13 Jul, 26

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- U.S. spot Bitcoin ETFs saw US$197.4M in inflows, snapping an eight-week outflow streak; Ethereum ETFs added US$84.3M.

- Circle secures final OCC approval to establish First National Digital Currency Bank, a national trust bank for digital asset custody.

- Polymarket files application to offer regulated margin trading in the U.S., following Kalshi’s approval earlier this year.

- Robinhood Chain gained rapid traction as memecoin activity drives daily DEX volumes above Ethereum and Base.

Technicals & Macro

Markets

The fragile post-war calm broke this week, and markets mostly looked through it. With formal US-Iran talks paused for the weeklong funeral observances for Ayatollah Khamenei, Iran fired on non-military commercial vessels in the Strait of Hormuz, and the US responded with airstrikes on Iranian targets. Shipping through the Strait slowed considerably late in the week, oil spiked midweek, and the 10-year yield climbed to 4.57 percent on Wednesday as jumping crude prices reignited inflation fears. Yet by Friday the tone had turned again, with rumours of renewed US-Iran contact dragging the dollar lower and oil halting its rebound.

The market read that the ceasefire is tenuous but a return to full-scale war remains unlikely, and equities backed that judgement: the S&P 500 closed at 7,575, up around 1.2 percent for a fourth consecutive winning week. The tension for the Fed is direct. The soft June payrolls report had knocked September hike odds down to roughly 50 percent, but the midweek oil spike pushed them straight back up, with futures now pricing about a 61 percent chance of a September hike. Bank of America added that front-end real yields are likely to stay elevated even as oil retreats.

This week’s US CPI print, the first to fully capture the oil round trip from war premium to pre-war levels and partway back, is the pivotal input into the 28 and 29 July FOMC, and Q2 bank earnings kick off Tuesday with JPMorgan and four other Wall Street majors reporting.

Stock Markets

Source: TradingView

The S&P 500 rose 0.42 percent Friday to close at 7,575.39, up more than 1 percent on the week, while the Nasdaq added 0.29 percent to 26,281.61 and also gained over 1 percent for the week. The Dow rose 149.60 points Friday to 52,637.01 but fell 0.5 percent on the week, and the Russell 2000 slipped 0.49 percent Friday to 2,977.81, though small caps remain the year’s leaders at plus 20 percent versus 10.7 percent for the S&P. The week’s defining single-stock story was Meta, which surged roughly 15 percent for its best week since early 2024, capped by a 6 percent Friday jump after Bank of America maintained its buy rating and a SemiAnalysis report highlighted improving AI compute economics. Nvidia rose about 4 percent Friday.

The other headline was Friday’s US debut of SK Hynix, whose ADRs priced at 149 dollars, opened at 170 and closed up roughly 13 percent after raising 26.5 billion dollars, the largest-ever US listing by a foreign company, a striking signal of appetite for AI memory exposure given Micron is already up more than 200 percent this year.

SpaceX was fast-tracked into the Nasdaq-100, though space names broadly stayed under pressure. Delta kicked off earnings season, and the KBW bank index enters Tuesday’s reports having outpaced the broader market since March. In Asia, the Kospi added 2.5 percent Friday into the Hynix debut and the Nikkei rose 1.2 percent, while mainland China lagged with the CSI 300 down nearly 2 percent Friday.

Fixed Income

The bond market spent the week trading the Hormuz headlines. The 10-year finished Friday at 4.56 percent, up roughly 10 basis points on the week, after touching 4.57 percent on Wednesday when the oil spike revived inflation fears, and the 30-year traded back above the 5 percent line on Tuesday. The 2-year closed at 4.21 percent, at or near its 2026 highs, reflecting an aggressive front-end repricing: September hike odds rose from roughly 50 percent after the soft jobs report to about 61 percent by Friday. The structure of the curve tells the story cleanly. The front end is pricing a Fed that may need to tighten into an energy-driven inflation impulse, while the long end remains below its 2026 highs, signalling that the market does not yet believe higher rates will be a durable regime.

