Content

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi

- Innovation

- Altcoins

- NFTs & Metaverse

- What to Watch

- Insights

- Disclaimer

- FAQs

- What significant changes occurred in the crypto market during the week of 26th September 2022?

- How did Bitcoin and Ethereum perform during the week of 26th September 2022?

- What were the major developments in the DeFi and Altcoin sectors during the week of 26th September 2022?

- What innovations were introduced in the crypto market during the week of 26th September 2022?

- What were the key events to watch in the crypto market following the week of 26th September 2022?

26 Sep, 22

Weekly Crypto Market Wrap, 26th September 2022

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi

- Innovation

- Altcoins

- NFTs & Metaverse

- What to Watch

- Insights

- Disclaimer

- FAQs

- What significant changes occurred in the crypto market during the week of 26th September 2022?

- How did Bitcoin and Ethereum perform during the week of 26th September 2022?

- What were the major developments in the DeFi and Altcoin sectors during the week of 26th September 2022?

- What innovations were introduced in the crypto market during the week of 26th September 2022?

- What were the key events to watch in the crypto market following the week of 26th September 2022?

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

Week in Review

- Pentagon launches effort to assess crypto assets as potential threats to national security.

- UK introduces law empowering the government to “seize, freeze and recover crypto” – Financial Conduct Authority (FCA) lists FTX crypto exchange as “unauthorised.”

- US Treasury asks for public opinion on crypto regulations, deadline for 3rd November.

- US House of Reps’ stablecoin bill seeks two-year ban on algorithmic stablecoins.

- South Korea asks Interpol to issue “Red Notice” for Terra (LUNA) co-founder Do Kwon, who says he’s not “on the run” despite unknown whereabouts following arrest warrant.

- Despite crypto ban, China accounts for 84% of global blockchain patent applications.

- California Governor Newsom vetoes crypto framework bill, calls for “flexible approach.”

- The US state of Colorado now accepting tax payments in crypto, as promised by governor.

- Australian Senator Andrew Bragg drafts bill for stablecoins and China’s digital yuan.

- New York judge orders Tether to document USDT backing.

- Putin threatens West with nuclear war, mobilises 300 thousand reservists to Ukraine.

- FED delivers another 75 bps rate hike – forecasts total hikes peak as high as 4.4% by end of the year, 4.6% in 2023.

- Bank of England says the UK is already in a recession, raises rates by 50 bps.

Winners & Losers

Macro Environment

- Markets struggled to find direction at week’s open however were quick to whipsaw, likely following the United States (US) Federal Reserve’s (FED) 75 basis point rate hike on Wednesday. The Benchmark FED funds rate now sits at 3 – 3.25%, the highest markets have seen since the global financial crisis, FED Chairman Jerome Powell further, signalling another 100 to 125bps to come over the next two FOMC meetings. Analysts are now estimating a terminal policy rate of 4.4% for 2022, peaking in May 2023 at 4.6%. Both 2Y and 10Y Treasury Bond Yields surged post FOMC meeting, the benchmark yield for 10YUST lifted to 3.829% on Friday – the highest since 2011, 2YUST saw a weekly high of 4.268%, nearing 2007’s record yields. The closely monitored 2Y and 10Y year yield curve inversion closed the week at a pessimistic -52bps.

- The United Kingdom is in strife, with the Bank of England (BOE) hiking interest rates 50bps on Thursday in conjunction with UK Prime Minister Liz Truss’ fiscal stimulus package which is the country’s largest tax cut since 1972. In response, the GBP/USD dropped to a 37-year low of $1.1042, with market participants growing wary of an intra-meeting rate hike to prevent the GBP from breaching parity with the USD. German Producer Price Index (PPI) numbers came out with a surprise increase of 7.9% in August, up 45.8% a year earlier, German PPI now sits at the highest it’s ever been at 168.60. This result will likely pressure the European Central Bank (ECB) to continue raising rates.

- Thursdays’ “Yentervention” answered macroeconomists’ growing uncertainties over the falling Yen (JPY). The Bank of Japan, having maintained its ultra-dovish monetary stance on Thursday, resulted in the Yen falling to almost ¥146. This movement prompted the Japanese government to initiate a USD buyback of Yen – the first government intervention since 1998. The Yen recovered more than 2% against the dollar on the day reaching 140.34.

