Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What are the key events that impacted the crypto market in the week of 29th November 2021?

- How did the new Omicron variant affect the crypto and stock markets?

- What were the winners and losers in the crypto market during this period?

- What are the technical insights and indicators for Bitcoin and Ethereum?

- What are the notable developments in DeFi and innovation, and what should investors watch for

- Disclaimer

29 Nov, 21

Weekly Crypto Market Wrap, 29th November 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What are the key events that impacted the crypto market in the week of 29th November 2021?

- How did the new Omicron variant affect the crypto and stock markets?

- What were the winners and losers in the crypto market during this period?

- What are the technical insights and indicators for Bitcoin and Ethereum?

- What are the notable developments in DeFi and innovation, and what should investors watch for

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- Prices on risky assets plummet under concerns of the new Covid-19 variant Omicron – US imposes travel ban on eight African countries while Moderna announces new vaccine on the way.

- Eurozone inflation approaches record-highs – Pew Research Center puts US’ annual inflation rate as eighth highest in the world.

- Jerome Powell confirmed for the nomination as Fed Chair for another four years.

- US’ PCE Price Index soars 5% year on year in October, preliminary GDP underwhelms.

- US’ SEC announces panel next Thursday to discuss cryptocurrencies, congress asks question on Tether.

- India announces bill set to ban most cryptocurrencies, paving the way for the country’s own CBDC.

- Long-term crypto holders are at a multi-year high, Glassnode reports.

- ASIC chair Longo states the rise of crypto “has been nothing short of phenomenal.”

- Australia’s ATO states it can’t rely on users’ own crypto records; it works on ways to “nudge” them.

- Australia’s Rest superannuation fund to invest in cryptocurrency assets for its 1.8 million members.

- Morgan Stanley increases exposure to bitcoin, totalling $300M in Grayscale shares.

- Citigroup set to hire 100 people for digital assets division; appoints first Head of department.

- El Salvador’s dollar debt plummets under bitcoin bond plans.

- Sportswear firm Adidas announces partnership with Coinbase.

Winners & Losers

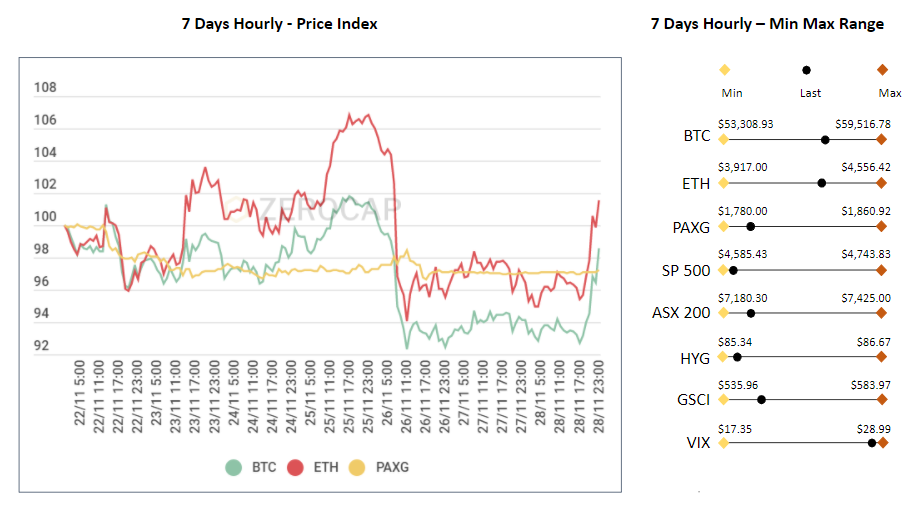

- The week began with BTC filling out its existing range, building newfound support above $56k. During this period a number of altcoins rebounded with conviction in the broader market. COVID concerns surrounding the new Omicron variant subsequently led to a significant market sell-off on Friday, led front and centre by UK equity markets. The UK100 had its largest single-day drop since June 2020 – 3.64%. It was definitely a case of sell now, ask questions later. While many alts faced further 10%+ drops, BTC found support above 53k with many taking this opportunity to purchase the asset at a 22%+ discount from the highs set earlier this month. The marketwide sentiment still remains in extreme fear as concerns of a May 2021 repeat sit fresh in the minds of investors, although a number of indicators point to a local bottom being set should COVID concerns not intensify. Overall, BTC returned -2.28% and ETH returned 0.86% WoW.

