC held comfortably above USD$70k through the ceasefire rally, and critically, not breaking down on Monday’s blockade announcement. While S&P 500 futures dropped over 0.9% and Dow futures fell 1%, BTC pulled back just 2.7% and held the USD$69k level, a considerably more contained reaction than equities given the magnitude of the geopolitical shock. The relative composure is worth flagging: in March, every escalation headline sent BTC and ETH sharply lower in lockstep with equities. At the moment we see the asset class is absorbing bad news without breaking structure.

BTC’s range also has quietly shifted higher over the past fortnight from USD$63k–USD$70k to USD$68k–$USD73k, and USD$73k resistance remains the key level to watch. A confirmed Hormuz reopening would likely be the catalyst to break through it, while the downside has repeatedly found support around USD$68k–USD$69k, a floor that is tightening with each test.

Our take is that the risk-reward setup heading into this week’s bank earnings is constructive: crypto has already priced in a prolonged conflict and is trading near range support, meaning any positive surprise or tailwinds around de-escalation has room to run, while further deterioration has been largely absorbed.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

Global markets were dominated by rapid shifts in geopolitical risk tied to developments between the U.S. and Iran, driving sharp rotation across asset classes. Early in the week, equities showed resilience despite escalating tensions, while oil was bid higher as participants balanced the threat of supply disruption in the Strait of Hormuz against hopes for a diplomatic resolution.

The tone shifted decisively midweek following the announcement of a two-week ceasefire which triggered a broader risk-on move. Oil prices fell sharply from USD 117.62/barrel to 91.05 as the geopolitical premium unwound. Equities rallied strongly, and volatility compressed. AUD/USD moved higher while crypto markets began to recover, albeit with some initial hesitation relative to equities.

Into the latter part of the week markets were well supported by the ceasefire backdrop, although momentum moderated ahead of critical U.S. inflation data. Equities were bid at a slower pace, oil held strong in the high 90’s and AUD remained supported above USD 0.70. Attention increasingly shifted toward macro fundamentals, particularly inflation, as market participants questioned whether the rally could be sustained beyond the immediate geopolitical relief.

That optimism proved to be short-lived heading into the new week, as ceasefire talks broke down over the weekend reigniting fears of supply disruption and pushing oil prices sharply higher once again. Risk assets reversed course with equities coming under pressure and AUD/USD weakening amid renewed USD strength. A stronger than expected U.S. CPI print added further strain, reinforcing stagflation concerns and complicating the Federal Reserve’s policy outlook. The week highlighted just how fragile market sentiment remains, with geopolitical developments continuing to dominate direction while macro data increasingly constrains the durability of risk on rallies.

On the desk, flows across majors were more selective this week, with ETH and SOL seeing stronger bid-side interest while BTC lagged, trading with a slight skew to the offer. SOL in particular attracted significant demand from clients, while activity across the broader altcoin complex remained relatively subdued in comparison. In stablecoins, USDT flows were firmly skewed on the offer with significant net outflows into both crypto and USD. AUDD also caught some sell side pressure, although activity was relatively light. USDT/AUD remained the most commonly traded pair last week, with AUD experiencing net selling pressure characterised by higher frequency, lower volume tickets. Across other currencies, EUR was also offered while NZD stood out attracting steady inflows.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and altcoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Oliver Davis, OTC Trader

Derivatives Desk

WHOLESALE INVESTORS ONLY

Derivatives markets moved through two distinct phases this week. The first half saw a continuation of the post-March 27 quarterly expiry clean-up, with open interest drifting lower and positioning resetting after the $14B BTC notional options expiry. The ceasefire rally then drew fresh speculative length back into the market, with aggregated BTC perp open interest stabilising in the $28-30B range after bottoming near $26B in late March. The seven-day equity winning streak pulled risk appetite higher across the complex, but then Friday’s softening and Monday’s Hormuz blockade headline risk have immediately tested that rebuilt positioning.

Interestingly, liquidation cascades have been notably absent relative to March, a sign that leverage flush did its job and the current participant base is now better margined.

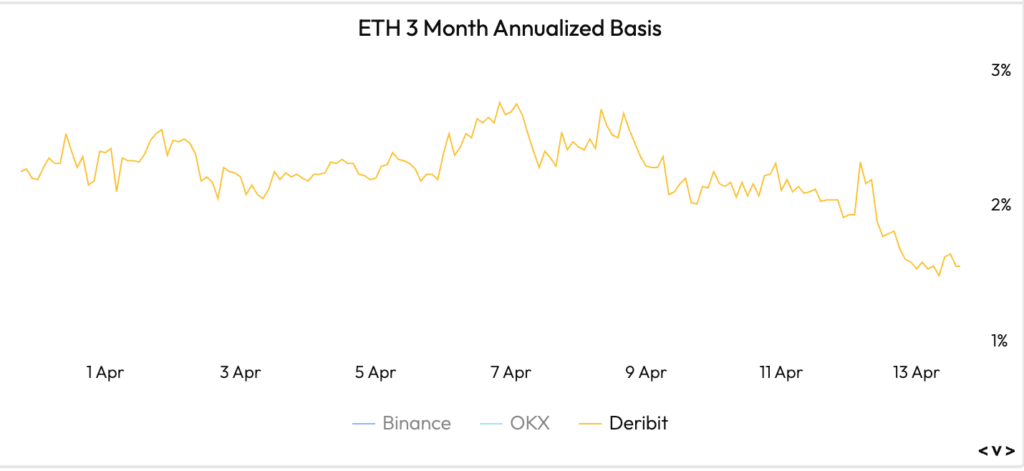

Funding dynamics shifted meaningfully through the week. BTC perp funding turned mildly positive mid-week as the ceasefire rally drew in long interest (the first sustained positive print since early March). However, funding flipped back in speed toward neutral-negative into Monday’s session as the blockade news triggered defensive positioning. ETH funding stayed structurally softer throughout, reinforcing the persistence underperformance in ETH (and the broader alts complex) speculative demand versus BTC. The ETH/BTC ratio remains under pressure.

