Content

- Weeks in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What were the key highlights in the crypto market for the week of 10th January 2022?

- Q: How did the macroeconomic factors affect the crypto market during the week?

- Q: What were the significant developments in Bitcoin and Ethereum during the week?

- Q: What are some notable trends and innovations in the DeFi space?

- Q: What are the key events and data to watch in the coming weeks?

- Disclaimer

10 Jan, 22

Weekly Crypto Market Wrap, 10th January 2022

- Weeks in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What were the key highlights in the crypto market for the week of 10th January 2022?

- Q: How did the macroeconomic factors affect the crypto market during the week?

- Q: What were the significant developments in Bitcoin and Ethereum during the week?

- Q: What are some notable trends and innovations in the DeFi space?

- Q: What are the key events and data to watch in the coming weeks?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Weeks in Review

- Fed Minutes points to earlier and faster rate hikes, abandoning previous pace stance.

- US JOLTS job openings fell to 10.5 million in November against an expected 11 million, with a record 4.5 million Americans quitting their jobs during the period. NFPs headline job growth came in below estimates at just 199k, but with an unemployment rate of 3.9% well below the expected 4.1%. Wage growth, meanwhile, was also well above expectations at 0.6% on the month and 4.7% y/y – pointing to supply side inflationary pressures in the job markets.

- Euro zone inflation hits a new record high for December, at 5% annualised.

- European countries impose new travel restrictions as Covid-19 cases soar – Hong Kong bans inbound flights including US and Canada in new travel ban.

- Happy 13th Birthday, Bitcoin; the crypto’s first block was mined on January 3rd 2009.

- Bitcoin will most likely take a large share from gold in the “store of value” market; Goldman Sachs.

- Kazakhstan government shuts down internet amid protests, causing Bitcoin’s hash rate to drop 13.4% – Kazakhstan is the second-largest bitcoin mining country in the world.

- Crypto investment funds had $9.3B in inflows for 2021 as institutional adoption grew.

- Number of countries banning crypto has doubled in the last three years; US’ LOC report.

- PayPal confirms research plans to launch a stablecoin.

- UK’s advertising watchdog ASA bans two Crypto.com ads for being “misleading because they failed to illustrate the risk of the investment.”

- “We are 50% of the way there,” says Ethereum co-founder Vitalik Buterin on the network’s development – proposes a ‘multidimensional’ fee structure.

- Biden unveils plan to boost competition in US meat industry, plans to issue new rules and $1B in funding in 2022 to support independent meat processors.

Winners & Losers

- The crypto market saw a further sell-off this week in the face of macro headwinds. After losing the $46,000 level, BTC fell as low as 40,500 joined by the rest of the crypto market. The Fed’s announcement of multiple rate hikes in 2022 saw correlation to US growth stocks increase. Lower liquidity at the beginning of 2022 has not helped the recent moves. Overall, BTC returned -11.45% and ETH returned -17.65% WoW.

- Global Stocks began the year on the defensive. The tech and growth sector selloff was more noticeable, with the Nasdaq index opening 2022 on the highest level of the week (16,473) and closing at 15,607, a 5.5% retracement. Shares in Tesla once again dominated the volatility, as it opened the year with a 13.5% jump (1,057.60 to 1,199.87) before the selling momentum accelerated. The stock closed the week at 1,026.96. Shares in Apple, following a brief climb toward the USD 3 trillion valuations, at which the share price reached 182.73, dropped to 172.17—valuing the company at USD 2.875 trillion. On the other hand, commodity shares, as a recipient of higher supply-side pricing, have started the year as the main beneficiary of stock portfolio reallocation strategy, Rio Tinto shares on the ASX closing last year at AUD 99.877, but have since climbed to above 106.

- The fixed income market once again dominated headline trading this week. Ten year UST yield has climbed from the year-end trading level of 1.51 towards a high of 1.77 this week. In conjunction with growth shares selloff, and an abundant supply of new corporate USD issuance, the credit market also took the full impact of liquidation flows. Despite the FED insisting that they will be patient with rate normalisation, the market is now pricing in the first rate movement to begin in April 2022, with over 3 hikes being priced into the current year. On the credit front, Chinese Local government investment vehicles currently have USD 8 trillion of outstanding liability via the bond market, that’s over half annual GDP, and they have been big dollar bond issuers. Collapsing property sales and Omicron stress are putting pressure on this part of the debt arena. Beijing may let some default; others might try to dump assets in a weak market.

