11 May, 26

Weekly Crypto Market Wrap: 11 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

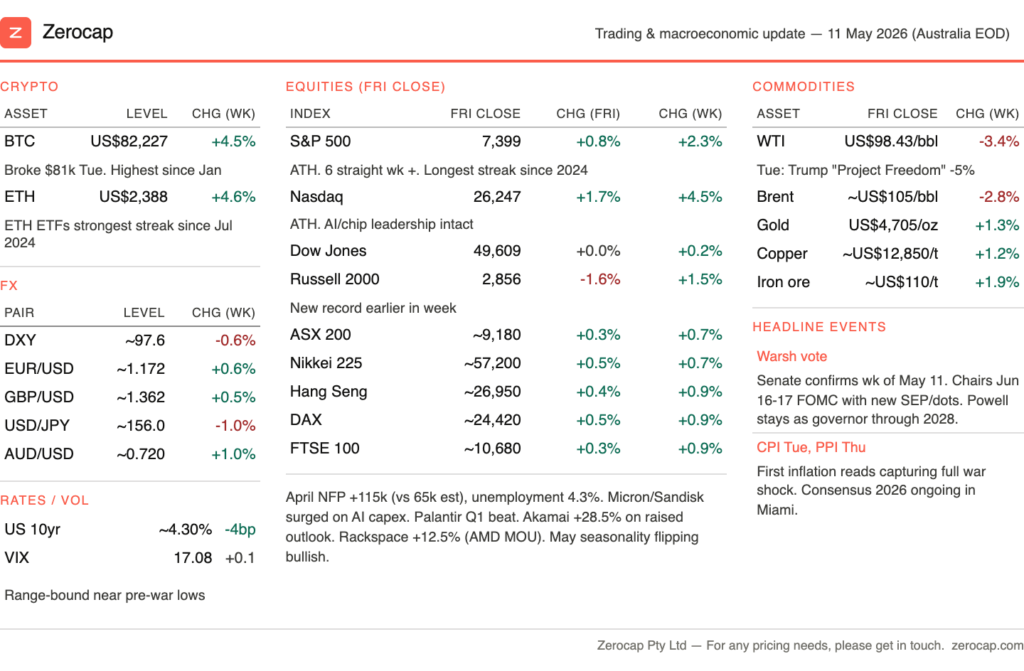

Week in Review

- U.S. spot BTC ETFs saw ~US$622.75M in inflows; ETH ETFs added ~US$70.5M

- Coinbase loses nearly $400 million in Q1 as CEO looks to reduce dependence on spot crypto trading

- Morgan Stanley’s bitcoin ETF absorbs $194 million in first month with no net daily outflows

- Strategy posts $12.5 billion Q1 loss as execs tout STRC ‘big success’

- Strategy likely to sell bitcoin to cover STRC dividends

Technicals & Macro

Markets

The risk-on regime is back and broadening. Equities posted a sixth consecutive weekly advance; BTC broke through $81k for the first time since January; and the war premium that defined Q1 has now substantially unwound (even as the conflict itself technically continues).

This week’s move in markets was driven by a combination of easing geopolitical risk, resilient macro data and continued strength in AI-linked technology names. Early in the week, reports surrounding “Project Freedom” — the Trump administration’s proposed framework for structured Iran de-escalation — helped push crude futures nearly 5% lower in a single session, reducing the immediate risk premium that had weighed on broader risk assets. That was followed by a stronger-than-expected April U.S. employment report on Friday, with nonfarm payrolls rising 115,000 against consensus expectations of 65,000 and the unemployment rate holding steady at 4.3%, reinforcing confidence that the US labor market remains resilient despite recent geopolitical disruptions.

Meanwhile, the technology sector continued to outperform, led by ongoing optimism around AI-related capital expenditure, with Micron, AMD and Apple rallying as investors gained further confidence that hyperscaler spending plans for 2026 remain intact. Notably, these gains occurred despite renewed military clashes around the Strait of Hormuz late in the week, suggesting markets are increasingly treating the conflict as a persistent but manageable background risk rather than a binary macro catalyst.

Source: A16z

The institutional macro focus now shifts to two key events this week. First, Kevin Warsh is expected to secure Senate confirmation, positioning him to chair the June 16–17 FOMC meeting and oversee the first updated dot plot and Summary of Economic Projections under his leadership. While Jerome Powell’s intention to remain on the Board of Governors through 2028 limits any immediate shift in the Committee’s policy balance, Warsh’s first press conference is still likely to act as a volatility catalyst given uncertainty around his policy stance and communication approach.