- Market spontaneity, fueled by differing global monetary policy outlooks, and worsening geopolitical tensions saw Chicago Wheat futures gain the most in 6 months on Tuesday, with corn also trending upwards. China was caught ramping up its soybean exports from Argentina: the US announcing an export sale of 136k tonnes of the crop to China. These gains were short-lived, however, following an end-of-week selloff in commodities – markets digesting recent central bank rate hikes, and geopolitical implications.

- Vladimir Putin’s alarming announcement of Russia’s partial mobilisation of troops to “liberate” east Ukraine’s Donbas region, saw Nickel and Wheat prices soar mid-week. The announcement raised concerns over local exports, seeing the Dow Jones Commodity Index: Nickel (DJCIIK) climb to a weekly high of 585, Gold (a haven asset) also jumping as high as $1,688.05 post announcement. Natural gas prices in Europe fell for a 4th consecutive week, with ample inflows of liquified natural gas filling countries’ reserves prior to the upcoming winter. Oil performed poorly, cementing a consecutive 4-week decline. WTI was down -4.611% week on week, dropping as low as $77.971 per barrel on Friday – the lowest since January, Brent also dropped to a weekly low of $84.608.

Technicals & Order Flow

Bitcoin

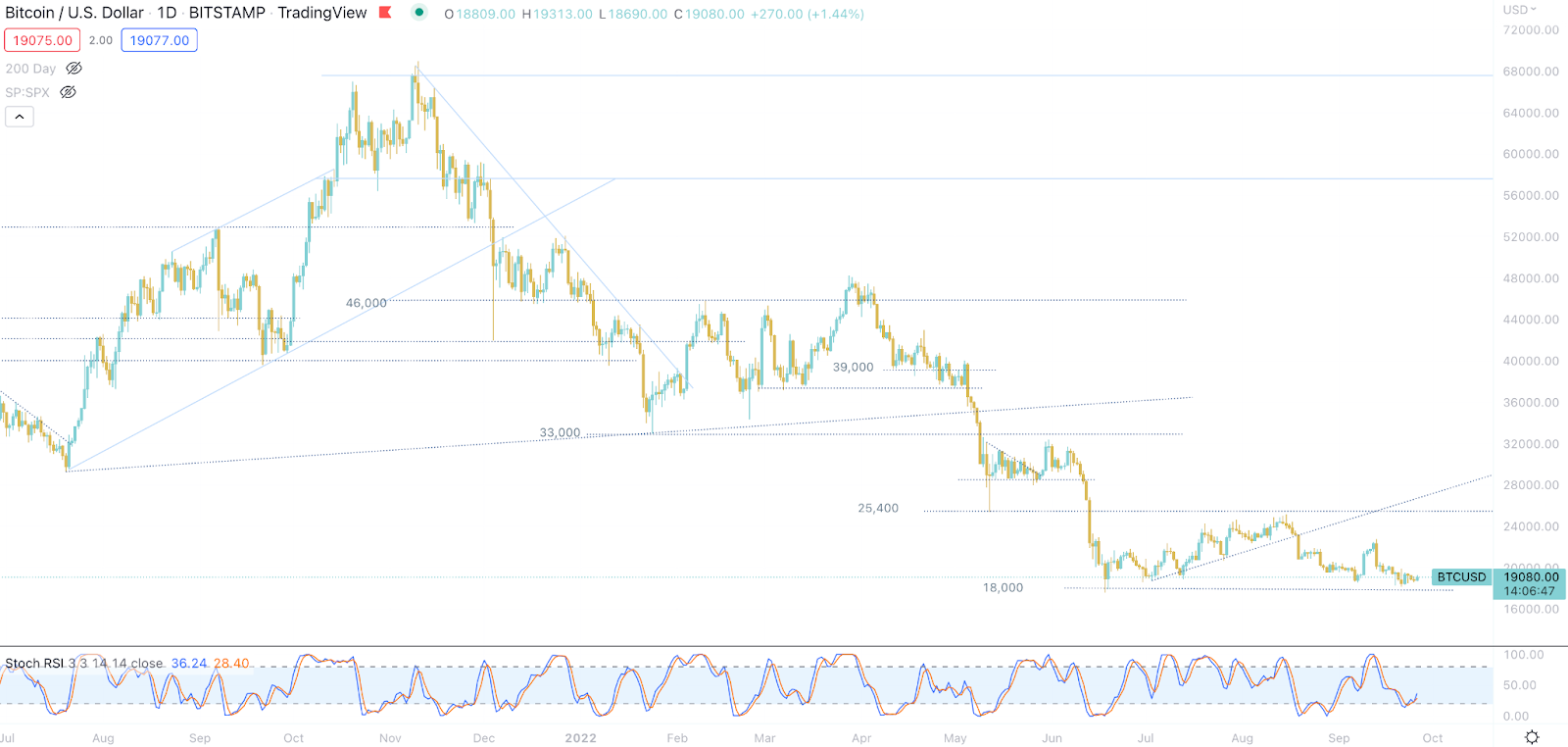

- This week, Bitcoin’s action centred around the 19,000 level. In the presence of early and mid-week selling, the 18,450 level was firmly held, potentially furthering its relevance as short-term support. Moves higher were hindered and the 19,650 level, the top of the 2017 bull run, acted as topside resistance. Moving forward we believe we will possibly see a consolidation between the 18,450 and 19,650 levels with possible breakouts to either side affirming short-term directionality.

