27 Apr, 26

Weekly Crypto Market Wrap: 27 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

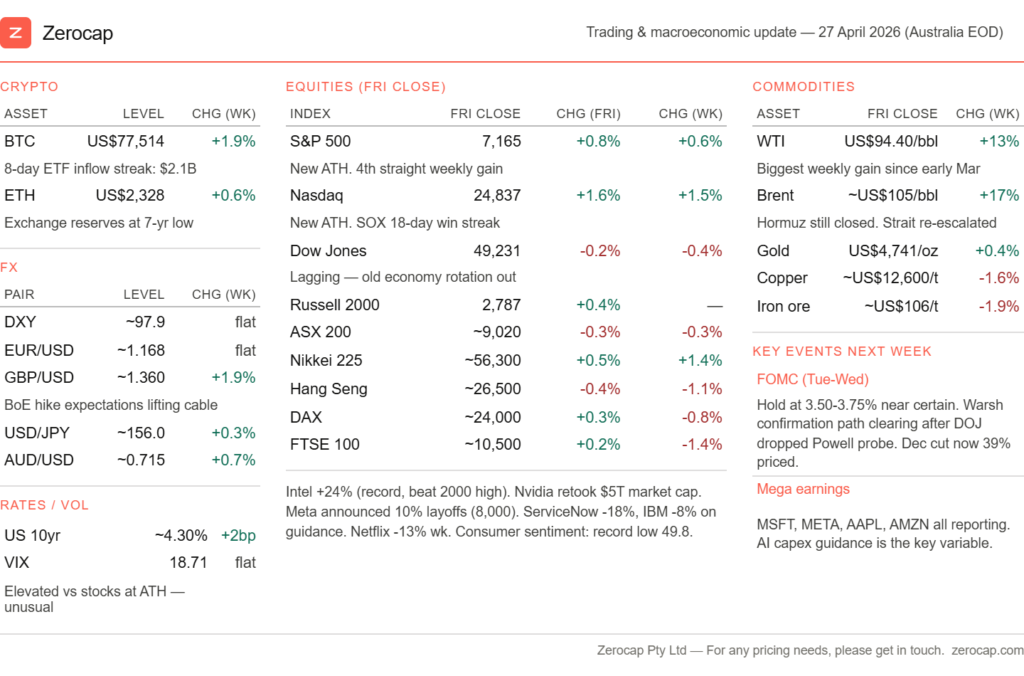

Week in Review

- U.S. spot BTC ETFs saw ~US823M in inflows; ETH ETFs added ~US$276M

- Michael Saylor’s Strategy buys 34,164 bitcoin for $2.5 billion as total holdings top 800,000 BTC

- Aave proposes 25,000 ETH contribution to DeFi United to plug Kelp DAO exploit hole

- Tether freezes $344 million in USDT on Tron after wallets flagged by US authorities

- Ethereum Foundation sells nearly $24 million of ETH to Tom Lee’s Bitmine

Technicals & Macro

Markets

A week of contradictions. The S&P 500 and Nasdaq closed at new all-time highs on Friday, powered by a semiconductor supercycle that has now produced 18 consecutive daily gains in the SOX index, the longest streak on record. Yet oil surged 13–17% on the week as the Strait of Hormuz re-escalated, consumer sentiment hit a record low of 49.8 (below readings during the GFC, COVID and the post-Ukraine inflation spike), and the VIX remained elevated near 19 even as stocks hit records, a divergence that typically signals the options market is pricing tail risk that the equity surface hasn’t yet reflected.

