Content

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi

- Innovation

- Altcoins

- NFTs & Metaverse

- What to Watch

- DISCLAIMER

- Zerocap Pty Ltd carries out regulated and unregulated activities.

- FAQs

- What significant event occurred with Zerocap in the week of 9th January 2023?

- What was the significant event in the Ethereum network during this week?

- What was the notable development in the DeFi space during this week?

- What was the significant event in the NFT and Metaverse space in this week?

- What was the significant development with BMW during this week?

9 Jan, 23

Weekly Crypto Market Wrap, 9th January 2023

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi

- Innovation

- Altcoins

- NFTs & Metaverse

- What to Watch

- DISCLAIMER

- Zerocap Pty Ltd carries out regulated and unregulated activities.

- FAQs

- What significant event occurred with Zerocap in the week of 9th January 2023?

- What was the significant event in the Ethereum network during this week?

- What was the notable development in the DeFi space during this week?

- What was the significant event in the NFT and Metaverse space in this week?

- What was the significant development with BMW during this week?

Zerocap provides digital asset investment and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

Week in Review

- Zerocap has been chosen by the Voluntary Administrators of Digital Surge to provide custodial and administration services to the business, securing and safely storing client digital assets.

- Bitcoin Genesis Day: First cryptocurrency completes 14 years since origin block created.

- FTX founder Sam Bankman-Fried (SBF) pleads not guilty of all counts in US federal court – US authorities create page to notify alleged FTX victims about SBF’s case.

- Ethereum transactions surpass Bitcoin by four-fold, 338% higher than 2021.

- European Central Bank urges CBDC development to benefit the crypto ecosystem.

- Coinbase reaches $100 million settlement with New York regulators due to poor KYC.

- China launches state-sanctioned NFT platform, reversing course on past crackdowns.

- Metaverse initiatives to possibly create $5 trillion in value by 2030; McKinsey report.

- Celsius founder Alex Mashinsky sued by New York Attorney General for allegedly hiding platform’s financial condition from investors.

- US SEC files objection to Binance.US acquiring crypto lender Voyage Digiital.

- Twitter security breach: leak of user email addresses totals at least 200 million.

- US Jolts Job Openings reach more than expected 10.5 million, while wage growth slows.

- FOMC Meeting Minutes: decision to step down from 75 to 50bps not an indication of weakening price stability goal, FED still sees higher inflation as “key factor” going ahead.

Winners & Losers

Macro Environment

- 2022’s yearly close saw all three major stock indices in the United States (US) (Dow Jones (DJIA), S&P 500 (SPX), and Nasdaq (NDX) suffer significant losses, marking the worst year for equities since 2008. The Dow fared best of the three, falling -9.22%, while the S&P 500 and Nasdaq fell -19.98% and -33.73% YoY respectively. The sharp decline across the board was attributed to persistently sticky inflation, an aggressive US Federal Reserve, volatile economic data, and escalating geopolitical tensions. Economists are expecting current bear market conditions to persevere until markets are either plunged into recession or bolstered by a dovish FED pivot – where an acceptable level of price stability has been re-established. Analysts further stipulate that Q1 2023 will see markets retest 2022’s lows prior to a broader macroeconomic recovery.

- Despite the reopening of China’s borders, Tuesday’s Caixin General Manufacturing PMI unveiled a fifth consecutive monthly decline in factory activity to 49.0 for the month of December 2022 – slightly above the 48.8 market expectation. Senior Economist at Caixin Insight Group Wang Zhe claimed the ongoing “Fallout from the pandemic” has been placing undue stress on both production and sales, with all output and total new order subindices contracting for their 4th-5th consecutive months respectively. Moreover, dwindling overseas demand and general global economic weakness have assisted in pushing buyer activity down towards April’s lows earlier in the year.

- Vital US employment data continued to be released throughout the week. Wednesday’s Job Openings and Labor Turnover Survey (JOLTS) for November depicted a fall in openings of -54,000 to 10.458 million, well above the 10 million consensus figure. There were notable decreases in job openings in the finance and insurance sector (-75,000) and in the federal government (-44,000) over the past month. On the other hand, there were marked increases in professional and business services (+212,000) and in nondurable goods manufacturing (+39,000).

