26 May, 25

Weekly Crypto Market Wrap: 26th May 2025

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- U.S. Senate advances and passes stablecoin legislation with bipartisan support, including the GENIUS Act.

- JPMorgan plans to allow clients to buy Bitcoin without custody, with Jamie Dimon confirming the move amid a $4 trillion client base.

- Ethereum’s Vitalik Buterin proposes scaling solutions including EIP-4444, partially stateless nodes, and easier, cheaper node operation.

- Solana’s ‘Alpenglow’ upgrade aims to boost network speed 100 times, with former Ethereum champion Max Resnick planning to transform Solana.

- Hong Kong passes stablecoin legislation, establishing a licensing regime for fiat-backed stablecoins, intensifying global regulatory competition.Kraken expands crypto trading with 24/7 tokenized trading of major stocks and efforts to bridge traditional finance and crypto markets.

Technicals & Macro

BTCUSD

Key levels

74,000 / 100,000 / ~110,000 / 120,000 (ATH)

The surge

Every time I write about a Bitcoin surge, I think about that horror movie “The Purge”. It’s a story about all crimes being legal for 24 hrs once per year, where chaos ensues. Reflecting on Bitcoin’s journey to becoming the world’s 5th largest asset globally, I can’t help but think about the people that took the early risks – when BTC was considered an anarchist asset, where no “Purge” or sandbox was there to shield from the eyes of the law. It was a real battle, and still is in some ways, against traditional monetary systems and regulators struggling to grapple with the concept of borderless and bankless transfers of money. Yet here we sit at all-time highs again – but this time the world is watching, and notably, the big end of town is taking real notice. Even Dimon from JPM is opening its doors.

This week brought new all-time highs of 112,000 this week, against more geopolitical and macro uncertainty. Trump is out of the gate on Europe now – with negotiations “going nowhere”, suggesting he slap a 50% duty on all European goods entering the U.S. starting June 1. Markets started to feel the heat again, but with less force than the last verbal spray from the President, and were quickly bid up. What was really fascinating was how quickly BTC caught a bid, further showing evidence of macro hedge behaviour, not just trading as a risk asset. Combine this with soaring 30-year bond yields above 5%, signalling risk premium pricing, and you have the perfect environment for bearer assets to catch a bid.

Gold trading efficiently

The OG bearer asset. Gold is still trading technically so well. Keep a close eye on 30Y bond yields, if they continue to move higher, gold is likely to follow.

BTCUSD back to 2018

Zooming back to 2018 on the ‘decentralised bearer asset’ provides more perspective on the journey. We’ve come a long way since we’ve been writing this weekly report. I still remember when BTC broke the 10K mark – the champagne (actually cheap prosecco) was flying. As the asset has further matured, it’s become apparent that the paradigm is truly different this time. We are seeing debasing of fiat currency to the point that scarcity is now the new valuation metric, less adoption curve and volumes as we have seen in earlier days.

