20 Apr, 26

Weekly Crypto Market Wrap: 20 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- U.S. spot BTC ETFs saw ~US$996M in inflows; ETH ETFs added ~US$276M.

- Polymarket explores a US$400M raise at a US$15B valuation.

- Kelp DAO exploit compromises ~US$292M in rsETH; AAVE sees lending market stress and ~US$6B in outflows.

- Drift secures up to US$127M from Tether for user recovery; shifts from USDC to USDT.

- Hyperliquid HIP-3 open interest surpasses US$2B as demand for 24/7 tokenized equity and commodity exposure accelerates.

Technicals & Macro

Markets

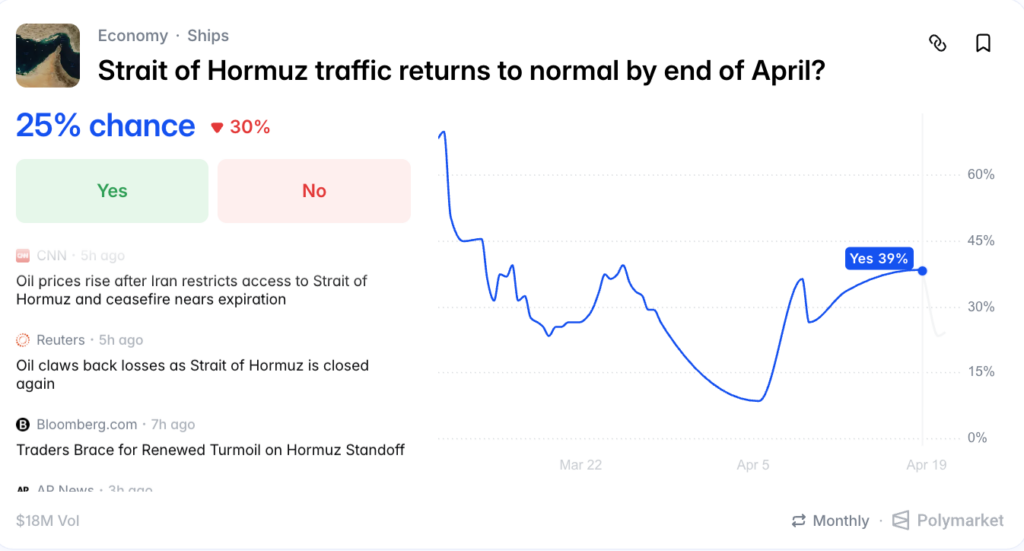

The war trade unwind arrived on Friday, and then Saturday tried to take it back. Iran’s Foreign Minister Aragchi declared the Strait of Hormuz “completely open” for all commercial vessels for the duration of the Israel-Lebannon ceasefire, and Trump quickly confirmed on Truth Social that the Strait was “completely open and ready for business”.

In an immediate response, oil crashed 10%, equities surged to new all-time highs, and the entire geopolitical risk premium that has been embedded in every asset class for these last seven weeks have begun to reprice in a matter of hours. Then on Saturday morning, Iran reversed course, reinstated “strict control” of the waterway and the IGRC attacked a tanker near the Strait – all within 12 hours of the initial announcement. Trump said Iran had tried to get “cute”.

The US naval blockade of Iranian ports remains in place, and the ceasefire expires next week. Ship tracking data from MarineTraffic showed that about two dozen vessels initially approached the Strait on Friday before most turned around and headed back to the Gulf. The physical reality on the ground has not yet matched the headline, but the market seemingly did not wait for confirmation.

Source: S&P500 – Bloomberg

The S&P is now up 11% in 11 days from its March 30 correction lows, hitting a fresh all-time high of USD$7162 on Friday. Bank earnings last week have been broadly strong (Bank of America beat), but Netflix dropped 10% on weak Q2 guidance, a reminder that the corporate picture is uneven. The three-week winning streak of 3%+ weekly gains is the strongest run since November 2025.

The VIX collapsed to 17.48, its lowest since late February, signalling that the market has materially repriced the war risk. However the question heading into Monday is whether Saturday’s Hormuz reversal triggers a giveback, or whether the market has already decided the war premium is permanently reduced.

