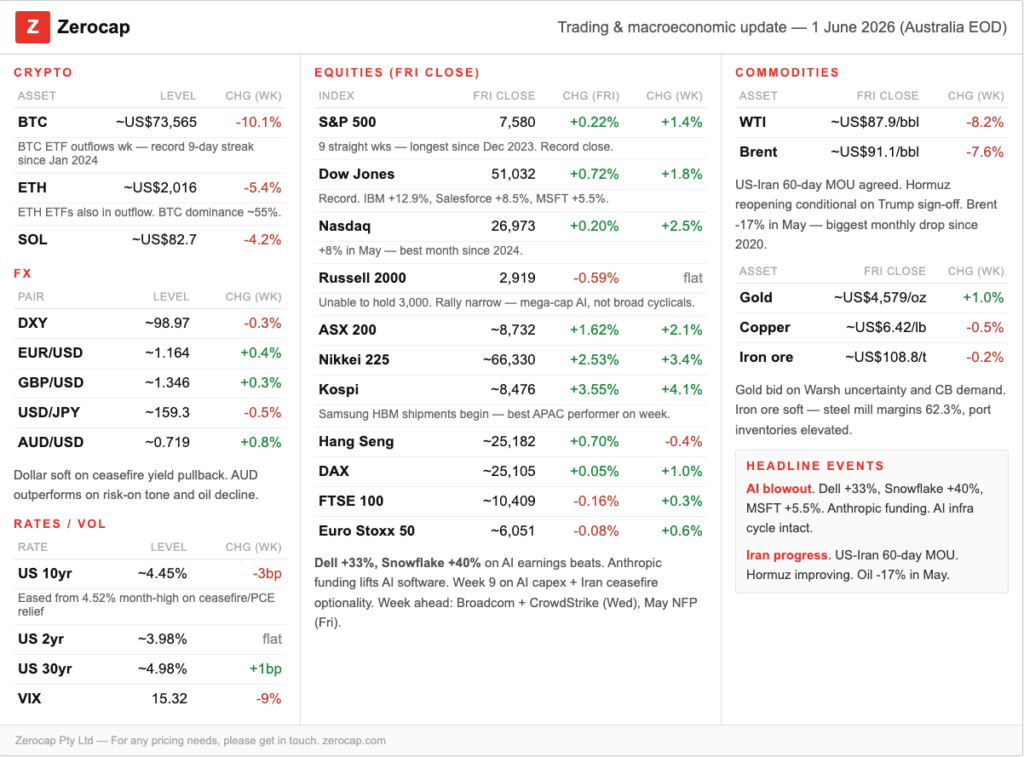

1 Jun, 26

Weekly Crypto Market Wrap: 1 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- U.S. spot BTC ETFs saw ~US$1.42B in outflows; ETH ETFs saw ~US$241.4M in outflows

- US has seized nearly US$1 billion in crypto from Iran

- DeFi TVL slides 14% since KelpDAO exploit as risk appetite retreats

- Global crypto ETP outflows deepen to US$1.5B as bitcoin products post worst weekly redemptions of 2026

- Grayscale’s Hyperliquid ETF negotiating ‘seed’ investment of roughly US$115 million in HYPE tokens

Technicals & Macro

Markets

The S&P 500 closed Friday at 7,580, extending its winning streak to nine consecutive weeks – the longest since December 2023 – while the Nasdaq pushed its May gain beyond 8%, marking its strongest monthly performance in over a year. Market sentiment continued to be supported by two key themes: ongoing upside surprises from the AI earnings cycle and easing geopolitical risk premium as diplomatic progress surrounding Iran contributed to lower oil prices and softer inflation expectations.

Reports of improving dialogue between Washington and Tehran, including discussion around extending existing de-escalation measures and broader negotiations, contributed to a sharp retracement in crude prices. The resulting decline in energy markets helped ease near-term inflation concerns and provided support across both equities and fixed income into month-end.