- A strong ADP Report released on Thursday showed private sector employment expanded by +235,000 jobs in December, with an annual pay increase of 7.3% YoY (lowest since March 2022). Nela Richardson, the Chief Economist, ADP elaborated on the increase: “The labor market is strong but fragmented, with hiring varying sharply by industry and establishment Size.” The report found increased employment in small to medium-sized establishments ranging from +32,000 to +159,000 additional hires, and steep reduction in large enterprise employment down -151,000. Transportation, Trade and Utilities industries were amongst the worst affected -24,000, whilst leisure and hospitality saw gains in excess of +123,000 jobs.

- Markets remained on edge until Friday’s release of the monthly Non-Farm Payroll Report, seeing total nonfarm payrolls decelerate to +223,000, and unemployment falling to 3.5% in December. Despite the report showing relative strength within the labour market, slowing wage growth numbers on average hourly earnings – up just 0.3% MoM and 4.6% YoY (Compared to 0.4% and 5% same time last year) saw markets takeoff. Investors are now looking to January 12th CPI numbers to confirm a 25 basis point hike in February’s FOMC meeting – FED fund futures at the time of writing are implying around a 25% chance of a 50 bps hike.

- A surge in portfolio allocation into the weekend saw fixed-income markets flourish – evidenced in the $63.7 billion worth of US Marketed debt issued in the first seven days of 2023 according to Dealogic. Gold was a standout performer alongside select growth stocks – Gold closing the week up 1.52% at 1,866. A weaker Dollar (DXY) slumped -0.62% WoW and saw FX Majors trace upwards.

