29 Jun, 26

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

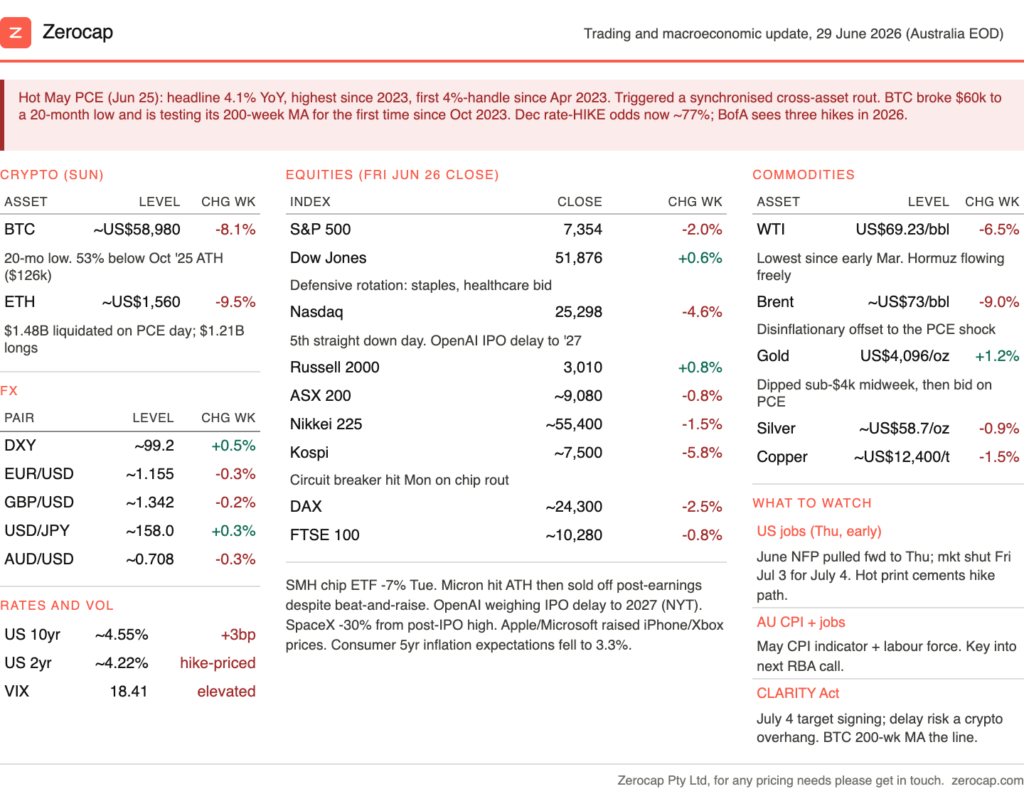

- U.S. spot Bitcoin ETFs saw US$1.79B in outflows, the second-largest weekly exit since launch; Ethereum ETFs shed US$273M.

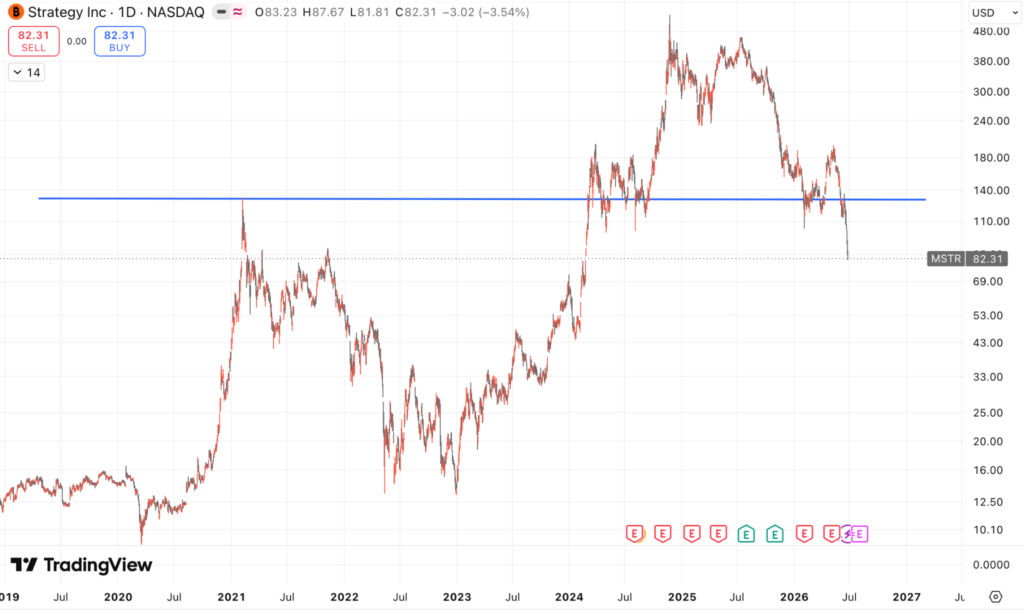

- Strategy (MSTR) briefly loses bitcoin premium as enterprise mNAV dips below 1; preferred equity product STRC prints all-time lows near US$72..