Yields held steady on Friday as bond markets caught their breath, and the June FOMC minutes released during the week reinforced the committee’s hawkish tilt following the removal of the easing bias. The next test is the CPI print, where the base case is a cooler headline given oil averaged well below war-period levels for much of the survey window, followed by the FOMC at month-end. A soft CPI likely unwinds a chunk of the 61 percent September pricing; a hot one cements it.

Energy

Oil rebounded on the re-escalation before stalling. WTI settled Friday at 71.41 dollars, up roughly 4 percent on the week but down 0.93 percent on the day as the rebound halted, with Brent around 75 dollars.

The moves reflect a market caught between two realities: physical supply has largely normalised, with Saudi exports restored to roughly 90 percent of pre-war levels, yet the attacks on shipping and the US airstrikes reintroduced a genuine risk premium, and Strait traffic slowed materially late in the week.

The forward question is whether the post-funeral resumption of Doha talks can stabilize the corridor, and tanker traffic data remains the cleanest signal, cutting through the political rhetoric in both directions.

Dollar

The dollar round-tripped with the geopolitics. The DXY caught a safe-haven and rate-repricing bid midweek as the airstrikes hit and September hike odds rebuilt, then faded Friday on the talks rumours to finish around 100.7, roughly flat on the week.

Cryptocurrency

Crypto passed a genuine stress test this week. When the US airstrikes hit on Wednesday, BTC dipped around 2.4 percent to roughly 62,150 dollars, but the 62,000 dollar shelf that traders have defended since last month’s lows held firmly, and by Friday BTC was grinding back through 64,400, retesting the resistance it failed at earlier in the week. It trades near 63,900 dollars today, up around 1.6 percent on the week. The relative performance point is worth making to clients: one widely-circulated Friday headline framed it as Bitcoin holding firm while gold slid into a geopolitical shock, a small but notable inversion of the usual safe-haven hierarchy, and further evidence that the de-leveraged holder base is absorbing bad news that would have produced cascading liquidations in March. ETH sits near 1,805 dollars, with XRP around 1.09 and SOL near 77 after a midweek washout.

The flow story finally turned. US spot Bitcoin ETFs snapped a 10-day losing streak on Wednesday with 197.4 million dollars of net inflows, the largest single-day haul in two months, coming off the worst month on record for the products in June. One strong day does not make a trend, but combined with the whale accumulation of recent weeks it suggests the marginal seller is exhausted and institutional demand is re-engaging at these levels. The CLARITY Act is the catalyst the market is leaning toward, with the crypto regulatory agenda slated for floor action this month after the 4 July signing target slipped, and positioning is already visible: Tom Lee’s Bitmine added another 74 million dollars of ETH during the week, continuing its march toward a stated goal of owning 5 percent of supply, explicitly framed as a CLARITY bet.

But the biggest structural shift was in stablecoins. Open USD launched with backing from a 140-strong consortium including Visa, Mastercard, Stripe and Coinbase, offering free mint and redemption with reserve income shared across partners. The model directly attacks the economics that have underpinned the incumbents: Circle shares fell 15 to 17 percent on the news, because the reserve float, the most profitable part of the stablecoin business, is now openly contested by a network with distribution that dwarfs any single issuer. For a desk that watches stablecoin rails as core settlement infrastructure, this is the most important competitive development in the space in some time, and the read-through to fee compression across the entire stablecoin complex is the theme to track into the second half.

The cautionary tale sits in the equity market, where the crypto IPO class of 2025 and 2026 continues to bleed: Gemini is down 89 percent from its September 2025 debut, BitGo 77 percent and Bullish roughly 71 percent from their opens, and the listing pipeline is effectively frozen until public-market sentiment repairs. Polymarket filed to bring margin trading to US customers, following Kalshi’s March authorisation, another step in the mainstreaming of prediction markets.

Technically, the picture is still constructive. BTC has now put in a higher low through a live geopolitical shock, the 62,000 dollar shelf is well defined, and a clean break of 64,400 opens the path toward the 15 June peak of 67,250 dollars, which is the level that would confirm the recovery structure. Below, 62,000 and then the 60,000 round number remain the lines that matter.

