9 Jun, 26

Weekly Crypto Market Wrap: 9 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

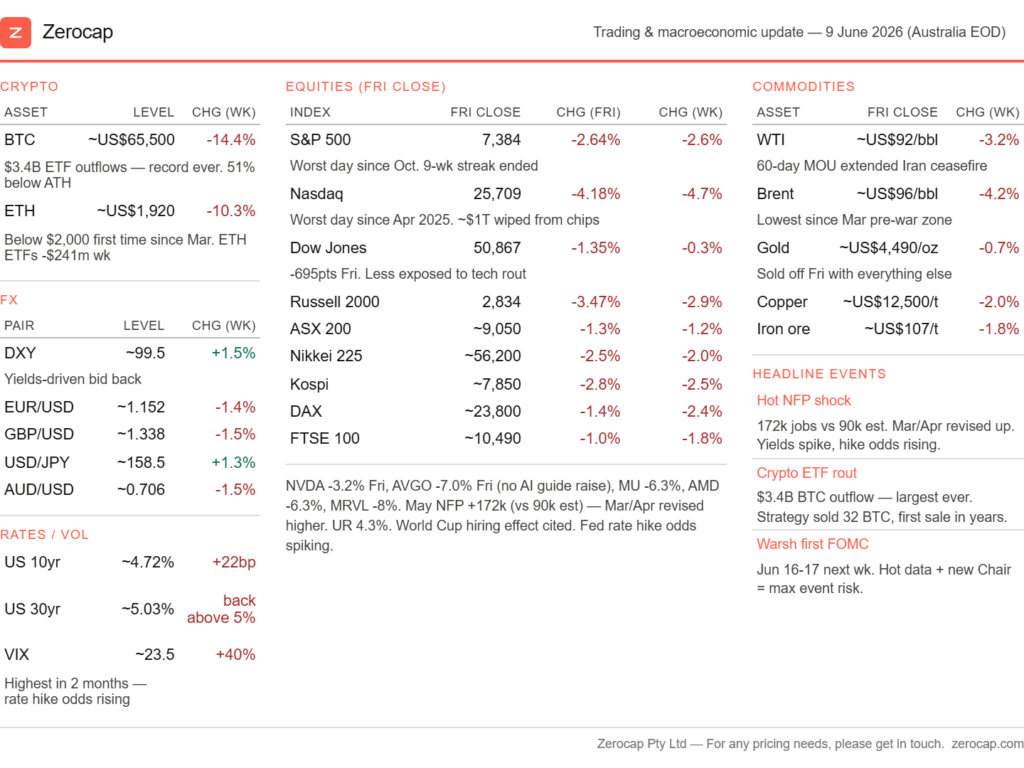

Week in Review

- U.S. spot BTC ETFs saw ~US$1.72B in outflows; ETH ETFs saw ~US$173M in outflows

- Tokenized equities reach US$5.5 billion market cap, fueled by SpaceX IPO access and exchange expansion

- ZEC rebounds 42% as ZODL founder details two-step emergency upgrade

- Michael Saylor’s Strategy buys another 1,550 bitcoin for US$101 million after small sale as total holdings rise to 845,256 BTC

- Hyperliquid hits record share of global perps market as HIP-3 tops US$62 billion monthly volume

Technicals & Macro

Markets

US equities sold off sharply on Friday following a stronger-than-expected labour market report that challenged expectations for policy easing. The S&P 500 fell 2.64%, its largest single-day decline since October, while the Nasdaq dropped 4.18%, its weakest session since the April 2025 tariff-driven sell-off. The Dow Jones Industrial Average lost 695 points (-1.35%), and the Russell 2000 underperformed, declining 3.47%. Semiconductor stocks bore the brunt of the move, with approximately US$1 trillion of market capitalisation erased across the sector.

The catalyst was a classic “good news is bad news” dynamic. May non-farm payrolls increased by 172,000 versus consensus expectations of approximately 90,000, while revisions to prior months were also revised higher. Unemployment remained steady at 4.3%, reinforcing the view that labour market conditions remain resilient despite softer consumer sentiment and ongoing geopolitical uncertainty. The stronger data prompted a significant repricing of interest rate expectations, with Treasury yields moving sharply higher as investors reassessed the likelihood of policy easing in the second half of the year.

The US 10-year Treasury yield rose toward 4.56%, while the 30-year yield moved back above 5%. Rate markets increasingly shifted toward a higher-for-longer outlook, with investors assigning a lower probability to near-term easing and reassessing the balance of risks around future policy decisions ahead of the June 16–17 FOMC meeting.