- The prior week’s hotter-than-expected U.S. inflation data spun up fears of the Fed over-tightening during their approaching rate hike. The seesawing sentiment translated into early week price action in equities and digital assets, with Bitcoin exhibiting heightened volatility.

- Despite the Fed’s rate hike meeting the expected 75bp, BTC tumbled 6.87% in the following hours. Sentiment remained negative into the weekend’s session as other central banks such as the BOE raised rates to fight looming inflation. WoW BTC returned -3.13%.

- Looking at Bitcoin’s options’ open interest out to the 30 Sep expiry, 18,000 for puts is shaping up to potentially be a significant strike. The growth in open interest at this strike is historically indicative of traders hedging downside exposure in the face of increased macro uncertainty. Notably, the 24,000 and 25,000 strikes for calls are of particular interest and, in our view, are likely to expire worthless for buyers. Volatility selling has been a fantastic way to capture ranges and high yield premiums over the past 6-months.

- Notably, Bitcoin’s net exchange outflows have persisted at historically significant levels since late June 2022. Previously, this has been indicative of participants accumulating. More recently, the availability of Bitcoin on exchanges has been increasing. This coincides with Ethereum’s merge, last week’s CPI printout of the US and this week’s rate hike from the Fed. The increasing inflows of BTC to exchanges, paired with the current heightened risk environment, historically indicates caution and preparation for potential selling from market participants.

