Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What were the major economic highlights of the week according to the report?

- Q: How did Bitcoin and Ethereum perform during the week?

- Q: What were the significant developments in the DeFi and Innovation sector?

- Q: What are the key factors to watch in the coming week?

- Q: What services does Zerocap provide, and how can one contact them?

- Disclaimer

1 Nov, 21

Weekly Crypto Market Wrap, 1st November 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What were the major economic highlights of the week according to the report?

- Q: How did Bitcoin and Ethereum perform during the week?

- Q: What were the significant developments in the DeFi and Innovation sector?

- Q: What are the key factors to watch in the coming week?

- Q: What services does Zerocap provide, and how can one contact them?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- US’ Q3 GDP shows sharp decline with a 2.0% annualised rate. PCE Price Index points to inflation still high, with the Index rising to 4.4% in September.

- S&P 500 and Nasdaq close at record highs, Dow Jones registers another record week.

- Eurozone inflation reaches 13-year high, rising to 4.1% in October.

- ASIC issues guidelines for crypto ETPs under five conditions, affirming that bitcoin and ether “appear likely to satisfy all five factors.”

- US SEC set to take charge of stablecoin regulations.

- Neuberger Berman partners with BlockFi to launch crypto ETFs.

- Biden’s CFTC chair pick wants a “beat cop” agency able to oversee 60% of the crypto market.

- US Department of Justice seeks director for its National Crypto Enforcement Unit.

- US FDIC preparing guidance on banks and crypto, set to release in upcoming months.

- DBS Bank joins Hedera council to explore opportunities in blockchain technology.

- Financial Action Task Force (FATF) releases updated crypto guidance report.

- Mastercard plans to allow partners to offer crypto loyalty rewards to their clients – prepares infrastructure for deployment of CBDCs

- MicroStrategy buys more 9k bitcoin, grows holdings to 114,042 BTC (roughly $7B).

Winners & Losers

- Volatility continued to shake the crypto markets this week. Bitcoin looked to be recovering from its fall from $67,000 before continued correction punished overleveraged traders. With price reaching as low as $56,500, not only was leverage reset but so too was the sentiment of a speedy recovery to a new all-time high (ATH). While Ethereum followed suit earlier in the week, the asset’s recovery saw it break a new all-time high at $4,460, outpacing BTC. The rest of the crypto market saw heightened volume with meme tokens such as SHIB more than doubling during the week. Metaverse tokens also saw healthy gains (MANA up more than 5x at its peak) as a result of Facebook’s announcement to rebrand the company to Meta. Overall, Bitcoin returned 0.78% for the week while ether returned 4.88%.

- Macroeconomic data dominated equity trading, as strong earnings season reporting concludes. Supply-side inflation expectations highlighted media headlines as G20 nations met over the weekend to discuss carbon emission controls and targeting during the COP26 event. The term ‘greenflation’ is the new representation of ESG induced supply and demand-side inflation with new investments unlikely to channel through projects with a large carbon footprint going forward. On the earnings front, 93% of all tech sector reporting had beaten estimates, and with Facebook’s name change, we now have a new major category called the MAANGs.

- UST curve flattened out substantially during the week as the market is now pricing in a much earlier hiking cycle from the FED. The interest rate curve is now interpreting a more aggressive tightening cycle, which will lead to the crowding out of economic activity down the track. Domestically, the RBA failed to carry through with their three-year bond-buying intervention, leading to a rush out of the door for bondholders. The yield on the two-year Govies benchmark went from 0.16% at the start of the week to close at 0.62%, a 380% jump. Several domestic institutions also revised their mortgage rate offerings higher. With the majority of the domestic banking industry relying heavily on mortgage lending as core income, the risk to underlying return will be the highlight from now on. There is also balance sheet risk; with first home buyers entering the market during the pandemic because of government incentives and low borrowing rates, a raise in variable interest rates could lead to a rise in non-performing loan (NPL) ratios.