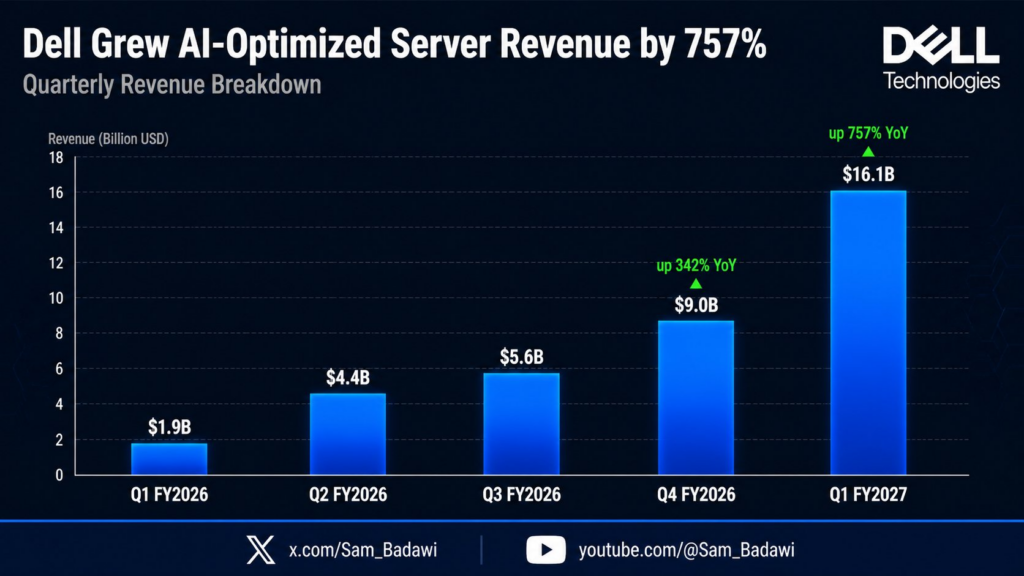

Source: X @sam_badawi

Dell and Snowflake each rallied more than 40% during the week following strong AI-related earnings results that reinforced confidence the infrastructure buildout cycle remains intact and continues to expand despite elevated rates and ongoing geopolitical uncertainty. The results provided another indication that enterprise AI-related capex remains resilient rather than showing signs of moderation. Microsoft gained 5.45%, supported in part by positive sentiment surrounding a new Anthropic funding round, while IBM (+12.9%) and Salesforce (+8.5%) extended the AI rally beyond semiconductors and into enterprise software, broadening participation across the sector.

The cross-market read-through is notable. Broader participation across software and infrastructure names suggests the rally is increasingly being supported by demand expectations and earnings delivery rather than multiple expansion alone, potentially extending the durability of the current earnings cycle. Small caps remained the relative laggard, however, with the Russell 2000 failing to reclaim the 3,000 level and continuing to underperform large-cap growth, reinforcing the narrow leadership profile that has characterised much of the recent rally.

Looking ahead, the coming week is heavily macro-focused. Friday’s May non-farm payrolls release remains the key event, with consensus expectations centred around ~85,000-96,000 jobs added and unemployment expected to remain near 4.3%. A softer labour print would support the disinflation narrative and reinforce expectations for a prolonged holding pattern from the Fed heading into the June 16-17 FOMC meeting, while a stronger result would likely challenge easing expectations given markets continue to price a relatively restrictive policy path through 2026.

Wednesday’s ISM Services release will also be closely watched for signs of whether softer energy prices and tighter financial conditions are beginning to impact broader activity. Particular focus will likely fall on the employment and new orders components. Geopolitically, markets remain sensitive to further developments surrounding Iran, with any additional de-escalation measures or progress in negotiations likely to remain an important driver for oil, inflation expectations, and broader risk sentiment.

Fixed Income

Source: TradingView

The US 10-year Treasury yield finished Friday near 4.45%, down modestly on the week after reaching highs around 4.67% in mid-May, as easing geopolitical risk premium and lower oil prices reduced some near-term inflation concerns. The 2-year yield remained relatively stable around 3.99%, leaving the 2s10s curve near +46bp. The curve continues to steepen gradually as front-end rates remain anchored by expectations for a prolonged holding pattern while longer-dated yields continue to reflect fiscal concerns, elevated issuance, and higher term premium.

April PCE inflation remained elevated, although both headline and core monthly prints came in modestly below consensus, providing incremental support for the view that policy rates may remain unchanged in the near term. Market pricing continues to imply a very high probability of no change at the June 16–17 FOMC meeting.

Attention now turns to Kevin Warsh’s first meeting as Chair following his appointment earlier in May. Markets will focus closely on the updated dot plot, revisions to the Summary of Economic Projections, and any shift in language around the policy path given the leadership transition. The backdrop remains challenging: inflation remains above target, energy markets remain sensitive to developments in the Middle East, and policymakers continue to balance resilient economic activity against signs of gradual disinflation. Against this backdrop, rates markets remain cautious, with investors continuing to price a restrictive policy environment despite some moderation in recent inflation concerns.

