Content

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi

- Innovation

- Altcoins

- NFTs & Metaverse

- What to Watch

- Insights & Events

- Disclaimer

- FAQs

- What were the key developments in the crypto market during the week of 3rd October 2022?

- What was the impact of the UK's tax cuts on the crypto market in the week of 3rd October 2022?

- What were the technical trends observed in Bitcoin and Ethereum during the week of 3rd October 2022?

- What were the major innovations in the crypto market during the week of 3rd October 2022?

- What were the key developments in the NFT and Metaverse space during the week of 3rd October 2022?

3 Oct, 22

Weekly Crypto Market Wrap, 3rd October 2022

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi

- Innovation

- Altcoins

- NFTs & Metaverse

- What to Watch

- Insights & Events

- Disclaimer

- FAQs

- What were the key developments in the crypto market during the week of 3rd October 2022?

- What was the impact of the UK's tax cuts on the crypto market in the week of 3rd October 2022?

- What were the technical trends observed in Bitcoin and Ethereum during the week of 3rd October 2022?

- What were the major innovations in the crypto market during the week of 3rd October 2022?

- What were the key developments in the NFT and Metaverse space during the week of 3rd October 2022?

Zerocap provides digital asset investment and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

Week in Review

- FED Chair Jerome Powell states DeFi needs appropriate regulation before attending to retail customers during Banque de France’s event on tokenisation.

- CFTC Chair Rostin Behnam states “Bitcoin might double in price if there’s a CFTC-regulated market” during NYU seminar, continues push towards regulatory clarity.

- One million Australians to start investing in crypto in the next 12 months; survey.

- Australia to start testing its digital dollar mid-2023; RBA whitepaper

- Meta introduces NFT cross-posting and sharing on Instagram – Apple includes NFTs for in-app purchases, faces backlash for 30% sales fee.

- Interpol officially issues Red Notice against Terra co-founder Do Kwon – Terraform Labs claims case is politicized to WSJ, $67 million in BTC frozen due to ties with Kwon.

- Celsius CEO Alex Mashinsky resigns, FTX considers asset bid bailout.

- Ripple (XRP) scores another win against US SEC as judge overrules commission.

- Putin annexes Ukrainian regions, Ukraine formally applies for NATO membership – on recent threats, Biden states US will defend “every single inch” of NATO territory.

- US’ Core PCE reaches higher-than-expected 6.2% for August – mortgage rates climb to 6.7% for 15-year fixed-rate loans, the highest since 2008.

- UK inflation continues to hit new highs, Euro zone soars to record 10% – GPD at record lows, EUR plummets under economic outlook.

Winners & Losers

Macro Environment

- The United Kingdom (UK) made headlines again this week, following the fallout of its iniquitous tax cuts announced the week prior, seeing a 5% tax slashed from the UK’s highest-paid workers – earning in excess of £150,000 per year. Analysts further speculate that the tax cuts will be funded by future out-rated welfare payments. The UK government, saving in excess of £11 billion – by matching growth in government benefits with earnings as opposed to inflation, is predicted to reach as high as 10% for the month of September. The tax cuts forced the Bank of England (BOE) to flip its quantitative tightening measures, initiating a £65 billion bond buyback scheme in order to circumvent mass insolvency in the pension fund sector and large holders of long-term gilts. The International Monetary Fund (IMF) further condemned the Truss government’s mini-budget, stating “untargeted fiscal packages at this juncture” were unwise – the pound sterling (GBP) tanking to an all-time low of $1.036 on September 26th.

- North Korea’s military presence in its eastern waters continued to heat up following a series of South Korean – United States bilateral military exercises involving the nuclear submarine: USS Ronald Reagan. North Korea responded just two days after the exercises concluded by conducting two ballistic missile tests, each landing within the sea of Japan. Japanese Vice Defence Minister Toshiro Ino commented on the missile tests, exclaiming that: “North Korea’s actions threaten the peace and safety not only for Japan but also the region and the international community, and are absolutely impermissible.” Asian foreign exchange markets were similarly armed with a stronger US dollar, and the Chinese Yuan (CNY) extended a 28th-month low of ¥7.26724 on Wednesday. Evidence suggests that market participants are racing to secure their forward dollar buying contacts before the People’s Bank of China’s (PBOC) moves to raise FX risk reserves to 20%, in a bid to bolster Yuan strength. Since the Japanese government’s “Yentervention” the Yen has since retraced to ¥145.90, just ¥0.10 shy of 1998’s high of ¥146. Markets seem to have become increasingly concerned about the depreciating Asian currencies, with the potential for capital flight en masse if conditions continue to worsen.