- Volatility measured by the VIX index remained subdued throughout the week. The range was tight, with the index trading between 15.5 to 17.5, closing somewhere in the middle.

- The commodities market generated much greater volatility during the week as supply-side constraints through the ‘greenflation’ induced price rise, contrasted with a slowing down from China’s weaker PMI data. While WTI contract price rallies passed seven-year high, ICE natural gas contract traded down 24% following Russian President Putin’s promise to increase supply to Europe. China’s Zhengzhou thermal coal contracts fell by 35% as both Manufacturing and Service PMI emerged weaker than forecast. Gold price struggling to break through the 100 DMA just below $1,800 convincingly.

Macro, Technicals & Order Flow

Bitcoin

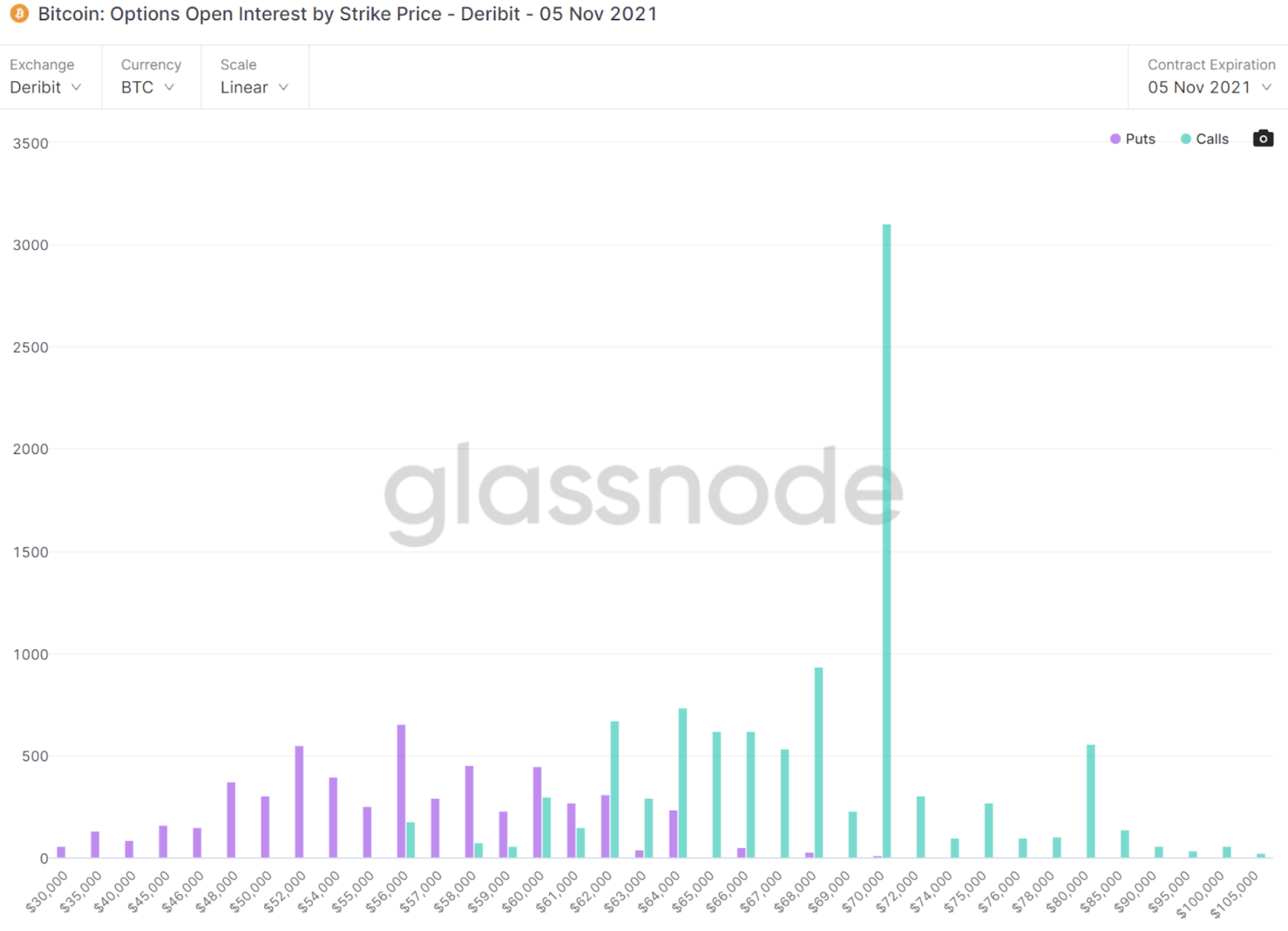

- The 57,500 level saw a nice false break leading to topside rejection by the descending trendline from all-time highs. We are forming a (loose) wedge here, with some strong optionality from Nov 5th indicating that we may see a topside break. The Nov 5th expiries and beyond are seeing notable open interest in the 70,000 and above level – with some traders expecting fireworks.

- Fundamentally BTC is well-positioned for another break – the narrative around ‘greenflation’ in the media is taking hold, with concerns around stagflationary environments with supply-chain constrictions across energy and other non-ESG sectors. With the increasing correlation between bitcoin and inflation, the market has begun showing its hand – with BTC recently rallying on inflation shocks over gold.

- On the back of this, there is a continued recent bid by funds, maintaining a steady accumulation. Furthermore, the velocity of bitcoin held by long-term holders may have slowed recently – but the trend is still clearly leaning towards supply constrictions in the current environment.

Bitcoin Held By Funds

Bitcoin: Total Supply Held by Long-Term Holders

- On-chain data is showing net-outflows from exchanges (indicating contraction in supply). However, this is relatively moderate compared to recent cycles from Sep and May of 2021, and Nov 2020.

Bitcoin Net Position Change