The desk is watching three things in order: whether this week’s CPI relieves or reinforces the September hike pricing that has been the primary macro weight on the asset class, whether ETF inflows string together consecutive positive sessions for the first time since May, and the Hormuz tape, where crypto has now demonstrated twice that it wears weekend geopolitical risk before equities can react.

Emir Ibrahim, Analyst

Spot Desk

Volatility compressed across digital assets throughout the week, as the BTC Volatility Index (DVOL) softened to 30-day lows near 35 while the complex traded largely in line with muted cross-asset volatility in broader risk markets. Majors spent the week trading within their previously well-defined ranges, with Bitcoin (BTC) and Ethereum (ETH) absorbing the week’s geopolitical shock without meaningful dislocation – consistent with an already deleveraged holder base wearing negative news without the heightened headline sensitivity of the year’s earlier market regimes.

Desk activity retained a defensive tilt for the week. BTC and ETH both recorded notable net selling skews, while Solana (SOL) was net bought in a countertrend skew as it works back into favour as a risk expression among crypto-native mindshare, supported by a pickup in on-chain activity and social metrics over recent weeks. PAXG demand remained softer than earlier in the year, with appetite for macro hedging within digital infrastructure still subdued amid the live geopolitical backdrop. Breadth across the longer tail was similarly limited in keeping with the defensive tone, with a net buying skew in XRP the primary additional activity of note.

In FX, AUD/USD firmed moderately, opening at 0.6940 and closing at 0.6952, before softening at Asia’s weekly open to trade near 0.6927 on the weekend re-escalation. The structural yield-differential story has taken a back seat, with geopolitical re-escalation and its second-order effects on safe-haven flows and AUD’s cyclical correlation to risk now the dominant driver. Domestically, the market implied probability of an RBA cash rate increase to 4.60% at the next board meeting held stable near 16%, reinforcing the local rates story’s diminished role as a directional input. Tuesday’s US core CPI and Wednesday’s PPI headline the macro calendar, though with with Hormuz traffic sharply disrupted and the status of the Strait contested amid exchanged US-Iran strikes, the risk reaction into tonight’s US cash open is the live risk into the week.

Elsewhere, stablecoins again dominated desk volumes, with both USDT and USDC significantly net sold as clients off-ramped into fiat. AUDD and AUDM continued to attract on-ramping interest at increasing size, with AUD-denominated fiat alternatives embedding further into settlement and treasury workflows across the space. Desk AUD flows were skewed toward off-ramping despite the firmer pair – a divergence between flow demand and spot direction indicative of robust underlying demand for AUD liquidity. In other FX activity, NZD was primarily bought while EUR was offered.

The OTC desk continues to provide tailored cryptocurrency liquidity solutions and competitive pricing across major digital assets, stablecoins, selected altcoins and key fiat currency pairs. With T+0 settlement capability, the desk continues to facilitate efficient execution and settlement across client flows.

Ben Mensah, OTC Trader

Derivatives Desk

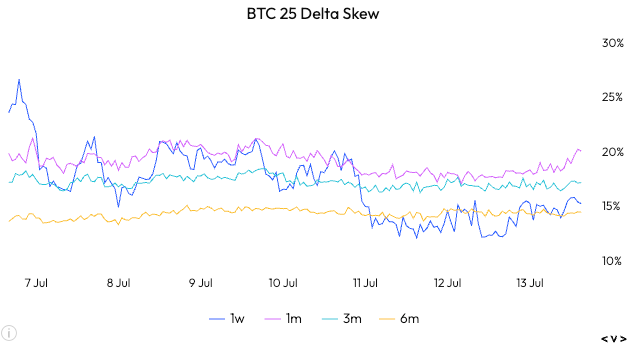

Bitcoin’s move back above $64k late last week, alongside ETH outperforming around $1,790, has eased bearish pressure, albeit within the range – but options markets are not yet behaving like traders are blindly chasing upside. Defensive positioning has eased, but not disappeared, with BTC and ETH puts still trading at a premium to calls.