Source: TradingView

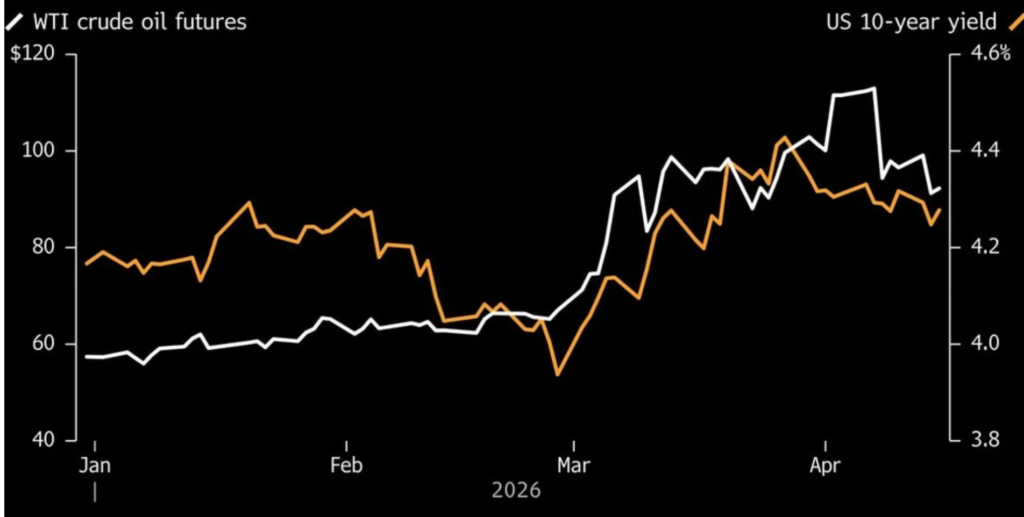

Yields have eased as the de-escalation trade gathered pace. The US10Y settled around 4.28%, down from its April highs near 4.44%, as the oil crash reduced inflation breakevens and briefly re-opened the door to rate cut expectations. The market is no longer pricing zero cuts for 2026, with some term structures now showing one 25bps cut priced for Q4, which is a meaningful shift from the “no cuts at all” consensus just two weeks ago. However the Saturday reversal complicates this dynamic where if oil rebounds sharply, the cuts may get priced back out.

Source: Bloomberg

Oil to minimal surprise had its most dramatic session since the war began. WTI plunged to 9.4% to USD$82.59, its lowest since late February while Brent crashed approximately 11% to around USD$89. Two weeks ago, Brent was above USD$113. The Hormuz reopening announcement was the catalyst, but the magnitude of the move reflects the scale of speculative long positioning that had built up in crude over seven weeks of supply disruption.

The physical picture remains uncertain: 230 loaded tankers are reportedly still waiting inside the Gulf, Saudi production capacity is reduced by ~600k bpd from facility attacks, and the East-West Pipeline bypass was also struck. Even if the Strait fully reopens, normalising supply will take weeks, not days.

The dollar sold off sharply as the war premium unwound. The DXY broke below 98 for the first time since January, settling around 97.9. The move was driven by the collapse in oil, which had been supporting the USD on terms-of-trade grounds, combined with the pricing of rate cut expectations.

Source: Coinglass

This was the week that crypto broke out. BTC surged to an intraday high of USD$78,348 on Friday, its highest level since February 4th and the first clean break above the USD$76,000 resistance that had capped every rally attempt since the conflict began. The move triggered a USD$762M in crypto liquidations with USD$593M on the short side, which is the most lopsided short squeeze since February. While the catalyst was relatively unambiguous on the Straits opening, the structural setup had been building for weeks as funding rates were pinned negative.

The Coinbase Premium Index, which tracks whether US spot buyers are paying more than the global average, hit its highest level since October 2025, indicating real institutional spot demand BTC’s 85% correlation with the Nasdaq during oil spikes meant that when the energy pressure lifted, crypto was one of the first places capital rotated back into.

The USD$76k-USD$78k zone is now the key battleground. If BTC holds above USD$76k through Monday’s session, despite Saturday’s Strait reversal, it would confirm a structural breakout from the seven-week war range. Above USD$78k, the next targets are USD$80k (psychological) and USD$82.5k (where the downtrend officially breaks). Below USD$76k, the move risks being labelled another ceasefire head fake, consistent with the pattern that has played out repeatedly since early March. The broader crypto market has also participated fully. SOL gained 4-5%, XRP held above USD$1.35, and AI-adjacent tokens rallied in sympathy with the semiconductor complex hitting records.