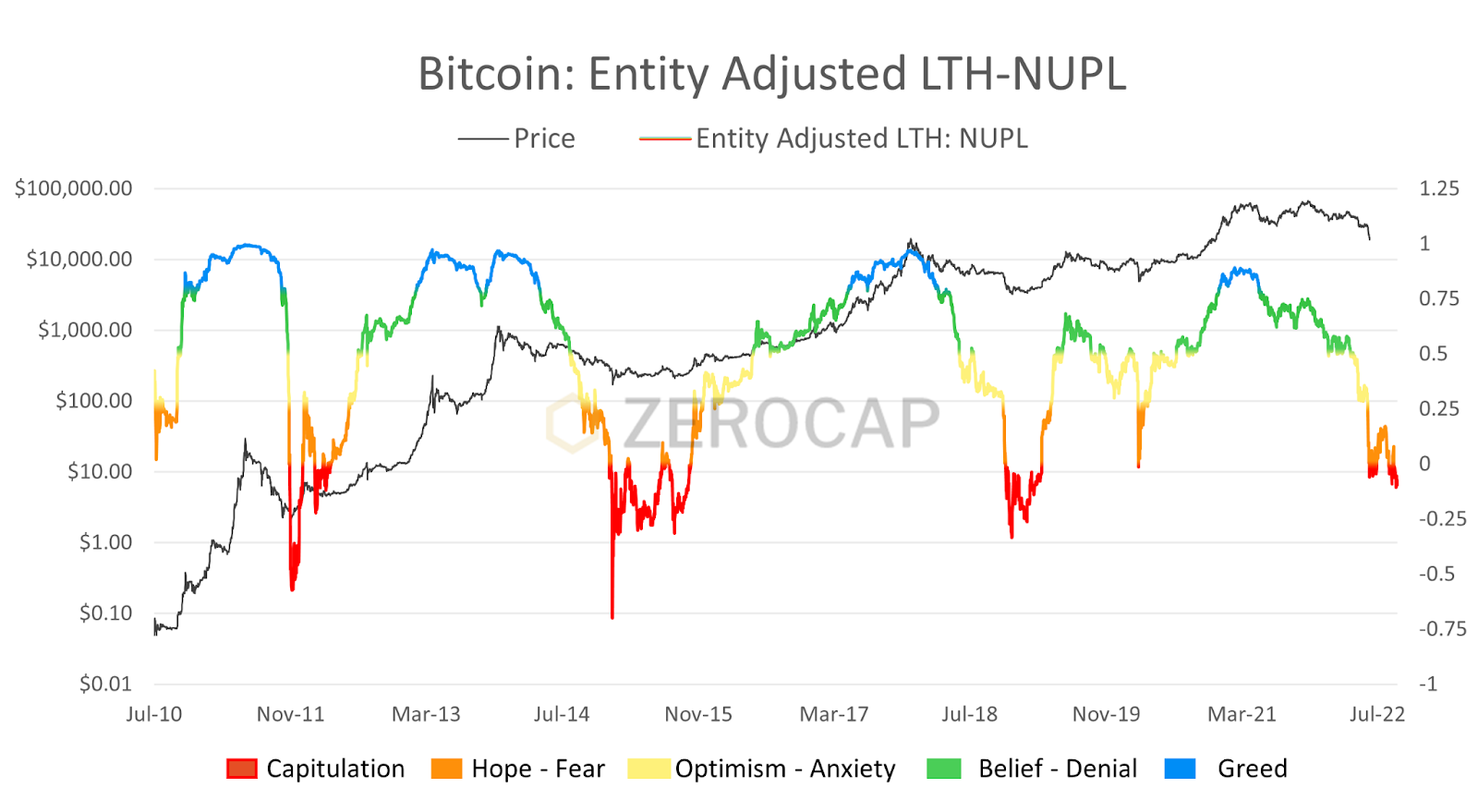

- Net unrealised profit and loss (NUPL) is a useful metric in analysing market cycles, and where the possible pain points are (turning points) of on-chain profitability. Long-term holder NUPL provides clarity surrounding the profitability of firmer hands. Currently, this metric resides at levels last seen at the start of 2019 and suggests the long-term attractiveness of current prices. The question is, how much more pain do we see in the market before investors reset positions for the next run?

- The negative effects of last week’s inflation data out of the U.S. flowed into sentiment this week. Heightened fears were the cause of ambiguity and indecisiveness amongst participants as the mid-week rate hike out of the U.S. approached. On-chain data suggests that participants are preparing for continued bearish action. Some options traders are taking into consideration a lack of support down to the 11,000 – 14,000 range with emphasis placed on the 18,000 strikes for puts. It is our view that short-term action is likely to be affected by further macro developments.

Ethereum

- Having lost the 1,420 support level during the weekend, Ethereum entered the week amidst a strong leg down. Following seller exhaustion, the price retraced from the Monday low of 1,280 to a high of 1,395 by the evening. Ahead of Wednesday’s FOMC meeting and as traders looked for confirmation in regard to direction, the price chopped around the 1,350 level.

- Following the 75bps printout of the Fed, volatility increased and caused liquidations on both sides of the book before a sell-off followed through to the weekly low of 1,220. Subsequently, the price found some relief alongside an increase in long open interest. By week close price had rolled over once again, suggesting an underlying weakness in the market. ETH closed out the week at 1,295 and returned -3.01% WoW.

ETHBTC Daily Chart

- Ahead of Wednesday’s FOMC, ETH/BTC showed strength and jumped more than 4% by Tuesday afternoon. However, following the broader market sell-off, ETH/BTC tumbled to its previous support zone around 0.067. WoW, the pair returned 0.16%. Following Ethereum’s merge, its bullish trend has somewhat diminished. This paired with the current macro uncertainty may see the pair break below 0.06 if the 0.065 – 0.067 region is lost. The next few weeks may be important if the price consolidates around this level.

- Following Ethereum’s merge, there was a notable uptick in user contract calls. Historically, such behaviour has indicated growth in activity on the Ethereum network that is beyond simple token transfers. Fears of network instability possibly motivated participants to sideline holdings prior to the event’s success. Upon confirmation of a successful merge, alongside a void of any technical issues in the days that followed, activity spiked. Interestingly, over the course of the week heightened volumes persisted particularly in the DeFi and NFT sectors.