- Stocks began the week on a positive note, as S&P 500 elevated above 4,700 and set for a Santa Claus rally into the Christmas period. However, with news of the new South African valiant strain hitting newswires around the globe, momentum began to reverse. The US benchmark lost 2.3% on Friday, while the Russell 2000 small-cap lost more than 4%. Travel, leisure and oil-related stocks hit the hardest with oil prices sinking.

- The VIX index and futures contracts jumped 40% following the media storm from Friday’s new COVID-19 mutation. The fact that we were moving from a week of record levels on the S&P 500 further intensified the velocity of the move. There was a slight hint of stabilisation on Sunday evening US time when US director of the National Institute of Allergy and Infectious Diseases, Dr Fauci, announced that he had told President Biden he thinks current vaccines give some Omicron mutated strain protection.

- Nickel & copper paced a base-metals selloff in London amid an uncertain demand outlook for the metal space. Gold prices had begun the week on a strong note above $1,865 but quickly retracted lower with a stronger DXY. The USD index maintained momentum throughout the week, helping to push USDJPY above 115.50 and AUD to the edge of 71 cents. High yield currencies took a backseat into the weekend on risk as fund flows concentrated on seeking haven shelter amid growing Covid panic. Oil prices dropped by 10% in a single day as the global partnership to employ strategic oil reserves to lower gas prices were reinforced by the fear of renewed border closures over the Christmas holiday travel peak season.

- Macroeconomic data was generally positive following a higher than expected US GDP growth report and a lower than expected initial claims count. There wasn’t much reporting due to the US Thanksgiving holidays, and economists were generally quiet given Covid strain reporting. In fact, several global institutions had upgraded their forecast for a faster tapering timeline by the US central bank during the week in anticipation of a stronger economic recovery and inflationary pressures.

- Geopolitical concerns also weighed on risk sentiment with Taiwan’s air force scrambling to warn off 27 Chinese aircraft entering their airspace. The rise in war game initiatives intensified over the weekend as China’s president met his top generals with speculation for further pressure on the island nation.

- The developed economy govie market saw some of the highest levels of volatility during the week. Stronger growth data and higher than expected consumer inflation forecast had pushed ten year UST yield towards a recent high of 1.65% before Friday’s retracement. The fear of another mutation causing border closures and hard lockdowns transferring into safe-haven assets rallying in place of stocks, credit and cryptocurrencies alike. Sub Investment grade market retracing hard, in line with a regional and global stock selloff. The top ten crypto market cap assets have been losing between 10% to 15 % since Friday. Asian stock futures maintained the bearish momentum into the weekend, leading to speculation that Monday’s opening will see further profit-taking as we move into the final month of the year. Although at the time of writing, we are seeing a rally from risk assets and equity market futures on the back of diminishing concerns.

Macro, Technicals & Order Flow

Bitcoin

- BTC saw the initial Covid drop, down to prior support under 55,000. The asset is now trading back into the range, with 60,000 in sight. Technically, the next notable level would be 62,500, the prior breaking point of the down-move from mid-November.

- Despite the week being mired with volatility around the unknown effects of the Covid-19 variant, Omicron, participants are clearly buying up risk as we write this on the back of moderation in concerns. Ultimately the short-term moves will be bound by what’s known and unknown – any unknowns, particularly around vaccine efficacy against this virus, could cause short-term liquidity issues. The real kicker will be whether the market plays to the same tune as March 2020, when risk was dumped, and later bought on the back of Central Bank stimulus expectations. We are in a different place this time – inflation is kicking, and we have extended bubbles in asset prices. Further lockdowns may not have the same market response, particularly now in December prior to year-end.

Longs vs Short Totals (Datamish)

- Indicators for BTC are still very bullish – on-chain indicators are showing supply squeezes on exchanges, funding rates are contained (after the expected liquidations linked to the Covid concerns), and newsflow has been positive for the week – with the institutional case for BTC further backed by Morgan Stanley’s increasing purchases of the Grayscale Bitcoin Trust (GBTC).