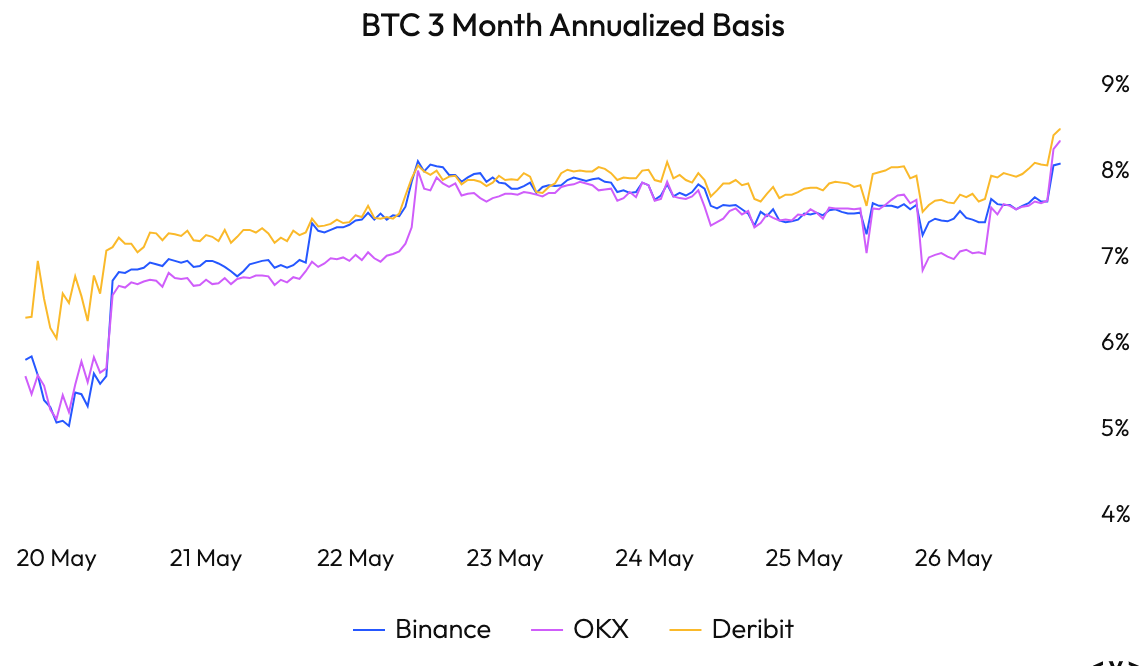

Basis expansion, slowly slowly

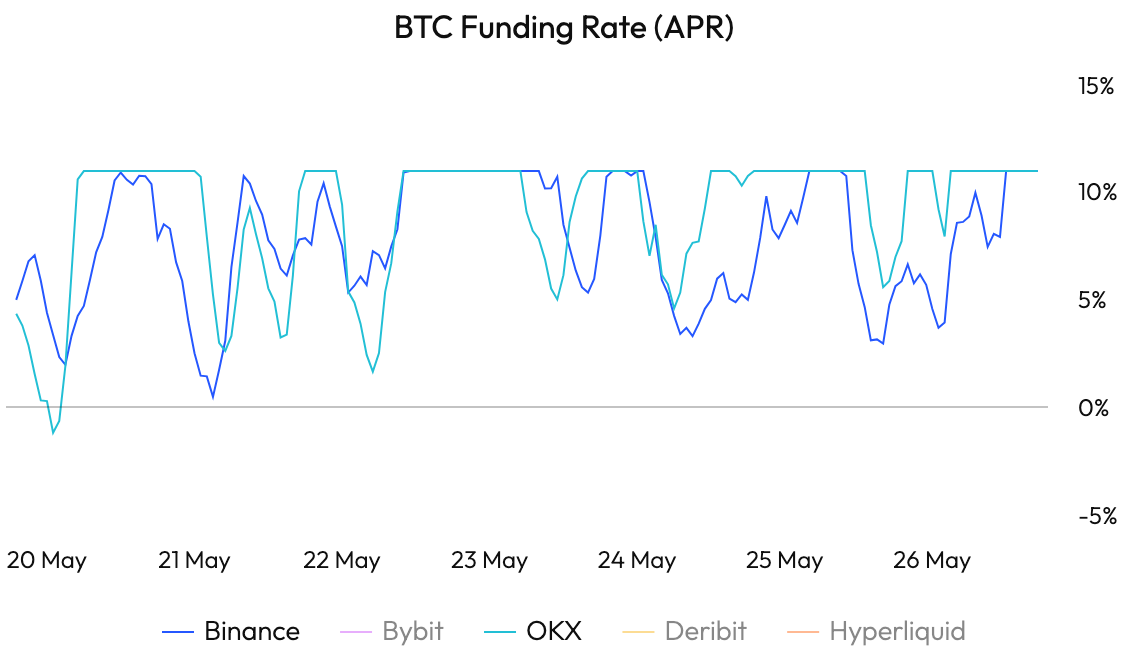

Futures 3M basis expanding, but still at historically low levels. Perpetual funding rates still capped – suggesting that leverage is contained. This is still a market that has not seen excess and mania enter just yet.. we could have a long way to go if leveraged buyers come in on a break of highs.

NASDAQ/BTCUSD

Compression, compression. Bitcoin is still taking centre stage on the equities / BTC ratio.

DXY heading lower

Last week I didn’t wanna be long, and I didn’t wanna be short.. erring on the short side now. We’ve broken the multi year range, and the market is selling uncertainty here. The challenge with a short USD view though is that long-term bond yields are pumping, the Fed is cautious, and there is elasticity in the US presidency. Who knows what comes next.

ETHUSD

ETHBTC

The Decun holding some buoyancy. BTC still has the momentum right now – another reminder to be careful betting against it.

Stay safe out there.

Jon de Wet, CIO

Spot Desk

It was quite the week on the desk, marked by a mix of key economic developments and exciting moves across the crypto markets.