- The Reserve Bank of Australia (RBA) revealed on Monday that since shoring up the economy throughout the Covid pandemic, it has amounted to a net loss of $37 billion AUD – the largest ever, resulting in negative equity of $12.4 billion. The consequence of the numerous government support programs such as Job Keeper, during the first two years of the pandemic, has led to the deficit. A recent review of the government bond-buying program revealed the funding of the benefits programs via bond issuance and buybacks with freshly printed money. The $281 billion purchased in bonds enabled the RBA to simultaneously fund the government programs whilst also lowering the general level of interest rates within onshore bond markets.

- S&P 500 closed its third straight quarterly loss since 2009, US treasuries fell on Friday following a month-end sell-off seeing 10-year yields hover at 3.83%. The Australian dollar closed weaker at around $0.64 AUD/USD, the Yen back below ¥145 at ¥144.70, and the Euro treading water at $0.98 (EUR/USD).

Technicals & Order Flow

Bitcoin

- Early last week, Bitcoin was bid up as traders moved out of GBP and into BTC, as marked record volumes have shown between the BTC/GBP pair. However, bears made their presence known, forcing action to remain below 20,250. Substantial selling volumes pushed the price below the 18,750 support before being firmly bid at 18,460, a support that is growing in relevance. Toward the latter part of the week, the price consolidated between 19,250 and 19,650 and closed +1.29% WoW. Recent action has remained contained within an ascending triangle pattern drawn from September lows.

- A poorly received 2022 economic Growth Plan out of the U.K. sent the British pound to all-time lows against the USD. Trading volumes between the GBP and Bitcoin spiked to a record high during Monday’s session as participants moved out of the sterling. Bitcoin’s action benefited. However, on Tuesday, the depreciation of the sterling sparked global recessionary fears.

- Sentiment was quick to revert following the BOE’s announcement outlining their plan to purchase 65b pounds worth of long-dated bonds. As short-term concerns were alleviated, risk appetite returned and Bitcoin edged higher. Bitcoin’s late week action remained compressed, we believe as a result of Apple stock’s grading being revised by the Bank of America initiating a sell-off in equities, a -0.6% QoQ GDP growth rate print out of the US and Fed Vice Chair Lael Brainard’s speech reminding participants of the Fed’s mission to bring down inflation through further rate hikes.

- Bitcoin’s Market Value to Realised Value Z-Score is a metric that takes the market cap of Bitcoin and divides it by the cost basis of positions in the market – it basically shows how much of the market has profitable or unprofitable positions. The metric is used to analyse whether BTC is under or overvalued and can identify cyclical trends. Since mid-June, Bitcoin has resided within a zone that is indicative of a cyclical bottom. This narrative corresponds with the recent accumulation of firmer hands such as long-term holders.

- During the aforementioned period, Bitcoin’s mining difficulty has appreciated to new all-time highs. While this trend can be indicative of improved network health and potentially improved efficiency amongst miners, it may also represent the increasing cost of mining Bitcoin. Notably, in the most recent adjustment, Bitcoin’s mining difficulty was lowered.

- Alongside the increased cost of mining, during September, BTC miner net position change persisted at negative levels, behaviour that implies BTC miners are selling in the face of increasing costs and diminishing returns.