Bitcoin Net Position Change

BTC Perpetual Swaps Funding

BTC Perpetual Liquidations 1W

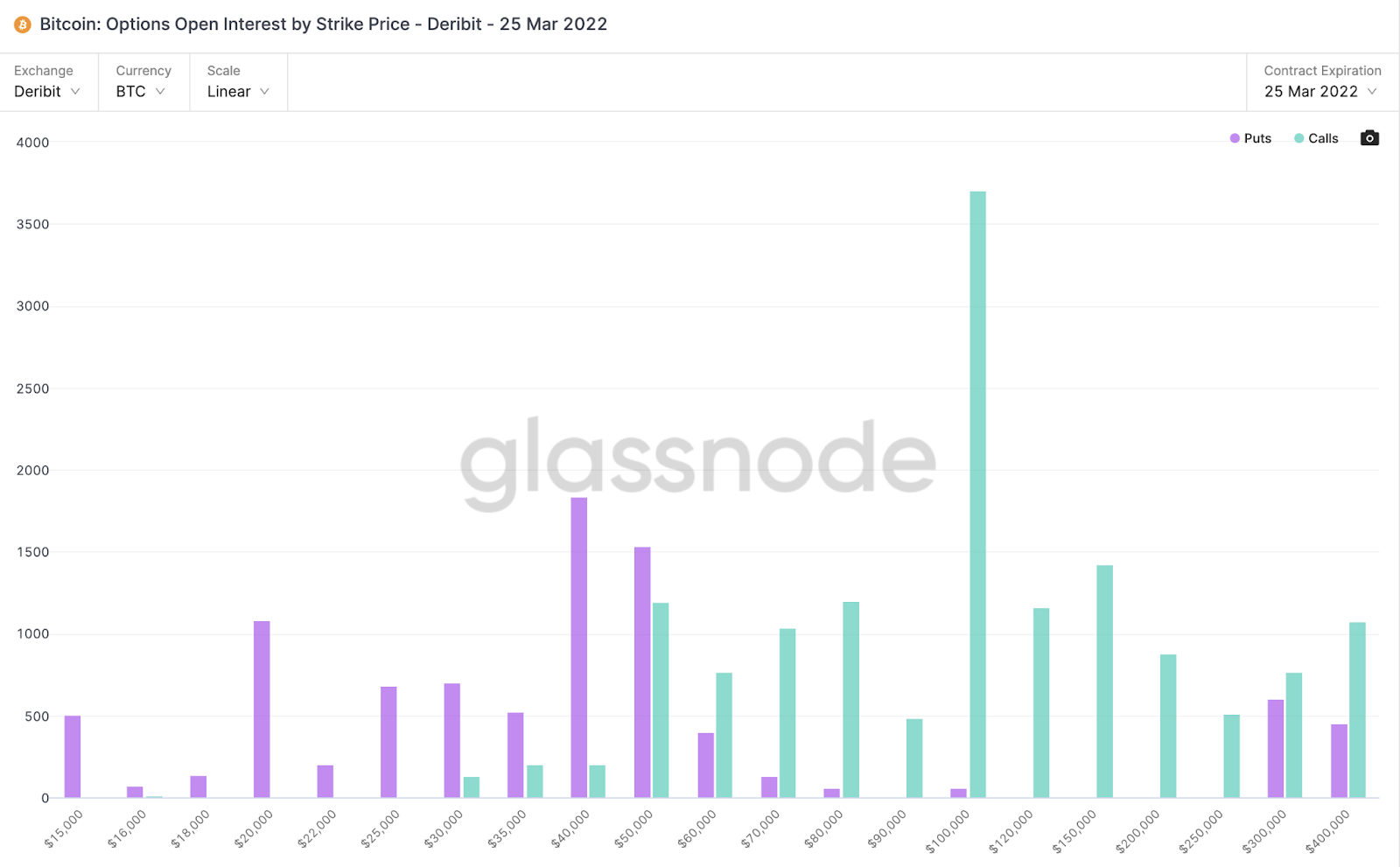

- Option strikes out to Dec 31 are clearly weighted to calls at 80,000 / 100,000 and 120,000. Out to Mar 25, 2022, we are still seeing interest weighted to 100,000 as the key level.

OI Interest by Strike – Dec 31, 2021

OI Interest by Strike – Mar 25, 2022

- The Futures Basis curve is beginning to rally on moderation of risk, a healthy sign coming into Europe’s session.

