12 Mar, 24

Weekly Crypto Market Wrap, 12th March 2024

Zerocap provides digital asset liquidity and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

This Market Wrap edition was released on a Tuesday due to the Labour Day public holiday in Australia, on Monday 11th March.

This is not financial advice. As always, do your own research.

Week in review

- Bitcoin reaches new all-time high of $72k US dollars – Bitcoin and gold both brake new price records on the same day.

- With a market cap of $1.4 trillion, Bitcoin has surpassed silver’s global cap.

- Tether (USDT) stablecoin reaches historic $100 billion market cap.

- US SEC pushes back on spot Ethereum ETF applications for BlackRock and Fidelity.

- FED Chair Jerome Powell states US is “nowhere near” the creation of a dollar Central Bank Digital Currency (CBDC).

- El Salvador’s Bitcoin investments now at 50% profit – Central American country declared Bitcoin as legal tender back in 2021.

- European Central Bank prepares for June rate cuts as inflation falls.

- US nonfarm payrolls grow by 275k, yet unemployment rate rises to 3.9%.

Technicals

BTCUSD

And I thought last week was a week.

We were wrong on the 69,000 retest a few weeks ago but nailed it on the gamma squeeze (optionality at 65,000 and 70,000). The 25-delta skew was looking more and more weighted to OTM calls and the option market makers needed to delta-hedge their positions into these levels. Further to this, there is still an insatiable bias from the ETF issuers. The market makers are in an interesting position – and it’s playing out in the variance between crypto native futures markets (going ballistic), and the CME, which has remained fairly.. well, orderly.

All-time highs were broken, after two weeks of media debate about what level was actually the high. Above 70K, all bets are out the door – we are in new territory.

Zooming back out on the charts, it’s fascinating to see the levels we’ve marked throughout the last few years. We are now out of the woods, and heading higher.