- Volatility was elevated during the first week of trading in 2022. What began as a steady climb quickly shifted gear into a sudden rally from mid-17 on the VIX index to breaking through 20 on the topside. Despite closing off the high, there remains unease in risk markets going into the weekend. Cryptocurrencies took the brunt of the risk to unwind during weekend trading, with BTC liquidation flows testing the psychological support of 40,000 and ETH at 3,000. Liquidity in asset trading should improve in the coming weeks as institutional demand returns from the Christmas break. However, with US CPI data forecast to be elevated, and central banks worldwide now searching for strategies to exit the world of extraordinary stimulus, it might be difficult to see actual volatility collapsing anytime soon.

- Macroeconomic data in the US focused on Friday’s Non-Farm Payroll figure for the month of December. On the headline, it completely missed the mark. Economists were forecasting 450,000 jobs created, but the data printed only 199,000. On closer inspection, previous months numbers were revised higher by 39,000, and the unemployment rate dropped to 3.9% from an expected 4.1%. There was also added inflationary pressure from stronger than forecast hourly earnings (4.7% YoY against expected 4. 2%).

- The FX and commodity markets were actually on the sideline for most of the week, as portfolio allocation moves appeared to maintain similar ratios or slight increases towards commodities. Gold prices did not benefit fully from this week’s movement despite continual inflation concerns. As short term interest rate spikes suddenly, Gold prices tend to play a defensive role because short-term money market funds tend to seek out opportunities with a yield element rather than precious metal. The market traded to a high of 1,831.31 before dropping lower to close the week at 1,795. AUDJPY reflected the risk mood of general asset risk tolerance, opening the year on a high of 83.66 but closing below 81.00.

- Will Clemente tweeted an interesting statistic on hiking regimes – positioning that over 77% of the time we’ve shifted to a hiking cycle, we’ve seen positive stock market returns for the first 6-months. The caveat to the current environment is how ‘shocked’ the market becomes if inflation runs away.