Technicals & Order Flow

Bitcoin

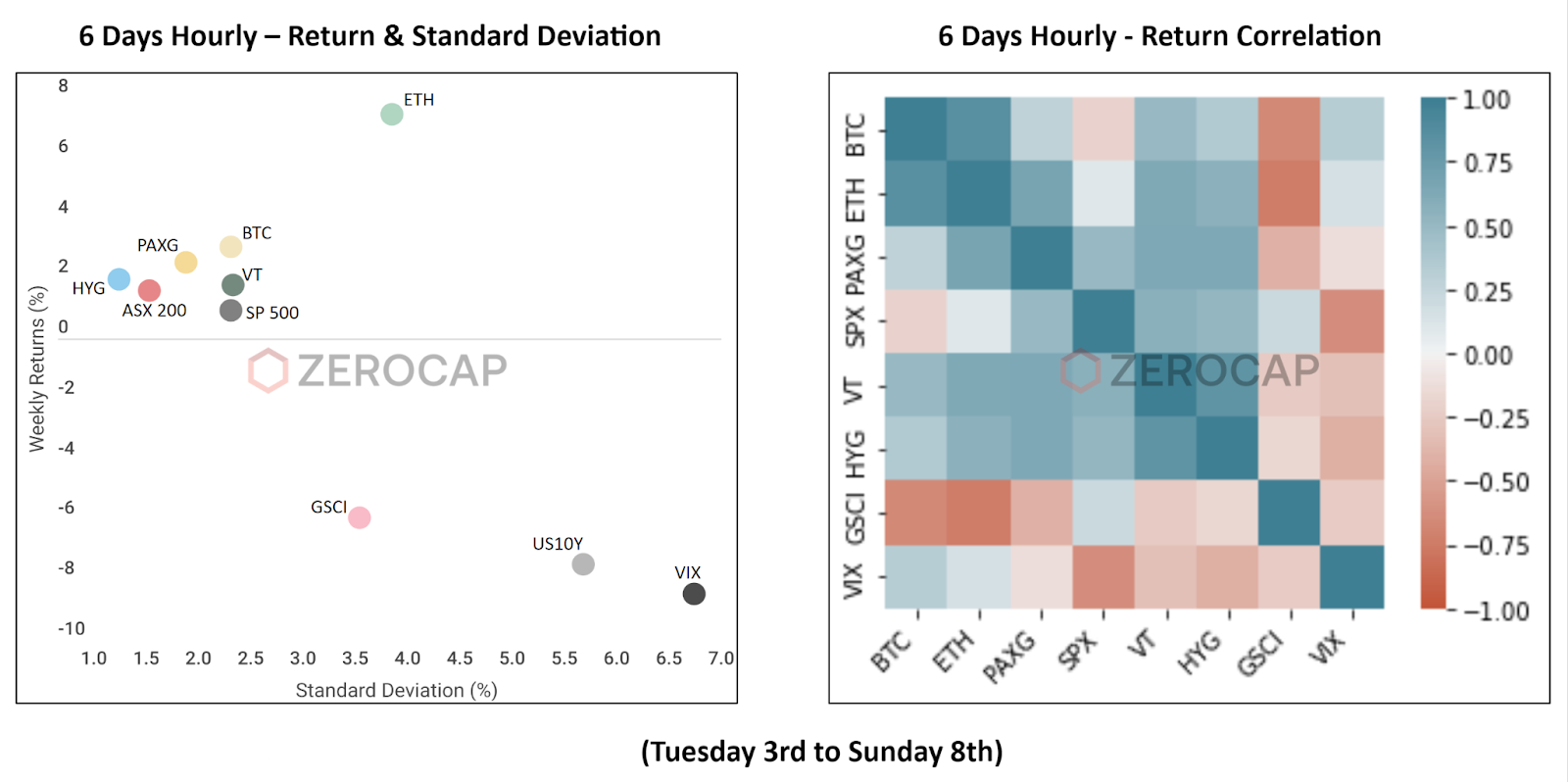

- BTC remained range bound with very low volatility, finding light bids below 16,670 while facing resistance above 16,750. However, on Wednesday, BTC broke through 16,750 before halting prior to 17,000, a key resistance level that was further respected later in the week. Soon after, a change in sentiment sent prices lower with the 16,750-16,700 zone serving as downside support, suggesting its relevance in the short term. Nonetheless, BTC ascended into the weekend, closing +3.03% WoW.

- In the lead-up to the release of the FOMC minutes on Wednesday, BTC edged higher. Notably, the move was exaggerated by short liquidations and later justified by positive ISM data. The print left investors with the impression that the FED may reduce further rate hikes and BTC subsequently climbed toward 17,000. However, the FOMC minutes outlined that a continued restrictive policy stance is not off the table until core inflation is brought under control and BTC edges lower. Shortly after, NFP and Unemployment figures out of the U.S. came in better than expected. Yet, BTC’s action suffered, moving lower due to a perceived sense of economic flexibility in the context of continued hawkish monetary policy from the FED.

- Meanwhile, BTC appears to be relatively numb to internal events with an announcement regarding a change to Mt. Gox’s creditor repayment selection from Jan 10. To Mar 10 and simmering concerns related to DCG possessing little impact on price action.

- Recently, we’ve mentioned the drying up of liquidity on exchanges due to heightened counterparty risk and fear following FTX’s capitulation. This downtrend has halted and could be indicative of recovering sentiment. A continuation of improved faith bodes well for both future price action and continued advancement within the space.

- Since FTX, Bitcoin’s 30d implied volatility has tracked lower and recently touched all-time lows. This behaviour outlines a void of expected volatility in the near term and re-affirms the lack of perceived significance surrounding DCG’s unfolding narrative – however, we are also seeing more HFT funds and trad prop participants enter the market to sell volatility which is compressing realised and implied volatility. As they say; “what goes up, must come down” and vice versa, right?

- BTC’s most recent difficulty adjustment suggests continued signs of miner capitulation. Historically, mining difficulty has possessed a cyclical relationship with price. Miner capitulation is often present in late-stage bear markets. Moving into 2023, this metric will be useful in analysing both the unfolding narrative surrounding miners and the health of the overall market.

- Last week, Bitcoin’s action seemingly ignored developments specific to the space while following suit with changing macroeconomic expectations. While the halt of exchange withdrawals may suggest improving sentiment, it is likely that the macro environment will continue to dictate action. Notably, participants are currently leaning toward a 25bp rate hike for February’s meeting. Moreover, all eyes are placed on this coming week’s CPI printout of the U.S.

