15 Jun, 26

Weekly Crypto Market Wrap: 15 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

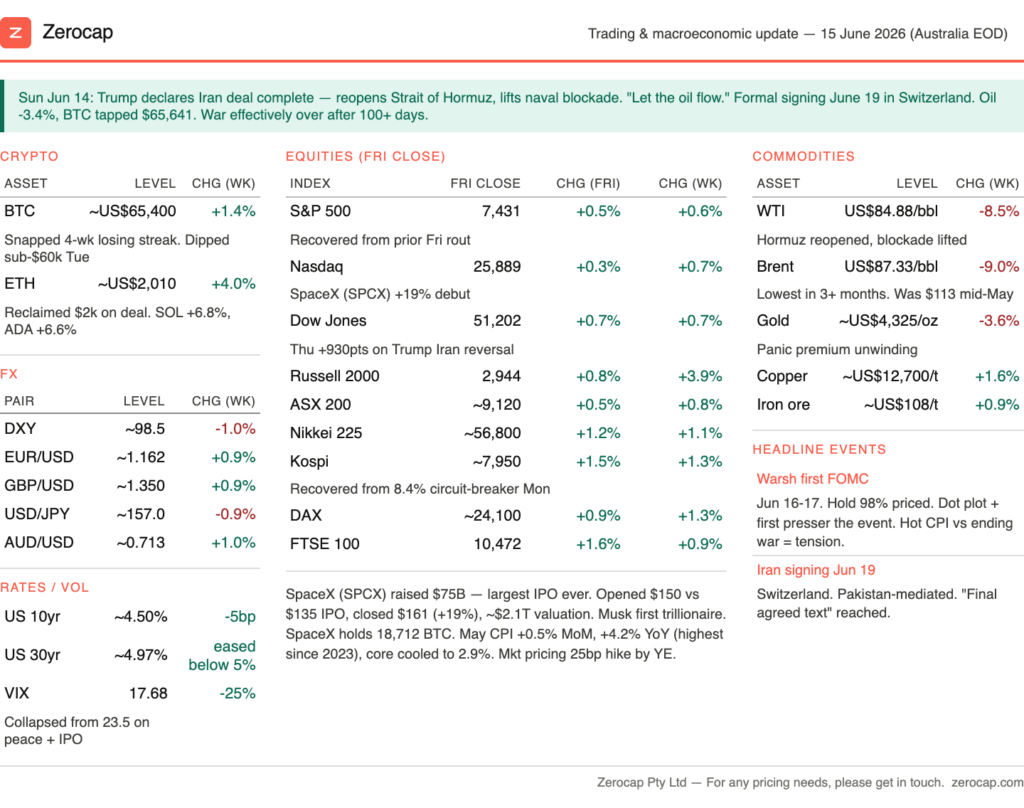

Week in Review

- U.S. spot BTC ETFs saw ~US$319M in net outflows; ETH ETFs recorded ~US$15M in outflows.

- Markets price zero probability of an RBA cut this week; Fed Chair Warsh heads inaugural FOMC meeting on Tuesday.

- BlackRock filed 8-A for iShares Bitcoin Premium Income ETF; yield-bearing BTC product expected to launch next week.

- Coinbase launched “Coinbase for Agents”; Mastercard unveiled “Agent Pay for Machines” supporting autonomous stablecoin transactions.

- Canton Network creator Digital Asset raised US$355M; Morpho raised US$175M to expand its open credit network.

Technicals & Macro

Markets

After more than 100 days of conflict that began with Operation Epic Fury on 28 February, President Trump declared the Iran agreement complete on Sunday (14 June), posting on Truth Social: “The Deal with the Islamic Republic of Iran is now complete… I hereby fully authorize the toll free opening of the Strait of Hormuz, and, simultaneously herewith, authorize the immediate removal of the United States Naval blockade. Ships of the World, start your engines. Let the oil flow!” A formal signing ceremony is scheduled for 19 June in Switzerland, with Pakistan reportedly mediating the final agreed text. The announcement capped a dramatic reversal in market sentiment that began earlier in the week. Following the prior Friday’s technology-led sell-off and Monday’s sharp decline in Asian equities, investor confidence improved materially as prospects for a negotiated resolution increased. Equities recovered strongly, oil prices moved lower, and the geopolitical risk premium that has influenced global markets since late February began to unwind.