Macro, Technicals & Order Flow

Bitcoin

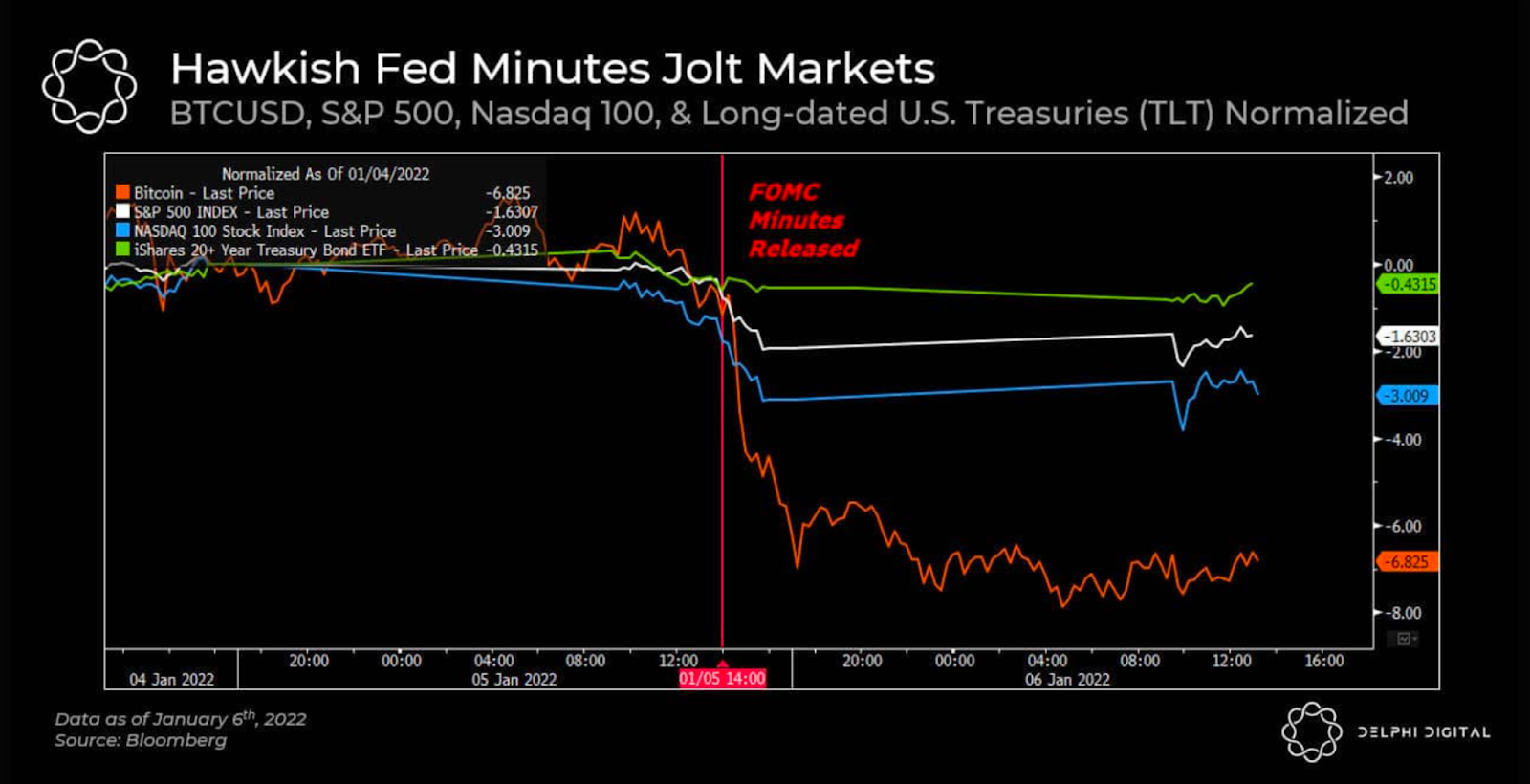

- Last week, as traders braced for a potentially volatile year and three expected rate hikes, relatively thin liquidity persisted around the 46,000 mark. On Wednesday, minutes from the Fed’s December meeting provided the stimulus to push BTC down to the 45,000 level where stops began to trigger, adding to the bearish pressure. As the market soaked up Wednesday’s news, BTC bottomed out around 41,000 before bouncing back to the 42,000 level where price action remained relatively stable.

- 40,000 is the key support, with 37,000 below this. Topside resistance sits at 46,000. It’s important to zoom out on the charts and maintain perspective on these moves. There are clearly market cycles playing out in price, and short-term risk moves occur when uncertainty abounds. The key is maintaining longer-term views on asset allocation – what happens when capital is forced to reallocate and hedge? How does BTC play out when the market is bidding scarcity premiums? These are some of the key fundamentals that we think about internally.

- Despite continuing concerns on inflation and supply bottlenecks, China’s regulatory crackdown, Covid resurgence and geopolitical concerns, the Fed is at the core of the investment outlook for 2022.

Fed Minutes and resulting cross-asset returns (Delphi)

