19 May, 25

Weekly Crypto Market Wrap: 19th May 2025

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- Coinbase joins the S&P 500 on May 19, boosting its stock and market presence. Also faces a data breach with criminal theft, offering a $20M bounty, and staff leaks customer data refusing to pay ransom.

- Dubai partners with Crypto.com to enable crypto payments for government services, aiming for a 90% cashless goal by 2026.

- Animoca Brands plans a U.S. listing citing Trump’s crypto-friendly policies, aiming to capitalize on the current regulatory environment.

- JPMorgan’s $4 trillion asset manager completes first public blockchain transaction on Ondo with Chainlink, marking a major institutional adoption.

- Standard Chartered partners with FalconX to provide banking services and streamline cross-border crypto settlements for institutional clients.

- eToro goes public with a $52 per share IPO, surpassing expectations and experiencing a 29% surge on debut.

- DeFi Development Corp increases Solana holdings over $100 million with a purchase of 172,670 SOL, boosting its total assets.Mastercard partners with MoonPay to launch stablecoin cards enabling Bitcoin and stablecoin payments at 150 million merchants worldwide.

Technicals & Macro

BTCUSD

Key levels

66,000 / 72,000 / 92,000 / ~110,000 (just north of the all-time high)

The Monday Asia run

As we took our morning trading team meeting in the office, BTCUSD was rallying like a wild horse, much to the delight of our team. Bitcoin is approaching a ‘golden cross’, where the 50-day moving average crosses above the 200-day average – a pattern often seen as a bullish signal. Although its effectiveness is directly related to the media attention prior to the crossing.

As Bitcoin trades higher, the U.S. economy continues to grapple with the effects of recent trade policies, leading to further concerns about stagflation. If you want an insight into the tight spot US policymakers are in, check the consumer sentiment and inflation expectations survey from the University of Michigan data print. Sentiment expectations are their lowest since 1980, and expected 1-year inflation numbers came in at 7.3%. These are some wild numbers, and reflect the damage already done by Trump’s tariff policies, despite the backpedalling.

Combine this with Moody’s recent downgrade of the U.S. credit rating from AAA to AA1, citing rising federal debt and interest costs, has further shaken investor confidence. The result – higher Treasury yields, with the 30-year rate breaching 5%, and prompting a shift towards safe-haven assets like gold and, yes – Bitcoin. But is this a shift to a ‘safe haven’, or something else? The ole’ ‘risk free’ rate of US treasuries is not so risk free with the volatility we’ve been seeing. Our house view is that markets are bidding up bearer assets and scarcity in the face of US policy moves and the resulting US treasury volatility.

We are also seeing some magic in the institutional ecosystem though, don’t get me wrong. Coinbase has just entered the S&P500 – which opens up a potential wave of huge passive capital (ETFs, retirements funds, mutual funds etc..). Coinbase shares rallied 25% on the news – and we could go higher.

Technically on BTCUSD we are seeing higher daily lows above the 100,000 mark, and after this morning’s break above 107,000 – it’s actually a fairly clear run at the highs after price resets into the range and finds a new base. Do we break this week? Tough to tell – the US macro docket is fairly light, although the weekly unemployment claims may provide a little fire either way.