Risk sentiment weakened globally. South Korean equities came under significant pressure, with the KOSPI declining sharply amid heavy foreign selling concentrated in semiconductor names including Samsung Electronics and SK Hynix. The move reflected a combination of profit-taking, concerns around AI-related demand expectations, and broader sensitivity to rising global yields and tighter financial conditions.

Looking ahead, attention now turns to May CPI and the June FOMC meeting. Investors will be closely monitoring inflation data for evidence of whether higher energy prices and geopolitical developments are beginning to influence broader price pressures. With labour market conditions remaining resilient and rate markets increasingly cautious on the policy outlook, upcoming inflation data has the potential to play an outsized role in shaping expectations for the remainder of the year.

Fixed Income

Source: TradingView

US Treasury yields moved higher throughout the week, with the 10-year yield finishing near 4.56% after rising approximately 6bp following the stronger-than-expected non-farm payrolls report. The 2-year yield climbed to 4.17%, its highest level since early 2025, while the 30-year yield moved back above 5%. Longer-dated maturities continued to reflect investor concerns around inflation, fiscal dynamics, and term premium, with both the 20-year and 30-year trading above levels that had previously acted as resistance during the spring rally.

The move was driven primarily by stronger labour market data and a subsequent repricing of policy expectations. Markets increasingly interpreted the payrolls report as evidence that economic activity remains resilient, reducing the urgency for policy easing and reinforcing a higher-for-longer rates outlook. Energy markets and geopolitical developments also remained an important consideration for inflation expectations, contributing to ongoing uncertainty around the medium-term policy path.

The 2s10s curve steepened modestly during the week as front-end yields repriced higher while longer-dated yields continued to reflect inflation and term-premium concerns. Credit spreads widened marginally but remained orderly, suggesting broader financial conditions tightened without signs of material stress emerging across credit markets.

Attention now turns to the June 16–17 FOMC meeting, the first under Chair Kevin Warsh. Markets will focus closely on the updated Summary of Economic Projections, the dot plot, and any changes to forward guidance. With recent economic data challenging expectations for policy easing, the meeting is likely to play an important role in shaping rates and risk-asset positioning through the second half of the year.

Commodities

Oil prices moved lower during the week despite the broader risk-off backdrop. Brent crude declined to approximately US$96/bbl (-4.2% on the week), while WTI fell to around US$92/bbl (-3.2%). The move was largely driven by improving expectations around diplomatic progress between the US and Iran, with markets increasingly anticipating a reduction in regional supply disruptions and a gradual normalisation of energy flows. Brent has now retraced materially from the mid-May highs near US$113/bbl and is trading closer to levels seen prior to the escalation in tensions.

Gold was modestly lower on the week, finishing around US$4,490/oz (-0.7%), although it continued to outperform many other defensive assets. The metal remains caught between competing forces: lower oil prices and a softer inflation outlook on one side, and higher real yields on the other. Copper declined approximately 2% as growth concerns weighed on industrial metals, while iron ore softened modestly following weaker demand signals from China.

The decline in oil prices remains one of the more important macro developments for financial markets. If sustained, lower energy prices would ease pressure on inflation expectations, reduce upward pressure on long-end bond yields, and provide central banks with greater flexibility around future policy decisions. While energy alone is unlikely to determine the policy path, the recent reversal has removed a meaningful source of inflation risk that had emerged during May.

Cryptocurrency

BTC remains trapped in a narrow psychological corridor, with price action suggesting a market searching for conviction rather than exhibiting outright panic. BTC fell approximately 14% on the week, before stabilising above the US$60k level, while ETH declined around 10% and broke below US$2,000 for the first time since March. Despite continued weakness across global risk assets, BTC’s ability to hold above US$60k suggests selling pressure may be moderating, although support alone is not yet evidence of renewed demand.

The dominant structural theme remains ETF flows. US spot Bitcoin ETFs recorded another week of significant net outflows, extending a multi-week reversal that has materially reduced one of the market’s primary sources of marginal buying pressure. ETH ETF flows remained similarly weak. At the same time, uncertainty surrounding Strategy has become an additional sentiment consideration following its first Bitcoin sale in several years and increased investor focus on capital management, financing flexibility, and dividend sustainability. While the sale itself was immaterial in size, it challenged a narrative that many market participants had previously viewed as unconditional.

Options markets continue to reflect a defensive tone. Front-end implied volatility remains elevated relative to recent months, while risk reversals retain a put bias consistent with ongoing demand for downside protection. The message from volatility markets is not one of panic, but rather caution, with investors maintaining hedges ahead of key macro events including CPI and the upcoming FOMC meeting. Markets are also beginning to look ahead to the anticipated SpaceX IPO later this month, a potentially significant capital markets event that could influence broader risk allocation and liquidity conditions at the margin.