Second, U.S. CPI (Tuesday) and PPI (Thursday) will provide the first full read on the inflation impact of recent energy price disruptions. Consensus expects headline CPI to firm on higher energy, while the key focus for markets will be whether core inflation begins to reaccelerate. Rate expectations remain anchored to a relatively restrictive path through 2026, though a softer core print would likely reopen scope for modest easing expectations into the June FOMC meeting.

As we move into May, equities enter a seasonally weaker six-month period on historical averages. The key question is whether current structural drivers — including the AI capex cycle, continued geopolitical de-escalation, and ongoing institutionalisation of digital asset markets — are sufficient to offset that seasonal headwind.

Equities

Source: A16z

The breadth narrative in the equity complex is also evolving. Small caps making new highs alongside continued strength in mega-cap technology point to broader market participation, a setup that historically tends to extend equity trends rather than constrain them. With Q1 earnings season now largely behind us at ~18% YoY growth, attention is shifting to whether the AI capex cycle is translating into incremental revenue at the device and software layer. Recent results from Apple, Microsoft and Amazon provided initial confirmation that AI-related spending is beginning to filter through into tangible demand, but the key validation point remains Nvidia’s upcoming earnings release later this month, which will be critical in confirming the durability of the infrastructure-led growth narrative.

Fixed Income

The 10-year U.S. Treasury note yield settled around 4.30%, down modestly on the week as the strong jobs print was offset by the pullback in oil and easing inflation concerns at the long end. The 2-year U.S. Treasury yield held near 3.97%. The US interest rate market continues to price zero cuts through 2026, with the first cut not fully priced until late 2027 — a notable degree of policy patience given that oil is now meaningfully lower from recent war-driven highs and equity volatility has compressed significantly.

The setup into Warsh’s first meeting is increasingly asymmetrical. If hawkish positioning continues to dominate into the transition, any perceived dovish signal from the new Chair would risk a sharp repricing lower in yields and a corresponding extension higher in risk assets, particularly crypto markets.

Cryptocurrency

Source: TradingView

This was the week Bitcoin broke out. BTC closed Friday at US$82,227, up 4.5% on the week, after breaching US$80,000 on Monday and reaching a high of around US$81,500 on Tuesday — its strongest level since late January. The move was driven by a convergence of catalysts: April U.S. spot Bitcoin ETF inflows of US$2.44bn, the strongest monthly total since October 2025; nine consecutive days of net inflows totalling approximately US$2.7bn over a three-week period; easing geopolitical risk following the “Project Freedom” de-escalation framework and the associated reduction in Strait of Hormuz tail risk; and a pronounced short squeeze that unwound leveraged positioning built during the prior consolidation range.

Total U.S. spot Bitcoin ETF assets under management crossed US$100bn for the first time, with cumulative inflows since launch reaching approximately US$58bn, marking a structural shift in how institutional capital accesses the asset. Flow leadership remains concentrated in BlackRock’s IBIT and Fidelity’s FBTC, while Morgan Stanley’s entry into direct ETF issuance via MSBT — priced below IBIT — signals intensifying competition for institutional flow share. Strategy (formerly MicroStrategy) added 34,164 BTC worth approximately US$2.54bn during the week, while brief market sensitivity around comments from Michael Saylor suggesting the firm “may sell some Bitcoin to pay dividends” was ultimately absorbed without meaningful follow-through in price action.