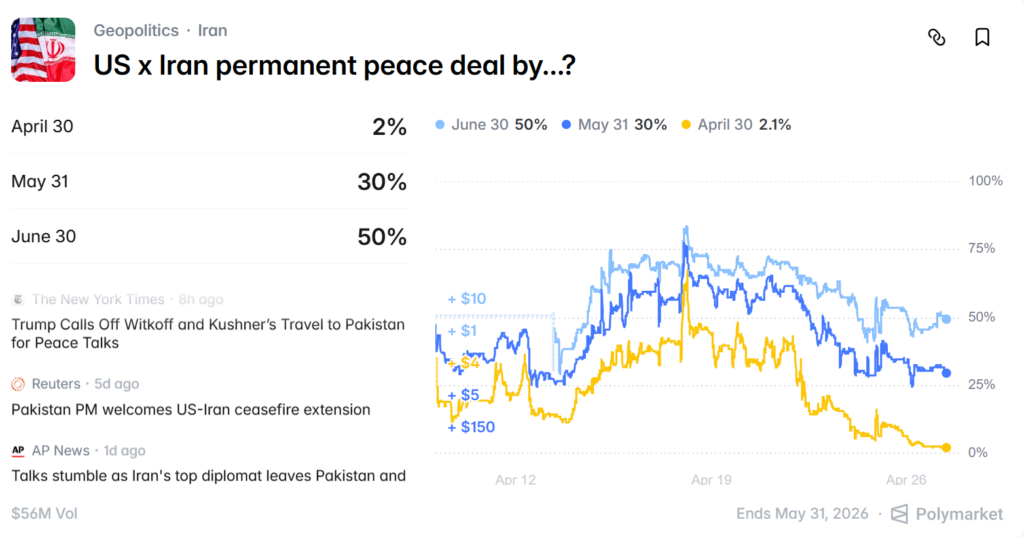

Source: Polymarket

The headline narrative was ceasefire diplomacy: Trump extended the Israel-Lebanon ceasefire by three weeks on Thursday and sent envoys Witkoff and Kushner to Islamabad on Saturday for Pakistan-mediated talks with Iran. But Iran’s Foreign Minister Araghchi left Islamabad on Sunday without meeting US officials, and Trump ordered a halt to negotiations, sending oil futures higher and US equity futures lower into Monday’s open. The ceasefire remains technically in place but is indefinitely extended rather than time-bound, and the US naval blockade of Iranian ports continues. The diplomatic channel exists but isn’t producing results.

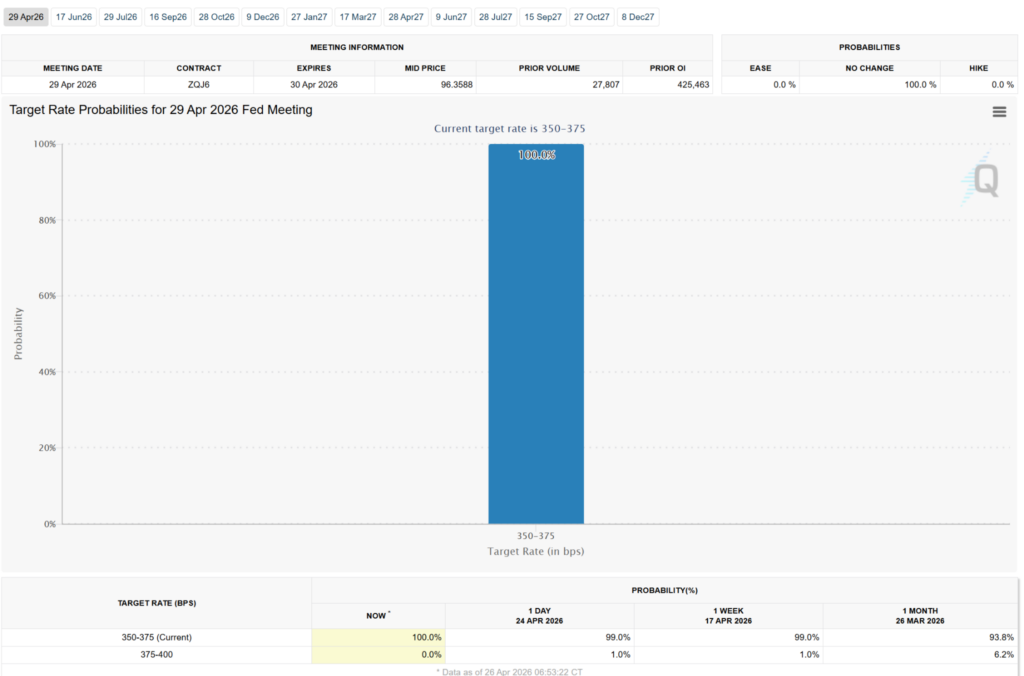

On the institutional side, the DOJ dropped its criminal investigation into Fed Chair Powell on Friday, clearing a significant obstacle to Kevin Warsh’s confirmation as the next Fed Chair. Markets are now pricing a 39% chance of a 25bp cut by December, up from 23% the prior session, it’s still a long way from certainty, but the first meaningful repricing toward easing since the war began. The FOMC meets Tuesday–Wednesday this week, with a hold at 3.50–3.75% near certain.