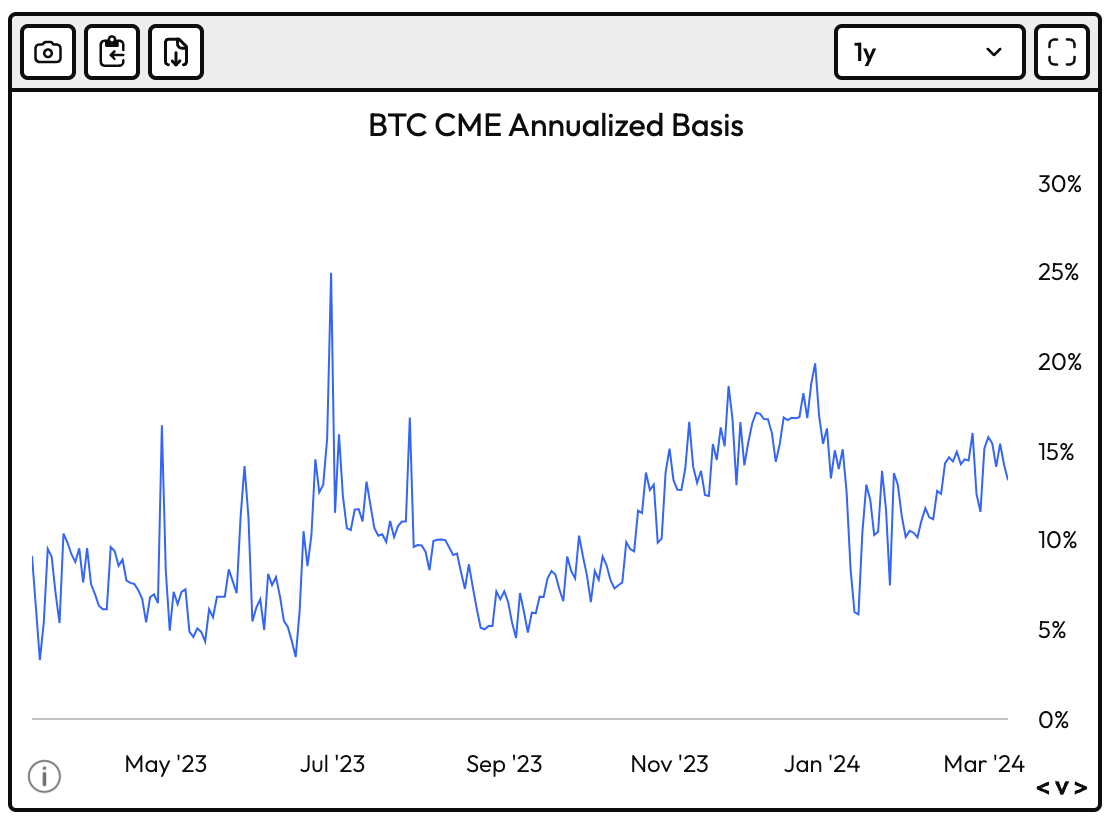

The difference between crypto native futures and the CME (institutional) futures is notable. The ETF issuers would prefer not to hedge orders in one giant market-moving block. So instead, they quietly buy spot BTC while selling CME futures. This gives them the underlying spot position ready for ETF buyers whilst not taking on directional risk. This means that they only have to unwind the futures shorts to sate the ETF bidding. The fact that the CME basis has remained relatively stable is telling – there are as many leveraged buyers as hedgers in the insto game, and this could be a coiled spring winding up. Our take is that the difference between crypto native and institutional markets is growing so wide, the arb opportunity will likely lead to reversion one way or another. But this could mean increased spot pressure to the upside as the basis collapses. In the end, the spot ETFs are backed by true underlying Bitcoin, not derivatives – and we don’t see the ETF buying pressure ending this month.. or next. In fact, it’ll probably take an ETH or SOL ETF announcement to ease some of the pressure. On top of this, we have a self-fulfilling prophecy building, that “crypto is uncorrelated from traditional markets!” If this narrative continues to grow, and more market participants hedge… we could have more gamma to come.

Key levels

50,000 / 69,000 / 70,000 / 80,000

Spot desk

Volatility

Increased volatility across the board on the spot desk. Notably, Tether briefly traded 20bps above parity at one point during the week, something we don’t see every day. Because of this, the desk had an increase in offramp activity from clients who were opportunistically looking to offload them at a favourable premium.

We are seeing increasing altcoin and majors’ flows, with BTC and ETH bids and certain alts getting some love. We are very interested in Fantom’s move, catching up to some of the other layer-1s. Full disclaimer, we bought Fantom during their private pre-seed sale many years ago – many of us still hold, I was the chump who sold mine to buy a house a few weeks back. Nonetheless – we think the DAG-based blockchain has some amazing benefits in the overall crypto ecosystem, and we wouldn’t be surprised to see more buying on the desk as this narrative builds some steam.

* Zerocap and staff hold proprietary positions in this token.

Inflation Narrative

With US CPI coming out this Tuesday, we will be watching intermarket volatility into the release. Keep an eye out for the all-time high level of 69,000 as the inflation figure could be a contentious one at these levels if we see any risk-off outliers. This said, sentiment is almost unstoppable (it seems). Every dump, we get a very fast reversion back to highs. This will not last forever, but in the meantime – be very wary of fading moves higher… or fading anything that starts with a “c” (crypto).

Trade idea: $ACE (Fusionist)

The Fusionist (ACE) token is a digital asset that operates on the Fusion blockchain network. It serves as the native currency within the Fusion ecosystem, enabling users to access and utilise various decentralised finance (DeFi) services and features. The purpose of the Fusionist (ACE) token is to facilitate seamless and secure value transfer, smart contract execution, and decentralised governance within the Fusion network. Additionally, it incentivizes network participants to contribute to the growth and development of the ecosystem through staking and participating in community-driven decision-making processes.

Fundamentals are strong, alongside some upcoming event risk – Fusionist’s Endurance upgrade was scheduled to take place on March 5th. Staking and validator functionalities will be activated following Endurance’s upgrade completion. The team also teased a major update coming in March.