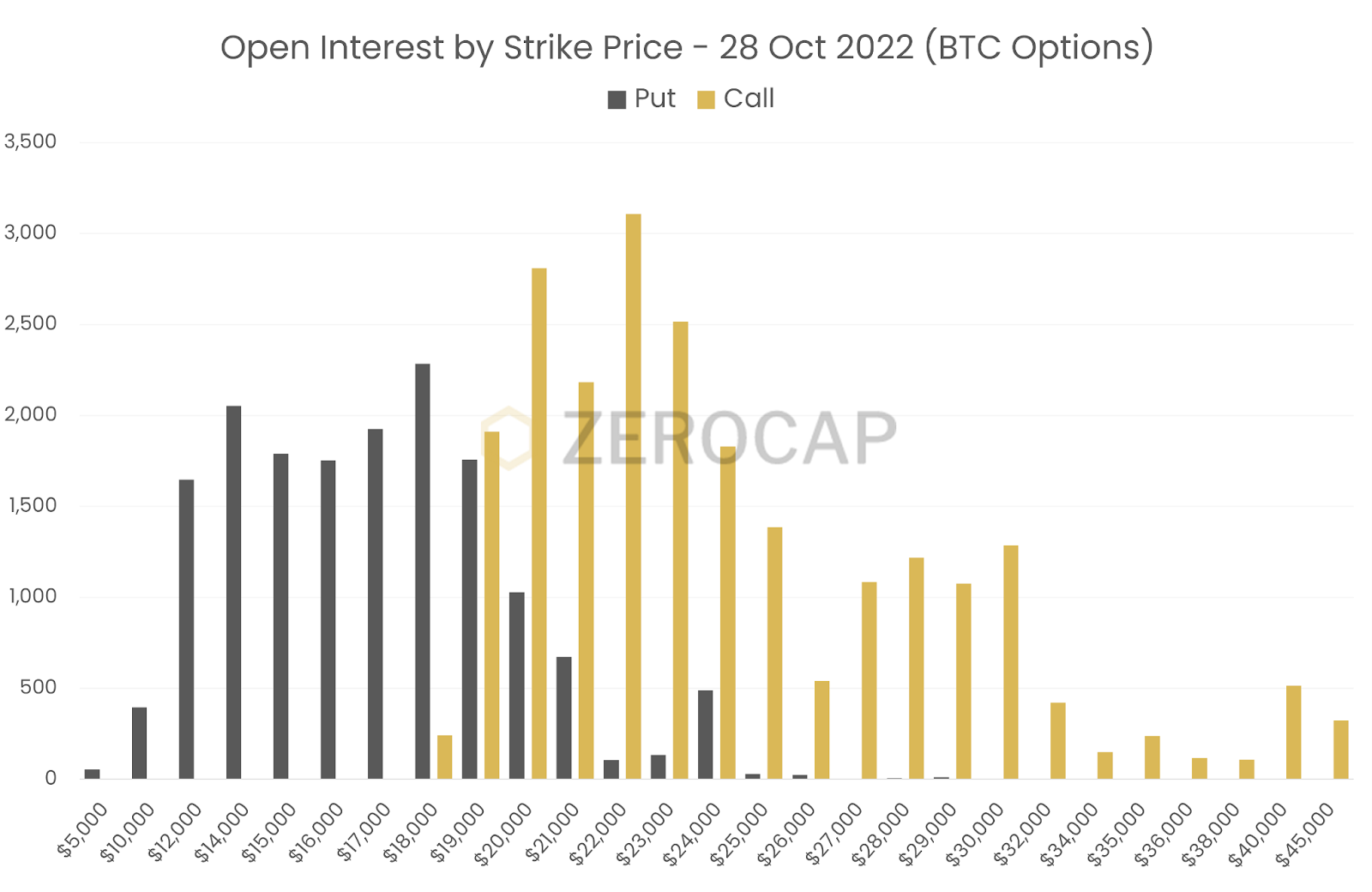

- Looking out to the October 28th options expiry, key short-term levels can be identified. There has been some interest in call strikes between 19,000 and 24,000. Correspondingly, there is also notable interest between the 12,000 and 19,000 strikes for puts as traders account for the potential of continued downside action.

- The macro environment continues to dictate action within the digital asset space. While the flows from GBP into BTC bolstered Bitcoin’s early week action, recessionary fears proved hurtful. This, alongside concerning economic data the US and the continued likelihood of further hikes acted to hinder any notable appreciation. While Bitcoin resides at relatively attractive levels, miners seem to be feeling the effects of increased costs. As markets enter the new month, participants look to start-of-month data prints from key monetary bodies to provide clarity surrounding direction. We still feel that Bitcoin could act as a geopolitical and monetary hedge against runaway inflation, but ultimately the market will decide over the coming year.

