6 Jul, 26

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- CLARITY Act missed the July 4 White House deadline – Senate adjourned June 25 and returns July 13

- A coalition of more than 140 companies backed Open USD (OUSD), a new stablecoin announced on June 30 and governed by an independent entity called Open Standard.

- Ethereum Institutional launched July 1 with backing from Joe Lubin and 500+ relationships spanning T1 banks, asset managers and sovereign institutions.

- Robinhood launched the public mainnet for Robinhood Chain, bringing tokenized stock trading live in more than 120 countries.

Technicals & Macro

Markets

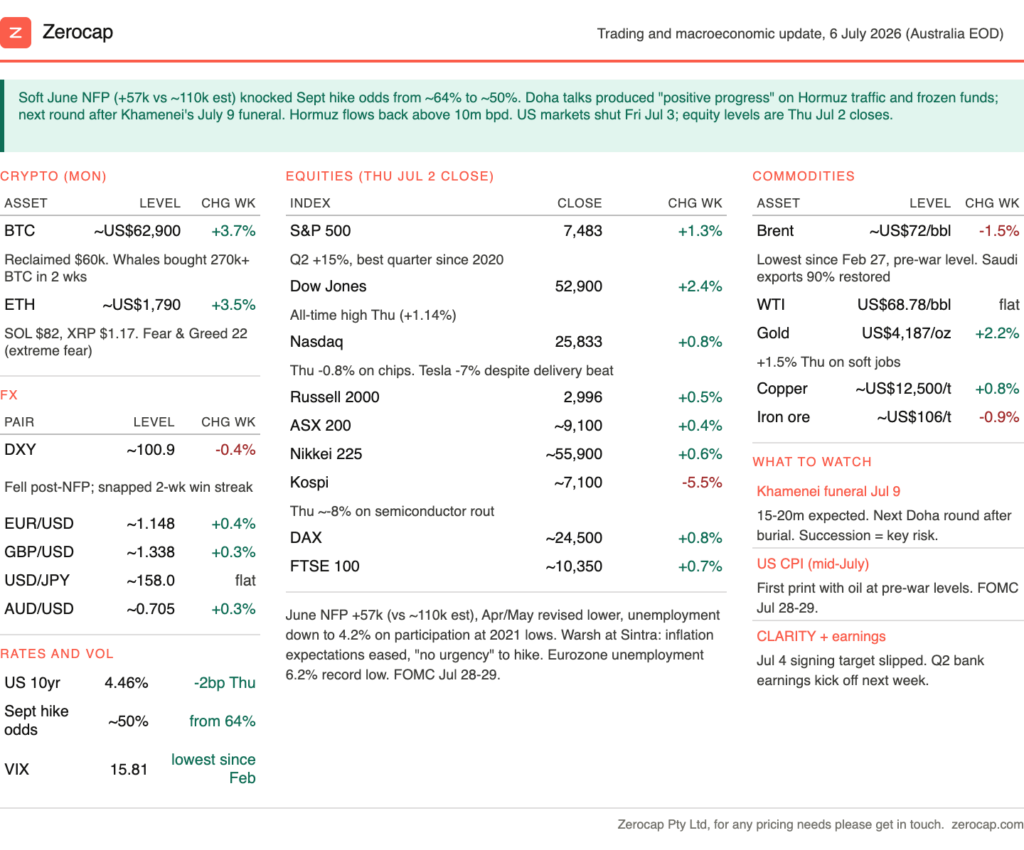

The tape flipped from inflation fear to growth fear in the space of one payrolls print. June nonfarm payrolls, released Thursday ahead of the Independence Day close, rose just 57,000, the fewest in four months and well short of the roughly 110,000 consensus. The damage was compounded by downward revisions to April and May, with May’s gain cut to 129,000 from the 172,000 originally reported. The unemployment rate actually ticked down to 4.2 percent, but for the wrong reason: labour force participation fell to 61.5 percent, near multi-year lows, so the drop reflects people leaving the workforce rather than genuine strength. Average hourly earnings held at 0.3 percent month on month and 3.5 percent year on year, so wage pressure has not fully rolled over, but the overall signal was clear cooling. Markets moved immediately, cutting the implied probability of a September rate hike to roughly 50 percent from about 64 percent the prior day. The report landed on top of a soft ADP private-payrolls number on Wednesday, so the labour-market message was consistent across the week.

