Content

- Holiday Break

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What is the significance of the Weekly Crypto Market Wrap for 20th December 2021?

- Q: What were the key highlights in the Bitcoin market for the week?

- Q: How did Ethereum perform during the week, and what are the key levels to watch?

- Q: What were the major developments in the DeFi and Innovation space?

- Q: What are the things to watch in the coming weeks in the crypto market?

- Disclaimer

20 Dec, 21

Weekly Crypto Market Wrap, 20th December 2021

- Holiday Break

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What is the significance of the Weekly Crypto Market Wrap for 20th December 2021?

- Q: What were the key highlights in the Bitcoin market for the week?

- Q: How did Ethereum perform during the week, and what are the key levels to watch?

- Q: What were the major developments in the DeFi and Innovation space?

- Q: What are the things to watch in the coming weeks in the crypto market?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Holiday Break

This week’s Market Wrap is our last of 2021 as the team takes a well-deserved break! We are grateful for your support and are looking forward to an amazing 2022. The next wrap will be out on Tuesday, January 4th.

Happy Holidays and a Happy New Year!

Week in Review

- Bitcoin reaches a milestone with 90% of total supply mined.

- FOMC Meeting – The Fed will double the tapering level, the market pricing in up to three rate hikes in 2022. J. Powell states inflation may stay “persistently high.” The Omicron variant does not impact tapering plans.

- Fed Chair Powell does not consider crypto a threat for financial stability – believes they can “certainly be a useful, efficient consumer-serving part of the financial system.”

- US Retail Sales drops again due to shortages and inflation, despite the holiday season.

- Rostin Behnam confirmed as new CFTC chair – Behnam believes the CFTC should be crypto’s “primary cop,” recently requesting oversight of its markets.

- In its 2021 annual report, US Financial Stability Oversight Council officially identifies cryptocurrencies as a threat to the financial system.

- US SEC announces agenda for the upcoming months, does not include crypto topics; Commissioners release statement on lack of digital assets in agenda – “The market can expect continued questions […] around this area of increasing investor interest.”

- Russia’s central bank seeks to ban crypto investments in the country; Reuters report.

- Senate hearing on stablecoins – regulatory uncertainty remains the main issue, USD-backed issuance put into question, while Senator Pat Toomey provides his own set of regulatory principles.

- The IMF Chief Economist calls for a global policy on cryptocurrencies, stating that crypto bans do more harm than good.

- UK advertising watchdog ASA bans crypto ads for Coinbase, Kraken Luno and more; ads allegedly misleading to viewers.

- Over 83% of millennial millionaires are digital asset investors; CNBC survey.

FED’s Dot Plot (Bloomberg)

Winners & Losers

- The entire market experienced bidirectional volatility this week with indecision still controlling price action. This period of consolidation has led to some smaller cap assets experiencing capital inflows as the retail crowd continues to take speculative bets. Moving into the holiday period, trade volume will likely continue to decrease with many in the US taking annual profits and most now waiting for the new year before repositioning. Overall, BTC returned -6.78% and ETH -5.04% WoW.

- Global Stocks played a defensive mood throughout the week. An atmosphere of hawkish central banks and global uncertainty relating to the Omicron variant weighed heavily on growth stocks. The Nasdaq opened the week at a high of 16,330 but quickly lost momentum following higher than expected US CPI data from the previous Friday. Meanwhile, the “buy UK” equity trade which dominated broker recommendations at the beginning of 2021, has backfired big time. This year, British stocks had suffered record outflows despite being at their cheapest level in more than 30 years. The valuation on the MSCI UK index has seen its discount versus global stocks widen throughout 2021 and is now at its broadest level since 1990.

- Bond curves bear flattened out as more front-end hikes are now being priced into the equation. However, every time an equity selloff materialises, money flows into the long end of the Govie curve in anticipation of the central bank PUT coming back sooner than expected, making flattening trades the best play of the week. Credit and risky assets took the most beating as the market was winding down to book their profit for the year and wait for a clean set of investment ledgers in the new year. Chinese developer Kaisa failed to service the latest USD bond coupon payments, with its shares dropping to the lowest level since December 2009.