This would be a momentum play on overall market sentiment, in a project with real fundamentals. Keep in mind, with any altcoin – you risk it going to zero.

Given spikes down to $10, we’d look at a cheeky $10.50 entry if you had a view.

Derivatives desk

WHOLESALE INVESTORS ONLY

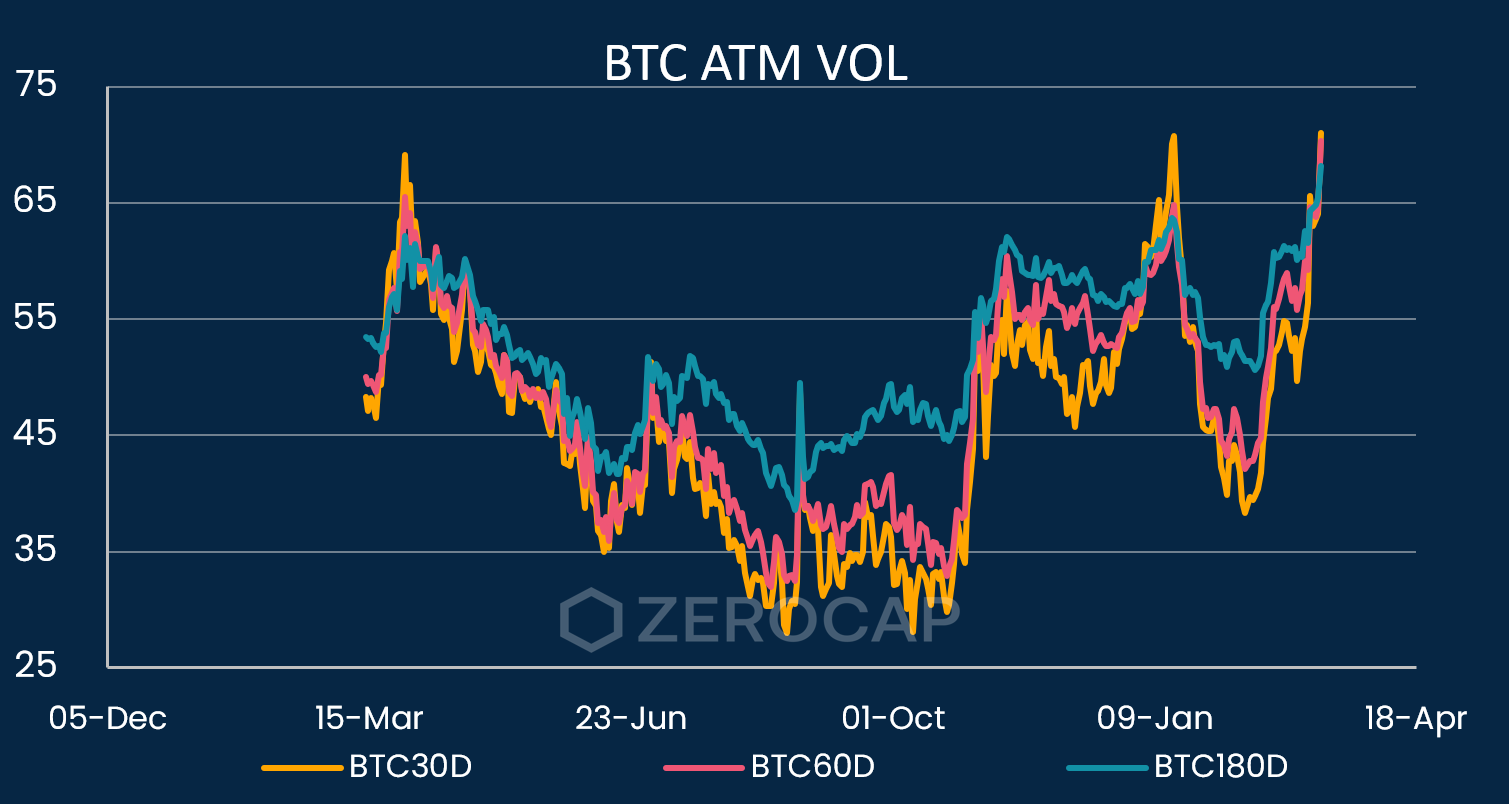