Source: LSEG

The real event risk is in the statement language and Powell’s final press conference before Warsh takes over. Q1 earnings season has been strong. Aggregate S&P 500 earnings growth is now tracking 16.1%, up from 14.4% at the start of April but the week ahead is the real test where MAG7 names report: Microsoft, Meta, Apple, and Amazon. The companies are worth nearly $16 trillion combined, representing a quarter of the S&P 500 Index’s market capitalization. AI capex guidance will determine whether the semiconductor rally has fundamental backing or has gotten ahead of itself.

Source: FedWatch

Yields held steady as the FOMC meeting approached, with the 10-year around 4.30%. The rate path repriced modestly: markets now assign 39% probability to a 25bp cut by December, up from 23% , driven partly by the DOJ closing its Powell probe (which clears the Warsh succession path) and partly by expectations that oil normalisation, if it materialises, would give the Fed room to ease in H2. The FOMC will almost certainly hold this week, but the statement will be parsed for any shift in the balance of risks language, particularly whether the committee explicitly acknowledges the war’s inflationary impact or continues to treat it as a supply-side shock that will resolve. The longer-run neutral rate at 3.1% remains the anchor for the long end, and any revision there would be the most consequential outcome.

Source: TradingView

The DXY held near 97.9, consolidating after its April decline from above 100. DXY is currently testing an inflection point after a sharp recovery from Jan lows. The key story was sterling, which rallied to approximately 1.36 as BoE rate hike expectations firmed, markets now price 22bp of hikes by year-end, which would put the BoE above the Fed and erode a key structural USD support. A hawkish hold from the Fed could see the dollar challenge recent highs particularly if GDP data surprises on the upside. This week the FOMC meeting and BoE decision (April 30) on consecutive days may create a compressed window of FX event risk on GBP/USD.