- The on-chain UTXO price distribution shows the depth of bitcoin activity at certain price levels. Last week, there was little resistance all the way up to 66,000. We’ve now built some near term levels up to 64,000, but above 64,000 we could see a clean run to break highs.

UTXO Realised Price Distribution

- The futures basis curve continues to expand – with the Proshares ETF gunning for $1.5B AUM in only a few weeks after its launch, this is keeping a healthy premium on BTC futures across the board. The ETF’s current allocation places 51% to buying CME bitcoin futures contracts that settle in November, with the remaining held in U.S. Treasury bills. This should keep a healthy premium on dated futures, aiding yield plays and liquidity for delta-neutral funds. Notably, the last few days have seen a drop in open interest and the premium in the CME – which is likely related to rebalancing on October’s expiry. Make no mistake, the ETF flows have a real effect on the basis curve.

BTC Futures Annualised Rolling 1 Mth Basis

Bitcoin Futures Open Interest

- In other derivatives markets, perpetual funding rates are elevated and the estimated leverage ratio is growing, but both metrics are stable. Leverage not betting the break just yet, but given optionality and on-chain indicators, we could still see a run at highs before November comes to a close.

BTC Perpetual Swaps Funding

Bitcoin Futures Estimated Leverage Ratio

Ethereum

- We mentioned last week that the risk environment was conducive to ETH breaking highs, and break it did, albeit moderately before retracing back into the range. This said, we are seeing key rejections at the ascending trendline from late Sep, and given the momentum behind the NASDAQ and general risk, we foresee ETH trading above highs again this week.

- On-chain indicators are backing this thesis – and we are seeing strong outflows from exchanges (indicating contraction in supply), at a faster velocity when compared to BTC’s outflow metrics. Every week the risk-on / risk-off characteristics between ETH and BTC is strengthening.

Ethereum Exchange Net Position Change

- On-chain data is continuing to show larger wallet holders with supply held by 10 to 100 ETH continuing to increase. Smart money is still accumulating, even at these levels.