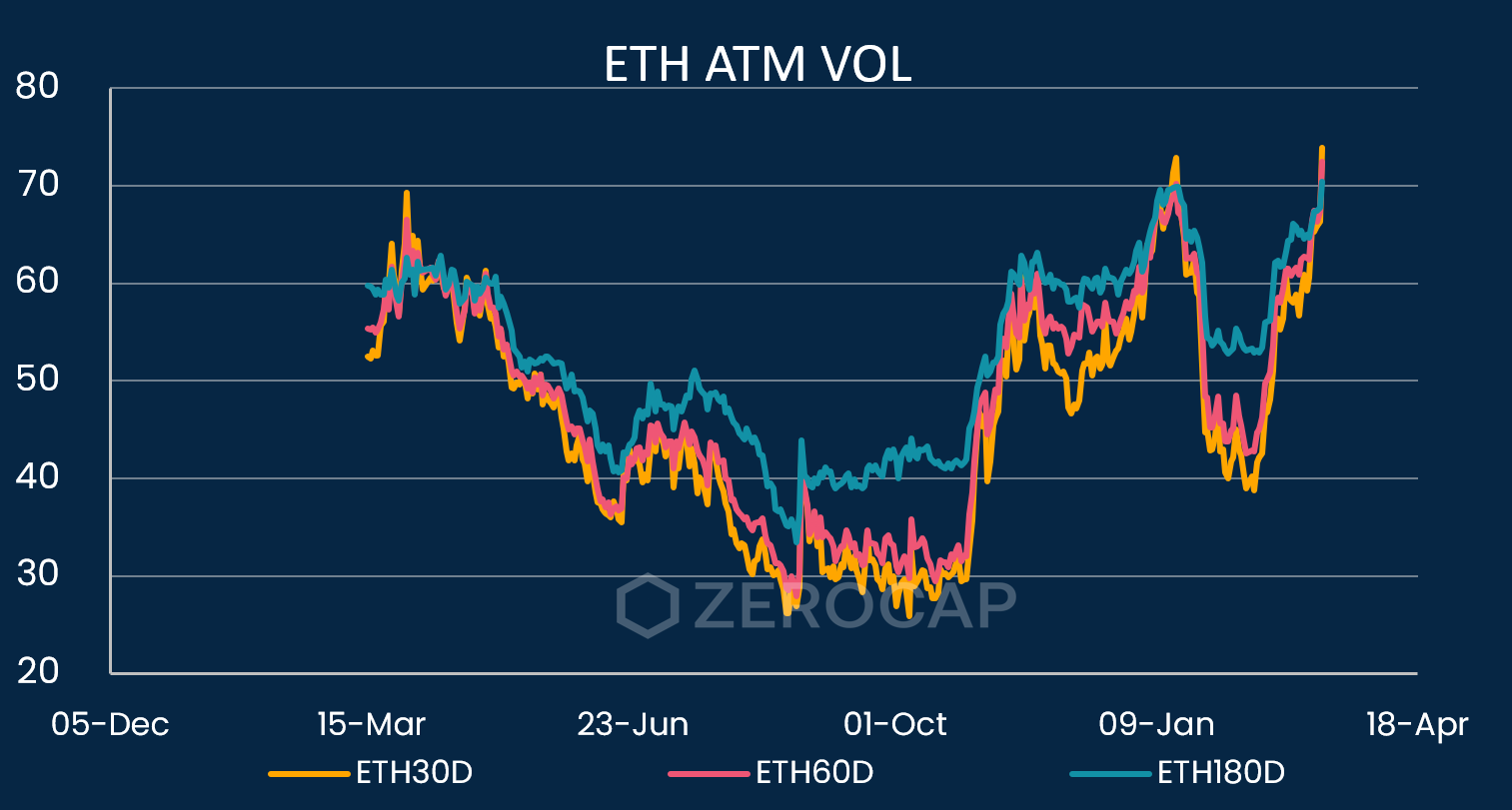

Protection is becoming expensive

At-the-money implied volatility has broken the January highs on both BTC and ETH. As shown below, it has more than doubled since October last year: 30-day ATM IV reached 70.33 (BTC) and 72.43 (ETH). We are back, baby!