- While ETH has not become a deflationary token since the merge, its merge to a proof of stake consensus mechanism has significantly reduced token issuance. As opposed to its previous 3.81% p.a. inflation rate, ETH’s supply is now expanding at a rate of 0.22% p.a. Having increased by approximately 8,100 ETH since the merge, the total ETH in circulation is slightly in excess of 120.5 million. In the absence of the merge’s impact on Ethereum’s supply dynamics, Ethereum’s supply would currently be approximately 120.7 million. This difference is expected to have notable long-term implications for supply availability.

- This week, specific Ethereum addresses generated with the ‘Profanity’ address tool, were drained of their tokens. Profanity utilises a random seed input to create the addresses’ private and public keys when generating Ethereum wallet addresses. The blockchain utilised this tool to generate millions of addresses per second. However, through a brute force algorithm, the vanity address could be returned to the initial seed input and subsequently the private key. This native issue to Ethereum resulted in hundreds of millions of dollars being drained from wallets.

DeFi

- A U.S. judge has ordered Tether to provide the court with specific evidence relating to the reserves backing its stablecoin (USDT). The evidence requested is expected to be replete with balance sheets, income statements, bank statements and more. These orders have been made as part of a lawsuit relating to whether Tether utilised USDT to inflate the price of cryptocurrencies, ergo partaking in market manipulation. Although Tether has begun publishing quarterly reports on its reserves, the specific details of the issuer’s commercial paper holdings have not been publicly disclosed.

- Falling victim to the aforementioned Profanity vulnerability, Wintermute’s DeFi-related wallets were drained for $160 million. The exploiter obtained access to the administrative wallet of Wintermute, enabling them to move the address’ funds to their personal wallet. Due to the nature of the exploit, the market maker’s OTC and centralised finance operations were not affected according to their official response. Officially, Wintermute appears to remain solvent with more than twice the stolen amount in equity. Wintermute has chosen to treat the exploit as a white hat hack. As such, the dominant market maker has offered the attacker 10% if they return the remainder of the stolen funds.

- According to an article published by Bloomberg, U.S. parliamentarians have proposed a law that aims to ban algorithmic stablecoins. Specifically, the bill would see it illegal to create “endogenously collateralised stablecoins” – those which are collateralised by a token created by the same issuer; for example Terra’s backing of UST with LUNA. Though no information on how this proposed ban would be enforced, it is our view that it is likely that American-regulated exchanges would not list or make use of these tokens.

Innovation

- Zilliqa, a layer 1 blockchain, has announced the prototype of its web3 gaming console to enable individuals to directly play NFT-based games without relying on centralised authorities. This console will be the first Web3-based console and face competition from existing industry giants such as Sony and Microsoft. It seeks to enable individuals to mine Zilliqa’s native ZIL tokens whilst playing on the console. Furthermore, the web3 gaming console will feature a built-in wallet, and first-party games, developed by Zilliqa.

- Following discussions and the proposal to migrate Helium from its own blockchain to Solana, the governance vote has passed with 81.4% of participants voting for the change. Consequently, the contracts of Helium tokens, including HNT and MOBILE, are set to be moved onto Solana smart contracts. In the same week, the creator of Helium, Nova Labs, partnered with T-Mobile to launch Helium Mobile – a 5G wireless service. Expected to launch in Q1 of 2023, the service will be a mobile virtual network operator, leveraging T-Mobile’s US.-based 5G network and Helium’s 5G nodes. Plans for Helium Mobile wireless offering will officially start at $5 per month and be built into Solana’s upcoming Saga phone.

Altcoins

- As part of its aggressive blockchain expansion, Tether has launched USDT on Polkadot. This announcement comes weeks after USDT was launched on NEAR Protocol – another proof of stake blockchain. Unlike bridged versions of the stablecoin, each native USDT token on Polkadot, issued by Tether, will be redeemable for $1. Resultantly, developers will have access to a stable cryptocurrency that is defended by centralised authorities. Notably, USDT will be accessible on all of Polkadot’s Parachains. Accordingly, it is our view that the stablecoin will likely become highly utilised on the layer-0 network given the necessity for a secure token after the depegging of Acala’s aUSD.