BTC Futures Annualised Rolling 1 Mth Basis

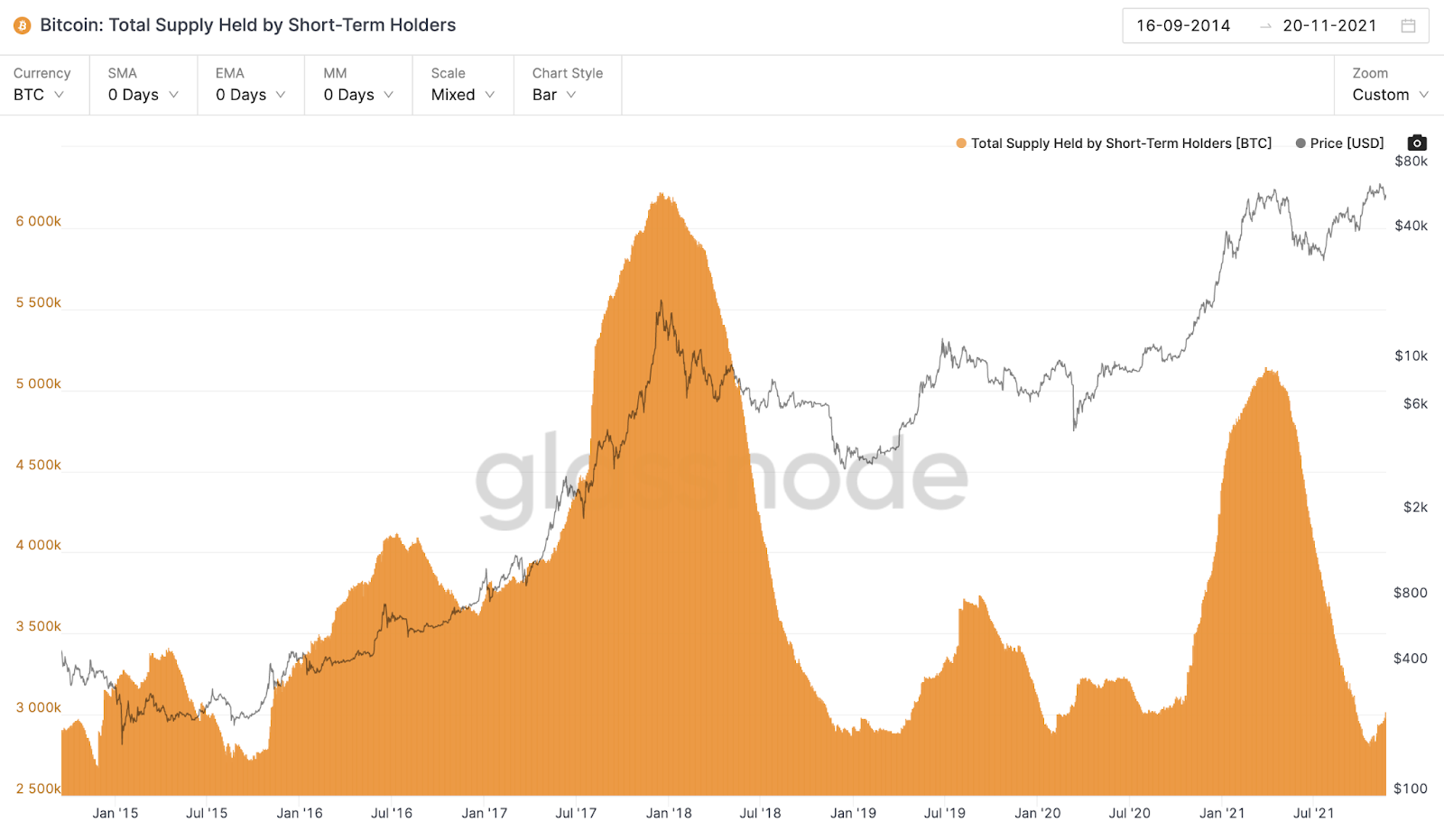

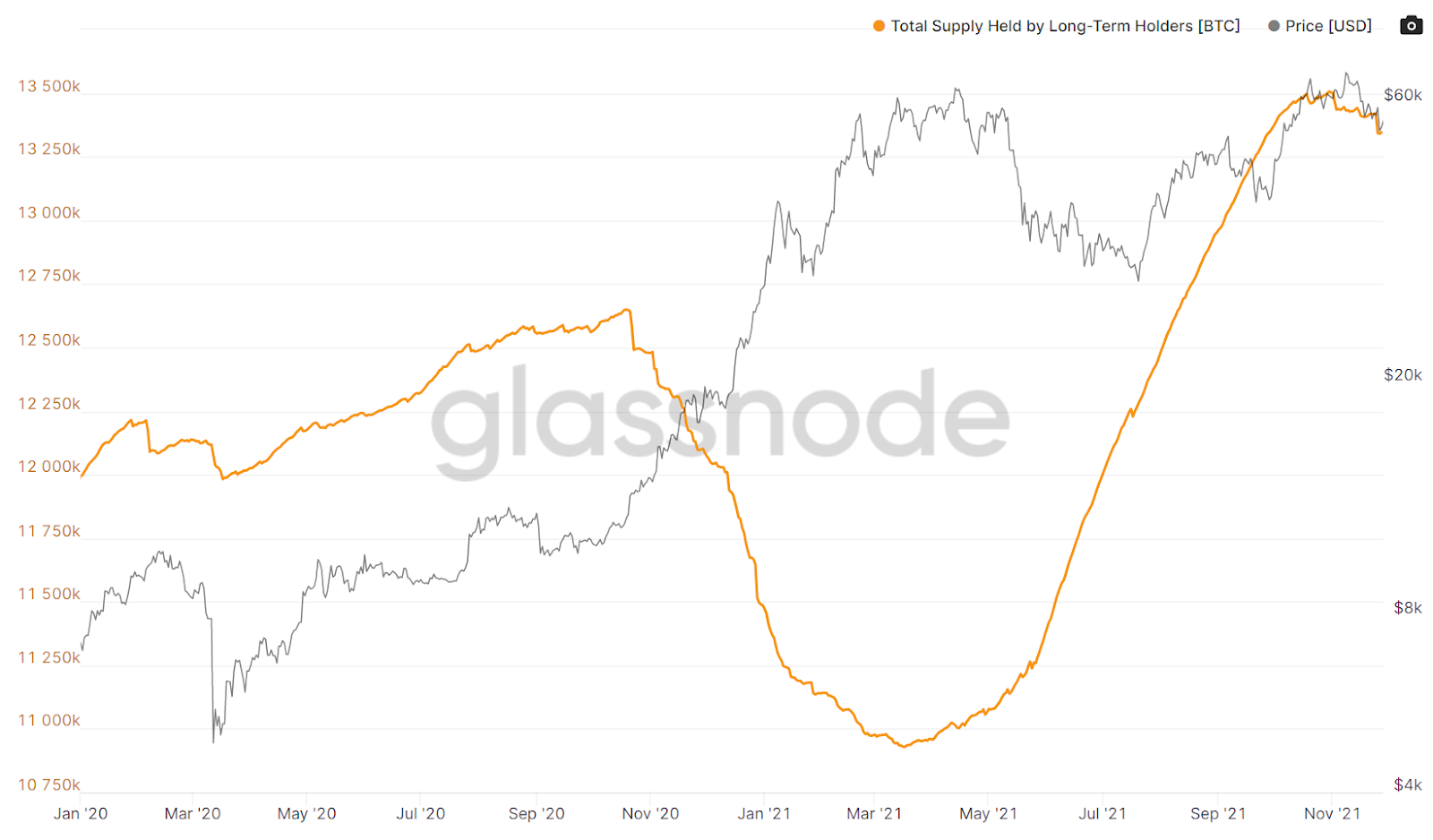

- The final note for this week is around short-term holder supply – we are at extremely low levels of short-term holder supply, and conversely long-term holder supply has been at highs. This is beginning to rotate which is typically a sign of a bullish market, given that the longer-term players sell into strength, and buy into weakness. The issue that could cause issues with this dynamic playing out is unexpected Covid shocks hitting markets with this new strain.

BTC Total Supply Held by Short-Term Holders

Bitcoin: Total Supply Held by Long-Term Holders

Bitcoin: Total Supply Held by Long-Term Holders

Ethereum

- Ethereum is technically trading very well – trading the Covid down-move and bouncing off prior highs from September. As we write, the asset is clearly buying risk alongside a sea if green in equity market futures.

