22 Jun, 26

Weekly Crypto Market Wrap: 22 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

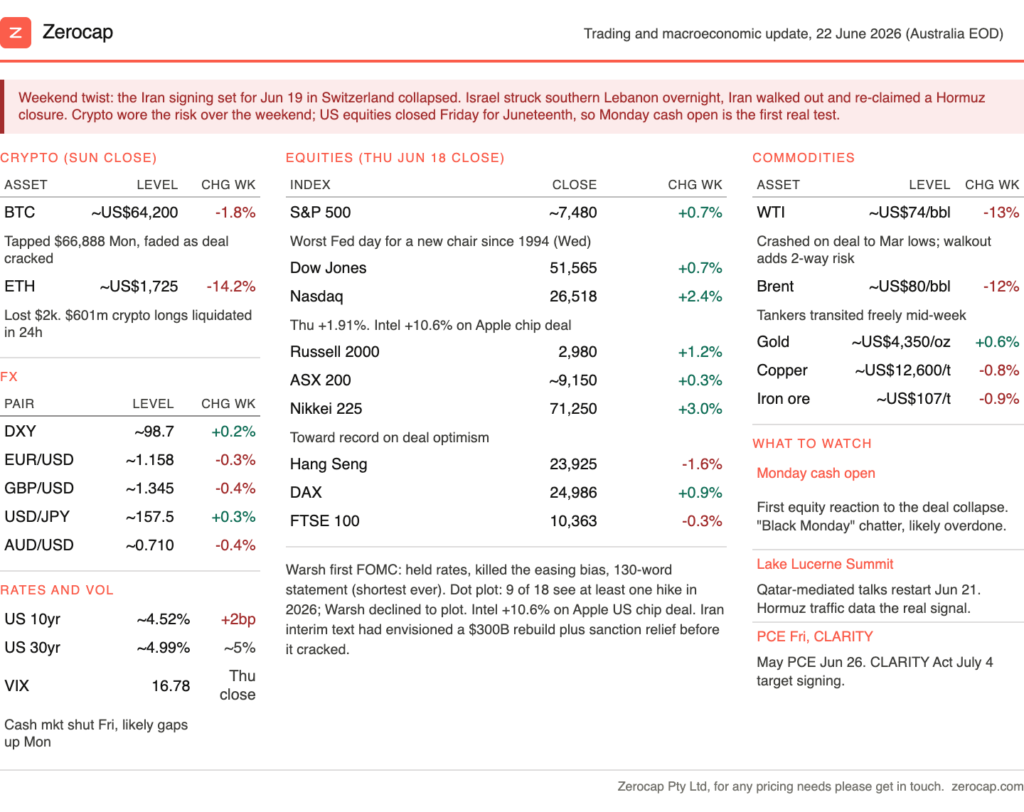

Week in Review

- The US-Iran interim peace deal, which had looked complete on 14 June, collapsed over the weekend after Israel struck southern Lebanon and Iran walked out of the Switzerland signing.

- US markets were closed Friday for Juneteenth, leaving Monday’s cash open as the first test.

- Strategy filed an amended STRC certificate on 15 June moving its preferred dividend from monthly to semi-monthly, effective 30 June.

- A Paxos subsidiary became the first company to receive its specific registration from the SEC.

Technicals & Macro

Markets

Two events dominated markets last week: Chair Kevin Warsh’s first FOMC meeting and the subsequent collapse of the proposed US-Iran peace agreement over the weekend.

The Federal Reserve left rates unchanged at 3.50-3.75% on Wednesday, but Warsh’s debut marked a notable shift in tone. The post-meeting statement was significantly shorter than under the previous regime, consistent with his long-held preference for more limited forward guidance. More importantly, the easing bias that had characterised prior communications largely disappeared, while the updated dot plot shifted modestly more hawkish. Nine of the eighteen participating policymakers now project at least one rate increase by the end of 2026. Warsh, who has previously criticised the dot plot as a policy communication tool, did not submit his own projection. Markets interpreted the meeting as incrementally hawkish, with equities weakening into the close and rate expectations shifting modestly higher. The broader takeaway was that inflation remains sufficiently elevated for policymakers to maintain a cautious stance despite recent improvements in energy markets.

