18 May, 26

Weekly Crypto Market Wrap: 18 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- U.S. spot BTC ETFs saw ~US$1B in outflows; ETH ETFs saw ~US$255.1M in outflows.

- eToro Q1 crypto contributions drop to US$13 million even as trading platform grows

- Strategy to retire US$1.5 billion in convertible notes at a discount

- Harvard dumps ether ETF as Abu Dhabi sovereign fund keeps adding to bitcoin positions

- Hyperliquid Policy Center argues onchain perps offer efficiency, transparency as ICE and CME reportedly press for CFTC oversight

Technicals & Macro

Markets

Market conditions reversed sharply over the past week as stronger-than-expected inflation data and renewed policy uncertainty challenged the rally in risk assets. U.S. equities printed fresh all-time highs on Thursday – with the S&P 500 closing above 7,500 for the first time and the Dow reclaiming the 50,000 level – before reversing sharply into Friday as markets reassessed the inflation and policy backdrop. Three developments drove the move. First, Tuesday’s April CPI release came in firmer than expected, with headline inflation rising 3.8% (YoY) versus 3.7% consensus and 0.6% (MoM). Energy prices increased 17.9% (YoY), reinforcing expectations that the recent Iran-related energy shock is now feeding into headline inflation. Core CPI also exceeded expectations, rising 0.4% (MoM) and 2.8% (YoY), suggesting underlying price pressures remain more persistent than markets had anticipated.

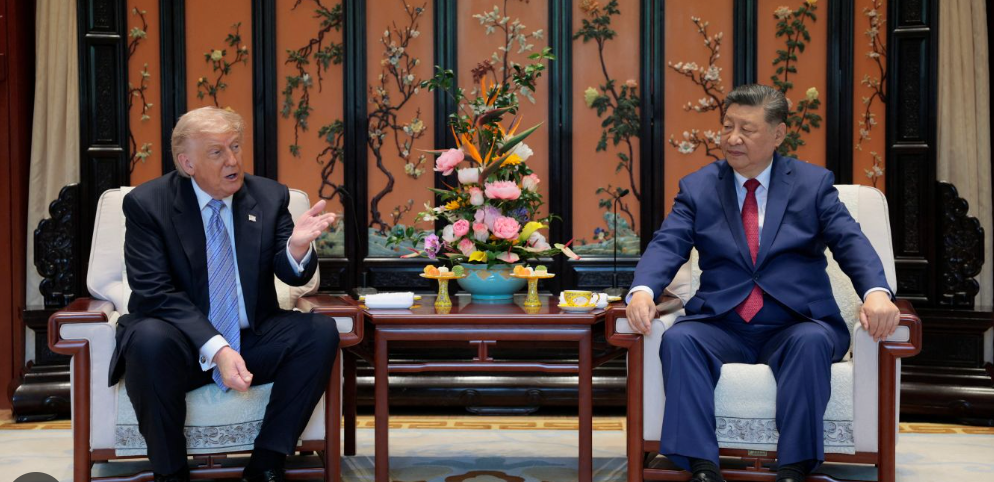

Source: CNN

Second, the Trump–Xi summit in Beijing on Wednesday and Thursday delivered little in the way of substantive policy breakthroughs despite more than two hours of bilateral discussions. The primary commercial outcome was a reported 200-aircraft Boeing order, below broader expectations for a larger agreement, alongside Chinese commitments to increase purchases of U.S. energy exports. While President Trump characterised the discussions positively, no major agreements were formally announced. More importantly for markets, strategic tensions remained evident beneath the diplomatic optics. Xi warned that any mismanagement of Taiwan risked “clashes and even conflicts,” while U.S. officials separately confirmed that Washington was not seeking Chinese assistance in relation to Iran, underscoring the continued geopolitical distance between the two sides despite the summit.

Third, geopolitical tensions re-escalated late in the week after President Trump warned that the Israel–Lebanon ceasefire was on “massive life support,” while renewed military clashes in the Strait of Hormuz on Friday reinforced concerns that the broader de-escalation narrative may be deteriorating. Rates markets reacted aggressively. The 10-year U.S. Treasury yield rose 28bp on the week to 4.58% – its highest level since September 2025 – as fed funds futures repriced materially toward a more restrictive policy path, with markets reducing expectations for easing and beginning to price a non-trivial probability of further tightening.