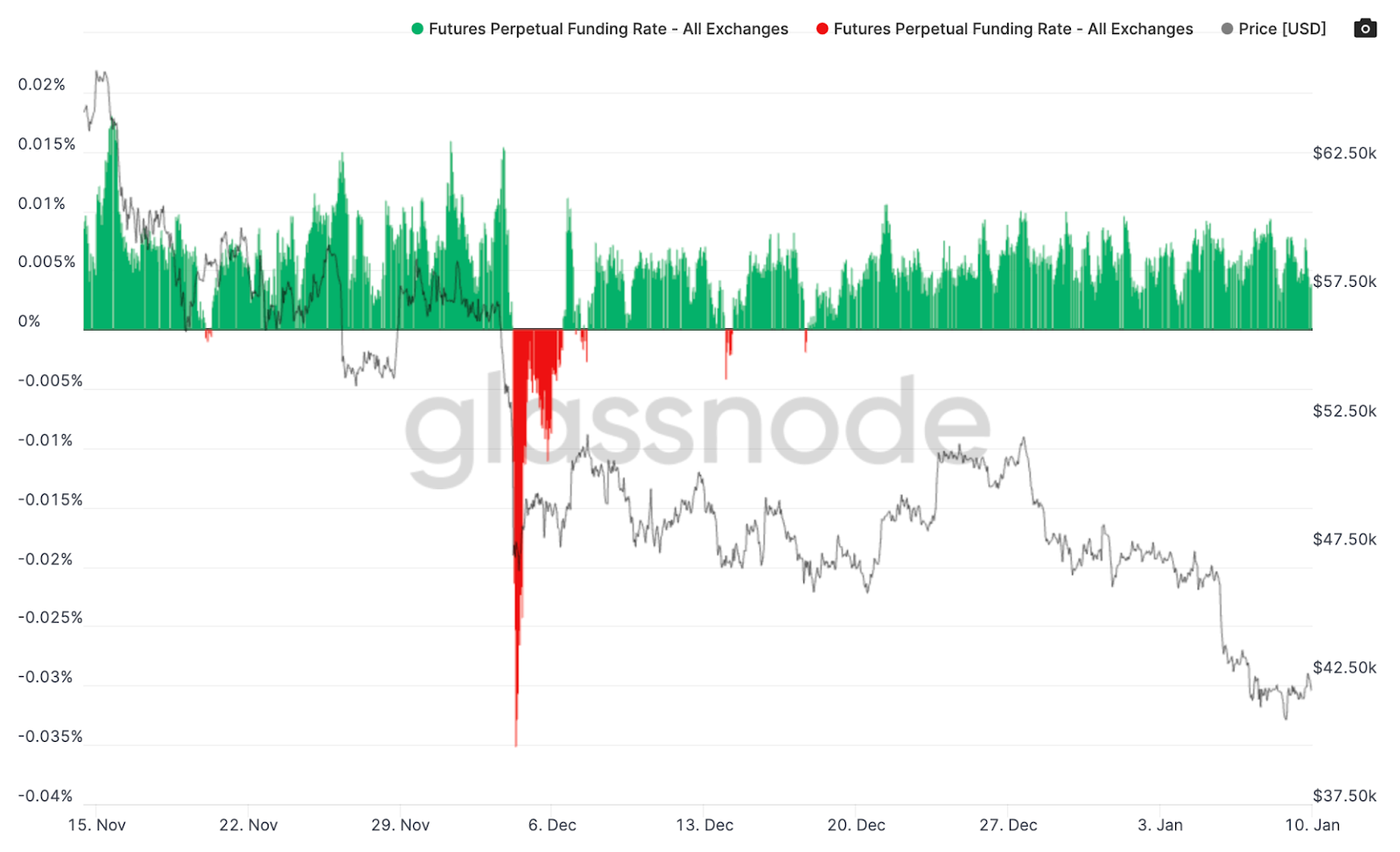

- On-chain indicators show that the supply squeeze on exchanges that sustained through December has now diminished, with supply now moving onto exchanges. Notably, long-term holders continue to accumulate in this market. This suggests that short term players are the active players here and are being hit hard on the recent price action. In aggregate, funding rates remain slightly positive, although this could shift given the weight of the market right now.