Attention then shifted to the Middle East. The interim US-Iran agreement, which had appeared close to completion following President Trump’s announcement on 14 June, was scheduled for formal signing on 19 June in Switzerland. Draft terms reportedly included provisions relating to the reopening of the Strait of Hormuz, the easing of maritime restrictions, reconstruction assistance and a pathway toward broader sanctions relief contingent on future nuclear negotiations.

Instead, the process deteriorated over the weekend. Renewed military activity in the region led to the postponement of the signing ceremony, while public statements from both sides suggested negotiations had become increasingly fragile. Iran subsequently indicated it would not return to talks under the current framework, while regional mediators, including Qatar, moved to preserve dialogue through a new round of discussions scheduled for later in June.

With US markets closed on Friday for Juneteenth, investors had limited opportunity to react to the breakdown. As a result, Monday’s reopening is likely to provide the first meaningful test of market sentiment following the renewed geopolitical uncertainty. While concerns around a broader risk-off move have emerged across social media and retail channels, the continued involvement of regional mediators suggests that negotiations have been delayed rather than definitively abandoned.

Stock Markets

Source: TradingView

Through Thursday’s close, the week had been broadly constructive for risk assets, which makes the weekend developments particularly significant. The Nasdaq Composite rose 2.4% on the week to 26,518, supported by a 1.9% gain on Thursday alone, while the Dow added 0.7% to 51,565 and the S&P 500 gained approximately 0.7% to around 7,480. The Russell 2000 advanced 1.2% to 2,980.

The standout individual performer was Intel, which rose 10.6% after President Trump announced the company would design and manufacture semiconductors domestically in partnership with Apple, reinforcing the broader US onshoring and strategic manufacturing narrative. Within the Dow, Caterpillar, Disney and Nvidia led gains on Thursday, while IBM, Johnson & Johnson and JPMorgan underperformed.

The late-week rally reflected a combination of continued strength in technology shares and growing optimism that a formal US-Iran agreement would be signed on Friday. International markets displayed a similar pattern. Japan’s Nikkei advanced approximately 3% on the week and approached record highs, Germany’s DAX gained 0.9%, while Hong Kong’s Hang Seng declined 1.6% and the UK’s FTSE 100 slipped 0.3%.

With US markets closed on Friday for Juneteenth, investors were unable to react to the subsequent deterioration in negotiations. As a result, Monday’s reopening will provide the first meaningful test of whether the improvement in risk sentiment observed throughout the week can be sustained in the face of renewed geopolitical uncertainty.

Fixed Income

The rates complex was primarily driven by Chair Kevin Warsh’s first FOMC meeting. The removal of the easing bias and a more hawkish dot plot pushed the front end modestly higher, while the 10-year Treasury yield remained anchored around 4.52% and the 30-year finished just below the 5.00% threshold at approximately 4.99%. Markets continue to price a prolonged hold in policy rates, with expectations for easing pushed further into the future following the meeting. The updated projections also reinforced a more hawkish policy outlook, with nine of eighteen participants now forecasting at least one rate increase by the end of 2026.

The key tension for rates markets remains the interaction between monetary policy and energy prices. On one side, elevated inflation and a more hawkish Federal Reserve support a higher-for-longer policy stance. On the other, the sharp decline in oil prices during the week had begun to improve the inflation outlook and, if sustained, could have supported softer headline inflation readings through the middle of the year. The deterioration in US-Iran negotiations over the weekend complicates that narrative. A renewed rise in oil prices driven by concerns around the Strait of Hormuz would challenge the disinflationary impulse that markets had begun to price and reduce the scope for any near-term moderation in policy expectations.

Attention now turns to the May PCE release on 26 June, which remains the Federal Reserve’s preferred inflation measure, although it is likely to lag the most recent moves in energy markets. Credit spreads remain relatively contained, suggesting markets continue to view recent moves as a repricing of expectations rather than a broader stress event.

Cryptocurrency

Bitcoin reached a seven-day high of US$66,888 on Monday as optimism surrounding the proposed US-Iran agreement carried over from the prior weekend, before fading through the week as the Federal Reserve adopted a more hawkish tone and attention turned to the scheduled signing. Following the collapse of negotiations over the weekend, BTC briefly fell to around US$62,200 before stabilising near US$64,200 by Sunday, leaving it down approximately 1.8% on the week.