NFTs & Metaverse

- Monopolising on the significant growth of Arbitrum, OpenSea announced that this dominant layer-2 network would be natively supported by the NFT marketplace. This is the first integration of a roll-up platform with OpenSea; though the team did stipulate it would support NFTs on Immutable X, layer-2 is yet to be supported on the marketplace. As such, NFTs launched on Arbitrum such as GMX’s GBlueberry Club and Dopex’s Diamond Pepes will be onboarded and purchasable on OpenSea. With the inclusion of the optimistic layer 2 platform, OpenSea supports a total of 5 networks and blockchains, Ethereum, Polygon, Solana, Kalyan and Arbitrum.

- Additionally, OpenSea released a new feature, SeaDrop, to enable creators to launch their collections on a dedicated drop page. SeaDrop allows entities to design their own page for NFT mints that are linked to OpenSea’s main server. Correspondingly, projects will now be able to offer investors a means to mint NFTs through OpenSea. Moreover, SeaDrop mitigates the necessity for coding expertise as the platform will offer creators with existing smart contracts OpenSea were incentivised to launch this service to make minting a safe feature and increase the NFT collections that can be created without the need for contracts.

What to Watch

- Developments in Russia x Ukraine conflict following military mobilisation.

- US’ Consumer Confidence report, on Tuesday.

- US’ Core PCE Price Index, on Friday.

Insights

- Here is MarketWatch’s coverage of the ETH Merge Note, our most recent structured product which seeks to reap ETH’s volatility following the merge update to provide dual outcomes for investors.

- Read about FSHD Global’s 11th Annual Sydney Chocolate Ball and how Zerocap’s sponsorship contributed to the cause of FSHD muscular dystrophy research.

- Regenerative Finance (Part 2) – A New Financial Paradigm: In Part 2 of 3 for our Regenerative Finance coverage, Innovation Analyst Nathan Lenga covers how financial incentives can be involved in bringing about a regenerative society and what protocols are currently working to innovate in this space.

Disclaimer

This material is issued by Zerocap Pty Ltd (Zerocap), a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799.

Material covering regulated financial products is issued to you on the basis that you qualify as a “Wholesale Investor” for the purposes of Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client), or your local equivalent.

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice,take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

FAQs

What significant changes occurred in the crypto market during the week of 26th September 2022?

The week witnessed several significant developments in the crypto market. The Pentagon launched an effort to assess crypto assets as potential threats to national security. The UK introduced a law empowering the government to seize, freeze, and recover crypto assets. The US Treasury sought public opinion on crypto regulations, and the US House of Representatives proposed a bill seeking a two-year ban on algorithmic stablecoins.

How did Bitcoin and Ethereum perform during the week of 26th September 2022?

Bitcoin’s action during the week centered around the 19,000 level, with the 18,450 level acting as a firm support. Ethereum, on the other hand, lost the 1,420 support level and saw a strong downward trend at the beginning of the week. Despite some recovery, Ethereum ended the week at 1,295, indicating an underlying weakness in the market.

What were the major developments in the DeFi and Altcoin sectors during the week of 26th September 2022?

In the DeFi sector, a U.S. judge ordered Tether to provide specific evidence relating to the reserves backing its stablecoin (USDT). Wintermute’s DeFi-related wallets were drained for $160 million due to the Profanity vulnerability. In the Altcoin sector, Tether launched USDT on Polkadot, marking its aggressive expansion in the blockchain space.

What innovations were introduced in the crypto market during the week of 26th September 2022?

Zilliqa, a layer 1 blockchain, announced the prototype of its web3 gaming console, which would enable individuals to directly play NFT-based games without relying on centralized authorities. Helium, after discussions and a proposal to migrate from its own blockchain to Solana, saw the governance vote pass with 81.4% of participants voting for the change.

What were the key events to watch in the crypto market following the week of 26th September 2022?

Following the week of 26th September 2022, key events to watch in the crypto market included developments in the Russia-Ukraine conflict, the US’ Consumer Confidence report, and the US’ Core PCE Price Index. These events could significantly impact the crypto market’s direction and volatility.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Interview with Ausbiz: How Trump’s Potential Presidency Could Shape the Crypto Market

Read more in a recent interview with Jon de Wet, CIO of Zerocap, on Ausbiz TV. 23 July 2024: The crypto market has always been

Weekly Crypto Market Wrap, 22nd July 2024

Download the PDF Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact

What are Crypto OTC Desks and Why Should I Use One?

Cryptocurrencies have gained massive popularity over the past decade, attracting individual and institutional investors, leading to the emergence of various trading platforms and services, including

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.