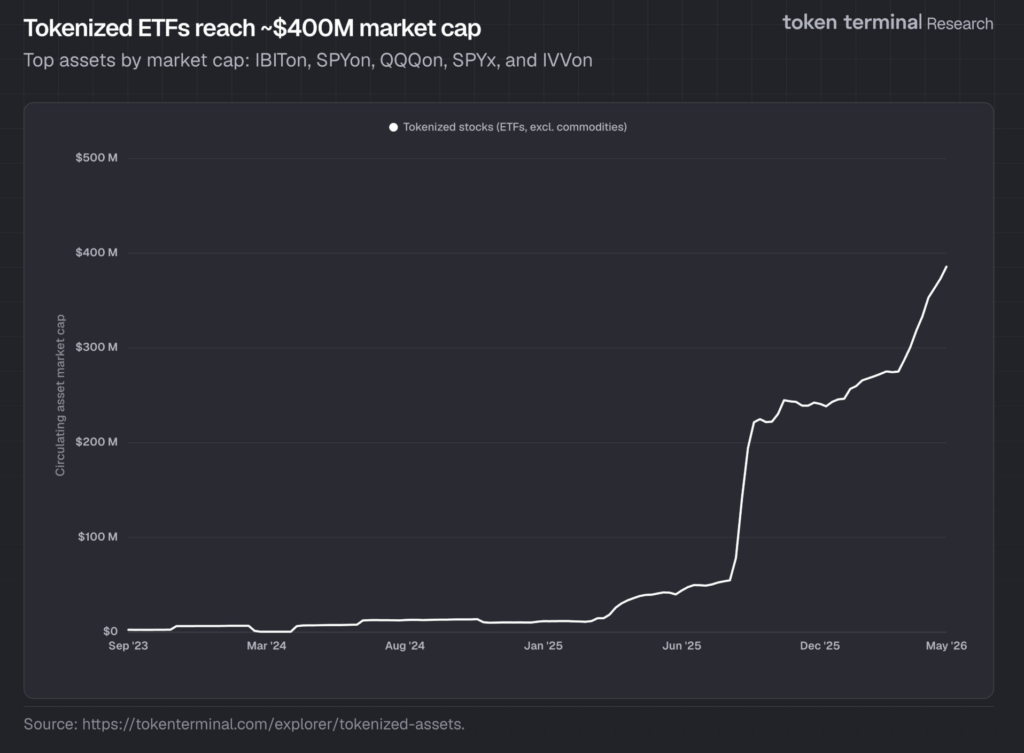

Source: Tokenterminal

Beyond spot and flow dynamics, sentiment was further supported by the Consensus 2026 conference in Miami, which opened on Monday and runs through the week, providing a modest structural tailwind to broader crypto positioning. However, the more notable development has been the continued rotation into tokenisation-focused themes. Crypto-linked equities such as Bullish (BLSH) and Galaxy Digital (GLXY), alongside the Centrifuge (CFG) token, have outperformed on growing momentum around tokenised financial market infrastructure, as investors increasingly position for tokenisation as a medium-term structural growth narrative.

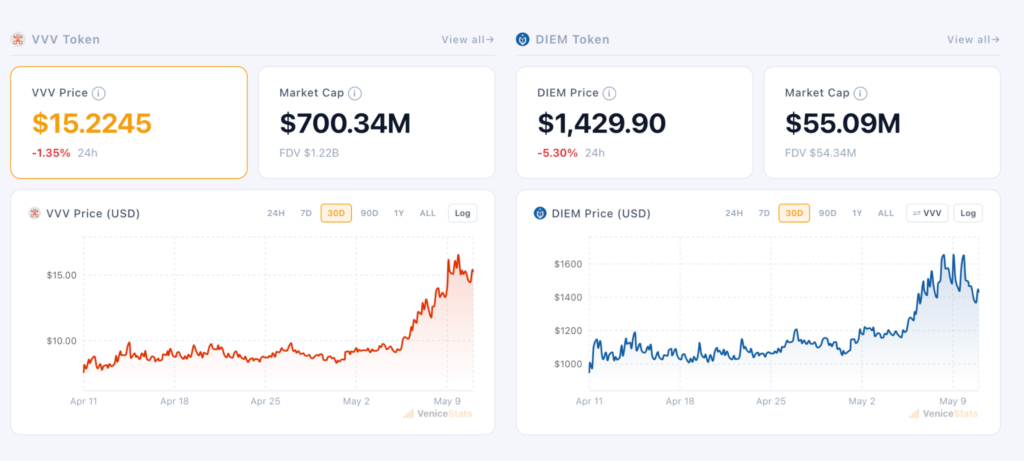

Source: Venicestats

In the AI compute and infrastructure token space, Venice Token (VVV) was the standout performer over the weekend, rising approximately 65% on the week from ~US$9.40 to a new all-time high of US$16.65. The move was supported by accelerating platform activity (8.8m monthly visits), aggressive buy-and-burn mechanics — with ~42% of circulating supply now permanently destroyed — and a scheduled reduction in annual emissions from 6m to 5m tokens effective May 1, with further step-downs expected through July. An additional tailwind came from eToro’s listing of VVV, improving retail accessibility and liquidity depth.