The weakness was more pronounced across higher-beta digital assets. ETH decisively lost the US$2,000 level, falling approximately 14% to around US$1,725, while Solana traded near US$70 and XRP around US$1.15. The weekend move triggered approximately US$601 million of long liquidations across digital asset markets over a 24-hour period, compared with just US$85.6 million of short liquidations, highlighting a predominantly one-sided unwind of bullish positioning rather than a broad increase in two-way volatility. The episode again reinforced BTC’s tendency to trade as a high-beta risk asset during periods of macro uncertainty, with price action closely aligned to broader shifts in risk sentiment throughout the Iran negotiations.

Strategy remained one of the most closely watched names in the digital asset ecosystem, with particular attention focused on its STRC preferred securities. Investor interest reflects the role these instruments play in funding Strategy’s broader Bitcoin acquisition programme and, by extension, the sustainability of its balance-sheet model. While STRC continues to trade below its stated value, market concerns around near-term funding stress eased somewhat following the stabilisation in BTC prices. Nevertheless, the preferred complex remains an important sentiment indicator, as any deterioration in pricing or dividend coverage could reignite concerns around future capital raising requirements and their potential implications for Strategy’s Bitcoin treasury strategy.

Two STRC developments framed the week. First, Strategy amended the security’s Certificate of Designations following shareholder approval earlier in June, moving dividend payments from monthly to semi-monthly effective 30 June. The change does not alter the dividend rate or total distribution amount but is intended to smooth cash flows and reduce the recurring post-dividend weakness that had weighed on trading.

Second, the market continues to assess Strategy’s late-May sale of 32 BTC (approximately US$2.5 million), the company’s first Bitcoin sale in nearly four years. While the transaction initially fuelled concerns around funding pressure, subsequent actions have pointed in the opposite direction. Strategy disclosed the purchase of an additional 1,587 BTC between 8 and 14 June for approximately US$100 million at an average price of US$63,024 per coin, reinforcing the view that accumulation remains the primary objective.

The broader takeaway is that concerns around near-term funding stress have eased materially. With a substantial USD reserve and the ability to adjust the STRC coupon through its variable-rate mechanism, the market’s earlier forced-seller narrative appears less compelling than it did immediately following the initial sale. That said, STRC remains an important sentiment indicator and will continue to be closely watched if BTC remains under pressure for an extended period.

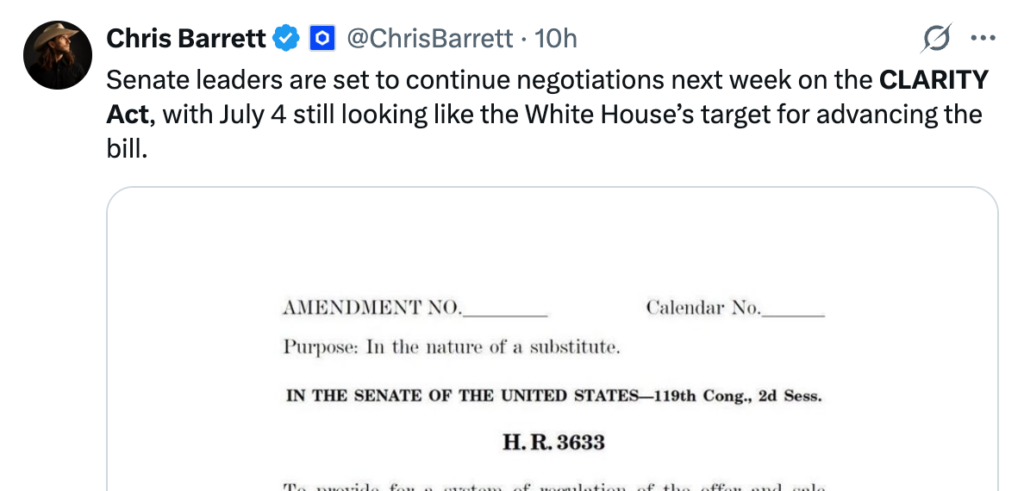

Source: X.com | Chris Barrett

On the regulatory front, the CLARITY Act remained one of the most important structural catalysts for digital assets. Following its advancement through the Senate Banking Committee, attention has shifted toward the legislative timetable and the likelihood of broader bipartisan support. While debate continues around the treatment of stablecoin rewards and yield-bearing products, the direction of travel remains broadly constructive for the industry. Markets continue to view regulatory clarity around digital asset classifications and market structure as a necessary precondition for deeper institutional participation, making progress on The Bill an increasingly important medium-term driver of sentiment.