- World Cup activity boosts Polymarket volume as Kalshi sets open interest records; DraftKings launched its own prediction markets exchange DKeX.

- Framework Ventures raises US$400M fund to invest across crypto, AI, robotics, energy and fintech.

- BlackRock-backed tokenisation platform Securitize targets early July NYSE debut via US$400M SPAC deal.

Technicals & Macro

Markets

Inflation remained the dominant macro theme this week, reinforcing the view that while the geopolitical backdrop has improved, the inflationary consequences of earlier energy disruptions continue to work their way through the economy. The May PCE report, released on Thursday 25 June, showed headline inflation rising to 4.1% (YoY), the highest reading since April 2023, while core PCE increased to 3.4%. Monthly inflation was broadly in line with expectations (headline +0.4%, core +0.3%), but the annual readings confirmed that the earlier energy shock has become embedded in the Federal Reserve’s preferred inflation measure. Markets interpreted the report as reinforcing the Fed’s recently hawkish stance, with expectations for policy easing pushed further into the future and rate hike probabilities increasing.

Only a few months ago, markets were debating the timing of the first rate cut. That discussion has now shifted toward the possibility of further tightening, representing one of the sharpest changes in policy expectations of the current cycle. Several Fed officials continued to emphasise that additional tightening remains possible should inflation prove persistent, while debate has increasingly centred on how long policy will need to remain restrictive.

There was, however, an important offset. Oil prices continued to decline as shipping through the Strait of Hormuz normalised and concerns over prolonged supply disruption eased. Brent traded below US$74 and WTI near US$69, improving the medium-term inflation outlook despite the elevated backward-looking data. Consumer inflation expectations also moderated, with longer-term measures declining in the latest University of Michigan survey. The result is a market facing two competing narratives: recent inflation data continue to justify a cautious Federal Reserve, while lower energy prices suggest headline inflation could begin easing over coming months if current trends persist. June payrolls, brought forward to Thursday ahead of the US Independence Day holiday, now represent the next major catalyst for markets.

Stock Markets

Source: TradingView

Stock markets endured a mixed and increasingly rotational week. The S&P 500 fell around 2% to close Friday at 7,354, while the Nasdaq declined 4.6% to 25,298, recording its fifth consecutive losing session. By contrast, the Dow Jones Industrial Average gained 0.6% to 51,876 and the Russell 2000 added 0.8%, highlighting that the weakness remained concentrated in large-cap technology and AI-related names rather than the broader market.

Higher-for-longer interest rate expectations following the PCE release continued to pressure long-duration growth stocks, while investor appetite for AI infrastructure names became noticeably more selective after an exceptional rally through recent months. Sentiment was further dampened by reports that OpenAI is considering delaying a public listing until 2027, with discussions reportedly centred on waiting to achieve a US$1 trillion valuation rather than pursuing an earlier IPO at a lower valuation. The report added to concerns that expectations across the AI ecosystem have become increasingly demanding. Meanwhile, SpaceX, despite a strong IPO debut, has retraced meaningfully from its post-listing highs, reinforcing investor caution toward richly valued AI-related businesses and contributing to broader weakness across the semiconductor complex.

The semiconductor complex remained under pressure. The VanEck Semiconductor ETF (SMH) fell 7% on Tuesday alone, extending the sector’s recent correction. Micron briefly traded at fresh all-time highs before reversing lower despite delivering another beat-and-raise quarter, a classic example of “good news not being good enough” after months of exceptionally high investor expectations. The reaction suggests markets are becoming increasingly selective toward AI-related names rather than indiscriminately rewarding strong earnings.

Elsewhere, Apple and Microsoft both announced price increases across selected product lines, reinforcing the broader narrative that pricing power remains intact but also highlighting the inflationary pressures still working through the economy. Capital rotated defensively, with consumer staples outperforming as investors favoured companies offering more resilient earnings profiles. Procter & Gamble, Clorox and Walmart all finished the week higher.