Ethereum

- This week, Ethereum experienced choppy price action ahead of a significant options expiry on September 30th. ETH’s correlation to BTC took centre stage during Tuesday’s session. By midday, the asset had rallied more than 8% off the back of fresh buy-side pressure as shorts were forced to close. Similarly, the move was succeeded by a 10.45% retreat by Wednesday morning. Price instability continued through the week with two more 5% + swings. By the weekly close, ETH sat at 1,277 for a -1.37% decline WoW.

- Following its Merge, Ethereum’s behaviour now more closely follows that of high beta assets. Following heightened uncertainty in global markets, Ethereum was subject to increased volatility during this week’s session. Alongside the USD’s continued strength, a number of large indexes are now placed at key inflection points and it is our opinion that the only certainty, in the short term, is that the impending move will be explosive. As participants await a decisive leg trend to materialise, liquidity has dried up. Hence, in the short term, we may see some sharper moves as order books struggle to absorb larger tickets. Time will tell though.

ETHBTC Daily Chart

- ETH/BTC continues its decline this week after a confirmed breakdown from the channel trendline above 0.07. While most of the week was spent consolidating under the trend, by Saturday, the price began grinding lower before falling more aggressively into the weekly close at 0.067 for -2.67% WoW. Looking ahead, the pair now finds itself in a support zone that extends down to the 0.064 level. Failure to hold this region would possibly result in a more serious breakdown to the 0.056 level which also coincides with the start of Q3’s merge-driven rally. As the flight to safety narrative drives relative strength for BTC, the possibility of a full retracement of ETH’s outperformance remains on the cards.

- The number of Ethereum addresses in loss continued higher this week. Coinciding with Ethereum’s consolidation at the 1,300 level, the metric fell just short of an all-time high. Currently, slightly under half of the circulating supply sits at an unrealised loss. This can likely be attributed to participants buying into the pre-merge rally toward 2,000. While many of these holders may be targeting Ethereum’s expected medium to long-term supply constriction, should the broader market continue to deteriorate, the possibility of a major capitulation event grows.

- Coinciding with post-merge chain stability, market participants continue to redeploy funds. This behaviour is shown in the percentage of circulating supply in smart contracts that have continued their strong recovery this week. Notably, the ETH Beacon Chain staking contract saw its largest monthly inflow in three months.

- Subsequent to Ethereum’s Merge, the daily number of blocks produced has risen from an average of 6k to 7.1k, approximately 18%. This increase can be attributed to a pseudo-random function that selects a validator every 12 seconds. Prior to the Merge, block time was primarily based on mining difficulty. Though small, the more efficient production of blocks enhances the speed at which transactions can be executed and reach finality.

- Complaints have been levied against Ethereum around censorship at the base layer. Since the merge, 23% of blocks produced have complied with the US OFAC list. This is occurring due to the dominance of Flashbots’ MEV-Boost client and the company’s compliance with US regulations. MEV-Boost prevents the proposal of blocks that include transactions coming from the blacklisted wallets. In the last 24 hours, Flashbots’ MEV-Boost accounts for just under 50% of the blocks relayed. In this sense, the client that far outperforms other Ethereum validating clients is using economic incentives to censor transactions.

DeFi

- According to TechCrunch, Uniswap Labs, the parent company of the decentralised exchange Uniswap, is rumoured to be preparing for a $100 million to $200 million funding round. This positions the entity for a $1b valuation. The company is reportedly engaging with potential investors, including Polychain and a Singapore-based fund. Prior to the capital raise, Uniswap Labs expressed an interest to expand its product offerings to include an NFT aggregator. It is possible that raised capital will be allocated to such features and other forthcoming DeFi projects on Uniswap’s roadmap.

Innovation

- SWIFT and Chainlink are collaborating to build a Cross-Chain Interoperability Protocol (CCIP). The proof of concept will enable the interbank payment system’s messages to instruct on-chain token transfers. This will assist SWIFT in communicating across a variety of blockchain environments. Jonathan Ehrenfeld Solé, Strategy Director at SWIFT, explained that the interbank network’s motivation to work on CCIP derived from an “undeniable interest” in crypto from dominant institutions.