- Volatility rose towards the FOMC and the ECB meeting, with a slight relief rally following less than expected tapering velocity (FED announced doubling the reduction in bond buying from a USD 15 billion a month reduction to USD 30

billion reduction, but this is coming from a record USD 120 billion a month purchase). The ECB was more dovish as the central bank sounded more concerned about growth and COVID19 cases than inflation. Another way of interpreting the week could also focus on the FED announcements stating that they no longer target full employment before normalising interest rate; the market now has three hikes in 2022 priced in with the first move brought forward to April. BoE and Norges bank raise rates, further dampening any hope of a Christmas rally in risky assets. - Geopolitical concerns are brewing as the market is shifting gear into a risk aversion mood, with Russia’s 100,000 troops lining across the Ukrainian border and Taiwan’s defence ministry and former Japanese PM Abe both raising the prospect of an all-out war between China and some US-allied nations over Taiwan’s sovereignty. Hong Kong held its first election since Beijing induced political reform, which turned out to be the lowest ever at 32%.

- Uncertainty over the Omicron variant also increased volatility on asset markets, as global coronavirus cases topped 266 million and 5.3 million death count since it began two years ago. The Netherlands went back into hard lockdown over the Christmas holidays, while London and NYC experienced over 20,000 daily cases. The US still has over 50 million residents yet to take the first dose of the vaccine.

- Macroeconomic data focused on both inflation and a growth focus this week. US PPI rose by 9.6% YoY and 7.7% on the core basis, both beating market estimates. UK inflation hit a ten year high of 5.1% as the Bank of England hiked rates by 25bp, in line with expectations. In contrast to other major economies, China cut its lending benchmark loan prime rate (LPR) for the first time in 20 months at its December fixing on Monday, largely in line with market expectations.

- The FX and commodities markets were somewhat quiet following the previous week’s volatility. The USD initially rose on the back of anticipation into the FOMC, with USDJPY climbing above 114.20 before dropping back to a low of 113.20 towards the week’s end. The AUD short squeezed higher following the previous week’s sub 70 cents trade, hitting a high of 0.7223 for the week before settling around 71 cents. The EUR was extremely choppy going into the ECB meeting, but a dovish Lagarde pushed the EUR down towards the weekly low of 1.1238 for the closing. Gold prices fluctuated around the USD 1,800 mark, but little of the new trend came through – it’s just following the bond market on a day to day basis. WTI futures weakened below the USD 70 mark as the spread of the Omicron variant weighed on holiday travel.