Ethereum Exchange Net Position Change

- Perpetual funding rates are elevated, and notably, the velocity of the funding rate change is swift. WIth leverage building, a break of highs may prove increasingly volatile.

ETH Perpetual Swaps Funding

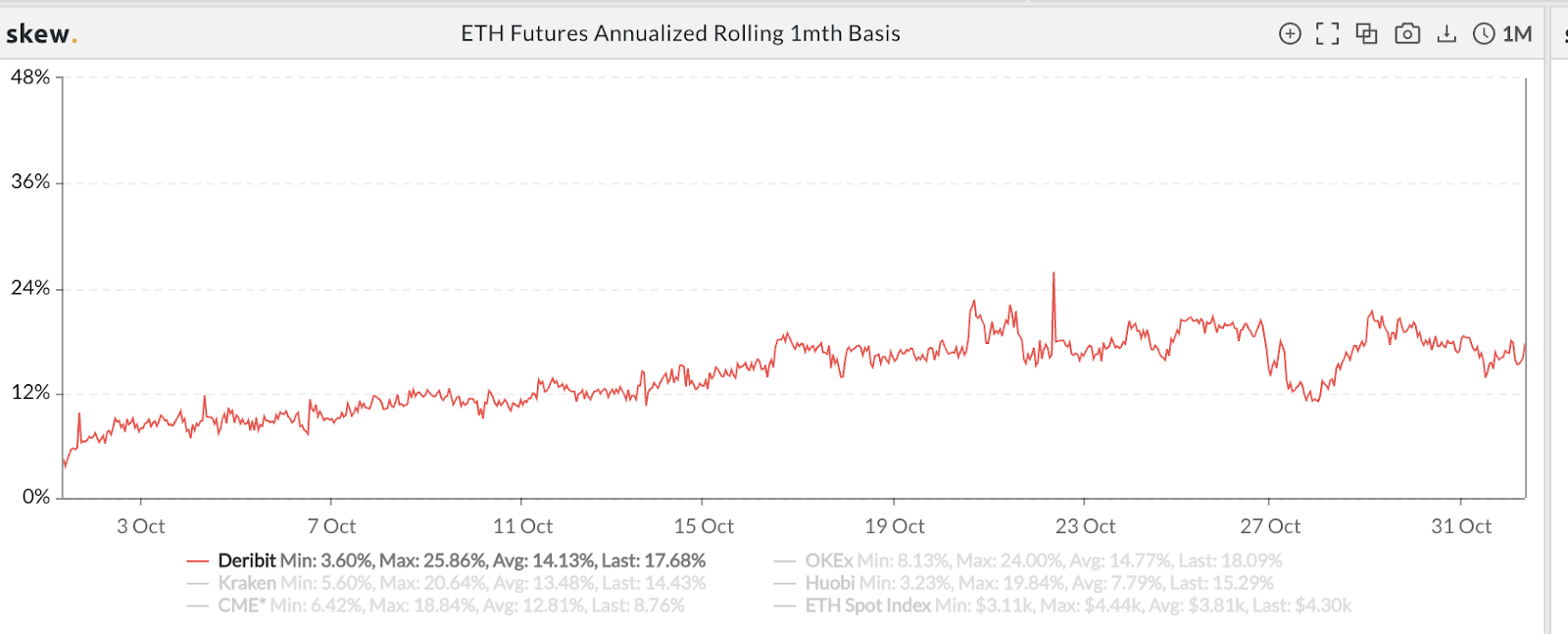

- The futures basis curve is expanding week on week for ETH. We didn’t think that ETH’s futures basis would rally like BTC’s basis curve given that ETH doesn’t have the same market structure bidding CME quarterlies, however looking at the ETH curve now – we could see some front running on the expectation that an ETH futures ETF could be on the horizon. Although, as we mentioned last week – we feel that pricing challenges, depth on the CME and the general hangover from getting the BTC ETF over the line will probably delay any decisions on applications from US regulators until at least early next year.