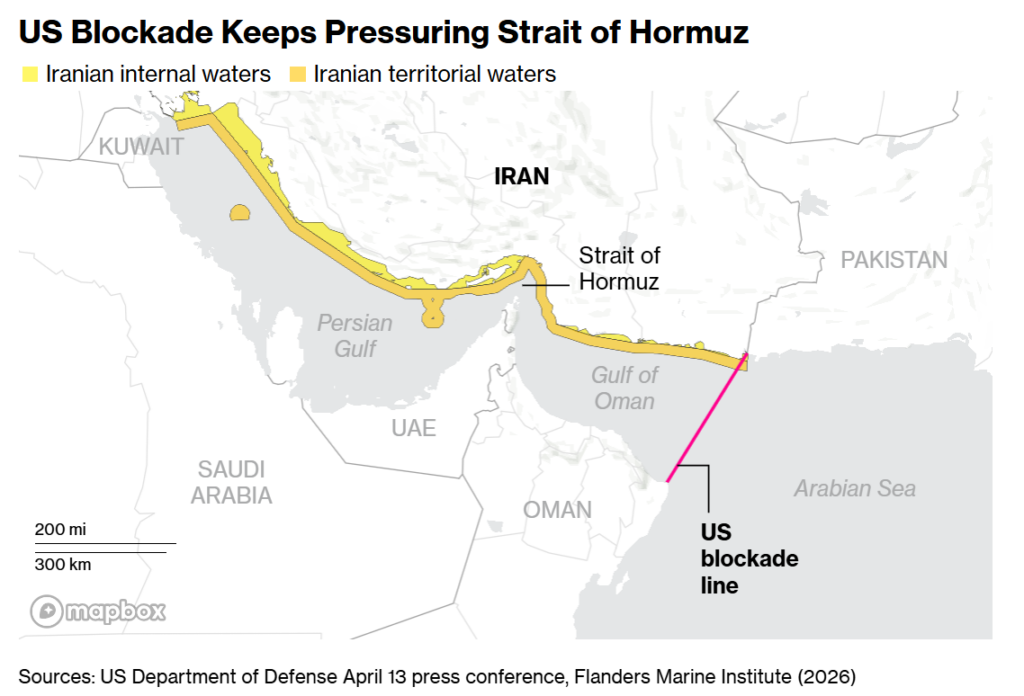

Oil re-escalated sharply. WTI surged 13% on the week to $94.40, which is its biggest weekly gain since early March, while Brent jumped approximately 17% to around $105. The Strait of Hormuz remains effectively closed despite Friday’s brief optimism around the Pakistan talks. Trump ordered the US Navy to “shoot and kill” vessels laying mines in the Strait on Thursday, and US forces boarded a sanctioned Iranian supertanker in the Indian Ocean. The diplomatic channel that briefly opened with Pakistan-mediated talks collapsed over the weekend when Iran’s FM left Islamabad without meeting US officials and Trump halted negotiations mic where if oil rebounds sharply, the cuts may get priced back out.

Source: TradingView (BTC/USD)

BTC consolidated near $77,500 after the prior week’s breakout, holding above the $76k level that was resistance for seven weeks and is now acting as support.

Volume actually gives the move a quietly bullish look. The February dump came with a major capitulation-style volume spike, which often marks forced selling exhaustion, and since then BTC has been grinding higher from the $62k–$63k lows with improving structure, higher lows, and a steady reclaim toward the $79k–$80k area. The only caveat is that the recovery volume has been relatively muted, so this is not yet a full “all clear” breakout, but that can also be interpreted positively. Sellers have not been able to push BTC back down despite lower participation, suggesting supply is drying up. As long as BTC holds above $77k, the recovery remains constructive, and a daily close above $80k–$82k, especially if accompanied by even a modest volume pickup, would likely confirm continuation toward $86k–$90k, with $96k as the next major level.

Overall, the chart looks like a base has formed, the February capitulation has been absorbed, and BTC is now trying to transition from recovery mode into bullish continuation.

The structural story continues to strengthen underneath: US spot Bitcoin ETFs logged their eighth consecutive day of net inflows through April 23, totalling $2.1 billion over the streak, with cumulative inflows since launch reaching $58 billion and total assets crossing $102 billion.

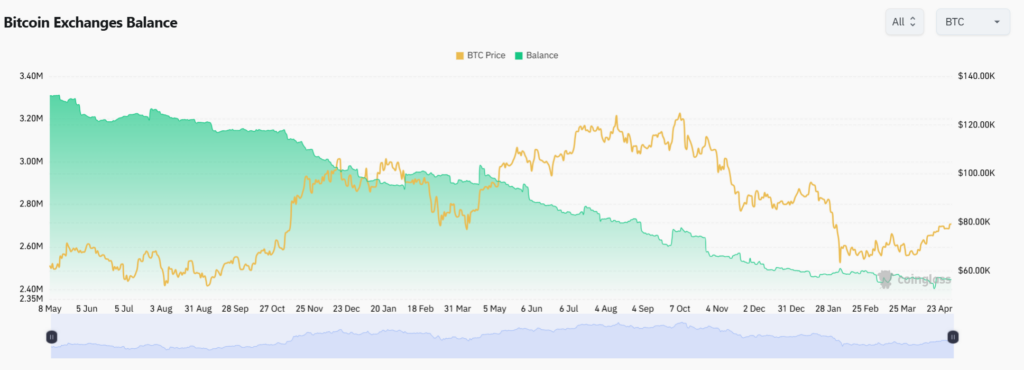

Source: CoinGlass

On the supply side, BTC exchange reserves have fallen to a seven-year low, which is a historically bullish signal indicating that coins are moving into long-term storage and off-exchange wallets rather than positioning for sale.

The Crypto Fear & Greed Index sits at 39 (“Fear”), an unusual reading given BTC is trading near two-month highs and equities are at all-time highs. The divergence between price, institutional flows, and sentiment mirrors the VIX/equity divergence in traditional markets: something under the surface isn’t aligned, and the FOMC meeting and mega-cap earnings this week could be the catalyst that resolves it in either direction.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

Market conditions over the past week were firmly macro driven and highly sensitive to geopolitical developments in the Strait of Hormuz, driving intermittent volatility across asset classes. Early into last week, Friday’s (April 17) strong session faded quickly with equities pulling back from record highs, while oil rebounded as the supply disruption premium resurfaced. Despite the escalation, broader risk sentiment remained relatively stable with markets showing willingness to absorb negative developments as attention turned to potential negotiations.