Asian markets felt the pressure early in the week, led by South Korea’s semiconductor-heavy KOSPI, which briefly triggered a circuit breaker after falling more than 8% intraday before recovering to close down 5.8%. The move reinforced how concentrated the recent weakness has become within the global AI and semiconductor supply chain.

Fixed Income

The bond market’s reaction was one of the more counterintuitive developments of the week. Despite a hot year-on-year PCE print and a firmly hawkish Federal Reserve, Treasury yields moved lower. The 10-year yield eased to around 4.37-4.39% by Friday, down roughly 7 basis points on the week and near a seven-week low, while the 2-year finished around 4.10% and the 30-year near 4.87%.

Several factors drove the move. First, while headline PCE accelerated to 4.1% (YoY) and core PCE to 3.4% – both the highest readings since 2023 – the report was broadly in line with expectations, with monthly core inflation proving slightly softer than feared. Rather than forcing another repricing higher in yields, the data largely reinforced the Federal Reserve’s existing hawkish stance.

Second, the continued collapse in oil prices toward pre-conflict levels weighed on inflation breakevens and improved the medium-term inflation outlook. At the same time, weakness across equity markets prompted a rotation into Treasuries, creating a classic flight-to-quality bid. The result was a market that remains hawkish on policy but increasingly constructive on the longer-term inflation outlook.

Markets continue to assign a meaningful probability to an additional rate hike before year-end, with policy expectations across 2026 remaining materially tighter than they were only a few months ago. New York Fed President John Williams reinforced that view during the week, noting that while inflation is expected to moderate over time, it remains well above the Federal Reserve’s target.

The yield curve remained modestly positively sloped, with the 2s10s spread holding around +27bp and the 10-year/3-month spread near +62bp, consistent with a market pricing slower growth rather than outright recession. The front end remains anchored by the prospect of further policy tightening, while the long end has been supported by lower inflation breakevens and renewed demand for duration. The combination points to a market that continues to expect restrictive monetary policy in the near term, while becoming increasingly confident that the inflation impulse from the Middle East conflict is beginning to fade.

Cryptocurrency

Bitcoin extended its recent correction, breaking below US$60,000 on Thursday 25 June to its lowest level since 2024 before sliding into the weekend near US$58,980, down roughly 8% on the week and more than 50% below its October 2025 peak of US$126,080. Ethereum underperformed once again, falling to around US$1,560 as higher-beta digital assets remained under pressure. The weakness reflected a combination of factors: the hotter-than-desired PCE report reinforced expectations that US interest rates will remain restrictive for longer, while continued ETF outflows and growing concerns surrounding institutional positioning weighed on sentiment. Crypto traded largely in step with the Nasdaq as macro-driven risk aversion dominated price action.

The selloff triggered approximately US$1.48 billion of liquidations over a 24-hour period, with more than US$1.2 billion coming from long positions, highlighting the extent of the leveraged flush. By the weekend, Bitcoin was testing its 200-week moving average for the first time since October 2023—a level that has historically acted as an important long-term support zone and major cycle inflection point.

Strategy (MSTR) remained one of the market’s primary areas of focus, shifting from a background overhang to a much more closely watched source of risk. The company now holds approximately 847,000 BTC acquired at an average cost of around US$75,650 per coin. At current prices, the position is worth roughly US$50.7 billion against a cumulative acquisition cost of approximately US$64.1 billion, representing an unrealised loss of around US$13.4 billion. Importantly, these are mark-to-market losses on an unencumbered treasury rather than margin-financed positions, meaning there is no automatic liquidation mechanism. Nevertheless, the deterioration has intensified scrutiny of Strategy’s financing model and contributed to a more cautious tone across institutional crypto markets.

The market’s primary focus, however, has shifted to STRC. Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock is designed to trade close to its US$100 stated value and sits at the centre of the company’s Digital Credit funding platform. During the week, STRC fell to a fresh all-time low near US$71.84, leaving it trading at almost a 30% discount to par and highlighting growing investor concern around the sustainability of the capital structure.

The pressure is increasingly structural. Annual preferred dividend obligations have expanded to approximately US$1.2 billion, while the company’s cash reserves have declined to around US$1.4 billion, materially reducing its dividend coverage. Although Strategy retains substantial financial flexibility and there is no immediate liquidity event, investors are becoming increasingly focused on the long-term economics of maintaining its funding model if Bitcoin prices remain depressed.