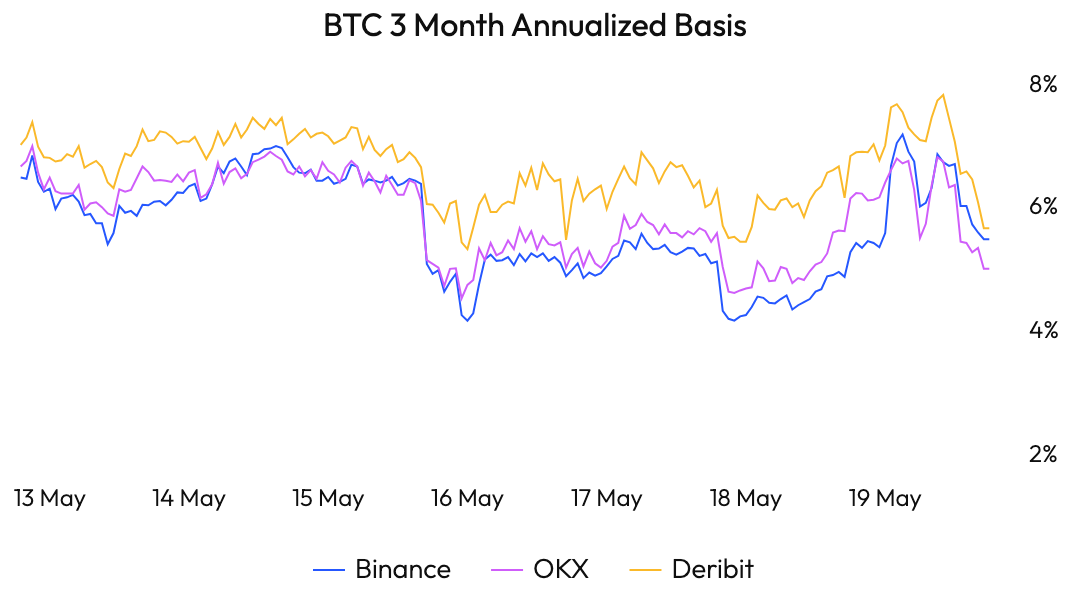

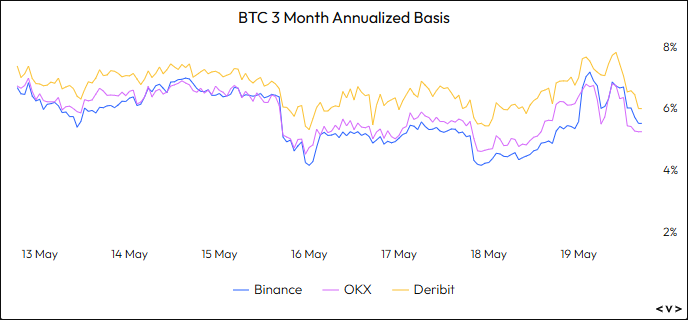

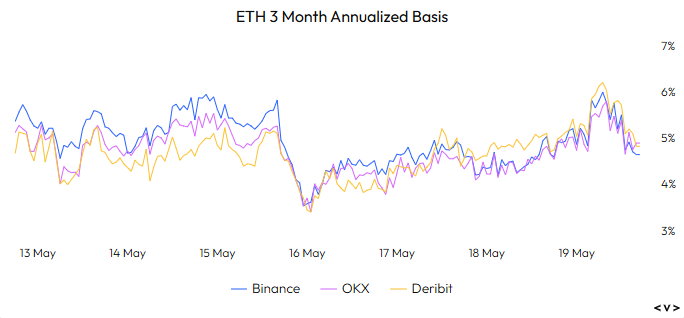

3M basis falling away despite the spot move higher. We have seen some limited liquidations, and I still position that leverage could go much, much higher on a move above the all-time high. My hedge fund buddy reminded me last week that the ETF issuers and market makers have been getting short futures and long spot to maintain delta-neutrality – unwinding the futures positions as we go higher. Given the quantum of ETF flows, this makes sense.

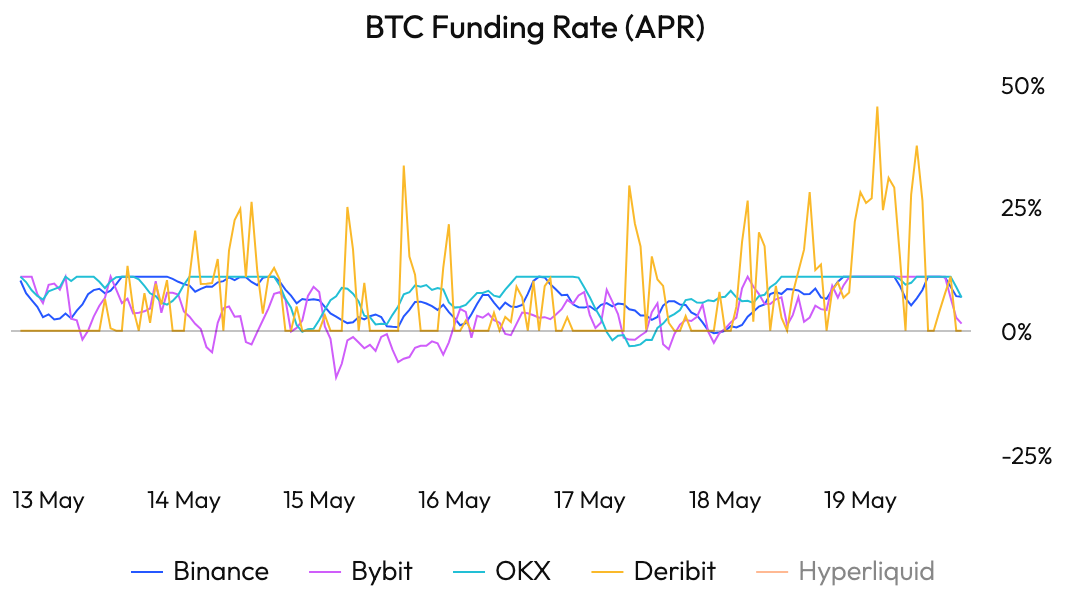

Perp funding rates – muchos room to move. Retail and the speculative crowd not in this trade at scale, just yet.

NASDAQ/BTC

Compression, compression. Bitcoin taking centre stage on the equities / BTC ratio.

DXY struggling for direction.

We are chopping up the shorter-term traders here. No love around that descending trendline, which is now invalidated. The USD is a weird one right now – I don’t wanna be long, and I don’t wanna be short..

Gold trading like a dream

Gold is trading technically so well at the moment. It’s a natural hedge as a safe haven, but also as we’ve mentioned, a bearer asset. Keep a close eye ona move back into the higher range if US data continues to surprise.

ETHUSD

ETHBTC

ETH actually hanging in there – the Decun upgrade has kept some buoyancy, but for how long? BTC has the momentum right now – be careful betting against it. Standard Chartered are still calling for 200,000 by the end of 2025 – and we tend to agree. Blink and you might miss it.