Commodities

Oil prices moved sharply lower during the week as the geopolitical risk premium partially unwound. Brent crude settled at approximately US$91/bbl on Friday – its lowest level in six weeks and down nearly 20% for May, the largest monthly decline since the Covid-19 pandemic – while WTI declined toward US$87, off roughly 17% month-on-month. The driver was consistent throughout: improving diplomatic signals surrounding the Iran conflict and reports of a tentative 60-day ceasefire extension, with energy markets increasingly pricing the possibility that Hormuz shipping disruptions could normalise over weeks rather than months. It is worth noting, however, that the path from diplomatic headline to physical barrel remains long – mines need clearing, infrastructure is damaged, and tanker flows will be slow to rebuild even if a deal is formalised.

Gold consolidated near US$4,500/oz on Friday, supported by Warsh-era rate uncertainty and structural central bank demand even as the Iran risk premium partially faded. The metal remains well off its January highs above US$5,400 but has found a floor – the pull between geopolitical relief and persistent inflation keeps the asymmetry skewed to the upside for now. Copper held near US$6.42/lb with little directional conviction, while iron ore softened to US$108.8/t – blast furnace operating rates in China unchanged week-on-week, steel mill margins slipping, and port inventories remaining elevated against near-record Australian and Brazilian export volumes.

The sharp reversal in Brent from its May highs is one of the most important macro developments for broader risk assets. If sustained, lower energy prices provide meaningful relief to headline inflation over coming months – directly reducing pressure on Warsh at the June FOMC and potentially doing more for rate expectations than any single data print. The caveat is that oil was also up over 50% since the year began; even after this correction, the energy shock has already been transmitted into April’s 3.8% PCE print, and the relief will take months to flow through.

Cryptocurrency

HYPE was the clear standout performer across digital assets during the week, closing near US$61–63 on Friday before extending toward US$70 over the weekend, materially outperforming both BTC and ETH despite broader market consolidation. Performance was supported by a combination of continued protocol growth, strong market share retention in decentralised perpetuals, and increasing institutional attention toward on-chain trading infrastructure.

Sentiment improved materially following comments from ICE CEO Jeffrey Sprecher at the Bernstein Strategic Decisions Conference, where references to Hyperliquid’s scale and reported engagement with the team were interpreted as a notable signal of growing traditional finance interest in decentralised market infrastructure. ETF-related flows also remained supportive, with newly launched HYPE-linked products continuing to attract early allocations, while protocol fee buyback mechanisms continued to provide a constructive supply dynamic.

More broadly, HYPE’s relative strength reinforces the current market preference for infrastructure-linked digital assets with observable revenue generation and market share leadership. While BTC and ETH traded largely as macro assets during the week, HYPE continued to trade more idiosyncratically, supported by protocol-specific catalysts and continued interest in the convergence between decentralised and traditional market infrastructure.

The contrast with BTC was notable. BTC stabilised near US$73,500, failing to meaningfully participate in the broader equity risk-on move, while ETH held just above US$2,000 and continued to underperform on a relative basis. BTC dominance moved back toward the 57–58% region, remaining elevated by historical standards and continuing to weigh on broader altcoin participation, particularly within the ETH/BTC cross.

Spot ETF flows also remained a headwind. US spot Bitcoin ETFs recorded an extended period of net outflows, marking the longest sustained redemption period since launch, while cumulative outflows over the period materially reversed the strong accumulation trend observed earlier in the year. Larger products, including BlackRock’s IBIT, experienced notable redemption activity, highlighting a softer institutional flow backdrop relative to previous months.

The deterioration in ETF demand has reduced one of the market’s key sources of marginal buying pressure. As a result, a more durable recovery in spot markets may increasingly depend on either renewed institutional allocations, stronger OTC demand, or improved crypto-native participation across both on-chain activity and derivatives markets.

For any pricing needs, please get in touch with the Zerocap desk.

Aaron Wong, Analyst

Spot Desk

The softer tone across digital assets persisted through the week, with participation remaining subdued despite stronger performance across broader risk assets. Market activity continued to reflect a more defensive positioning environment, with crypto-specific liquidity conditions and weaker institutional participation remaining more influential than the supportive macro backdrop.