Equally significant, MSTR common traded close to its underlying Bitcoin net asset value, with the multiple compressing toward 1.0x. That matters because Strategy’s accumulation model is most effective when its equity trades at a premium, allowing it to issue stock and acquire additional Bitcoin on an accretive basis. As that premium disappears, the efficiency of the funding flywheel is materially reduced, even though alternative financing avenues remain available. MSTR shares have now fallen roughly 36% over the past eight trading sessions and more than 80% from their July 2025 peak.

The key risk the desk is watching is the reflexive feedback loop developing around Strategy rather than an imminent forced liquidation. Perceived stress in Strategy’s capital structure encourages traders to hedge by shorting BTC, which pushes the Bitcoin price lower, increases the mark-to-market losses on Strategy’s treasury, places further pressure on STRC, and reinforces bearish sentiment. The cycle can become self-reinforcing even without any actual Bitcoin sales.

Importantly, Strategy still has several levers available before touching its BTC holdings. The company can adjust the STRC dividend, raise additional equity or preferred capital, or suspend STRC distributions at the Board’s discretion. It also faces no meaningful near-term debt maturities, making an immediate forced-sale scenario unlikely. Nevertheless, the longer BTC remains below Strategy’s average acquisition cost, the more challenging the coverage metrics become, and the greater the pressure on investor confidence.

Beyond Strategy, capital continues to rotate toward the AI complex at the expense of digital assets. Institutional positioning also remained under pressure, with a US$1.29 billion dark-pool block trade in BlackRock’s Bitcoin ETF widely interpreted as evidence of large-scale institutional repositioning rather than retail activity. Meanwhile, the longer-term adoption story continues to progress. Banca Sella became the first Italian bank operating under the Markets in Crypto-Assets Regulation (MiCA) framework to launch Bitcoin services for clients. While these developments reinforce the structural investment case, near-term price action continues to be dominated by liquidity conditions, institutional flows and macroeconomic expectations rather than fundamental adoption.

Technically, BTC continues to absorb supply in the US$58,000-59,750 region, but there is still little evidence that accumulation has been confirmed. A recovery through US$60,750 would be the first constructive signal, with the US$61,750-62,250 zone representing the next key resistance band. Initial support sits between US$58,000 and US$58,400, while a decisive break below US$59,250 would likely expose the large options interest clustered around US$55,000.

The near-term balance of risks remains skewed to the downside. Restrictive monetary policy expectations, continued capital rotation toward AI-related equities, and the reflexive pressure surrounding Strategy’s capital structure all remain headwinds for digital assets. Offsetting those risks are deeply washed-out positioning, the absence of any imminent forced selling from Strategy, and the continued decline in oil prices, which could ease inflation expectations and reduce pressure on interest rates if reflected in July’s inflation data.

The desk will be watching three key developments this week: whether BTC can continue to defend its 200-week moving average and the US$58,000 support zone; whether STRC begins to stabilise or its discount widens further; and Thursday’s US payrolls report, which is likely to be the next major catalyst for both rates and digital asset markets.

Emir Ibrahim, Analyst

Spot Desk

Risk sentiment remained defensive throughout the week as digital assets extended their downturn alongside broader markets. A hotter-than-expected May PCE print and increasingly hawkish Fed expectations reinforced the higher-for-longer rates narrative, weighing on liquidity-sensitive assets. Crypto-specific sentiment remained under pressure from continued ETF outflows, ongoing uncertainty surrounding Strategy’s Variable Rate Preferred Stock (STRC), and the continued rotation of speculative capital toward AI-related equities. Bitcoin (BTC) fell below US$60,000 for the first time since October 2024, with Ethereum (ETH) declining in tandem.

Desk activity reflected the softer market tone. BTC flows were more balanced than in recent weeks but retained a modest net selling skew, while ETH experienced more pronounced sell-side activity as overall participation continued to fade. Activity beyond the majors was subdued, with the breadth of client interest narrowing further after several weeks in which Solana (SOL) and selected higher-beta tokens had generated more constructive two-way flow. Overall, clients remained focused on liquidity preservation rather than deploying incremental risk.

In FX, AUD/USD weakened sharply, opening the week at 0.7011 and closing at 0.6895. Broad US dollar strength, driven by hawkish Fed repricing and higher US real yields, weighed on commodity-linked currencies, while the shift in US policy expectations continued to erode the yield-differential support that had benefited the Australian dollar earlier in the year. Market pricing has now largely transitioned from expecting policy stability toward a renewed tightening bias, with several major banks forecasting additional Fed rate hikes through 2026.