The key complication remains inflation. May CPI, released on Wednesday, rose 0.5% MoM and 4.2% YoY, marking a third consecutive monthly acceleration and reflecting the lagged impact of higher energy prices earlier in the quarter. However, the core reading was more encouraging, rising 0.2% MoM and 2.9% YoY, suggesting underlying inflation pressures may be moderating despite elevated headline readings.

This creates a challenging backdrop for Chair Kevin Warsh’s first FOMC meeting on 16–17 June. Headline inflation continues to support a higher-for-longer policy stance, while softer core inflation and the recent collapse in oil prices strengthen the argument that the inflation impulse may prove temporary. Markets overwhelmingly expect no change in policy rates this week, leaving the updated dot plot, economic projections and Warsh’s inaugural press conference as the primary focus. Investors will be watching closely for any indication of how policymakers balance still-elevated headline inflation against improving inflation dynamics and a rapidly changing geopolitical backdrop.

Dollar

Source: TradingView

The US dollar softened over the week as geopolitical risk premium eased and safe-haven demand retraced. The .DXY fell to approximately 98.5 (-1.0% on the week). The market dynamic shifted noticeably: throughout the conflict, escalating tensions supported the USD through both safe-haven flows and higher energy prices; the prospect of de-escalation has begun to reverse both effects. EUR/USD firmed to approximately 1.162 (+0.9% on the week), GBP/USD rose to around 1.350 (+0.9%), and AUD/USD strengthened to roughly 0.713 (+1.0%), supported by improving risk sentiment and expectations that lower energy prices may reduce pressure on global growth.

USD/JPY eased to approximately 157.0 (-0.9% on the week), with the yen benefiting from lower oil prices and a moderation in the intervention concerns that had emerged as the pair approached 160. Looking ahead to this week’s FOMC meeting: A more dovish policy signal could place further pressure on the USD through narrowing rate differentials, while a hawkish interpretation of still-elevated headline inflation would likely support a reversal of recent weakness. The formal Iran signing on 19 June also remains an important event risk, particularly if it reinforces expectations of a durable reduction in geopolitical tensions.

Fixed Income

Treasury yields eased modestly during the week as the sharp decline in oil prices improved the inflation outlook despite the stronger headline CPI print. The 10-year Treasury yield settled around 4.50% (-5bp on the week), retracing from the prior week’s post-NFP high near 4.55%, while the 30-year yield moved back below 5% to approximately 4.97%.

Rates markets remain caught between competing narratives. Headline inflation of 4.2% (YoY) and resilient labour market data support a higher-for-longer policy stance, while the sharp fall in oil prices – with Brent declining from approximately US$113/bbl to US$87/bbl over the past month – and softer core inflation readings suggest the inflation impulse from the energy shock may be beginning to reverse. Markets continue to assign a meaningful probability to further tightening by year-end, although that outlook could shift if lower energy prices translate into softer headline inflation over coming months.

Attention now turns to Chair Kevin Warsh’s first FOMC meeting on 16–17 June. The updated Summary of Economic Projections and dot plot will provide the clearest indication yet of how the committee under new leadership is balancing elevated headline inflation against improving core inflation dynamics and easing geopolitical risks. The 2s10s curve remained modestly positive during the week, while credit spreads retraced some of the prior week’s widening as risk sentiment improved.

Cryptocurrency

Bitcoin snapped a difficult four-week losing streak, closing the week approximately 1.4% higher near US$65,400 after recovering from an intraday low around US$60,755 earlier in the period. Price action remained heavily influenced by macro developments throughout the week. The May CPI release failed to provide a decisive catalyst, with the combination of elevated headline inflation and softer core inflation leaving BTC largely range-bound around US$61,000. Sentiment improved materially later in the week as geopolitical tensions eased, helping BTC rally alongside broader risk assets and finish the week back above US$65,000. The episode reinforced BTC’s tendency to trade as a high-beta risk asset during periods of macro uncertainty, with de-escalation supporting risk appetite across both traditional and digital asset markets.