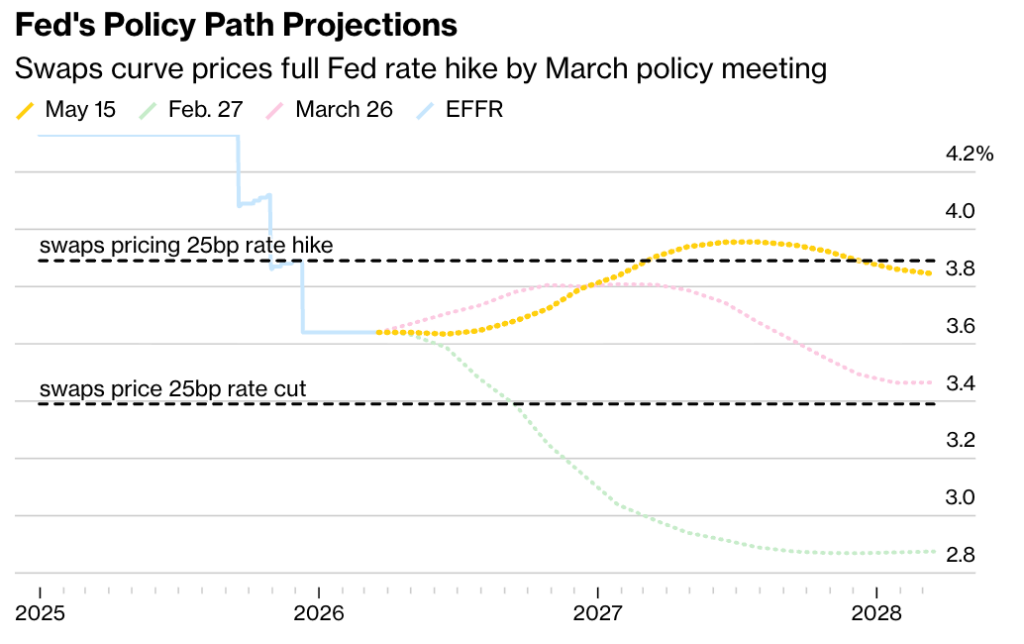

Source: Bloomberg

The Powell era formally concluded on Friday, with Jerome Powell’s term as Federal Reserve Chair ending on May 15 and Kevin Warsh sworn in over the weekend as his successor. Powell will remain on the Board of Governors through January 2028, limiting any immediate shift in the Committee’s overall policy balance. Warsh is set to chair the June 16–17 FOMC meeting, which will include updated Summary of Economic Projections and a revised dot plot — providing markets with the first formal insight into the policy outlook under his leadership.

The threshold for a hawkish repricing has fallen materially following the stronger-than-expected CPI release and renewed upside pressure in energy markets. Markets now price no rate cuts through 2026 and have begun, at the margin, to consider the possibility that the next policy move could ultimately be another hike rather than an easing cycle. Reinforcing that shift, the Empire State Manufacturing Index rose sharply to 19.6 in May versus expectations of 7.0, marking its strongest reading in more than four years. The release was also accompanied by a notable acceleration in the prices paid component, adding to the broader inflationary signal ahead of Warsh’s first meeting as Chair.

Equities

The S&P 500 reached an intraday all-time high of 7,517.12 on Thursday before reversing sharply on Friday, falling 109 points on the session. The Nasdaq Composite similarly traded to a fresh high near 26,707 before giving back gains into the close. The rally through most of the week continued to be led by AI-linked hyperscalers and semiconductor names. Cisco exceeded fiscal Q3 expectations and raised guidance, while Cerebras Systems surged 68% in its Nasdaq debut on Thursday, marking one of the largest AI-focused IPOs in recent years. The Dow also reclaimed the 50,000 level for the first time since February.

Friday’s reversal was led by AI-linked technology and semiconductor equities as higher Treasury yields and firmer inflation data pressured duration-sensitive growth exposure. Nvidia fell 4.4%, AMD declined 5.7%, Micron dropped 6.6%, Intel lost 6.0%, and Cerebras retraced roughly 10% following its post-IPO surge.

Fixed Income

The 10-year U.S. Treasury yield surged 28bp on the week to 4.58%, its highest level since September 2025, with the move accelerating following Tuesday’s hotter-than-expected CPI release and extending through the remainder of the week amid rising energy prices and renewed deterioration in the Iran ceasefire backdrop. The long end also came under sustained pressure, with the 30-year U.S. Treasury yield moving back above 4.95% as markets repriced inflation risk and reduced expectations for policy easing.