Technically, BTC is testing the lower half of the US$60,000-US$65,000 range that has developed since the post-FOMC stabilisation. A recovery through US$65,800 would improve near-term momentum, while a move back above US$70,000 would strengthen the case that a durable low is in place. For now, however, the broader structure remains characterised by lower highs and lower lows relative to late-2025 levels, and the market remains well below the major resistance zone around US$80,000. On the downside, a sustained break below US$60,000 would bring the May cycle low near US$59,100 into focus, followed by support in the low-US$50,000s.

The setup into Monday remains finely balanced. The collapse of the Iran agreement is a clear near-term headwind for risk assets, but sentiment remains deeply pessimistic, positioning has largely reset following the recent liquidation event, and leverage conditions remain subdued. Against that backdrop, a constructive geopolitical headline, softer-than-expected inflation data, or further regulatory progress could trigger a meaningful relief rally precisely because expectations have become so defensive.

Emir Ibrahim, Analyst

Spot Desk

Risk sentiment remained cautious throughout the week as markets digested a combination of central bank developments and ongoing geopolitical uncertainty in the Middle East.

In the United States, the FOMC left interest rates unchanged at 3.50%-3.75%. Market attention was focused on Kevin Warsh’s first press conference as Chair of the Federal Reserve, where he reiterated that price stability remains the Fed’s primary objective and indicated policymakers remain prepared to respond should inflationary pressures persist. Markets interpreted the meeting as relatively hawkish, with expectations for policy easing pushed further into the future. Warsh also announced a broad review of the Federal Reserve’s policy framework and decision-making processes, signalling the potential for meaningful institutional changes over coming years.

Geopolitical developments remained a significant driver of sentiment. Negotiations between the US and Iran continued throughout the week, although progress was complicated by ongoing conflict involving Israel and Hezbollah in Lebanon. Markets also remained sensitive to developments surrounding the Strait of Hormuz given the implications for global energy markets, inflation expectations and broader risk appetite.

Domestically, the RBA left the cash rate unchanged at 4.35% in a unanimous decision. While recent data has pointed to slower growth and some moderation in labour market conditions, the Bank maintained that inflation remains above target and that policy must remain sufficiently restrictive. The decision was broadly in line with expectations. Upcoming inflation data will be closely watched, although current market pricing suggests any material shift in the RBA’s outlook remains unlikely in the near term.

Digital asset markets traded lower over the week as macroeconomic uncertainty weighed on sentiment. BTC (-3.7%) closed at US$63,310, while ETH (-1.1%) finished at US$1,707. Solana outperformed the broader market, gaining 1.6% to close at US$72.46. In stablecoins, USDT continued to trade modestly below parity, reflecting abundant secondary-market liquidity. USDC also traded at a discount to redemption value, although the move remained orderly and primarily reflected broader market liquidity dynamics rather than concerns around the underlying issuer.

On the desk, client flow was dominated by stablecoin selling, with USDT accounting for the majority of activity and USDC displaying a similar bias. FX flow was led by AUD demand, alongside more modest buying interest in USD, EUR and NZD. Crypto activity remained relatively light, with modest net buying in BTC while ETH recorded a net selling skew. Participation across smaller-cap digital assets was limited.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Oliver Davis, OTC Trader

Derivatives Desk

The most significant development across derivatives markets this week was the divergence between stabilising spot markets and still-cautious derivatives positioning. Following the liquidation event and volatility repricing seen earlier in June, BTC recovered from the low US$60,000 region and spent much of the week attempting to establish a more stable trading range, albeit with mixed results. Despite spot price action being slightly more constructive (in the majority), derivatives markets continue to reflect some caution.