Over the same period, broader AI infrastructure tokens — including TAO, RENDER, FET and NEAR — also saw firm buying interest, though relative performance remained dispersed. VVV notably outperformed peers, reflecting a combination of realised platform usage, deflationary token mechanics, and a privacy-centric positioning narrative that differentiated it within the basket.

The Fear & Greed Index closed the week at 36, still in “Fear” territory despite Bitcoin trading near year-to-date highs. From a positioning perspective, the setup remains asymmetrical: structural demand continues to absorb supply in a relatively de-leveraged market, while sentiment indicators remain cautious. Key levels into next week are US$85,000 as near-term resistance and US$78,000 as breakout support. Maintaining a sustained hold above US$80,000 through upcoming CPI data and the early phase of the Fed leadership transition would be consistent with scope for a continuation toward higher highs into late May.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

Market conditions over the past week remained firmly driven by developments in the U.S.–Iran conflict and associated energy supply disruptions in the Strait of Hormuz, resulting in significant cross-asset volatility. Early in the week, reports of direct U.S.–Iran exchanges of fire and Iranian strikes on the UAE’s Fujairah energy infrastructure sharply lifted oil prices and reignited stagflation concerns. Equities were broadly offered, with energy a clear outperformer, while Treasuries sold off as higher oil prices repriced inflation expectations and pushed front-end yields higher.

Sentiment shifted materially through the middle of the week as growing optimism around a potential ceasefire triggered a broad risk-on rotation. Equities rallied on Wednesday (May 6), led by technology and industrials, with semiconductors outperforming following strong earnings and guidance from AMD. Oil reversed sharply from a high of US$102.70/bbl to US$88.66/bbl, although later Iranian pushback to ceasefire-related headlines saw crude recover part of those losses into the end of the week. Digital assets continued to trade as a high-beta expression of broader risk sentiment, with BTC reclaiming and consolidating above the US$80,000 level for the first time since late January, while ETH remained rangebound between US$2,250 and US$2,400. Forward funding rates continued to steepen from relatively subdued levels, indicating gradual improvement in positioning without evidence of excessive leverage returning to the market.

In Australia, attention centred on the Reserve Bank of Australia (RBA) following its 25bp rate hike on May 5, delivered by an 8–1 majority and reinforcing a persistently hawkish policy bias. While the move was broadly expected, the voting split underscored ongoing concern around inflation persistence despite rising global uncertainty. The AUD strengthened following the decision, though Governor Bullock’s relatively measured “wait and see” communication tempered near-term tightening expectations. AUD/USD traded near four-year highs at 0.7277.

On the desk, flow was concentrated in BTC and SOL, both of which saw sustained client demand through the week. BTC flows remained firmly bid as price action consolidated above the $80,000 level, while SOL also attracted consistent buy-side interest. ETH activity was comparatively subdued despite rangebound trading conditions, while PAXG recorded modest bid-side demand. Stablecoin activity remained heavily one-directional, with notable net selling pressure in USDT/USD. AUDD followed a similar pattern, although overall activity was light.

Across fiat FX flows, USD demand was exceptionally strong despite broader softness in the DXY, characterised by several larger notional tickets. AUD flows shifted to a net bid tone, marking a change from recent weeks and supported by the RBA’s hawkish decision. The NZD also saw strong inflows, while EUR flows were firmly offered. GBP activity remained minimal.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and selected altcoins, alongside key fiat currency pairs. With T+0 settlement, we ensure seamless execution and settlement across all flows.

Oliver Davis, OTC Trader

Derivatives Desk

WHOLESALE INVESTORS ONLY

Derivatives markets traded with a firmer tone through the week ending 10 May, although positioning remained relatively measured despite the recovery in spot prices. BTC continued to consolidate higher following the late-April rebound, with aggregate futures open interest recovering modestly but remaining well below the ~US$47bn peak observed during the more aggressively positioned October 2025 rally (currently ~US$26bn). Price action remained constructive into the weekend, though the absence of meaningful liquidation activity and only modest increases in perpetual open interest suggest the move has been driven primarily by spot-led demand rather than a material rebuild of leveraged positioning.