The dominant structural theme remained ETF flows. US spot Bitcoin ETFs recorded another week of significant net outflows, extending the longest redemption streak since launch and continuing to remove an important source of marginal demand. While geopolitical uncertainty and shifting interest rate expectations likely contributed to the softer flow backdrop, attention now turns to whether improving macro conditions and greater policy clarity can stabilise institutional participation. The broader digital asset market responded positively to the improvement in sentiment, with ETH reclaiming the US$2,000 level and several major altcoins outperforming BTC into the weekend.

The anticipated SpaceX IPO also attracted market attention following disclosure of the company’s 18,712 BTC holding, estimated at approximately US$1.6bn. The announcement further highlighted the growing intersection between large-scale corporate balance sheets and digital assets. Separately, Strategy remains an important sentiment consideration, with investors continuing to monitor capital management decisions and the implications for its Bitcoin treasury strategy. Heading into the FOMC meeting, positioning appears materially cleaner than earlier in the quarter. Funding rates remain subdued, open interest has retraced significantly from recent highs, and basis remains compressed relative to historical averages. Sentiment indicators continue to reflect elevated caution despite the recovery in price, leaving the market highly sensitive to policy outcomes. BTC support remains concentrated around the US$60,000–63,000 region, with resistance emerging toward US$68,000. The combination of lighter positioning, improved geopolitical conditions and a pivotal Fed meeting creates a genuinely two-sided setup, with policy communication likely to determine whether the recent recovery develops into a broader relief rally or remains a temporary rebound within a wider consolidation range.

Emir Ibrahim, Analyst

Spot Desk

Digital assets traded with relative stability for much of the week, with volatility remaining muted despite a more headline-sensitive backdrop across US equities, rates and FX. Bitcoin (BTC) and Ethereum (ETH) were range-bound for most of the period – indicative of a market that had largely absorbed the recent deleveraging impulse – before improving weekend risk sentiment following geopolitical de-escalation drove a constructive break above the ranges that had anchored intra-week price action.

Desk activity was broadly aligned with a well-contained, though still defensive, market structure. BTC and ETH both recorded modest net selling skews, consistent with ongoing ETF outflows and a generally cautious institutional backdrop, while Solana (SOL) remained the more constructive expression of risk appetite and retained a net buying bias.

Institutional activity remained mixed throughout the week, as record ETF outflows across both BTC and ETH contrasted with continued strategic accumulation and infrastructure-led capital formation. Bitmine added to its ETH holdings, further extending its position as the largest corporate ETH treasury holder, while Morpho raised US$175 million to expand its open credit network. Despite ETF-related headwinds for major digital assets, strategic capital continues to be deployed into the infrastructure layer.

Altcoin preference was primarily led by AI-adjacent and usage-driven narratives. Anthropic’s model access restrictions following a US government export-control directive drove renewed interest in decentralised AI infrastructure, supporting strong performance in Bittensor (TAO) and Venice (VVV) through the weekend session. Collector Crypt ($CARDS) also extended its run as daily spot volumes on the Solana-based graded trading card platform continued to trend toward new all-time highs. The common thread remains a preference for revenue-generating, usage-driven and product-market-fit narratives rather than broad speculative beta. PAXG interest remained limited, consistent with softer demand for gold-linked exposures as inflation and debasement concerns moderated.

In FX, AUD/USD traded a two-sided week, initially softening to nine-week lows near 0.6979 – on weaker metals and softer risk sentiment – before recovering strongly into Friday’s New York close. Momentum carried into Monday’s Asia session, with the pair trading as high as 0.7088 following reports of a US-Iran interim peace agreement that could reopen the Strait of Hormuz and improve broader risk sentiment. Lower US Treasury yields also marginally reduced USD yield support during the period.

US CPI rose at its fastest annual pace in three years, although the result was broadly in line with expectations. Domestically, markets continue to price little probability of a near-term RBA rate cut, while Fed Chair Warsh’s inaugural FOMC meeting remains the next major event risk for global markets.