The Reserve Bank of Australia (RBA) delivered a widely expected 25bps rate cut at its May meeting, lowering the cash rate to 3.85% from 4.1%.

The rate cut initially weighed on the Australian dollar, causing AUD/USD to dip in the hours following the announcement as markets digested the RBA’s more cautious stance. However, the currency quickly regained ground, lifted by broader USD weakness and improved risk sentiment. By the end of the week, AUD/USD had recovered strongly, and as of Monday, it had broken above $0.65 – marking a six-month high.

Client sentiment around AUD remained relatively subdued, and we continued to observe greater on-ramping than off-ramping in the USDT/AUD pair.

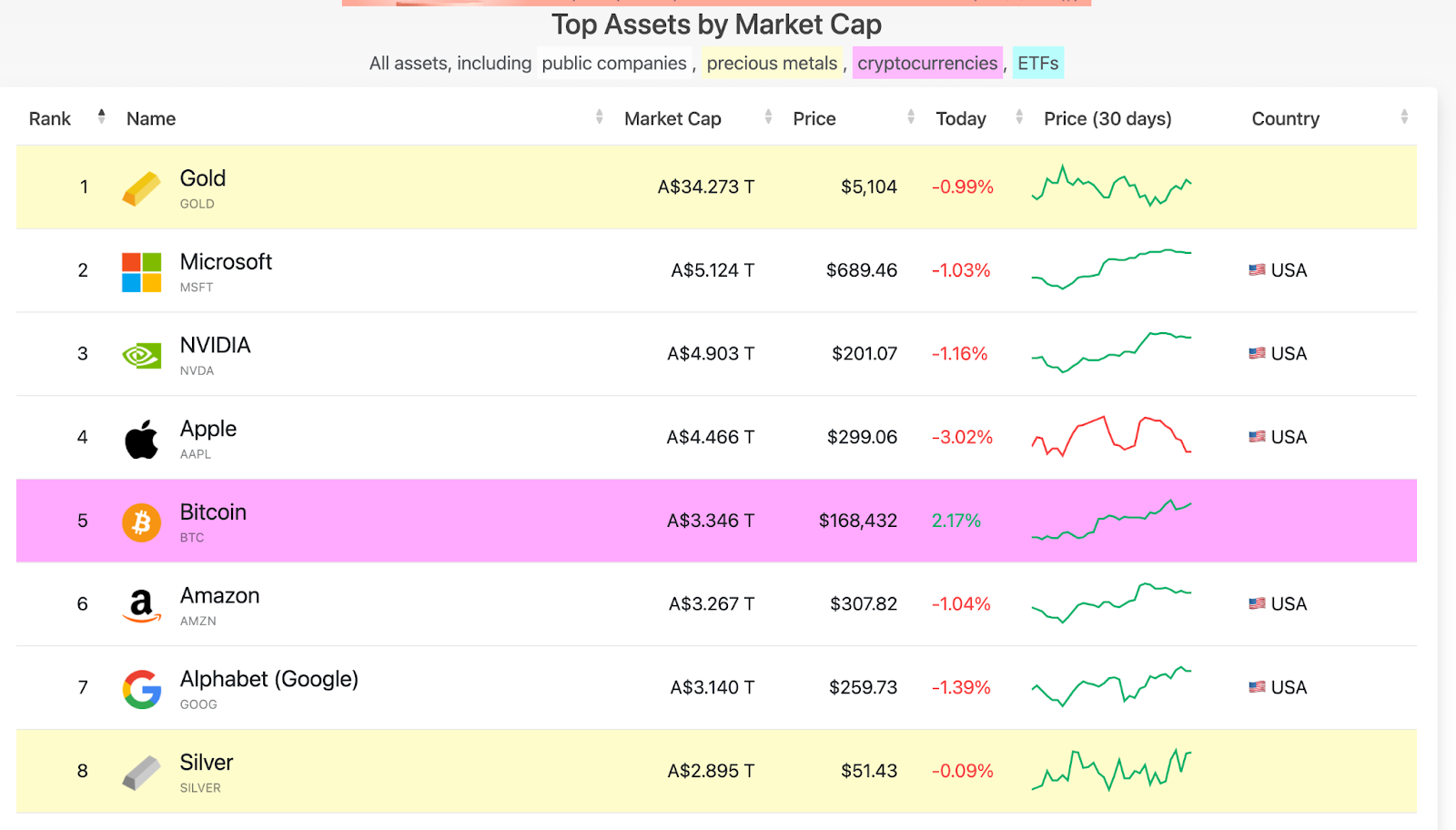

USDT/USD flows remained heavily skewed toward off-ramping, extending the trend in demand we observed the week prior. This is expected to slow on Monday due to the U.S. banking holiday, though we anticipate demand will resume over the rest of the week.On the spot desk, all eyes were on Bitcoin as it surged to a fresh all-time high of $111,970, cementing its place among the world’s top