- Despite the persisting issue of ETH’s high gas fees, and the resulting inflows to other major altcoins, bullish pressure has persisted. On supply, it’s interesting to note that since the launch of the EIP-1559, over 1 million ETH ($4billion+) has been burned. This all adds to topside pressure, particularly when institutions are circling.

- This said, layer 1’s are definitely gaining traction; Avalanche is doing 55% of the number of ETH transactions after just 14 months for example. The risk environment, short-term on Covid Omicron, and longer-term on inflationary pressures, will ultimately be the line in the sand between the bulls and bears in the altcoin market.

- ETH open interest to Dec 31, still very weighted to 5,000, buoying sentiment.

ETH Open Interest by Strike: Dec 31, 2021

- ETHBTC naturally took a spill on risk, and is now rallying against bid equity futures coming into the European open. The risk on/risk off divergence in these assets continues to grow in comparison to each other – despite correlating on immediate newsflow shocks.

ETHBTC Daily Chart

- Like BTC, outflows from exchanges are still clearly in the supply crunch zone.

Ethereum Exchange Net Position Change

- Perpetual funding rates seeing notable spikes in both directions as the market has been trying to determine direction on the back of virus concerns. This is indicative of some fairly aggressive short-term players looking to capture momentum.

ETH Perpetual Swaps Funding

- The futures basis curve is rallying out of the slump towards 10% annualised.