Macro, Technicals & Order Flow

Bitcoin

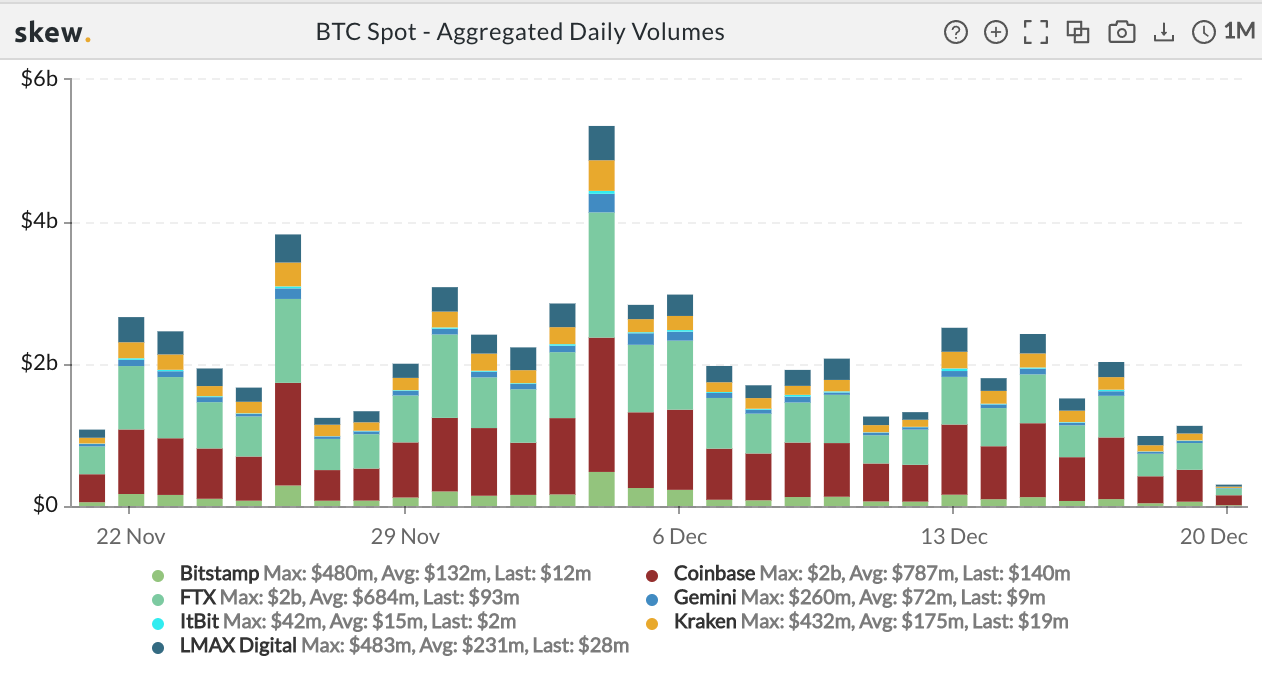

- This week, as sentiment subsided in preparation for the Federal Reserve’s Wednesday announcement, the 200-Day Moving Average sitting around the 46,000 mark acted as the key level, with the prospect of three rate hikes in 2022, followed by a further three expected hikes in 2023 leading the market narrative. The promise of sustained market liquidity (easing the taper at a slower than expected pace) boosted sentiment pushing prices back to the 49,000 level. However, rising concerns of Omicron running rampid in Europe and doubts whether inflationary pressure can be controlled pulled the price back to the 46,000 mark.

- Whilst 200-SMA was respected early in the week, spot volumes are beginning to drop off coming into the end of the year, chopping up momentum and breakout traders. Beware as liquidity thins into the New Year – levels are less likely to be respected.

Spot BTC Aggregated Volumes

- As the risk of Omicron, lockdowns and a delayed labor market recovery grows, short-term movements will likely be dictated to the extent at which investors move away from risk-on to risk-off assets over the new year. BTC is clearly acting as a risk asset against this backdrop right now – however, we still hold that medium-term, this is the hedge that makes sense.

- On-chain indicators outline that the supply squeeze on exchanges is persisting and has grown since November. Conversely Funding rates are mixed across exchanges, showing indecision in the derivatives market. On aggregate however, the rates are positive showing a bullish lean in an otherwise slowing market. This said, outflows have persisted from exchanges over the past month, which has seen prices bleed lower.

Bitcoin Net Position Change

BTC Perpetual Swaps Funding

- Recent bearish price action has created a vacuum of open interest volume between the 45,000 and 50,000 levels going out to December 31. However, strikes are still weighted towards calls at 80,000, 100,000 and 200,000

- Open interest out to Mar 25, 2022 shows that emphasis is placed on the 80,000, 100,000 and 150,000 levels for calls.