- The Commodity Futures Trading Commission (CFTC) is suing Ooki DAO for offering leveraged and margin trading products without registering as a Futures Commission Merchant. Prior to the initiation of the lawsuit, the CFTC charged the creators of Ooki DAO, bZeroX, with a $250k fine. Subsequently, bZeroX converted its services from a centralised platform to a service operated by a DAO. Notably, with the CFTC suing a DAO for this reason, the typical decentralisation defence is evidently not as comprehensive as believed. Moreover, the commission determined that any individual who voted within the DAO’s governance process is liable.

Altcoins

- Following USDT’s recent integrations with a number of blockchains, Circle has announced that it plans to expand USDC onto Polkadot, Cosmos, Arbitrum, Optimism and NEAR Protocol. This will provide users and developers on those chains with a stable and secure stablecoin that can be redeemed for $1, thereby increasing the adoption of the token. Furthermore, the expansion onto layer 0s will see USDC natively supported on all other blockchains existing on top of the network. Circle is also reportedly in discussions with Cosmos to leverage its interchain security for USDC.

- Marking its 4th major outage in 2022, the Solana network has stopped processing transactions, going offline for a total of 2 hours and 45 minutes. The halting of Solana’s product production arose as a result of a validator running a duplicate validator. This saw two blocks being produced for the same block by one validator, confusing other validators on the network. The error caused a partition in the Solana network, requiring the restart and update of 80% of nodes to resume the production of Solana blocks. These events freeze all network activity, placing borrowers on DeFi platforms in a precarious situation of losing their collateral once transactions start again.

- Amidst significant speculation, Cosmos has launched the whitepaper for the future of the Cosmos Hub – its own blockchain on the layer 0 network. The roadmap increases the importance of the Cosmos Hub by offering interchain security through its diverse set of validators. Other chains on Cosmos will be able to rent validators from the Cosmos Hub, paying with ATOM tokens. Additionally, the roadmap outlined a revamp of the tokenomics and emissions around ATOM. As well as the elevated focus on value accrual for ATOM, the issuance of the tokens will rise to 10 million per month before falling to a monthly rate of 300k.

- Responding to the burgeoning popularity of Cosmos, competitor Polkadot announced its updated roadmap. One key feature outlined includes Asynchronous backing, wherein parachains’ block time will halve from 12 seconds to 6 seconds, allowing for lower latency and faster finality. This change has the potential to increase Polkadot’s transactions per second to 100k – 1 million. Further, Polkadot will be offering nomination pools for staking, allowing for the permissionless creation of staking pools by participants. The roadmap also introduced fraud proofs through dispute slashing, a new governance model and an improved cross-chain messaging mechanism.

NFTs & Metaverse

- The United Arab Emirates (UAE) has announced that the Ministry of Economy’s new headquarters has opened on the metaverse as part of Dubai’s Metaverse Strategy. The virtual headquarters will feature multiple stories, each with a different purpose relating to the ministry. To support the adoption and usage of these headquarters, the UAE has altered regulations so that visitors will be able to virtually sign legal documents. Accordingly, individuals within the UAE will no longer need to visit the Ministry of Economy’s physical headquarters in Dubai or Abu Dhabi to provide their signature on documents.

- Apple has enabled NFT purchases under its ‘In-App Purchases’ model. However, the entity is charging its standard 30% commission fee. Unlike other applications on the App Store, NFT marketplace apps do not rely on Apple to facilitate purchases or sales, but rather make use of the blockchain. These fees significantly overshadow those of NFT marketplaces on websites; OpenSea takes a 2.5% fee and Magic Eden a 2% fee. These inflated costs arguably pave the way for blockchain-based phones currently being developed, such as Solana’s Saga phone.