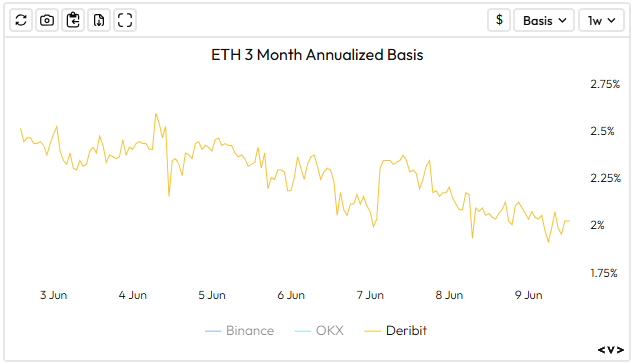

From a positioning perspective, the market appears substantially cleaner than it did earlier in the year. Open interest has retraced materially from peak levels, funding conditions have softened, and 3-month basis has compressed toward the lower end of its annual range. BTC support is concentrated in the US$60k region, with the next major technical level closer to US$55k. The resulting setup is increasingly two-sided: weaker macro data or a more accommodative policy outlook could support a sharp recovery given lighter positioning, while further deterioration in flows or renewed rates pressure would likely place support levels under renewed scrutiny.

The cleaner interpretation is not panic but consolidation. The market has largely completed its deleveraging phase and is now attempting to establish where long-term demand re-emerges. The next phase will likely be determined less by positioning and more by macro conditions, liquidity trends, and whether institutional flows begin to stabilise.

Emir Ibrahim, Analyst

Spot Desk

Risk sentiment shifted repeatedly throughout the week as markets navigated a combination of Middle East tensions, resilient US economic data, and continued weakness across digital assets. BTC fell below US$60k for the second time this year, closing the week down 14% and printing a new 2026 low of US$59,070, dragging the broader digital asset complex lower. US equities spent most of the week broadly unchanged at the index level, although sector performance remained highly dispersed. Early gains were driven by continued strength across AI-related technology names before a sharp sell-off into Friday as investors reassessed the implications of resilient labour market data for the path of monetary policy.

US economic data remained broadly constructive. JOLTS job openings exceeded expectations (7.6 million versus 6.8 million forecast), reinforcing the view that labour market conditions remain relatively tight despite signs of gradual moderation elsewhere. Rates markets experienced significant volatility as Treasury yields reacted primarily to developments in energy markets. Crude oil rallied approximately 9% to US$99.06/bbl early in the week following Iranian threats to disrupt key shipping routes and renewed regional tensions, raising inflation expectations and weighing on fixed income markets. Those moves partially reversed later in the week as signs of geopolitical de-escalation emerged, allowing Treasuries to recover and yields to retrace lower.

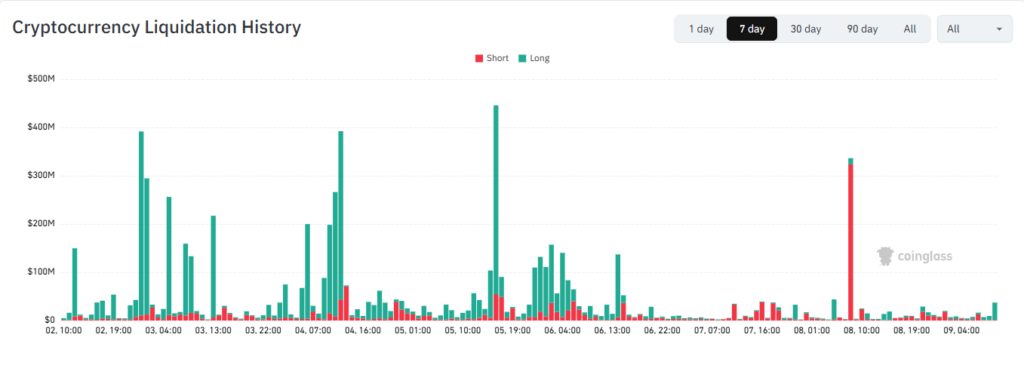

Digital asset markets remained under sustained pressure throughout the week. BTC (-14.0%) and ETH (-15.8%) both experienced persistent selling as ETF flows remained weak and broader risk appetite deteriorated. Spot Bitcoin ETFs extended their run of net outflows, while long liquidations accelerated downside momentum across derivatives markets. More than US$5.4bn of leveraged positions were liquidated during the week, with the largest liquidation events occurring on 4 and 5 June.

Source: https://www.coinglass.com/liquidations

Despite broad weakness across digital assets, HYPE continued to outperform, reaching fresh all-time highs as ongoing buyback activity and continued investor demand supported price action. Stablecoin pricing remained orderly throughout the week, although USDT spent much of the period trading at a modest discount to par around 0.9985 before recovering toward 0.9996 as BTC and ETH stabilised from recent lows. USDC also traded slightly below parity, reflecting continued demand for fiat liquidity amid the broader risk-off environment.