Funding dynamics stabilised across major venues over the week. BTC perpetual funding oscillated around flat to modestly positive levels, generally within a low single-digit annualised range, indicating cautious re-engagement in long positioning but limited evidence of leverage expansion. ETH funding continued to underperform BTC and traded closer to neutral overall, reinforcing persistent relative weakness in the ETH/BTC cross, which remained near the lower end of its recent range around 0.029–0.030. Overall, perpetual markets continue to reflect balanced positioning and subdued directional conviction rather than speculative excess.

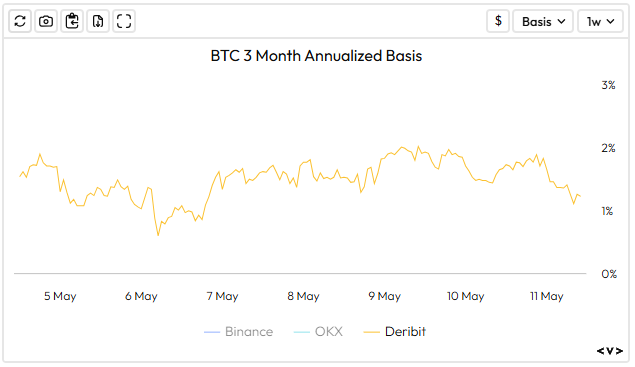

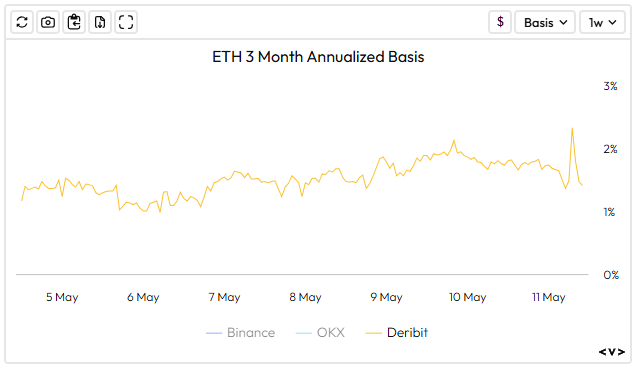

Futures curves have remained relatively flat, albeit slightly steeper than the compression observed during the April volatility episode. BTC 3-month annualised basis traded in the ~1–3% range depending on venue, remaining well below levels typically associated with more aggressive leverage cycles. ETH basis continued to show intermittent relative strength versus BTC in the front end, though the broader curve remains flat across tenors. Overall, futures markets continue to reflect a constructive but measured risk environment, with limited evidence of meaningful leverage extension further out the curve.

Volatility markets softened through the week as realised volatility declined and near-term event risk continued to decay. BTC front-end implied volatility drifted lower, with 1-week ATM trading in the mid-30% area, while 1-month and 3-month tenors remained broadly stable in the high-30s. The term structure flattened modestly as demand for short-dated protection eased, consistent with a more orderly spot environment and reduced hedging urgency. Skew remains marginally put-biased, though downside demand has compressed materially versus the April dislocation. ETH volatility followed a similar trajectory, maintaining a structural premium to BTC consistent with higher beta exposure and comparatively weaker spot structure.

From a technical perspective, BTC continues to trade within a constructive consolidation range following the recovery from April lows. Near-term support has progressively shifted higher into the high-US$70k to ~US$80k region, reflecting a strengthening pivot zone following the recent rebound. Overhead supply is now more clearly defined above this area, with resistance layering into the mid-to-high US$80k region where prior distribution has capped upside momentum. ETH remains comparatively fragile, with rallies continuing to fade below key resistance levels and persistent relative underperformance versus BTC evident across both spot and derivatives markets.

Credit conditions remain orderly with no observable signs of stress across major venues. Liquidations have been subdued since the April volatility episode, and open interest has recovered gradually without evidence of rapid leverage re-accumulation. Borrow rates across BTC, ETH, and stablecoins remain contained, with activity largely driven by basis trading and liquidity management. Collateral and margin conditions are unchanged, with no visible signs of forced deleveraging or credit strain, consistent with a broadly stable market structure.

Source: Velo.xyz

What to Watch

Tues: Aus Federal Budget, US Core CPI MoM/YoY, Aus Consumer Sentiment Index

Wed: US PPI MoM

Thu: US Retail Sales MoM

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 22 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 15 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 9 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.