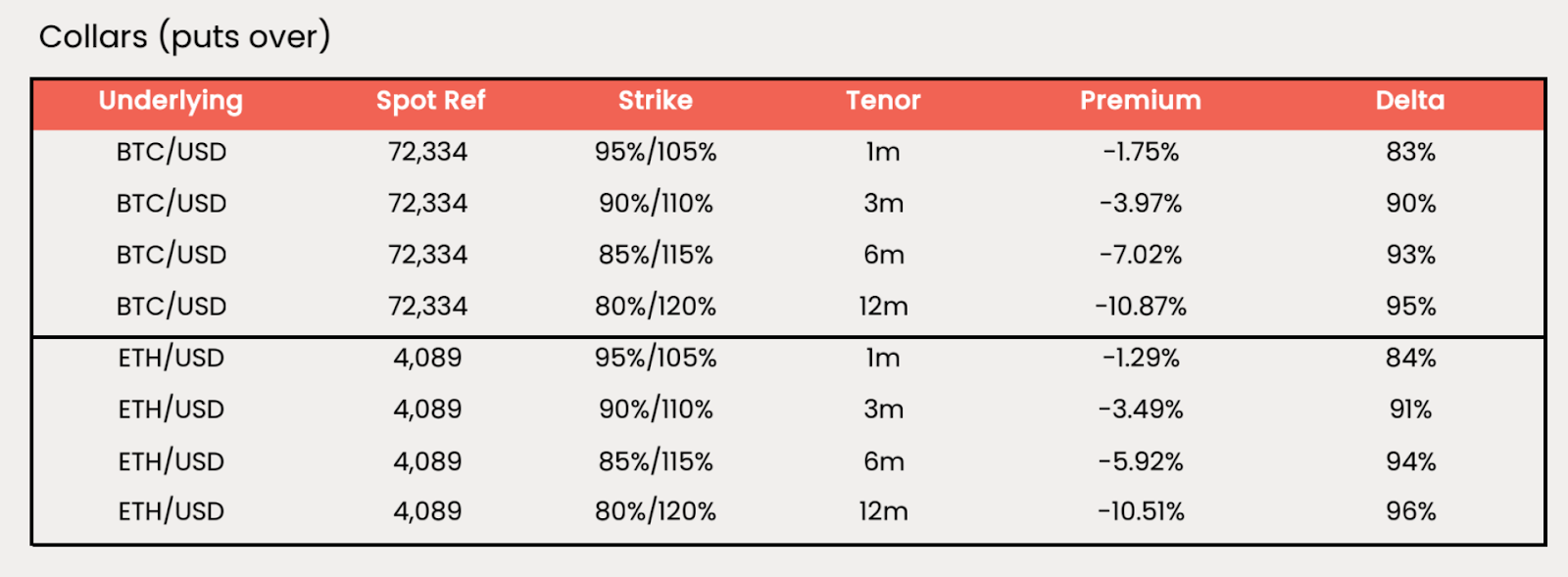

Cheapen up protection with Collars

Investors looking for cheaper downside protection can take advantage of the current skew towards calls – sell some of their upside for cheaper protection on the downside. Symmetrical collars are paying decent premiums at the moment for both BTC and ETH. Reach out to our team for pricing on collar products.