Against a challenging backdrop for digital assets, client activity was more constructive than broader market positioning implied. While BTC and ETH experienced significant declines, desk flow showed modest accumulation in BTC and strong buying interest in SOL. ETH flow remained slightly net offered, although sell-side participation was relatively limited given the magnitude of the move in spot markets. The dominant theme across client activity remained stablecoin off-ramping, with proceeds primarily converted into AUD, USD, and NZD.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins, and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Oliver Davis, OTC Trader

Derivatives Desk

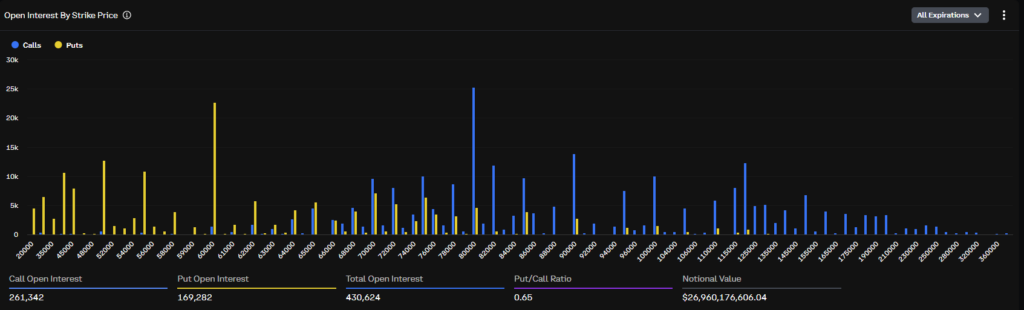

Structured products markets transitioned from consolidation toward risk repricing through the week ending 9 June, with options markets reacting in line with spot and leverage markets. While broader financial conditions were generally maintained, crypto underperformed broader risk assets as softer ETF participation and weaker liquidity conditions weighed on sentiment.

The most notable development was the sharp repricing across BTC volatility markets. Front-end implied volatility moved from the low-30% regime that characterised late May into the mid-to-high 40% area, with 1-week ATM volatility briefly approaching ~60% during periods of peak stress. This represents the largest shift in derivatives market structure over recent weeks and reflects a rapid reassessment of near-term uncertainty rather than a disorderly deleveraging event.

Options positioning also turned more defensive. Risk reversals shifted further toward puts through the week, with downside protection attracting a premium relative to upside exposure as participants rebuilt hedges following several weeks of volatility compression. Front-end skew remains notably more defensive than late May levels, suggesting markets continue to price downside tail risk despite relatively steady macro conditions.

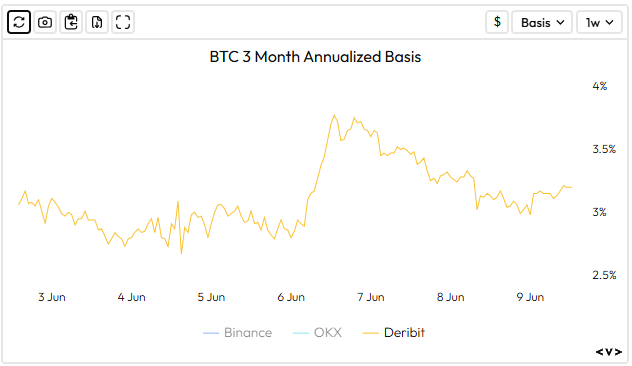

Carry markets were comparatively stable. BTC perpetual funding remained positive but contained across major venues, while 3-month annualised basis compressed in the outright selloff, back towards 3% —- reinforcing the view that leverage participation remains selective rather than aggressive. The absence of material carry expansion despite higher volatility suggests positioning still remains relatively clean.

Technically, BTC has transitioned back into a more fragile structure after failing to reclaim higher resistance zones. The market continues to trade around an important liquidity region, with support layered toward the mid-US$50,000 area and resistance now re-established around the low-US$70,000 region. A sustained reclaim of prior resistance levels would likely be required for volatility to compress meaningfully, while further weakness risks extending downside momentum into lower support bands.

The key derivatives takeaway is that markets are no longer pricing simple consolidation. Instead, options markets are pricing higher realised volatility and greater near-term uncertainty, while funding, basis and credit conditions continue to suggest this remains a repricing of risk rather than a broad deleveraging event.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

Source: Deribit.com

What to Watch

Wed: US CPI (MoM & YoY), US Core CPI (YoY), CN CPI (MoM & YoY)

Thu: ECB Interest Rate Decision, US PPI (MoM), US Initial Jobless Claims

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.