OI Interest by Strike – Dec 31, 2021

OI Interest by Strike – Mar 25, 2022

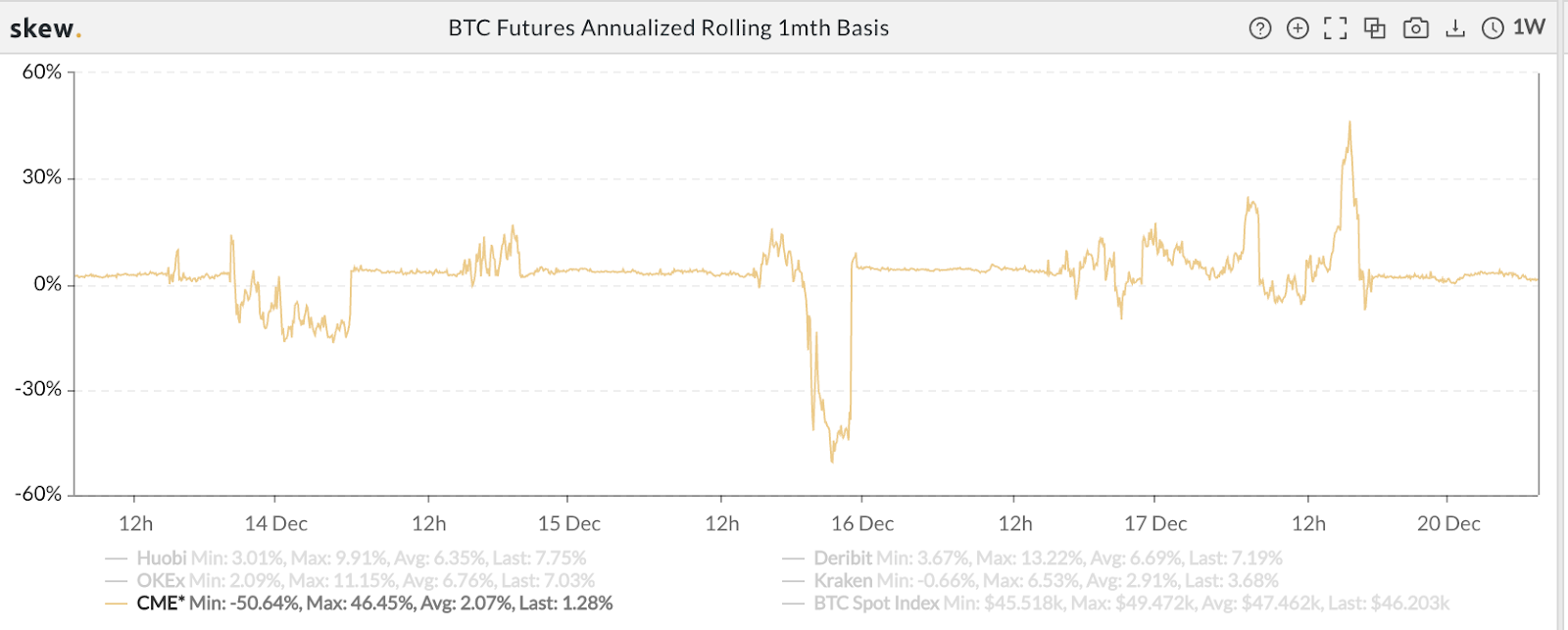

- The futures basis curve steadily increased throughout the week on native crypto exchanges. However, notably the CME slipped into backwardation after the FOMC announcements were made.

BTC Futures Annualised Rolling 1 Mth Basis (Crypto Exchanges)

BTC Futures Annualised Rolling 1 Mth Basis (CME)

- Short-term holder supply that bottomed in late October has continued to show consistent signs of growth. Conversely, long-term holder supply continues to support signs of rotation. This indicator needs assessment as the correlation is breaking against the prior trends, but worth keeping an eye on given the divergence.

BTC Total Supply Held by Short-Term Holders

Bitcoin: Total Supply Held by Long-Term Holders

Bitcoin: Long-Term Holder Net Position Change

Bitcoin Futures Open Interest

- In summary, bond tapering, albeit at a slower velocity than expected post-FOMC, and proposed interest rate hikes for 2021 are clear signs that the investment environment is changing. We are entering a period of consolidation, with lower levels of liquidity and leverage over the Christmas period. Going into the new year, short-term volatility will primarily be event and liquidity (lack thereof) driven, further conditioned by the advancement or retraction of the Omicron variant. Perhaps a time to drop the tools and take a break until we get some clear direction into 2022, or play entries via structured products for yield against this backdrop.

Ethereum

- The week began with a sell-off as investors began to de-risk in preparation for the Fed announcement. This marked the weekly low around 3,600. Following the Fed’s announcement that bond tapering was to be slower than expected, ETH renounded alongside risk assets.

- As the macro landscape tightens, short-term volatility will be led by investors de-risking or adding to risk, as well as institutional rebalancing before the EOY. On balance we believe derisking against any event risk is more likely if newsflow turns south over this period.

- Key levels for ETH are clearly the support at 3,600 and the prior notable highs before 4,800.

- DEX’s have seen consistent growth for the better part of 2021. However, overall sentiment for the space is unclear. In recent regulatory hearings, the U.S. Treasury Assistant Secretary expressed favourable commentaries on DeFi stating that the “right laws and regulations should be technology-agnostic” whereas Senator Warren has scrutinised the space, blaming a lack of regulation.

- This coupled with a decrease in the growth of funding in the DeFi space and funding growth in the NFT & Metaverse spaces suggests that the focus on DeFi may be dwindling.