ETH Futures Annualised Rolling 1 Mth Basis

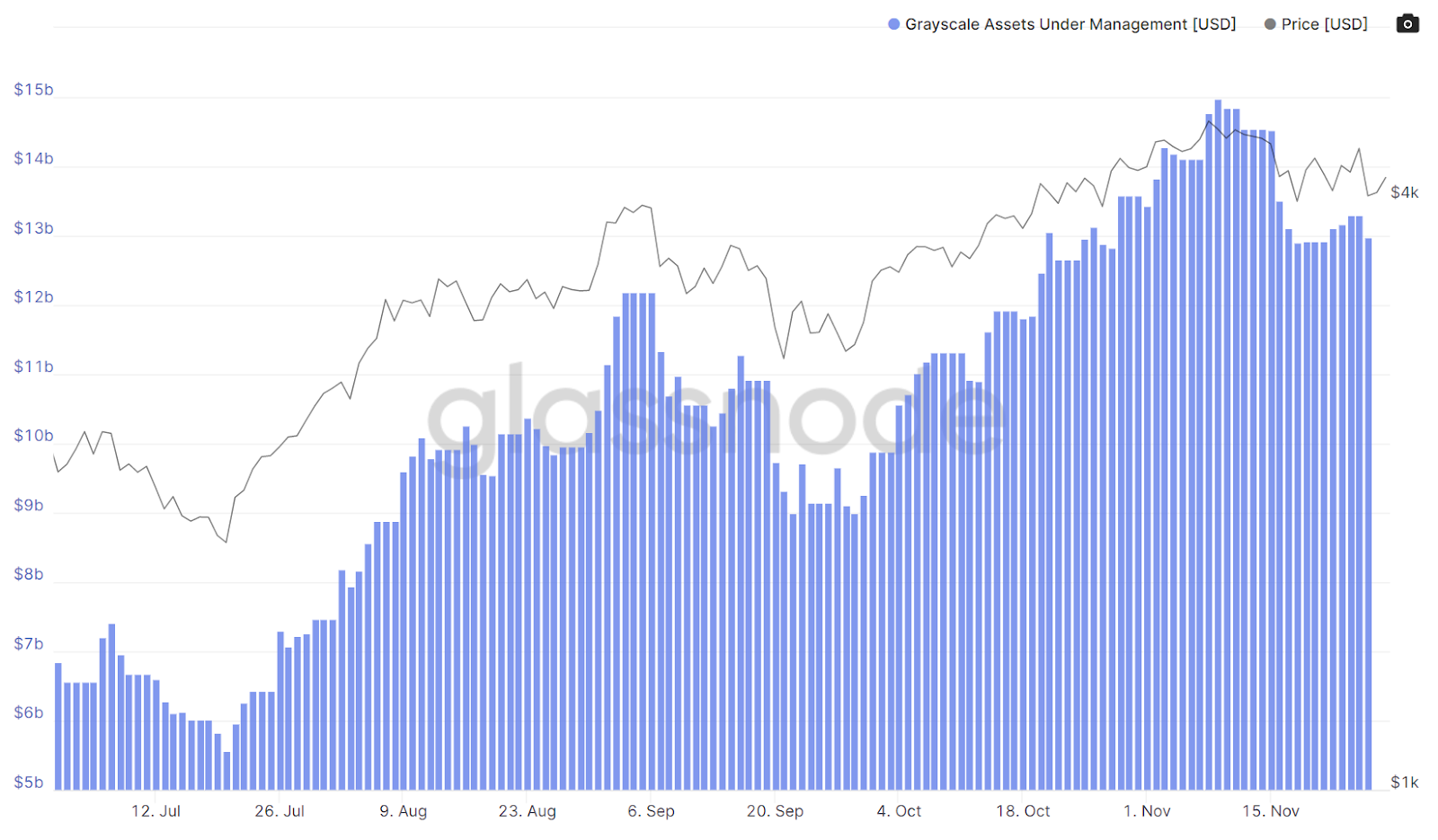

- Grayscale AUM has held throughout this week, showing the hands of institutions – not willing to liquidate on risk.. yet.

Ethereum Grayscale AUM

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,407,541. This represents 7.09% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- In summary, nice bounce in risk – but we need to get closer to the full picture on this variant and the market’s take on this before calling the next move.

DeFi & Innovation

- Total value locked on Layer 2 Ethereum networks reaches all-time high, doubling over the last couple of months.

- Ethereum co-founder Vitalik Buterin proposes network update to reduce fees.

- Collins Dictionary crowns “NFT” as the word of the year.

- Solana Foundation report claims each Solana transaction spends less energy than two Google searches.

- BOE governor says CBDCs are the revolution of money during a streamed committee.

What to Watch

- Further research on the new Covid-19 variant and market reactions.

- Fed Chair Powell’s testimony on the CARES act tomorrow and Wednesday (Coronavirus Aid, Relief, and Economic Security Act).

- US SEC’s cryptocurrency panel on Thursday.

- Australia’s quarterly GDP report.

- Developments in India regarding the crypto ban bill.

FAQs

What are the key events that impacted the crypto market in the week of 29th November 2021?

The article highlights several key events, including concerns about the new Covid-19 variant Omicron, Eurozone inflation approaching record highs, Jerome Powell’s confirmation as Fed Chair, India’s announcement of a bill to ban most cryptocurrencies, and significant investments and partnerships in the crypto space.

How did the new Omicron variant affect the crypto and stock markets?

The discovery of the Omicron variant led to a significant market sell-off, with many assets facing drops. Bitcoin found support above 53k, and the market sentiment remained in extreme fear. The stock market also saw losses, with travel, leisure, and oil-related stocks hit the hardest.

What were the winners and losers in the crypto market during this period?

The week began with Bitcoin building support above $56k, but COVID concerns led to a significant sell-off. While many altcoins faced further drops, Bitcoin found support, and the overall sentiment remained fearful. BTC returned -2.28%, and ETH returned 0.86% week over week.

What are the technical insights and indicators for Bitcoin and Ethereum?

For Bitcoin, indicators are still very bullish, with on-chain indicators showing supply squeezes, and option strikes weighted to calls at higher levels. Ethereum is trading well, bouncing off prior highs, and bullish pressure has persisted despite high gas fees. Both assets are showing signs of recovery and bullish momentum.

What are the notable developments in DeFi and innovation, and what should investors watch for

Developments include the total value locked on Layer 2 Ethereum networks reaching an all-time high, Ethereum co-founder Vitalik Buterin proposing a network update to reduce fees, and the crowning of “NFT” as the word of the year. Investors should watch for further research on the new Covid-19 variant, Fed Chair Powell’s testimony, the US SEC’s cryptocurrency panel, and developments in India regarding the crypto ban bill.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 22 Nov. 2021 0:00 UTC to 28 Nov. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Zerocap Participates in RBA Project Acacia

Zerocap is proud to have participated in Project Acacia, a landmark pilot led by the Reserve Bank of Australia (RBA) in collaboration with the Digital

Weekly Crypto Market Wrap: 18 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 11 May 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.