- Christie’s has launched its own Ethereum-based NFT marketplace to host an auction house for exclusive, high-quality NFTs. The marketplace has been created in collaboration with Manifold, ChainAlysis and Spatial. This offering, named Christie’s 3.0, will enable the company to offer on-chain purchases and sales of NFT items in a direct fashion. This differs from Christie’s past approach to auctioning off NFTs. In 2021, Christie’s sold Beeple’s “Everydays – The First 5000 Days” for over $69 million. Notably, however, the auction and purchase itself were conducted off-chain.

What to Watch

- OPEC bi-annual meeting on Wednesday – organisation considering crude oil output cut.

- Developments in Russia x Ukraine conflict following territory annexation and Zelensky’s official NATO membership application.

- US unemployment rate, on Friday – despite being in a technical recession, the US has used solid employment data as an argument against recession.

- Developments in Russia x Ukraine conflict following territory annexation and Zelenskyy’s official NATO membership application.

Insights & Events

- Join Zerocap CEO Ryan McCall at Bloomberg LP’s upcoming event “Innovation & Regulation: The Next Frontier for Crypto in Australia,” this Wednesday.

- Regenerative Finance (Part 3) – Social Incentives and the Endgame: In the final part of our Regenerative Finance coverage, Innovation Analyst Nathan Lenga covers how ReFi can potentially boost social incentives with NFTs as “impact certificates,” current applications developments and the endgame of this disruptive financial framework.

In his latest Ausbiz interview, Zerocap CIO Jonathan de Wet discusses current fluctuation across markets, Grayscale Investments’s trust, Cosmos’ app-building framework and more.

Disclaimer

This material is issued by Zerocap Pty Ltd (Zerocap), a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799.

Material covering regulated financial products is issued to you on the basis that you qualify as a “Wholesale Investor” for the purposes of Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client), or your local equivalent.

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice,take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

FAQs

What were the key developments in the crypto market during the week of 3rd October 2022?

The week saw significant developments in the crypto market, including FED Chair Jerome Powell’s statement on the need for appropriate regulation for DeFi, CFTC Chair Rostin Behnam’s prediction of Bitcoin’s price doubling if there’s a CFTC-regulated market, and Australia’s plans to start testing its digital dollar in mid-2023. Other notable events included Meta’s introduction of NFT cross-posting and sharing on Instagram, and Ripple scoring another win against the US SEC.

What was the impact of the UK’s tax cuts on the crypto market in the week of 3rd October 2022?

The UK’s tax cuts, which saw a 5% tax slashed from the UK’s highest-paid workers, led to speculation that the tax cuts would be funded by future out-rated welfare payments. This forced the Bank of England to initiate a £65 billion bond buyback scheme to prevent mass insolvency in the pension fund sector and large holders of long-term gilts. This had a significant impact on the crypto market, particularly on Bitcoin, which saw increased trading volumes.

What were the technical trends observed in Bitcoin and Ethereum during the week of 3rd October 2022?

Bitcoin saw substantial selling volumes pushing the price below the 18,750 support before being firmly bid at 18,460. Ethereum experienced choppy price action ahead of a significant options expiry on September 30th. ETH’s correlation to BTC took centre stage during Tuesday’s session, with an 8% rally followed by a 10.45% retreat by Wednesday morning.

What were the major innovations in the crypto market during the week of 3rd October 2022?

Major innovations included SWIFT and Chainlink collaborating to build a Cross-Chain Interoperability Protocol (CCIP), Uniswap Labs preparing for a $100 million to $200 million funding round, and the Commodity Futures Trading Commission (CFTC) suing Ooki DAO for offering leveraged and margin trading products without registering as a Futures Commission Merchant.

What were the key developments in the NFT and Metaverse space during the week of 3rd October 2022?

Key developments included the United Arab Emirates (UAE) announcing that the Ministry of Economy’s new headquarters has opened on the metaverse, Apple enabling NFT purchases under its ‘In-App Purchases’ model, and Christie’s launching its own Ethereum-based NFT marketplace to host an auction house for exclusive, high-quality NFTs.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 2 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Zerocap Launches Institutional OTC Desk for Tokenized Gold Trading

Zerocap’s institutional OTC desk enables investors to access tokenized gold efficiently, supporting portfolio diversification and inflation hedging strategies. The core objective is to provide seamless

Weekly Crypto Market Wrap: 23 February 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.