In a clean bull market, skew normally flips quickly as traders rush for upside convexity. This time however the market is more balanced: spot has recovered, ETF flows have stabilised but remain choppy, and options traders are still paying for downside insurance. US spot BTC ETFs saw $264.2m of inflows on 6 July and $11.1m on 7 July, before flipping back to $186.1m of outflows on 9 July. This indicates a shift in sentiment, but not an almighty 180 just yet.WHOLESALE INVESTORS ONLY

Source: Velo.xyz

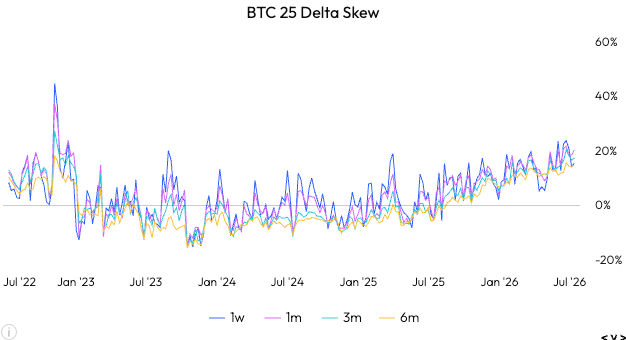

Important to zoom out on the weekly shift in skews – there is a sustaining trend shifting to downside protection over the past year.

As with markets, these tend to be cyclical. The house view is that easing macro uncertainty and reduced US-Iran escalation risk should see skew normalise from put-rich levels, with upside demand rebuilding if spot can break higher.

The macro overlay is keeping front-end volatility supported, rather than lifting the whole surface. One-week BTC ATM IV has rebounded into the 14 July CPI release, while longer-dated tenors remain comparatively stable. The read-through is that traders are paying for near-term event protection, but not yet repricing a broader volatility regime shift.

That makes sense given the June FOMC backdrop. The Fed’s June statement still described inflation as elevated, and the minutes showed policy-rate expectations had moved higher over the intermeeting period. With June CPI due on 14 July, the market has a clear front-end catalyst to hedge around. This is not a market to be short gamma indiscriminately. However, it is not a bad market to monetise upside levels that clients are genuinely happy to sell. We are seeing a number of clients trading the weekly and monthly rolls, shorting BTC and ETH calls at levels they are comfortable selling.

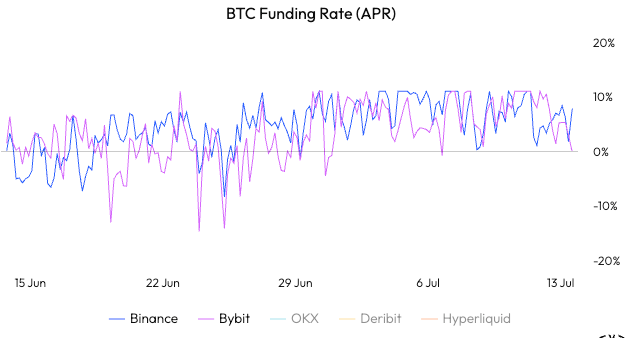

Perp funding is constructive, but not excessive. That is the right kind of backdrop for structured yield – enough demand for upside exposure to generate premium, but not the late-cycle froth that usually makes short-volatility trades dangerous.

BTC perp funding has shifted from two-way and uncertain to positive, indicating longs are once again willing to pay for leverage. Notably, against this backdrop Open Interest is steady. These are healthy markets, but not to be taken lightly against the geopolitical backdrop – USA vs Iran is still a powderkeg.

In short, futures and options are showing improving sentiment, while ETF flows and macro event risk argue against leaning too aggressively into outright directional leverage. The house take is that BTC remains range-bound through the next month of macro and geopolitical catalysts, with scope to re-accelerate if CPI cooperates and the US-Iran risk premium fades.

Jon de Wet

CIO

What to Watch

Tue: US Inflation Rate YoY

Wed: US PPI YoY, CN GDP Growth Rate YoY, BoC Interest Rate Decision

Thu: Fed Chair Warsh Testimony

Friday: US Building Permits

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 22 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.