Into the latter part of the week, sentiment quickly turned increasingly unstable as conflicting headlines around the negotiations and regional security drove sharp intraday reversals. Early optimism around a potential U.S. – Iran breakthrough briefly pressured oil lower and lifted risk assets; crude oil ultimately held onto most of its gains. At the same time, strong PMI data and hawkish inflation components pushed yields higher and reinforced expectations of a prolonged FED hold. Gold sold off (-2.37%), failing to benefit from geopolitical risks as higher yields capped upside, while BTC (+6.58%) made new local highs and is trading around US 78,700.

In FX, AUD opened the trading week at US $0.7122 with firmer USD conditions and geopolitical uncertainty supporting the Dollar. Price action was largely traded rangebound through the week (0.7122/0.7178) with the exception of some quick excursions outside this range driven by macro headlines. For the Aussie Dollar, attention turns to critical inflation data on Wednesday with some particularly large forecasts:

Source: Trading Economics

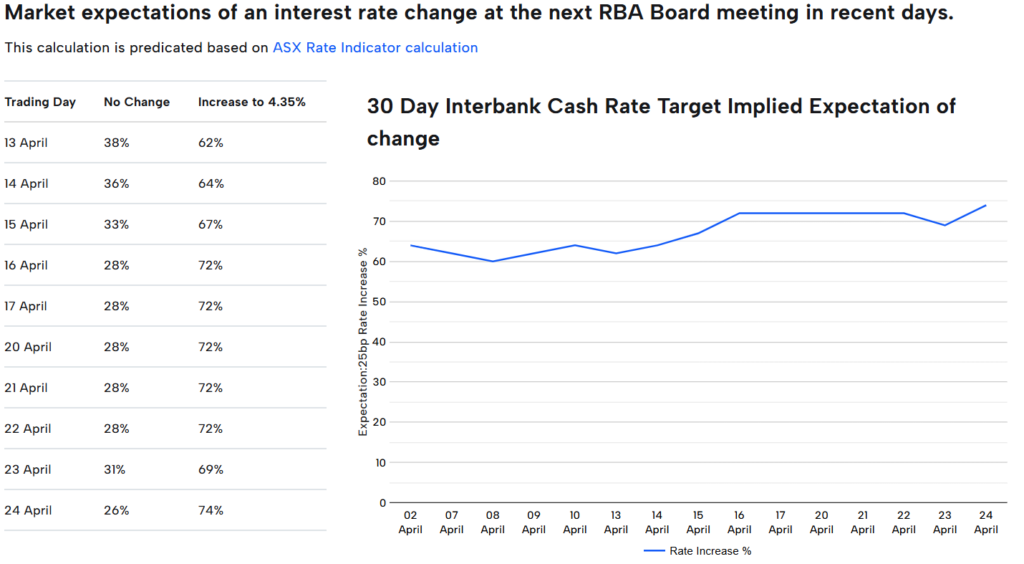

With inflation expectations notably elevated, there is the potential for a meaningful repricing in AUD volatility, particularly with the next RBA interest rate decision around the corner on May 5. Any material surprises in the print is likely to swing rate expectations – currently pricing a 74% chance that there will be a 25 basis point hike to 4.35% – and act as the key driver of near term AUD direction.

Source: https://www.asx.com.au/

On the desk, crypto flows were largely concentrated in the majors. SOL attracted strong bid-side demand while BTC traded with a skew towards the offer. ETH was broadly neutral. In the altcoins, PAXG saw some light sell side pressure consistent with subdued gold demand. Stablecoins were largely one directional on the desk last week – we noticed significant offramping activity in both USDT/USD and USDC/USD. AUDD remained traded at consistent frequency, widely rotated into AUD.