Desk activity broadly aligned with market direction. BTC and ETH both recorded modest net selling skews, while SOL remained the strongest source of altcoin participation and finished the week with a net buying bias. Outside of larger-cap assets, participation remained selective, with flows concentrated in a small number of idiosyncratic themes rather than broad-based risk appetite.

Relative strength across altcoins remained concentrated. HYPE continued to outperform following strong momentum in decentralised perpetual infrastructure narratives, while VVV and ZEC also attracted incremental interest on usage-driven and thematic flows respectively. Overall, trader engagement remained concentrated in differentiated crypto-native exposures rather than wider market rotation.

Stablecoin activity remained the dominant feature of desk flows. Significant off-ramping across both USDT and USDC into USD-denominated flows reinforced ongoing demand for dollar liquidity. Across broader FX activity, EUR remained offered, NZD demand was firm, and AUDD participation stayed elevated with flows skewed toward on-ramping activity.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins, and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Ben Mensah, Trading Analyst

Derivatives Desk

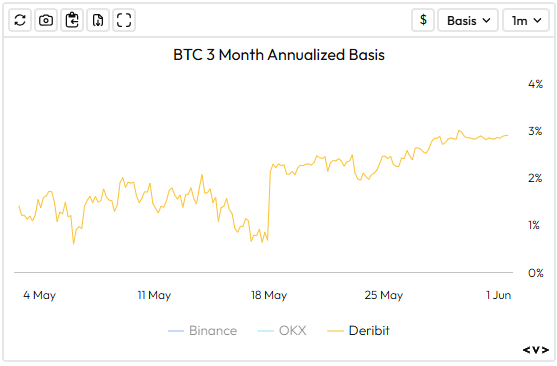

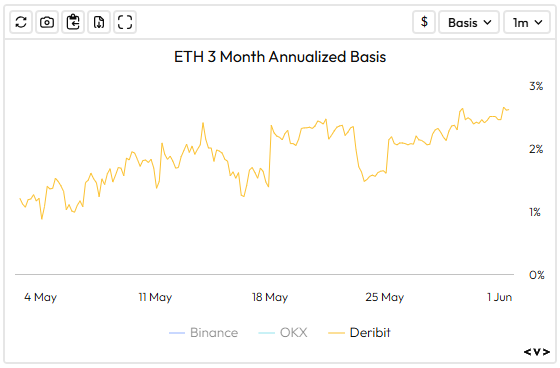

Structured products markets transitioned from macro repricing toward stabilisation through the week ending 1 June. US Treasury yields retraced from recent highs as oil moved lower and geopolitical risk premium eased, helping improve broader financial conditions. Despite the more constructive backdrop, crypto participation remained measured, with BTC price action continuing to resemble consolidation rather than breakout conditions.

BTC options markets reflected a cautious picture beneath the surface. Front-end implied volatility edged modestly higher through the week, with 1-week ATM volatility trading around ~33% into the weekend despite improving macro conditions and recovering spot prices. Term structure moved slightly more positive through front tenors, while skew stayed modestly put-biased, suggesting downside hedging demand remains present but contained. Overall, options markets continue to imply range-bound conditions rather than a meaningful expansion in realised volatility.

Positioning metrics also remained subdued. Perpetual funding recovered back into consistently positive territory, while the 3-month annualised basis moved modestly higher into the ~3–4% range across major venues. More notable was BTC’s resilience despite softer ETF demand and relatively muted derivatives participation. While US equities continued trading near all-time highs, crypto leverage metrics remained contained, suggesting positioning remains relatively light rather than crowded.

Credit conditions remained stable overall, with borrow markets normalising, liquidation activity subdued, and funding dispersion across venues compressed.

The broader derivatives complex continues to point toward balance rather than aggressive risk-taking. More constructive funding and forwards have improved sentiment at the margin, but subdued leverage, contained basis, and stable volatility markets continue to support a consolidation regime rather than a meaningful expansion in positioning.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

What to Watch

Mon: EU Unemployment Rate (April)

Tues: ISM Manufacturing PMI, EU CPI (YoY, MoM)

Wed: AU GDP (QoQ, YoY)

Thu: ISM Service PMI (May), AU Balance of Trade

Fri: Non Farm Payrolls, US Unemployment Rate, EU GDP (QoQ, YoY)

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.