Stay safe out there.

Jon de Wet, CIO

Spot Desk

Market sentiment remains positive as Bitcoin continues its upward trajectory, closing out the week with its highest ever weekly close above 106k and approaching its January peak of 109k. BlackRock and Fidelity have seen continued capital growth into the spot Bitcoin ETFs since April. These inflows suggest growing confidence among institutional investors who are beginning to view Bitcoin as a viable long-term asset class, particularly amid persistent inflation and geopolitical uncertainty.

The desk noticed somewhat balanced two way AUD/USDT flows throughout the week with a skew towards the offer as AUD/USD closed out the week -0.08%. There’s an interest rate cut priced in this week from the RBA – but it’ll be the accompanying statement that drives AUD either way.

Our clients were bidding up small cap altcoins such as EUL, MPLX and GEOD in addition to showing some buying interest in majors BTC and ETH. We saw a noticeable pick up in demand on the bid for USDT/USD with no signs of slowing down, and spent the majority of the week axed to sell USDT. This demand is likely to continue, and when we are skewed heavily on one side of the book we can offer extremely favourable rates on both USDT/AUD and USDT/USD pairs. Feel free to hit up the OTC desk through the live chat on the Zerocap portal any time to discuss any enquiries surrounding our axes!

The OTC desk continues to offer tailored cryptocurrency liquidity solutions, offering competitive pricing across major coins, altcoins, and memecoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Oliver Davis, OTC Trader

Derivatives Desk

WHOLESALE INVESTORS ONLY*

BTC and ETH basis rates have remained historically stable despite the recent rally in spot prices, suggesting that market leverage remains contained for the time being.

BTC 6%, ETH 4.88%

Trade Idea: ETH Discount Note

Given the recent change in ETH sentiment, now might be a good time to consider gaining some exposure to ETH. One way to play it would be to enter the market at a discounted level via a Discount Note.

OVERVIEW

Term: 6-Months

The structure has a binary payout outcome depending on the price of ETH observed at expiry. Payout for this options strategy depends on the price of ETH at expiry with reference to the Strike Level – the two scenarios are:

Expiry Price above Strike Price (25% above current price):

- Maximum return of 36% – received in USD.

Expiry Price below Strike Price:

- 8% discounted purchase price at current levels into the ETH token – received in Spot.

RISK PROFILE

- Maximum loss for this product is the initial investment amount.

- May suit investors with a stable to moderately bullish view on ETH.

- May not suit investors who think a major bull run in ETH is likely before expiry.

- May not suit investors who think ETH will fall significantly before expiry.

Hit the desk up for all your derivatives needs.

Austin Sacks, Derivatives Analyst

What to Watch

This week is macro-heavy with a dovish tilt. China and Australia central banks lean into easing, while inflation reports from the UK and Japan may complicate their respective central bank paths. PMIs offer key insight into real-economy spillovers from tariffs. Traders should watch AUD and CNY for policy-driven moves, and GBP and JPY for inflation surprises.

Monday, 19 May – EU-UK Summit; China Activity Data

- EU-UK Summit: London hosts a reset dialogue—defence, fishing rights, and youth mobility dominate. Limited market impact unless US/EU dynamics are affected.

- China (Apr): Industrial Output and Retail Sales expected to soften (IP seen at 5.5% YoY), capturing first effects of last month’s tariffs. Sentiment buoyed by recent 90-day truce, but structural issues in consumption and property remain.

Tuesday, 20 May – PBoC LPR, RBA, Canadian CPI

- PBoC LPR: Expected 10bps cut, following earlier RRR and policy rate moves. China easing bias firmly in play.

- RBA: Market prices a 25bps cut (98% odds), with NAB calling for 50bps. Macro data and subdued inflation support easing despite cautious prior rhetoric.

- Canada CPI: April print to guide BoC expectations. Market leans toward two cuts by year-end; Tuesday’s inflation read critical.

Wednesday, 21 May – UK CPI

- UK inflation seen spiking to ~3.6% (prev. 2.6%) on regulated price resets and tariff pass-through. BoE focus stays on summer cuts, but risks skewed to the upside.

Thursday, 22 May – ECB Minutes; Flash PMIs

- ECB Minutes: From April’s 25bps cut—watch for signals on June. Lagarde dismissed larger cuts; attention on discussion tone and growth concerns.

- Flash PMIs (EZ, UK, US): PMIs to gauge trade war drag vs. stimulus tailwinds. EZ Composite expected to hold above 50. UK Composite risks another contraction; services weakness a key watch.

Friday, 23 May – Japanese CPI, UK Retail Sales

- Japan CPI: Core seen at 3.4% YoY. Tokyo data flagged upside; inflation stickiness may pressure BoJ policy path despite global headwinds.

- UK Retail Sales: April data to reflect early Trump tariff effects. Solid weather and wage gains may support a 0.3% MoM lift, but price sensitivity is rising.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | Treasury Yields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 27 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 20 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.