DEX Volume (Delphi)

DeFi TVL in Competitor Chains (Delphi)

- On DeFi, we are referring more and more to the technology adoption curve as a way to understand where DeFi is on the spectrum of its growth and adoption. We’ve seen huge uptake of DeFi in the crypto space, largely from yield farming and arbitrage opportunities in token rewards. The technology itself is incredible, but we foresee moderation in prices before we really get uptick in traditional institutions and legacy finance taking up the technology in a meaningful way. Where do you think we are on the curve?

Technology Adoption Curve

- We are still seeing strong derivatives interest in higher ETH prices, specifically around the 5,000 and 10,000 levels.

ETH Open Interest by Strike: Dec 31, 2021

- ETHBTC continues to range around its multi-year high, as ETH continues to outperform BTC during rebounds on risk. As I write this, we are heading lower – which coincides with a key shift in on-chain data – showing that for the first time since October, exchanges experienced a net inflow, suggesting a supply expansion on exchanges.

ETHBTC Daily Chart

Ethereum Exchange Net Position Change

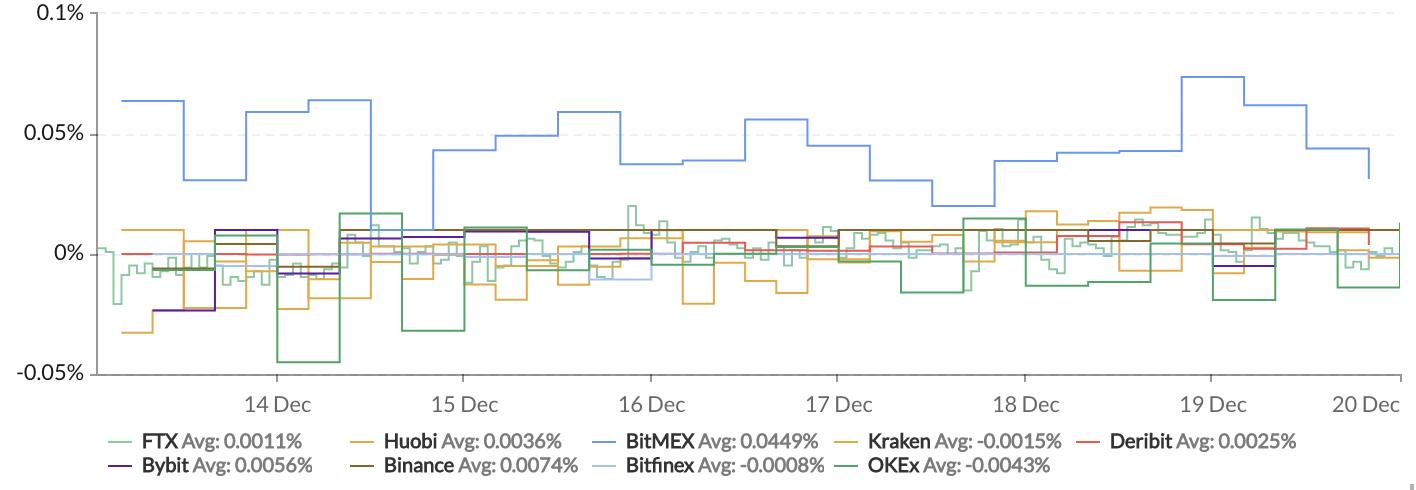

- Perpetual funding rates remain relatively stable across most exchanges, as volatility is contained.