Stablecoins remained the dominant feature of desk activity, with significant off-ramping across both USDT and USDC into USD. AUDD and AUDM continued to attract strong on-ramping demand, with client engagement around alternative local rails for AUD-denominated settlement and treasury management remaining elevated. Elsewhere, desk AUD flows carried a significant net buying skew, EUR remained offered, and NZD demand was firm.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Ben Mensah, OTC Trader

Derivatives Desk

Derivatives markets stabilised through the week as the sharp volatility repricing observed in early June began to moderate. While implied volatility remains above the exceptionally compressed levels seen throughout May, options markets became increasingly orderly as spot prices consolidated and broader risk sentiment improved.

Front-end BTC implied volatility softened during the week, with 1-week ATM volatility retracing into the high-30% region. The combination of a largely in-line US inflation print and the subsequent de-escalation in Middle East tensions removed two of the largest near-term event risks facing markets, allowing short-dated volatility premium to normalise. As a result, the term structure steepened modestly as front-end implied volatility compressed more rapidly than longer-dated tenors. Risk reversals remained put-skewed across front maturities, although downside demand moderated materially from the levels reached during the recent sell-off. Collectively, options markets continue to price uncertainty, but no longer imply an immediate extension of downside volatility.

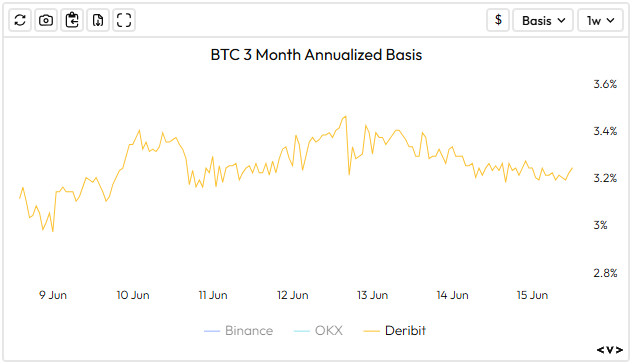

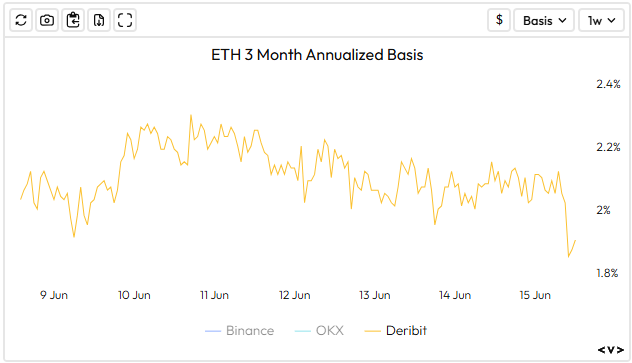

Carry markets improved modestly. Perpetual funding remains uneven but has generally returned to positive territory across major venues. Cash-and-carry returns remain subdued, with BTC 3-month annualised basis trading around 3% and ETH basis closer to 2%, highlighting the absence of aggressive leverage despite the recovery in spot prices. The combination of relatively elevated implied volatility and compressed basis remains notable, with options markets offering significantly more premium than futures carry markets.

Technically, BTC continues to consolidate above the US$60,000 support region, while resistance remains concentrated around US$75,000. The market’s ability to hold above recent lows despite elevated volatility and defensive positioning is constructive from a market structure perspective.

Overall, derivatives markets have transitioned from repricing toward stabilisation. The inflation data and subsequent Iran peace agreement have reduced near-term macro uncertainty and contributed to a meaningful compression in front-end volatility, while funding, basis and broader positioning indicators continue to suggest a market that has largely completed its recent deleveraging phase. Volatility remains above May lows and skew remains modestly defensive, but derivatives markets are increasingly reflecting consolidation rather than stress.

WHOLESALE INVESTORS ONLY

Source: Velo.xyz

What to Watch

Tue: RBA Interest Rate Decision, BoJ Interest Rate Decision

Wed: GB Inflation Rate YoY, Fed Interest Rate Decision, Fed Press Conference

Thu: BoE Interest Rate Decision

Fri: JP Inflation Rate YoY

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.