Fed Chair Warsh, speaking at the ECB Forum in Sintra noted that inflation expectations have moderated over the past month and that there is “no urgency” to raise rates, while reaffirming the commitment to price stability. That is a meaningful softening in tone from the hawkish debut FOMC in June, and it matters because it tells you the new Chair is watching the cooling labour data as closely as the sticky inflation prints.

The geopolitical backdrop also improved: US-Iran talks in Doha concluded with what both sides described as positive progress on Strait of Hormuz traffic and the release of frozen Iranian funds, though the next round is on hold until after Ayatollah Khamenei’s funeral on 9 July, with 15 to 20 million mourners expected in Tehran. The succession question in Iran is now the single largest geopolitical variable, but for markets the near-term signal is de-escalation, with oil at pre-war levels doing the disinflationary work. The combination of a cooling jobs market, a softer Fed and lower oil is, on balance, a risk-positive mix, which is why equities closed the holiday-shortened week near records even as the growth data disappointed.

Stock Markets

Source: TradingView

US markets were closed Friday 3 July for Independence Day, so the levels here reflect the Thursday 2 July close, which capped a strong start to the third quarter. The Dow closed at an all-time high around 52,900, up 1.14 percent on Thursday and roughly 2.4 percent on the shortened week, leading the major indices as capital rotated toward cyclicals and value on the softer-Fed, lower-rates read. The S&P 500 finished near 7,483, up around 1.3 percent on the week, after posting a 15 percent gain for the second quarter, its best quarterly performance since 2020. The Nasdaq lagged, closing near 25,833 and slipping about 0.8 percent on Thursday as the semiconductor complex extended its recent weakness and Tesla fell roughly 7 percent despite reporting a quarterly delivery beat, a classic “sell the news” reaction after a strong run. The Russell 2000 pushed just below 3,000 at 2,996, its participation confirming the breadth of the rotation. The standout tension in the tape is that the AI and chip leadership that drove the first half is now the source of the drag, while old-economy and rate-sensitive names are carrying the indices.

Internationally, the picture was mixed: European bourses firmed on the softer dollar and record-low eurozone unemployment of 6.2 percent, while the Kospi took another heavy hit, falling around 8 percent on Thursday and roughly 5.5 percent on the week as the global semiconductor sell-off hit Samsung and SK Hynix hardest.

Fixed Income

The 10-year yield eased to around 4.48 percent, down a couple of basis points on Thursday and lower on the week, as the soft payrolls report pushed investors to scale back hike expectations. The front end led the move, with the market now pricing roughly a 50 percent chance of a September hike, down from about 64 to 67 percent before the jobs data, and the broader 2026 path meaningfully less aggressive than the three hikes that were priced at the June peak.

Warsh’s Sintra comments that inflation expectations have eased and there is no urgency to tighten validated the move and gave the bond market permission to rally. This is the mirror image of the prior fortnight: two weeks ago the hot PCE print had the market pricing an 80 percent chance of a December hike, and now a soft jobs report has the front end pricing barely even odds for September.

The curve stayed modestly positive, consistent with a soft-landing rather than recession pricing, and the notable feature is that the long end is being anchored by the collapse in oil and easing inflation expectations rather than by growth panic. The next test is the mid-July CPI print, which will be the first inflation reading to fully capture oil back at pre-war levels, followed by the FOMC on 28 and 29 July.