Domestically, the implied probability of the RBA lifting the cash rate to 4.60% at its next meeting eased from 31% to 19% following mixed inflation data. Headline CPI surprised to the downside, although trimmed mean inflation increased by 0.4% (MoM), lifting the annual rate to 3.6%. On the desk, AUD flows maintained a strong net buying bias as clients used the weaker exchange rate to off-ramp at size. Adoption of both AUDM and AUDD also continued to increase as AUD-denominated settlement rails became more deeply embedded within client treasury and settlement workflows.

Stablecoins again accounted for the majority of desk volumes. Continued off-ramping across both USDT and USDC into USD reflected the ongoing preference for dollar liquidity, with both stablecoins continuing to trade modestly below par in secondary markets amid subdued crypto demand. Elsewhere, EUR remained offered, while NZD and GBP both attracted net buying interest.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Ben Mensah, OTC Trader

Derivatives Desk

The defining feature of derivatives markets through the week ending 29 June was the sharp divergence between volatility and leverage. BTC’s move below the key US$60,000 level triggered a repricing across options markets, while futures and credit conditions remained comparatively orderly. The derivatives complex continues to point toward a liquidity-driven correction rather than a broad deleveraging event.

Options markets saw the largest adjustment. Front-end BTC implied volatility rose from the low-40% area into the high-40% range, with 1-month implied volatility lifting to around 45%. Risk reversals also moved materially further toward puts, with 1-week 25-delta skew widening to approximately 4-5% as demand for downside protection accelerated. The move reflects a repricing of near-term uncertainty rather than systemic stress.

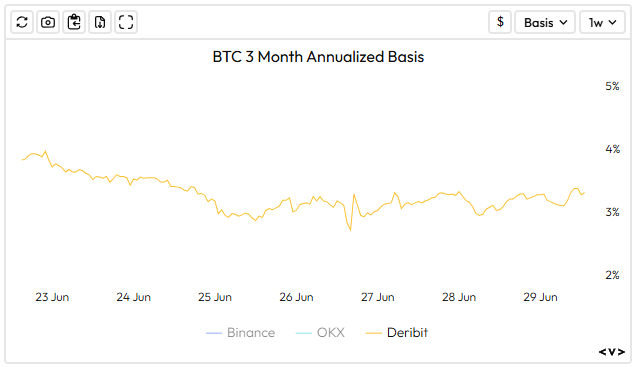

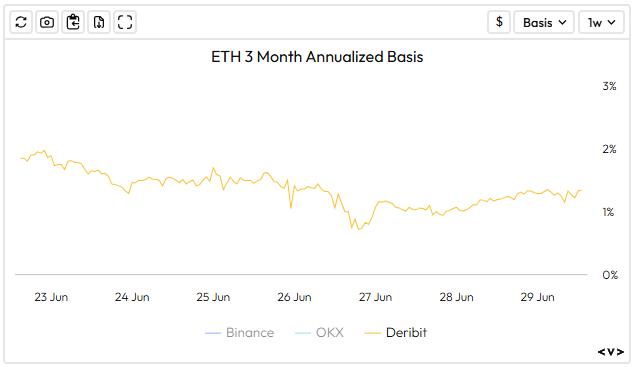

Carry markets remained comparatively resilient. BTC 3-month annualised basis held near 3.5%, up from around 2% a month ago, while ETH basis remained closer to 1.5%, reinforcing the divergence between BTC and broader crypto risk. Perpetual funding briefly moved negative before recovering to slightly positive levels, suggesting positioning was reduced rather than replaced by aggressive short exposure. Open interest declined only modestly and credit conditions remained orderly.

A developing market structure theme is the moderation in structural spot demand. ETF outflows, combined with Strategy’s slower pace of BTC accumulation, has reduced two of the market’s largest sources of incremental buying, leaving price action increasingly driven by discretionary institutional flows.

Technically, the loss of US$60,000 shifts focus toward support at US$55,000–56,000, while US$61,000–62,000 now becomes initial resistance ahead of US$65,000. Overall, options markets continue to price a wider distribution of near-term outcomes, while resilient funding, basis and credit markets suggest this remains a liquidity reset rather than a disorderly deleveraging cycle.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

What to Watch

Tue: RBA Meeting Minutes, ECB President Lagarde Speech

Wed: Fed Chair Warsh Speech, US JOLTs Job Openings

Thu: US Non Farm Payrolls, US Unemployment Rate, AU Balance of Trade

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.