ETH Perpetual Funding Rates

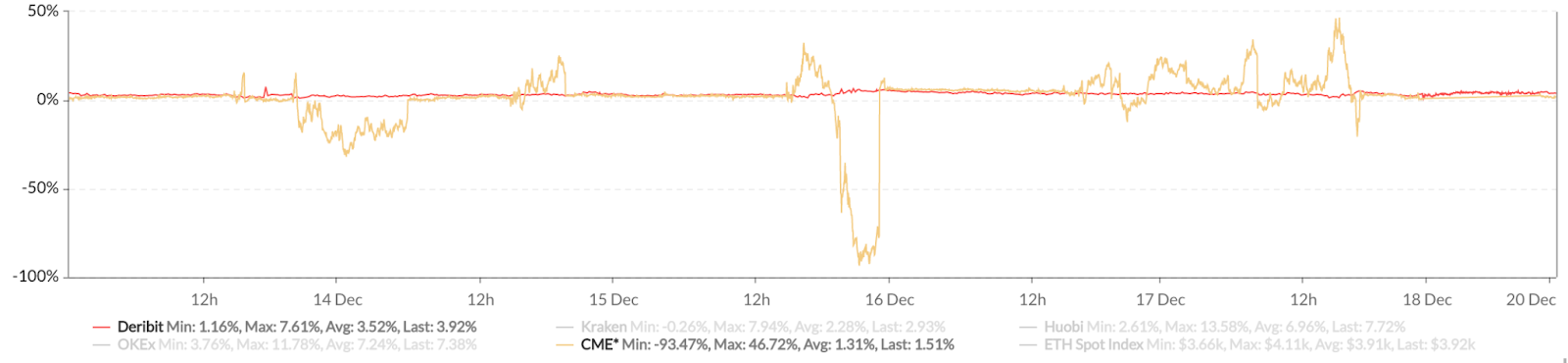

- The futures basis saw a wild drawdown into backwardation, followed by a sharp recovery into the positives at the CME. Total open interest on ETH CME Futures has surged above $1 billion, now representing 10% of total CME open interest. There is definitely some price discovery happening here.

ETH Futures Annualised Rolling 1 Mth Basis

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,699,604. This represents 7.32% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- In summary, ETH continues to outperform BTC on risk-on moves. As the Fed attempts to control inflation through tightened monetary policy, investor confidence may begin to diminish into 2022. ETH’s price action moving forward will likely be dependent on the risk environment, and the extent of its utilization in the DeFi, NFT and Metaverse ecosystems against major competitor protocols, and its role in emerging Web 3.0 themes.

DeFi & Innovation

- US Senator Elizabeth Warren states DeFi is “the most dangerous part of the crypto world” during hearing, calls for immediate regulations on DeFi and stablecoins.

- Wells Fargo and HSBC partner to use blockchain technology in FX settlements.

- Universities such as Berkeley, MIT, Harvard and more partner to form an Education DAO that promotes Web 3.0 innovations.

- Michael Jordan launches HEIR, a fan-engagement platform built on the Solana blockchain.

- Nike enters the metaverse with RTFKT acquisition; company makes virtual sneakers.

What to Watch

- Further details on tapering plans for 2022 and the alleged rate hikes proposed by Fed.

- Australia’s Monetary Policy Meeting Minutes on Wednesday.

- US’ Core PCE Price index on Thursday.

- Developments following US Senate’s hearing on stablecoin regulations.

- Potential rebuttal by US’ SEC on the lack of crypto topics in its recent agenda release.

FAQs

Q: What is the significance of the Weekly Crypto Market Wrap for 20th December 2021?

The Weekly Crypto Market Wrap is the last one for 2021 as the Zerocap team takes a holiday break. It provides a summary and analysis of the previous week’s events in the digital asset market, including Bitcoin’s milestone, the Federal Reserve’s plans, and the overall market performance.

Q: What were the key highlights in the Bitcoin market for the week?

Bitcoin reached a milestone with 90% of the total supply mined. The Federal Reserve’s plans for tapering and rate hikes, along with concerns about the Omicron variant, influenced the price. The 200-Day Moving Average around the 46,000 mark acted as a key level, and the market is entering a period of consolidation with lower liquidity.

Q: How did Ethereum perform during the week, and what are the key levels to watch?

Ethereum began the week with a sell-off but rebounded after the Fed’s announcement. Key levels for ETH are the support at 3,600 and the prior notable highs before 4,800. The price action moving forward will likely depend on the risk environment and its utilization in the DeFi, NFT, and Metaverse ecosystems.

Q: What were the major developments in the DeFi and Innovation space?

US Senator Elizabeth Warren called DeFi the “most dangerous part” of the crypto world and called for regulations. Wells Fargo and HSBC partnered for blockchain technology in FX settlements. Universities formed an Education DAO for Web 3.0 innovations, and companies like Nike entered the metaverse.

Q: What are the things to watch in the coming weeks in the crypto market?

Investors should watch for further details on tapering plans for 2022 by the Fed, Australia’s Monetary Policy Meeting Minutes, the US’ Core PCE Price index, developments following the US Senate’s hearing on stablecoin regulations, and potential responses by the US’ SEC on the lack of crypto topics in its recent agenda release.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 13 Dec. 2021 0:00 UTC to 19 Dec. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.