Ethereum

- Like Bitcoin, we are seeing compressed volatility in Ethereum. ETH began the week in a choppy range between 1,1160 and 1,200 and was quick to sweep the lows causing minor long liquidations before reclaiming the range and breaking to the topside. By Tuesday 1,220 was established as the next resistance level, causing another small range to form. With increased passive liquidity (as displayed by deeper order books and tightening bid/ask spreads mid-week) price continued to build out intraday ranges due to a lack of aggressive market participants. Wednesday, Friday and Sunday all saw minor range breaks to the upside as shorts stopped out and market bid volume spiked. ETH closed the week at 1,290 for a 7.48% increase WoW.

ETHBTC Daily Chart

- ETH/BTC has seen its largest weekly outperformance since October as excitement about the Shanghai upgrade and its impact on staking sets in. The previous resistance level of 0.0726 that had suppressed price throughout December was finally broken on the sector’s Wednesday rally. This sparked continuation to the upside into the weekend to close out the week at 0.0753, a weekly return of 4.28%. The pair’s impressive performance over the course of this bear market leads many to forecast an all-time-high breakout in the coming year as Ethereum further entrenches itself at the core of the industry.

- In line with ETH/BTC’s breakout we have seen open interest in ETH trend higher in recent weeks. A host of Ethereum-based narratives have spun up of late causing reflexive growth for the asset’s relative performance. The Shanghai upgrade is likely to occur this quarter, layer-2s are seeing significant growth and alt layer-1s are dwindling in comparison. All of which indicates a strengthening ecosystem positioning for the asset. As BTC falls back on its store of value narrative and ETH flourishes into a burgeoning hub of on-chain activity, 2023 could be the year that we see a tangible divergence in price drivers for the two assets.

- Ethereum developers have announced plans to move forward with the Shanghai upgrade, which will allow users to withdraw ETH that has been staked on The Beacon Chain. The upgrade was originally slated for March, but will now prioritise enabling token withdrawals over other potential changes. Before the most recent core developer call, it was uncertain whether the Shanghai upgrade would focus on more developments including Proto-Danksharding; however, it is now known that this upgrade will solely concentrate on the withdrawal of staked tokens. As a result of these upgrades, it is expected that more people and institutional investors will participate in staking to support the Ethereum network and earn yield. Currently, with nearly 13.8% of circulating ETH tokens staked, these coins have a value of over $21 billion.

DeFi

- Smart contract security firm, Dedaub, identified a vulnerability in Uniswap’s Universal Router smart contract that could have allowed for reentrancy attacks and drained user funds mid-transaction. Uniswap launched a bug bounty program in late 2022 in order to assure the safety and efficacy of its protocol following the launch of its NFT-related aggregator features, and awarded Dedaub $40k for flagging the vulnerability; this included a 33% bonus for reporting the issue during Uniswap’s bonus period in November 2022. The vulnerability was classified as medium severity with a high impact and low likelihood by Uniswap.

- SushiSwap, an Ethereum-based DeFi platform, has announced that it will be winding down its token launchpad and lending protocol due to financial difficulties and the need to effectively allocate resources for the survival of the main protocol. According to the company’s CTO, Kashi, the lending protocol, was flawed and operating at a loss, while MISO, the launchpad, required a significant amount of resources. SushiSwap will now prioritise its popular decentralised exchange network. The company’s CEO recently revealed a $30 million loss over the past year, hence the decision to discontinue the launchpad and lending protocol is part of the company’s efforts to address its financial challenges.

Innovation

- BMW has partnered with Coinweb, a decentralised blockchain layer 2 network, to integrate blockchain-based solutions into its Thailand operations. This will see the development of a smart contracts platform to simplify the financing process for BMW vehicles. Another focus of the collaboration is the creation of a blockchain-based loyalty program for customers. Coinweb will leverage Binance’s BNB Chain for transactions, with the option of broadcasting them to other blockchains when required. The CEO of BMW Leasing in Thailand remarked that the adoption of decentralised tech platforms will enhance “infallible efficiency and transparency”.