five most valuable assets by market cap, now exceeding $2.1 trillion. The rally revived interest across the market, with altcoin activity picking up notably. Clients were buyers of BTC, ETH, SOL, SUI, and HYPE, with buying flows outweighing selling across most pairs. The uptick in altcoin demand suggests a growing appetite for diversification beyond Bitcoin, especially as momentum returns to the broader market.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions, offering competitive pricing across major coins, altcoins, and memecoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Reshad Nahimzada, Trading Analyst

Derivatives Desk

WHOLESALE INVESTORS ONLY*

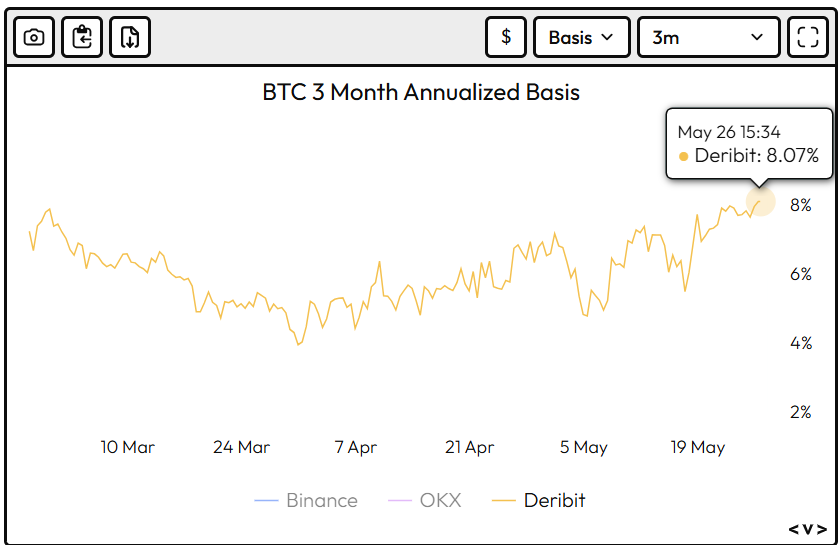

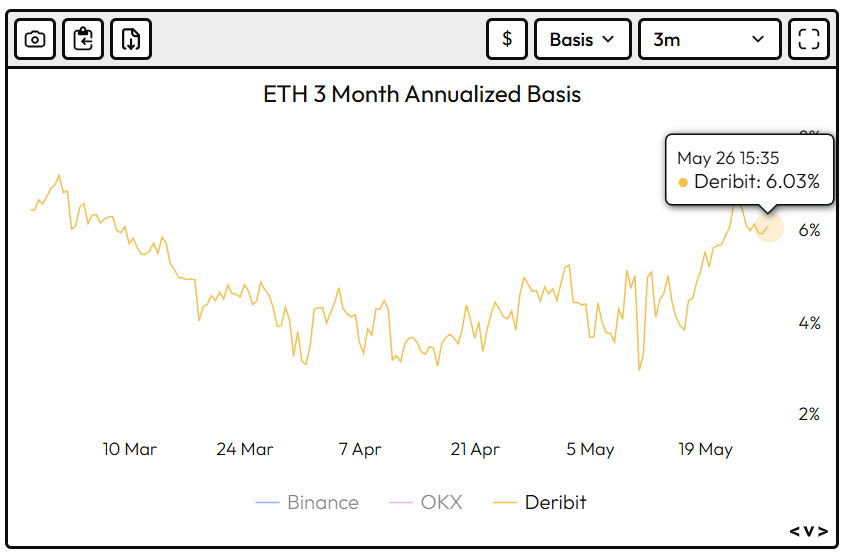

BTC and ETH basis rates are climbing as Bitcoin breaks into price discovery. The 90-day basis rate for BTC has surged to its highest level in the past three months, underscoring strong bullish sentiment among traders. Elevated basis levels in both BTC and ETH reflect increased optimism and a growing appetite for risk across the digital asset derivatives market.