In FX, our AUD book was more balanced this week characterised by lower volume, higher frequency sales, and higher volume, lower frequency buys. Consistent with the significant offramping demand in USDT and USDC, USD saw substantial interest last week. EUR flows remained broadly consistent, while GBP activity was minimal. NZD saw relatively significant demand.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and altcoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Oliver Davis, OTC Trader

Derivatives Desk

WHOLESALE INVESTORS ONLY

Derivatives markets entered a transition phase this week as the April 24 $7.9B BTC options expiry passed and spot stalled below the psychologically significant $80k level. The expiry was the largest since December and concentrated around two poles: $75k calls (~$395m in OI, acting as the primary upside magnet) and $62k puts (~$330m, the main downside hedge). Max pain sat at $71k, well below spot, meaning the expiry was net positive for bulls who had positioned early. The rollover was orderly, with dealers closing out April structures and rolling into May and June tenors without forcing a significant spot move. Post-expiry, aggregated BTC open interest fell over 6% in 24 hours to 744.3k BTC, the sharpest single-day decline since the March 27 quarterly. This is a clear sign of leverage unwinding as price pulled back from Wednesday’s failed $80k breakout attempt.

Funding rates flipped back to negative across most major exchanges after briefly turning positive during the mid-April ceasefire rally. The negative print is significant, it means shorts are once again the dominant side of perpetual contracts, paying longs to hold their positions. This is the same setup that preceded both the March 27 short squeeze and the April 18 Hormuz rally, where $762m in liquidations (95% shorts) were triggered. The implication is clear: there is a meaningful pool of short positioning that could be violently unwound if a catalyst arrives (FOMC, ceasefire deal, mega-cap earnings beat). ETH funding remains structurally weaker than BTC, rates below -0.01%, consistent with the persistent ETH and broader altcoin complex underperformance on the speculative demand side.

Implied volatility has compressed materially. BTC’s 30-day implied vol index (Deribit BVIV) dropped to 42% (the lowest since January 31) while ETH’s equivalent dipped below 65%, also the lowest since early February. The vol compression is notable because it’s occurring while geopolitical headline risk remains elevated and the FOMC meeting is 48 hours away. The market is effectively pricing that the next move will be range-bound, which is historically the point at which vol sellers get caught. Skew remains put-leaning across all tenors, with risk reversals showing persistent demand for downside protection. The put bias has normalised from the March extremes but hasn’t flipped to calls despite spot being up 18% from the war lows.

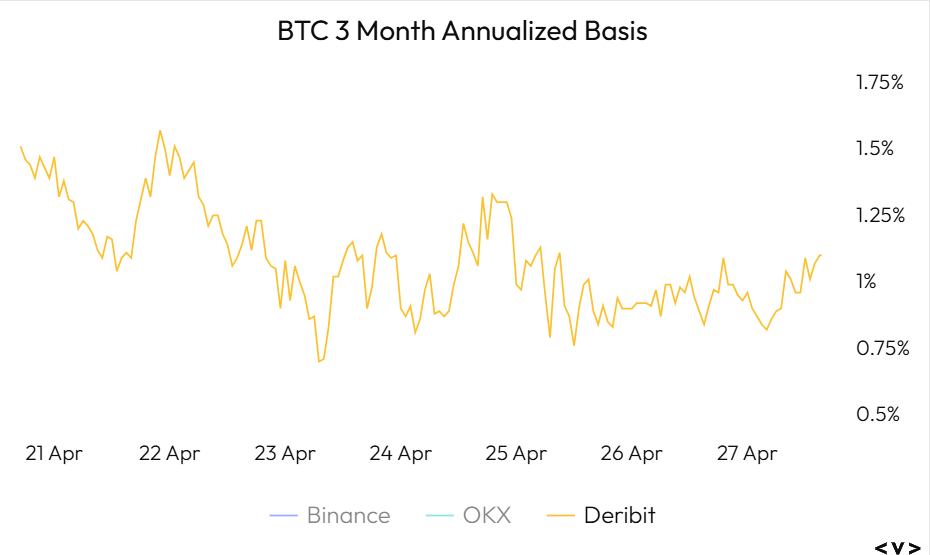

Source: Velo.xyz

The 3-month annualised basis remains compressed near 1%, offering essentially no carry incentive relative to the risk-free rate. At these levels, cash-and-carry institutional participants have little reason to add basis exposure, and the futures curve is signalling that the market sees limited asymmetry over the next quarter. This reinforces the de-leveraged nature of the current environment, there is very little speculative length to shake out, which paradoxically makes the setup more constructive for a move higher on a catalyst.

Emir Ibrahim, Analyst

What to Watch

Tues: BoJ Interest Rate

Thurs: FOMC meeting, US Core PCE Price Index MoM, US GDP QoQ

FRI: US ISM manufacturing PMI

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 22 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.