Cryptocurrency

Crypto steadied and clawed back ground after the late-June washout. Bitcoin recovered to around 62,900 dollars, up roughly 3.7 percent on the week, reclaiming the psychologically important 60,000 dollar level it had lost when the hot PCE print drove it to a 20-month low near 58,900 the prior week. ETH rose to around 1,790 dollars, with Solana near 82 dollars and XRP around 1.17 dollars. The recovery was driven by the same macro pivot that lifted equities: the soft jobs report and Warsh’s tone eased the higher-for-longer pressure that had been the primary weight on non-yielding assets, and the reclaiming of pre-war oil levels removed a key inflation overhang. The most constructive signal was on-chain: whale wallets accumulated more than 270,000 BTC over the past two weeks, a clear sign that large holders treated the sub-60,000 dollar zone and the test of the 200-week moving average as an accumulation opportunity rather than a breakdown.

Under the surface, the recovery was led by names with genuine catalysts rather than broad beta, which is a healthier signal than a pure sentiment bounce.

JUP led the majors, up around 13 percent on returning Solana demand, a live revenue-funded buyback, and a governance proposal to lift the share of protocol fees directed to buybacks and burns to 70 percent, a clear pivot toward hard value accrual. MORPHO rallied more than 13 percent after Standard Chartered initiated coverage with a 60 dollar end-2030 target, roughly 33x upside from current levels, framing it as a dual play on DeFi lending and onchain banking infrastructure, and notable as another instance of a tier-one bank putting formal price targets on DeFi tokens. ONDO firmed on positioning ahead of the DTCC tokenization group’s July go-live alongside BlackRock, JPMorgan and Goldman Sachs, a reminder that the real-world-asset tokenization thread continues to attract the largest names in traditional finance. And VVV traded well after Erik Voorhees announced a 65 million dollar raise for Venice at a 1 billion dollar valuation, a strong private-market mark for the AI-inference token in a soft tape.

The infrastructure headlines were also arguably more consequential than the price action. Robinhood launched the public mainnet for Robinhood Chain, an Arbitrum-based layer-2 that takes its tokenised equities live in more than 120 countries alongside a 7 percent USDG lending product, a meaningful step in the convergence of brokerage and onchain rails.

But the biggest structural shift was in stablecoins. Open USD launched with backing from a 140-strong consortium including Visa, Mastercard, Stripe and Coinbase, offering free mint and redemption with reserve income shared across partners. The model directly attacks the economics that have underpinned the incumbents: Circle shares fell 15 to 17 percent on the news, because the reserve float, the most profitable part of the stablecoin business, is now openly contested by a network with distribution that dwarfs any single issuer. For a desk that watches stablecoin rails as core settlement infrastructure, this is the most important competitive development in the space in some time, and the read-through to fee compression across the entire stablecoin complex is the theme to track into the second half.

Technically, reclaiming 60,000 dollars was the first repair signal, and BTC now needs to clear the 64,000 to 65,000 dollar zone to confirm the bottom is in, with the 200-week moving average having held as major support on the prior week’s test. On the downside, a loss of 60,000 dollars would re-expose the 58,000 dollar area and the 55,000 dollar options cluster below it.

The asymmetry has improved modestly: the macro tailwind from a softer Fed and lower oil is now working with crypto rather than against it, whale accumulation is providing a demand floor, and sentiment is washed out, but the AI trade continues to compete for the marginal risk dollar and the CLARITY Act’s slipped 4 July signing target is a near-term disappointment.

The desk is watching three things in order: whether BTC can convert the 60,000 dollar reclaim into a hold above 64,000, whether STRC continues to stabilize as BTC recovers, and the mid-July CPI print as the next macro catalyst.

Emir Ibrahim, Analyst

Spot Desk

Markets remained cautious throughout the week as participants digested a combination of softer US economic data, evolving central bank expectations and ongoing geopolitical uncertainty in the Middle East.

Negotiations between the US and Iran continued throughout the week and continued to be a critical driver of sentiment. Sentiment was sensitive to developments surrounding the Strait of Hormuz and the broader implications for global energy markets. Although oil prices eased from recent highs as supply concerns moderated, geopolitical risk continued to influence inflation expectations and broader risk sentiment.

Domestically, attention centred on the release of the RBA’s June meeting minutes, which reinforced that the Board remains in a “wait and assess” mode following earlier policy tightening. Members noted that financial conditions are now somewhat restrictive and that the economy is slowing broadly as expected, although underlying inflation remains above target and poly must remain sufficiently restrictive. Australia’s balance of trade surplus also widened during the week, although the release had only a modest impact on market pricing.