ETH Futures Annualised Rolling 1 Mth Basis

- On the back of stronger futures pricing, Institutional interest in ETH is growing alongside it. The Grayscale AUM continues to climb which is a strong institutional signal.

Ethereum Grayscale AUM

- The ETH/BTC trade that we’ve been mentioning did get the whip to the topside, finding resistance at prior highs. Again, we still think ETH/BTC has room to move to the downside longer-term, but for now – a break of ETH/USD highs should send ETH/BTC above key levels.

ETH/BTC

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,078,840. This represents 6.84% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- Notably, our OTC desk is still seeing significant flow looking to capture profits before the 5,000 level. If we break highs at 4,460 – planning exits up to 4,800 is not a bad play here. Note that the 5,000 is a psychological level – lots of expectation and orderflow ready to move before and above this level. Good luck for the coming week if it’s an exit for you!

DeFi & Innovation

- Facebook changes corporate name to Meta, highlighting focus on metaverse products – metaverse cryptos rallied, with up to 300% surge in 24 hours across the ecosystem.

- Gamestop set to enter the metaverse with “Web 3.0” job listing.

- THORChain successfully concludes two security audits following July exploits.

- LinkedIn reports crypto job listings have surged 615% since August 2020.

- Actor Matt Damon partners with Crypto.com after exchange’s $1M donation towards his clean water initiative, records TV spot for global ads – FTX buys Superbowl ad.

- Adobe partners with OpenSea for Photoshop-issued NFTs.

What to Watch

- Bitcoin held around its 60k support while ethereum broke its all-time high. As Metaverse and Meme coins rally and DeFi gains more momentum, are we in “altcoin season” territory or could it be froth building before the big drop?

- Fed’s FOMC meetings, on Tuesday and Wednesday, for more details on tapering and economic recovery expectations.

- Confirmation and details regarding US SEC taking charge of stablecoin regulations – are there guidelines ready to be presented?

- Bank of England’s monetary policy report on Thursday.

- Further details following ASIC’s new crypto guidance, with a focus on the new “crypto asset” category for licensing applications and the necessary authorisations to hold underlying assets.

FAQs

Q: What were the major economic highlights of the week according to the report?

A: The report highlights the US’ Q3 GDP showing a sharp decline, Eurozone inflation reaching a 13-year high, ASIC issuing guidelines for crypto ETPs, and MicroStrategy buying more Bitcoin. It also mentions various market movements, partnerships, and regulatory developments.

Q: How did Bitcoin and Ethereum perform during the week?

A: Bitcoin experienced volatility, recovering from a fall before correction, with price reaching as low as $56,500. Ethereum broke a new all-time high at $4,460, outpacing BTC. Bitcoin returned 0.78% for the week, while ether returned 4.88%.

Q: What were the significant developments in the DeFi and Innovation sector?

A: Facebook changed its corporate name to Meta, focusing on metaverse products. Gamestop is set to enter the metaverse, THORChain concluded security audits, and LinkedIn reported a surge in crypto job listings. Adobe partnered with OpenSea for NFTs, and other partnerships and initiatives were noted.

Q: What are the key factors to watch in the coming week?

A: The report suggests watching Bitcoin’s support around 60k, the Fed’s FOMC meetings for details on tapering, confirmation on US SEC taking charge of stablecoin regulations, the Bank of England’s monetary policy report, and further details following ASIC’s new crypto guidance.

Q: What services does Zerocap provide, and how can one contact them?

A: Zerocap provides digital asset investment and custodial services to investors and institutions globally. They offer trading, prime services, and innovation & technology related to digital assets. They can be contacted at [email protected] or through their website www.zerocap.com.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 25 Oct. 2021 0:00 UTC to 31 Oct. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 20 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.