Structurally, BTC is now up over 20% since the onset of the conflict and 14% in April alone. The desk’s view is that if the ceasefire holds and the Strait actually normalises, the path to USD$85k+ is wide open. If it collapses, we expect BTC to absorb negative news better than equities on a risk-adjusted basis. The floor has been rising with each escalation cycle, and dynamic (shifting) beta can often be at play with BTC alongside geopolitical and risk moves.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

The past week marked a structural regime shift across the digital asset landscape as the “war trade” unwind catalysed a sweeping rotation back into risk. As geopolitical de-escalation headlines drove a significant repricing across global markets, crypto rallied as a high-beta expression of broader macro optimism.

On the desk, client flow dynamics shifted away from the defensive, Bitcoin-heavy bias seen earlier in the year; as we observed a counter-trend net selling skew in Bitcoin (BTC) and capital favouring higher-beta majors like Ethereum (ETH) and Solana (SOL), which saw robust net buying in a display of recovering risk appetite.

The technical highlight was BTC decisively breaching the supply zone above US$75,000 that had capped price action following February’s liquidation-driven move. BTC rallied to fresh quarterly highs of $78,348 during Friday’s New York session, driven by the reported reopening of the Strait of Hormuz and aided by a US$593M short squeeze. However, Iran’s reinstatement of “strict control” over the waterway on Saturday caused risk to falter, leading BTC to pare gains and close the week at $73,801. ETH followed a similar trajectory, rallying from an open of $2,191 to highs of $2,464 before retracing to $2,263. Despite the weekend volatility, a historical episode of sustained negative funding and a Coinbase Premium Index at yearly highs suggest the move remains underpinned by genuine spot demand rather than purely derivative-led speculation.

Performance across the altcoin complex was mixed for the week; while majors provided a constructive backdrop for pockets of localised exuberance in names like $ASTEROID, flows in previous sector leaders such as BitTensor (TAO) and Aave (AAVE) were muted as they faced localised setbacks. TAO saw a sharp sell-off following the turbulent exit of the Covenant AI team from the ecosystem, while AAVE saw a $6.6 billion TVL exodus following contagion stemming from a $292M exploit of the Kelp bridge, where attackers utilized stolen rsETH as collateral to borrow $196M in WETH – demonstrating that while the macro tide is rising, the long-tail is not immune to technical idiosyncratic risks.

In FX, the AUD/USD pair re-emerged as the premier outperformer amongst the G10 complex, surging from a weekly open of 0.7000 to four-year highs of 0.7221. This move was fuelled by a confluence of the AUD’s role as a cyclical “global barometer” for risk, coupled with domestic data that continues to reinforce the structural rising yield differential. While headline Australian unemployment remained steady at 4.3%, a technical read beyond the “noisy” headline print revealed a falling participation rate and an increase in total hours worked – representing a “canary in the coal mine” indication of a constrained and tightening labour force context that saw market-priced probabilities for a 25bps rate hike at the May 5th meeting strengthen to 72% through the week, cementing the RBA’s hawkish divergence against other G10 peers as the tightening domestic narrative persists.

This backdrop underpinned a net buying skew of AUD on the desk that was uncharacteristic of the year; while USDT saw a significant offramping skew against USD as participants utilised a well-bid market to trade into other fiat crosses.

Despite the weekend’s geopolitical pivot and BTC’s retracement to the mid-73k range, the structural floor for both majors and the AUD remains elevated, suggesting the market is increasingly focused on resolution optimism and structural currency drivers over transient war premiums.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and altcoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Ben Mensah, Trading Analyst

Derivatives Desk

WHOLESALE INVESTORS ONLY

Derivatives markets over the past seven days have been defined by a steady rebuild in risk appetite, before a late-week macro wobble tested that re-leveraging. Aggregate BTC perpetual open interest pushed higher from ~$29B to briefly test ~$33B mid-week, driven by systematic and momentum-led inflows, before retracing modestly into the weekend as macro uncertainty (long end interest rates and USD strength) capped positions. ETH lagged this build, with open interest rising only modestly and continuing to reflect weaker speculative engagement versus BTC.

Notably, liquidation activity remains contained. Despite intraweek daily spot swings of ~3–4% in BTC, there has been no evidence of forced deleveraging events. This reinforces the view that positioning remains cleaner, with tighter risk management and lower effective leverage across both retail and institutional cohorts. The absence of cascading liquidations continues to differentiate current conditions from the dislocations observed through March.