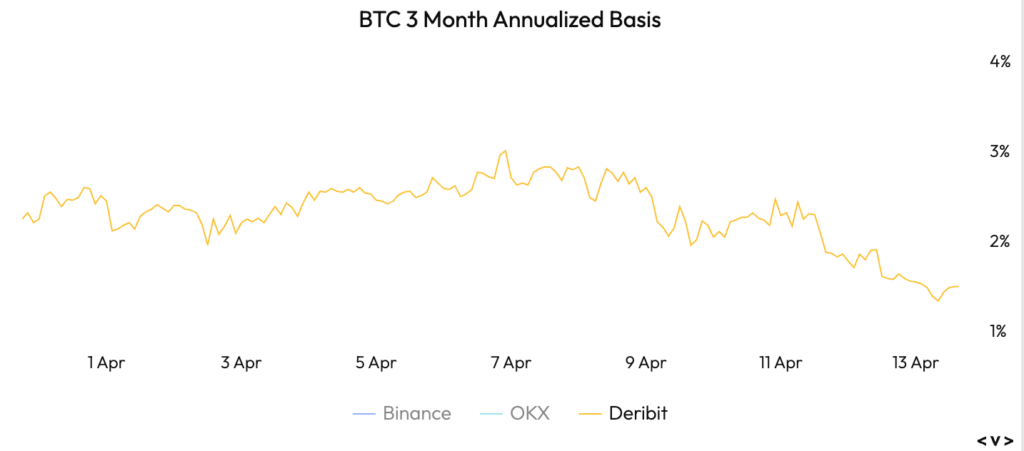

Volatility repriced sharply through the week. BTC ATM implied vols compressed into the high 40s on 1W during ceasefire optimism (the lowest since February) – before kicking back to the previous week’s levels of low to mid 50s on Monday’s escalation news. The curve has steepened modestly, with front-end vols now carrying a geopolitical premium relative to the 1-3M tenors that remain in the low-50s. Skew still remains put leaning but has normalised from March extremes.

The options term structures carries a notable kink around the April 25 monthly expiry, where open interest has been rebuilding post the March 27 roll. Dealers appear short gamma in the $68k-$72k range, meaning that moves in either direction through those strikes would be mechanically amplified by hedging activity, a setup that favours a breakout over continued range trading if a catalyst arrives (such as a ceasefire confirmation or escalation).

Positively, crypto credit remains stable with no indication of dress signals. Haircuts are flat, margin utilisation is well within normal ranges, and borrow demand continues to be dominated by BTC/ETH collateralised lending for liquidity recycling rather than leverage expansion. The absence of margin stress during Monday’s blockade sell-off (despite a 2.7% BTC move) is a notable contrast to the previous March episodes where smaller moves triggered cascading liquidations. Overall, the derivatives complex reflects a market that has de-risked, absorbed headline news, and is now coiling for directional move. The question is now which catalyst breaks it out.

Source: Velo.xyz

This Week’s Trade Idea – BTC Yield Entry Notes

BTC’s tightening into a $68k-$73k range and the current put skew create a compelling setup for Yield Entry Notes. This strategy monetises the elevated cost of downside protection by selling puts at levels where the desk sees structural support.

Yield Entry Note sample terms:

For a 1-month BTC Yield Entry Note with a $60,000 strike price, one can generate approximately 2.15% yield (~29.3% annualised). The premium has widened modestly versus the prior week due to Monday’s vol reprice, making entry more attractive. There are two possible outcomes at expiry:

- BTC expires above $60k: investment paid back in cash + earns ~2.15% yield (~29.3% annualised, paid in cash).

- BTC expires below $60k: investment used to buy BTC at $60k + earns ~2.15% yield (~29.3% annualised, paid in BTC).

The strike sits roughly 15% below spot, at a level that has not been breached since the initial war-shock lows in early March and now sits below the range that has held through six weeks of conflict escalation.

Risk Considerations:

- Even if BTC was to trade below the strike on expiry, you would buy at the strike. This exposes the position to larger downside moves (short gamma and short convexity).

- In stressed conditions, liquidity in downside strikes can reduce, increasing hedge slippage and exit costs.

- The trade is most attractive for investors who would be comfortable owning BTC at the $60k level regardless.

Please contact the derivatives desk for refreshed pricing.

Emir Ibrahim, Analyst

What to Watch

Tue 14 Apr: US PPI (Mar) — Pipeline inflation read. Consensus +1.2% MoM (prior +0.7%). Hot print reinforces higher-for-longer Fed, extends USD strength, adds fuel to the stagflation trade.

Thu 16 Apr: China Q1 GDP + Industrial Production + Retail Sales — Major AUD proxy. GDP consensus 4.7% YoY (prior 4.5%). A beat supports the China complex and lifts AUD and commodities; Industrial Production (consensus 5.9%) and Retail Sales (consensus 2.4%) round out the demand picture.Thu 16 Apr: AU Labour Force (Mar) — Domestic centrepiece. Consensus ~+15k jobs, unemployment 4.3%. Weak print pressures AUD; tight read keeps May on hold.

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 27 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.