Altcoins

- Decentralised liquid staking platform, Lido, has seen substantial traction as of late with a new narrative emerging in the lead-up to Ethereum’s Shanghai upgrade. Upon withdrawals from Ethereum’s Beacon Chain being unlocked, liquid staked tokens like Lido’s stETH will be exchangeable for 1 ETH, with the underlying platforms taking a cut on all redemptions of staked positions. Amidst this narrative playing out, Lido’s governance token, LDO, rose over 100% WoW after benefiting from a squeeze of the positions of those shorting the token.

- A Solana-based token, BONK, saw quadruple-digit gains over the week as traders jumped into the token. BONK is another dog-inspired meme coin that is intended to be used across the Solana ecosystem and has already seen over 50 dApp integrations. In line with the rising token price of BONK, Solana’s SOL finally saw positive price appreciation after facing downward selling pressure following the FTX collapse. It is possible that the nearly 70% WoW price increase of SOL led to eyes turning back to the blockchain, before eventually finding BONK.

NFTs & Metaverse

- Hong Kong’s Animoca Brands has revised its fundraising target for its new metaverse-focused investment fund, Animoca Capital. The company’s chairman, Yat Siu, stated in a Twitter Spaces interview that it now aims to raise approximately $1 billion in Q1 2023; reflecting a fall from its original target for the fund of $2 billion. Nonetheless, Siu acknowledged that market conditions may impact the final amount raised. As well as the difficulty Animoca faces in raising capital, the company is dealing with issues relating to getting its financial reports audited. The firm was granted an extension for its 2020 financial report despite it initially being the request from Australian regulators that it be audited by the end of 2022.

- China has launched a national digital asset exchange for NFTs and the metaverse. The China Digital Assets Trading Platform (CDEX) was created by the China Technology Exchange, the Cultural Relics Exchange, and the Copyright Service Centre to standardise the trading process and eliminate black market speculation. It aims to act as a credible inventory service mechanism for tradeable digital assets by providing registration, verification and rights monitoring through the China Cultural Protection Chain. The platform, which only has a live sign-up process at present, was created in response to the speculation surrounding NFTs; Chinese tech giants like Tencent, Ant, Baidu and JD all banned the secondary trading of digital collectibles in mid-2022 in response to concerns.

What to Watch

- Australian CPI and FED Chair Jerome Powell to speak at Riksbank’s International Symposium, on Tuesday.

- US CPI, on Wednesday.

- UK’s monthly GDP report and US’ preliminary University of Michigan Consumer Sentiment, on Friday.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice,take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

FAQs

What significant event occurred with Zerocap in the week of 9th January 2023?

Zerocap was chosen by the Voluntary Administrators of Digital Surge to provide custodial and administration services to the business, securing and safely storing client digital assets.

What was the significant event in the Ethereum network during this week?

Ethereum developers announced plans to move forward with the Shanghai upgrade, which will allow users to withdraw ETH that has been staked on The Beacon Chain. The upgrade was originally slated for March, but will now prioritize enabling token withdrawals over other potential changes.

What was the notable development in the DeFi space during this week?

SushiSwap, an Ethereum-based DeFi platform, announced that it will be winding down its token launchpad and lending protocol due to financial difficulties and the need to effectively allocate resources for the survival of the main protocol.

What was the significant event in the NFT and Metaverse space in this week?

China launched a national digital asset exchange for NFTs and the metaverse. The China Digital Assets Trading Platform (CDEX) was created by the China Technology Exchange, the Cultural Relics Exchange, and the Copyright Service Centre to standardize the trading process and eliminate black market speculation.

What was the significant development with BMW during this week?

BMW partnered with Coinweb, a decentralized blockchain layer 2 network, to integrate blockchain-based solutions into its Thailand operations. This will see the development of a smart contracts platform to simplify the financing process for BMW vehicles and the creation of a blockchain-based loyalty program for customers.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Interview with Ausbiz: How Trump’s Potential Presidency Could Shape the Crypto Market

Read more in a recent interview with Jon de Wet, CIO of Zerocap, on Ausbiz TV. 23 July 2024: The crypto market has always been

Weekly Crypto Market Wrap, 22nd July 2024

Download the PDF Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact

What are Crypto OTC Desks and Why Should I Use One?

Cryptocurrencies have gained massive popularity over the past decade, attracting individual and institutional investors, leading to the emergence of various trading platforms and services, including

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.