A 28bp weekly rise in the 10-year U.S. Treasury yield, combined with oil moving back above US$100/bbl, has materially altered the market’s rate-cut narrative. Some desks are now openly modelling the possibility that Warsh inherits a Federal Reserve facing renewed tightening risk rather than an easing cycle. Fed funds futures have effectively removed all expected cuts through 2026, with the first fully priced 25bp cut now pushed into late 2027, while probabilities of an additional hike by end-2026 have begun to build at the margin.

The curve has also steepened meaningfully, with the 2s10s spread widening as markets increasingly price a combination of resilient growth and elevated inflation risk at the long end. Supporting that view, April retail sales rose 0.5% (MoM) versus expectations of 0.6%, while the sharp rebound in the Empire State Manufacturing Index reinforced evidence that economic activity remains relatively firm despite tighter financial conditions. Taken together, the data continue to complicate the inflation outlook and reduce confidence in a near-term policy easing cycle.

Commodities

WTI closed the week at US$102.74/bbl, up 4.4%, while Brent settled at US$110.47/bbl, up 5.2% on the week. Both benchmarks moved sharply higher on Friday following President Trump’s confirmation that China would increase purchases of U.S. crude exports – a development markets’ interpreted as supportive given ongoing disruption risks in the Strait of Hormuz – alongside renewed military exchanges in the region.

Despite several weeks of diplomatic positioning, the Strait remains effectively constrained from a shipping and supply-flow perspective. Elevated tanker congestion within the Gulf, combined with reduced spare capacity across key regional producers, continues to reinforce a structural risk premium in crude markets and provide support for prices remaining above the US$100/bbl level.

Cryptocurrency

Despite Bitcoin closing Friday at US$77,758, down 5.4% on the week following a sharp late-session reversal, the broader narrative was initially one of resilience before signs of macro fatigue began to emerge. BTC successfully defended the US$80,000 level through Tuesday’s hotter-than-expected CPI release, trading within an intraday range of roughly US$80,415 – US$82,084 even as ETH and broader altcoins experienced more pronounced selling pressure. That relative stability continued to reflect the structural ETF bid that has underpinned spot demand in recent weeks.

Performance across the altcoin complex was notably mixed. SKYAI, BUILDon, Humanity and Injective were among the stronger performers, while Aerodrome Finance, Ondo, Virtuals Protocol and Pudgy Penguins lagged materially. SAGA rose 56.6% and Solv Protocol gained 25.5%, while Osmosis declined 36.7%. More notably, XRP and SOL linked ETF products continued to attract stronger institutional demand even as ETH ETF flows remained negative, providing early evidence that institutional crypto allocations may be broadening beyond a predominantly Bitcoin-centric framework.

Crypto-linked equities underperformed spot markets throughout the week, with miners such as MARA and CleanSpark falling more than 10%, reflecting both operating leverage to underlying crypto prices and broader sensitivity to deteriorating risk sentiment. Elsewhere, tokenisation-related developments remained supportive at a structural level, with droppRWA reportedly securing US$12.5bn in tokenised real estate mandates and outlining plans to expand into broader real-world asset categories.

The technical setup into next week remains finely balanced. BTC’s US$76,000 – US$78,000 region — the breakout zone established during the Hormuz-related rally six weeks ago — now represents the key near-term support area. A sustained hold through Nvidia’s earnings release on Wednesday and any further rise in Treasury yields would reinforce the structural demand narrative. Conversely, a break below US$75,000 risks exposing the US$70,000 – US$72,000 region, while upside resistance is now more clearly defined around US$82,000.

Fundamentally, the longer-term backdrop remains constructive. Cumulative spot ETF inflows remain near US$58bn, exchange reserves continue to sit near multi-year lows, and large-holder accumulation trends remain intact. However, with the 10-year U.S. Treasury yield at 4.58% and oil prices back above US$100/bbl, crypto markets are now being forced to absorb genuine macro tightening pressures rather than benefiting from the combination of falling yields and geopolitical de-escalation that supported the earlier rally phase. Even so, relative performance through Friday’s broader technology-led sell-off was comparatively constructive, reinforcing the emerging view among some investors that Bitcoin may be beginning to trade with greater resilience during periods of geopolitical and macro stress.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

The past week saw broad de-risking across digital assets as tighter financial conditions and rising yields weighed on liquidity-sensitive risk assets. The move was largely macro-driven rather than reflective of crypto-specific deterioration, although recent technical breakdowns have left overall positioning more defensive.

Desk flows continued to exhibit a countertrend dynamic through the week. BTC recorded a modest net buying skew as lower prices attracted selective deployment, while Solana (SOL) remained the preferred expression of altcoin risk appetite and extended its consistent buy-side skew. ETH participation remained materially lighter than both BTC and SOL, reflecting weaker relative performance and limited conviction around ETH as a higher-beta allocation.