90-day basis rates for BTC and ETH are currently:

- BTC 8.07%, ETH 6.03%

Trade Idea: ETH Discount Note

With risk appetite rising across the crypto market, an altcoin rally could be on the horizon. Should this scenario play out, we believe ETH is particularly well-positioned to lead the move, given its relatively oversold status compared to other major digital assets. A strategic way to gain exposure at a discounted entry point is through a Discount Note, which enables investors to participate in potential upside while entering the market below spot.

OVERVIEW

Term: 6-Months

The structure has a binary payout outcome depending on the price of ETH observed at expiry. Payout for this options strategy depends on the price of ETH at expiry with reference to the Strike Level – the two scenarios are:

Expiry Price above Strike Price (25% above current price):

- Maximum return of 36% – received in USD.

Expiry Price below Strike Price:

- 8% discounted purchase price at current levels into the ETH token – received in Spot.

RISK PROFILE

- Maximum loss for this product is the initial investment amount.

- May suit investors with a stable to moderately bullish view on ETH.

- May not suit investors who think a major bull run in ETH is likely before expiry.

- May not suit investors who think ETH will fall significantly before expiry.

Hit the desk up for all your derivatives needs.

Austin Sacks, Derivatives Analyst

What to Watch

Packed macro week with central bank action (RBNZ, BoK), inflation prints (AUS CPI, US PCE, Tokyo CPI), and Nvidia’s earnings under the AI/trade microscope. Directional risks skewed toward softer inflation and slower growth, reinforcing the global rate-cut narrative.

WED 28 May – Nvidia Earnings

All eyes on Nvidia’s Q1 FY26 earnings. AI-chip demand remains robust, but China export curbs and GB200 supply constraints are the key overhangs. Guidance will be pivotal – KeyBanc expects softer upside and trimmed H2 estimates. Street sees EPS at $0.92 on $43.09bn revenue; margins eyed at 71%.

WED 28 May – RBNZ Policy Decision

Markets fully priced for a 25bps cut to 3.25%. Trade-related uncertainty and dovish rhetoric signal further easing ahead. April’s mixed data is unlikely to derail the trajectory. Kiwi rates and NZD reaction will hinge on any forward guidance language.

WED 28 May – FOMC Minutes (7 May meeting)

Look for insight into the Fed’s read on tariff impacts and dual-mandate risk balancing. No new data since the meeting, but the tone around inflation vs labour market risk will be parsed for any policy shift cues. Notably, recent tariff de-escalation won’t be captured here.

WED 28 May – Australian CPI (Apr)

Consensus at 2.3% Y/Y (prev. 2.4%); Westpac sees 1.9%. A soft print supports the RBA’s dovish pivot after May’s 25bps cut. Sticky non-discretionary inflation remains a risk. CPI surprise will swing pricing for another rate cut in Q3.

WED 28 May – OPEC+ JMMC

Ministers may propose a 411kb/d hike for July, triple the scheduled addition. Saudi’s strategy remains focused on quota enforcement. Any aggressive supply signal could pressure crude into month-end.

THU 29 May – Bank of Korea (BoK) Decision

Q1 GDP contraction (-0.2% QoQ) tilts the balance toward resuming cuts. Market split, but dovish tone expected as growth risks outweigh inflation concerns. Rhee’s comments on sub-2.25% rates by year-end will be revisited.

FRI 30 May – Tokyo CPI (May)

Seen as a lead indicator for national CPI. Core inflation may firm slightly; comes amid weak output data and rising BoJ policy complexity. Sticky prices may keep the BoJ cautious on further easing.

FRI 30 May – US PCE Inflation (Apr)

Core PCE seen soft at +0.12% M/M, 2.5% Y/Y. Headline near 2.2%. Tariff pass-through minimal so far. Weak print would reinforce bets for 50bps Fed cuts this year. Watch for commentary from Waller, Bostic, et al. on inflation risks.

FRI 30 May – Canada GDP (Q1)

Early signs of tariff impact expected; Q1 saw pre-Liberation Day levies hit key sectors. Markets are pricing in a 25bps BoC cut with low conviction – a weak print would bolster that case amid policy split and hot CPI backdrop.

Emir Ibrahim, Analyst

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | Treasury Yields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 25 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Zerocap Participates in RBA Project Acacia

Zerocap is proud to have participated in Project Acacia, a landmark pilot led by the Reserve Bank of Australia (RBA) in collaboration with the Digital

Weekly Crypto Market Wrap: 18 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.