Volatility markets remain the clearest expression of this dynamic. Front end BTC implied volatility has retraced from levels reached during the early-June selloff, although 1-week ATM volatility remains elevated relative to the low-30% regime that characterised May. Risk reversals also remain firmly put-skewed across front tenors, indicating that participants continue to pay a premium for downside protection despite the recovery in spot markets. The combination of lower volatility and persistent defensive skew suggests markets are becoming more comfortable with the immediate outlook, but remain unconvinced that downside risks have fully dissipated.

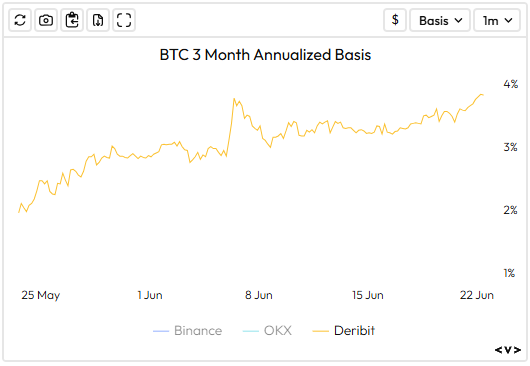

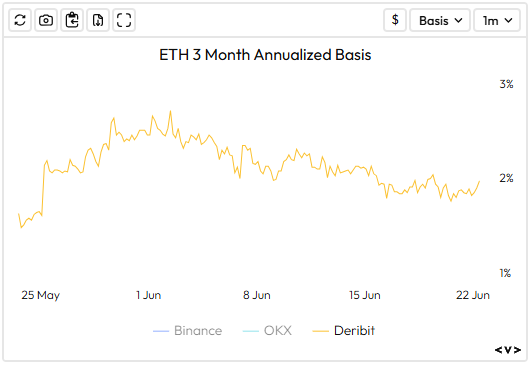

Carry markets continued to improve through the week. BTC 3-month annualised basis has recovered from approximately 2% a month ago to around 4%, representing the highest levels seen since the early-June liquidation event. In contrast, ETH basis remains comparatively flat, reinforcing the continued divergence between BTC and broader crypto risk. Perpetual funding rates remained modestly positive across major venues, although funding has generally lagged the recovery in basis, suggesting balance-sheet deployment is returning more quickly than directional speculative positioning. Open interest also remains below prior highs, indicating the improvement in carry markets is being driven by a gradual normalisation in risk appetite rather than aggressive leverage expansion.

The more interesting market structure theme remains the absence of marginal buyers. Spot ETF flows have softened materially through June, while Strategy’s pace of BTC accumulation has slowed relative to earlier phases of the cycle as funding costs across its capital structure have increased. Collectively, this suggests two of the market’s largest structural sources of demand are currently contributing less incremental liquidity than during prior rally phases.

From a technical perspective, BTC continues to build above the June washout lows, with support established in the low US$60,000 region and a more important resistance zone emerging around US$70,000–72,000. A sustained break above this range would likely require a reacceleration in spot demand, while a failure to hold current levels would risk reopening the broader correction.

Overall, derivatives markets continue to send mixed signals. Options markets remain defensively positioned, with elevated implied volatility and persistent downside skew, while carry markets have improved steadily as BTC basis recovers. The result is a market that is stabilising beneath the surface, although institutional participation remains concentrated in BTC and has yet to broaden across the wider digital asset complex.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

What to Watch

Monday cash open (today), the first equity reaction to the weekend deal collapse. Watch whether the deal premium that built into Thursday’s close gets repriced in a single session.

AU CPI + jobs — May monthly CPI indicator (Wed) and labour force report (Thu). Key into the next RBA call and the May-hike trajectory.

Lake Lucerne Summit, the Qatar-mediated talks that launched 21 June are the most important near-term catalyst. A breakthrough revives the de-escalation trade; a breakdown reopens the energy-shock and stagflation narrative.

May PCE (Friday 26 June), the Fed’s preferred inflation gauge and the next test of whether the oil reversal is feeding into cooler prints. A soft read gives Warsh room to walk back the hawkish September dot plot; a hot one cements higher-for-longer.

Q1 GDP and Micron / FedEx earnings, data picks up toward the end of the month, with Micron a key read on the AI memory-demand debate that triggered the early-June chip rout.

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.