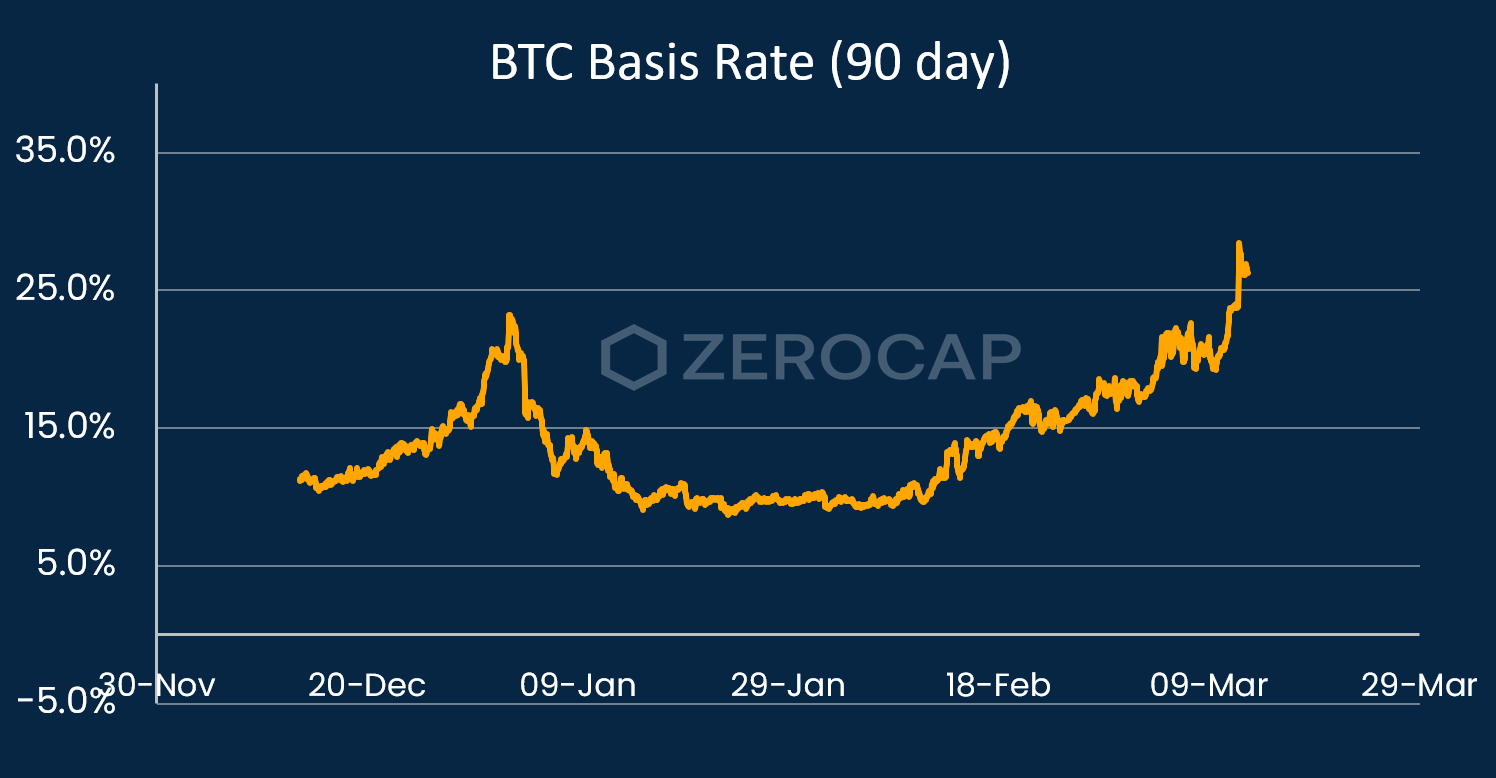

Basis Rate continues higher

The BTC Basis rate is now sitting above 25% annualised on longer-dated Futures contracts. We are seeing demand to capture the yield premium from this flow via the basis trade.

We honestly think this is one of the greatest USD funding trades around – get in touch, we’d love to package it up for you.

Contact the derivatives team at [email protected] for more information.

What to Watch

- US monthly and yearly CPI reports and 10-year bond auctions, on Tuesday.

- UK’s monthly GDP and US 30-year bond auctions, on Wednesday.

- Ethereum network’s long-awaited Dencun upgrade, on Wednesday.

- US monthly retail sales and unemployment claims, on Thursday.

- Empire State manufacturing index, on Friday.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | Treasury Yields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.