PAXG activity strengthened relative to recent weeks. Despite spot gold softening into Friday’s close amid firmer yields and USD strength, demand for tokenised gold remained firm, consistent with continued geopolitical hedging and collateral rotation activity.

Within the longer-tail segment, Hyperliquid (HYPE) materially outperformed the broader market, rallying to six-month highs following Coinbase’s acquisition of Native Markets’ USDH brand assets. Venice (VVV) and Zcash (ZEC) also outperformed as AI and privacy-related narratives regained momentum, although strength across the long-tail remained highly ‘event’ and ‘narrative’ driven rather than indicative of broad-based risk re-expansion.

In FX, AUD/USD briefly revisited recent highs near 0.7271 on Australia’s Federal Budget release before reversing sharply lower to close near 0.7144. The Budget itself was largely interpreted as a relative non-event for spot FX markets, with proposed reforms to capital gains tax, negative gearing and trust income taxation generating limited immediate market impact.

Elsewhere, desk flows saw EUR firmly offered, NZD bought, and sizable off-ramping flows from stablecoins into USD. AUDD participation remained meaningful and skewed toward the offer as clients continued to utilise AUD-denominated stablecoins, including AUDD and AUDM, as alternatives to traditional fiat settlement rails.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins and selected altcoins alongside key fiat currency pairs. With T+0 settlement, we continue to facilitate seamless execution and settlement across client flows.

Ben Mensah, Trading Analyst

Derivatives Desk

Derivatives markets remained largely range-bound through the week ending 18 May, with positioning stable and leverage conditions broadly unchanged as macro liquidity conditions remained the dominant constraint on risk-taking. BTC continued to consolidate in the high US$70,000 range while aggregate futures open interest dipped modestly, remaining well below earlier-cycle levels seen during more aggressively leveraged phases of the market.

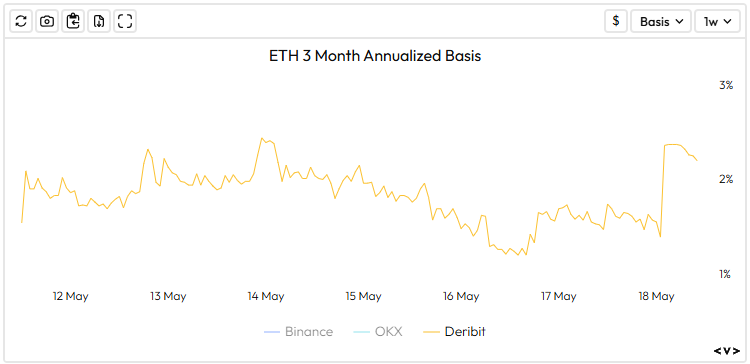

Funding conditions across major venues stayed near neutral to modestly constructive, with BTC perpetual funding holding around flat to low single-digit annualised levels. The 3-month basis was a relative outperformer, firming into the ~2–3% annualised range, and looked to be a sign of very slight credit adjustment rather than stronger speculative positioning.

The dominant macro driver over the week was the repricing of the U.S. Treasury curve following firmer inflation prints and resilient activity data. U.S. yields moved higher over a matter of sessions, with the 10-year pushing toward ~4.5 – 4.6%, while real yields moved back into restrictive territory relative to neutral estimates. The tightening in real rates remains a key transmission mechanism for crypto markets, with higher real yields suppressing leverage appetite and constraining liquidity-sensitive risk-taking across digital assets.

Volatility markets remained anchored, with BTC 1-week ATM implied volatility trading around 36% and the term structure flat through the 3-month tenor in the high-30% range. The absence of meaningful vol expansion alongside higher yields and geopolitical uncertainty points to limited positioning and subdued reflexivity. ETH continued to underperform BTC across both spot and derivatives markets, with softer funding, elevated relative implied volatility, and sustained pressure in the ETH/BTC cross near 0.0275, consistent with ETH behaving as a higher-beta macro risk proxy in a tightening liquidity window.

Overall, derivatives markets continue to reflect balanced positioning and subdued directional conviction, consistent with a macro regime defined by tighter global liquidity conditions and elevated real rates.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

What to Watch

Tues: RBA Meeting Minutes, JPY GDP QoQ & YoY

Wed: EU CPI MoM, YoY

Thu: FOMC Minutes, US Initial Jobless Claims, AU Unemployment Rate (Apr)

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 22 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.