Digital asset markets traded higher over the week as easing rate expectations supported broader risk sentiment. BTC (+6.84%), ETH (+13.59%) and SOL (14.59%) all posted weekly gains, with SOL outperforming in the majors. In stables, USDT continued to trade modestly below parity while USDC also traded at a discount to its redemption value. The stablecoin sector also saw the announcement of Open USD (OUSD), a consortium backed US dollar stablecoin supported by more than 140 industry participants.

On the desk, client flow was dominated by stablecoin selling, with USDT bids accounting for the majority of activity. FX flow was led by USD and NZD, while AUD traded broadly balanced over the week. Crypto activity remained relatively light, with both BTC and ETH recording net selling, while participation across smaller-cap digital assets was limited.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Oliver Davis, OTC Trader

Derivatives Desk

The derivatives market has moved from outright downside protection toward a cautiously constructive posture.

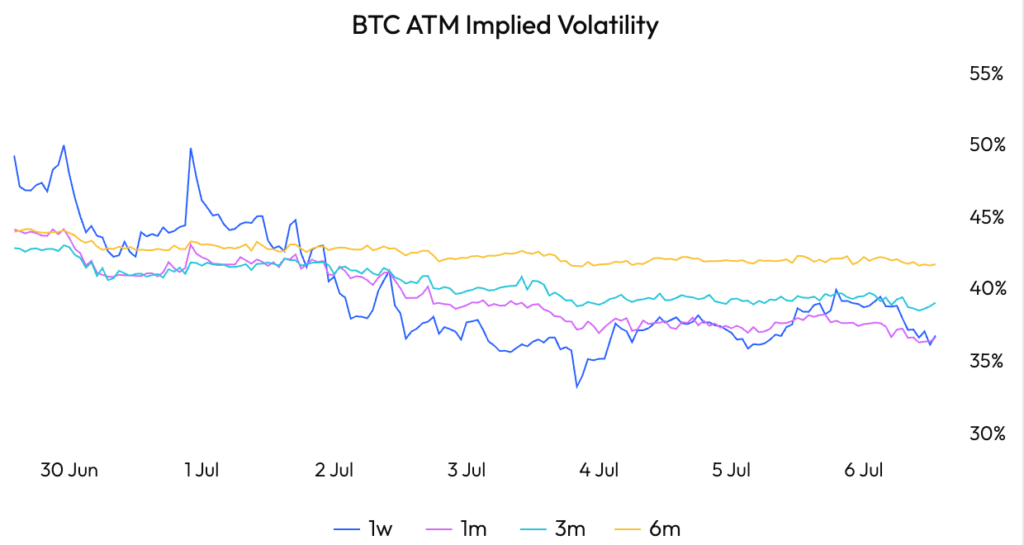

The June sell-off drove a sharp repricing in volatility and protection demand. Since then, Bitcoin’s recovery above $60k has coincided with falling 30-day implied volatility in both BTC and ETH, reversing much of the volatility premium that built during the drawdown. This is important: the market is no longer paying the same premium for immediate downside insurance, but neither is it yet showing the type of broad-based leverage typically associated with late-cycle euphoria.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

The options tape has shifted accordingly. Recent BTC flow has concentrated in calls between $60k and $70k, while ETH activity has shown notable interest in $2,500 calls. That is a meaningful change from June’s defensive positioning, although it should not be confused with an all bullish signal. A material part of the rebound was mechanically driven: approximately $272m of short liquidations accompanied the move higher on 2 July.

The practical read-through is that upside volatility has become the more natural source of yield, particularly for holders who are comfortable monetising BTC into strength. However, with CPI and the FOMC minutes ahead, this is not a market for indiscriminate exposure. The desk will be watching these macro catalysts for the next signal.

Jon de Wet

CIO

What to Watch

Wed: Fed Chair Warsh Speech, US JOLTs Job Openings

Thu: US FOMC Minutes, CN Inflation Rate YoY

Friday: US Existing Home Sales

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.