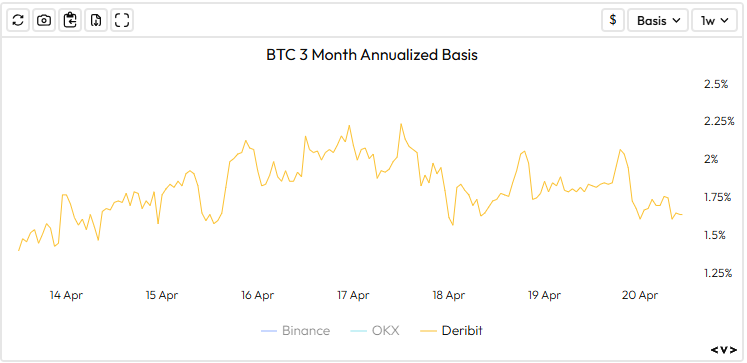

Funding dynamics remained soft and continued to reflect a market lacking directional conviction. BTC perpetual funding has spent much of the month in negative territory, indicating a persistent bias toward short positioning rather than demand for leveraged longs. While brief episodes of positive funding have emerged more recently (alongside short-term price strength), these prints have so far been limited in magnitude and duration, failing to establish a sustained long premium.

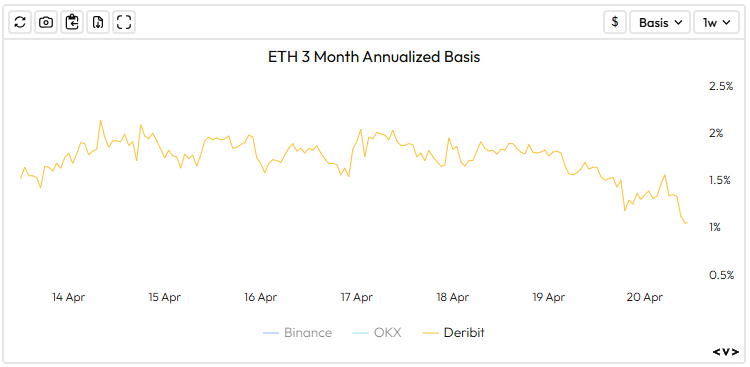

ETH funding has followed a similar but more muted profile, generally oscillating around flat with intermittent dips into negative territory. This continues to reflect weaker speculative demand relative to BTC and reinforces the broader softness in the ETH/BTC cross (-1% on the week).

Volatility markets saw a modest firming at the front end, with BTC implied vol generally stable overall. Short-dated vols traded in the ~40s% range, briefly firming into risk events, while 1M remained anchored around ~40-42%, keeping the curve near neutral..

ETH vol continues to trade at a persistent premium to BTC, reflecting higher beta and more reflexive spot behaviour. Particularly post the heightened ETH volatility caused by Aave concerns.

Overall, volatility conditions remain contained, with mild front-end sensitivity but no evidence of a structural repricing across the term structure. BTC put/call skew has moved to flat, in line with neutral funding markets.

From a technical perspective, BTC continues to consolidate within a well-defined range, with near-term resistance at $68k and a more structural ceiling toward $76k. Support now sits in the high $60k, with a break lower opening a move toward the $58k region where stronger spot demand previously emerged. ETH remains comparatively weaker, with resistance at $2.4k and key support around $1.8k; a sustained break below this level would likely accelerate relative underperformance.

Crypto credit conditions remain stable. Borrowing rates for BTC and ETH have held in a tight range (~1.5–2.5% annualised for BTC, ~1–2% for ETH), with no meaningful spikes in demand for leverage. Lending flows continue to be driven primarily by yield strategies rather than directional risk-taking. Haircuts and margin requirements are unchanged, and utilisation levels remain moderate, indicating no signs of systemic stress.

Overall, the derivatives complex reflects a market that is gradually re-engaging risk but remains tactically cautious. Skew signals are normalising, and leverage is rebuilding in a controlled manner. With positioning no longer stretched and technical ranges tightening, the setup increasingly points toward a volatility expansion phase — with the next directional catalyst likely to dictate whether this resolves to the upside breakout or a renewed downside test.

Source: Velo.xyz

What to Watch

TUE: GB Unemployment Rate, US Retail Sales MoM

WED: Fed Waller Speech, GB Inflation Rate

THU: ECB President Lagarde Speech, US Initial Jobless Claims

FRI: JP Inflation Rate YoY

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 13 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 7 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Zerocap Partners with Singapore Gulf Bank to Solve Institutional Fiat Settlement

How Zerocap and Singapore Gulf Bank are solving institutional crypto fiat settlement with real-time USD rails during Asia hours. The Problem With Legacy Settlement Institutional

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.