Bitcoin Net Position Change

Bitcoin Net Position Change of long-term wallets

BTC Funding Rate Across Exchanges

BTC Perpetual Swaps Funding – Aggregate

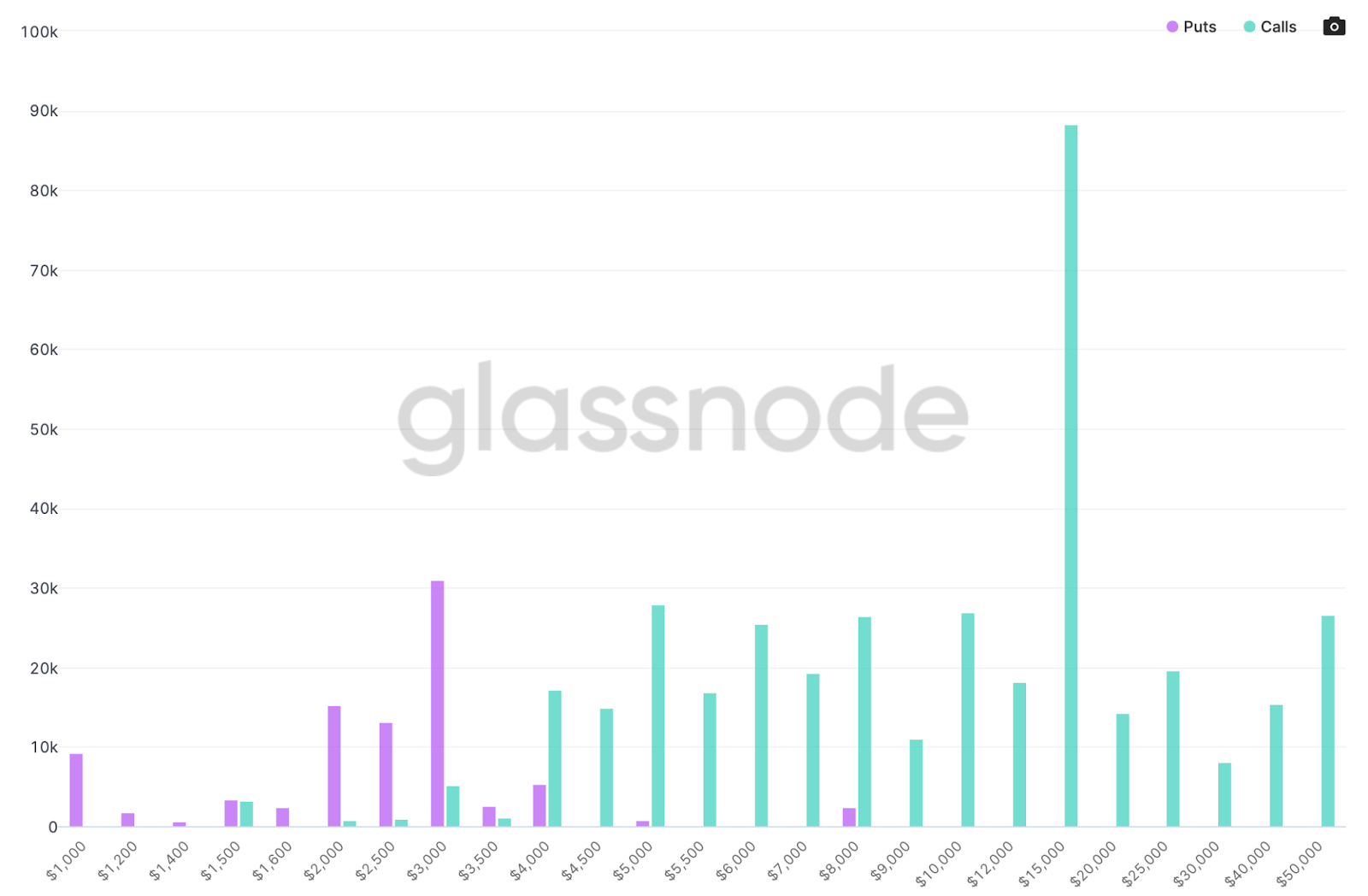

- Out to Mar 25, 2022, there has been significant growth in open interest for 50,000 and 60,000 calls since last week. Emphasis at the 70,000 and 100,000 levels for calls remains. Implied volatility continues its downtrend making bullish plays increasingly attractive.

OI Interest by Strike – Mar 25, 2022

BTC Implied Volatility

- The futures basis curve’s gradual decline continued this week with basis curves in CME dipping into the negatives closing out this week around -1%, and crypto hovering around 5% and -1%. The basis curve across crypto exchanges also declined to approximately 5%. Open interest dropped to lower levels following liquidations during the mid-week break through 45,000.

BTC Futures Annualised Rolling 1 Mth Basis (Deribit & CME)

Bitcoin Futures Open Interest

- Moving forward into 2022, it is expected that participants will build out their Q1 allocation strategies. This should prompt increases in volumes. However for now, with a supply inflow into exchanges, traders are bracing for volatility in the short term. In saying this, keep an eye on the big picture.

Ethereum

- Despite a recent surge in ETH co-founder Vitalik’s social media activity, the price of ETH remained relatively stagnant at the start of the week, setting weekly highs around 3,900. ETH, like the broader market, followed hints from the Fed to trim its balance sheet sooner than expected.

- Bearish pressure persisted for the remainder of the week marking the weekly lows around 3,000, dropping alongside its implied volatility.

- Importantly, the key support level at 3,600 was breached, with the next notable support at the 3,000 and 2,550 regions respectively.

ETH ATM Implied Volatility

- As various L1 and L2 solutions emerged in 2021 to address the scalability challenges with Ethereum, Terra and Binance led the space trending above all other blockchains apart from ETH, with almost $100 billion and $90 billion TVL respectively.

Blockchains by Total Value Locked (TVL) (Delphi)

- As bullish momentum built around Fantom with the launch of several new projects alongside highly desirable yields on stablecoins of around 30-60% APR, the tide shifted at the start of 2022 as Fantom has now overtaken Avalanche in daily transactions.

Daily Transactions on ETH, AVAX & FTM (Delphi)

- Gas fees on Polygon have increased 10x during the last week, with the launch of a new game called “Sunflower Farmers” now consuming about 30% of the gas on Polygon.

- Another L2 blockchain, Arbitrum One, experienced network outages for upwards of 4 hours yesterday, exhibiting the infancy stage of ETH-centric L2 solutions, and presents an opportunity for further competitors to enter the space.

Gas Price on Polygon (Delphi)

- Open interest out to Mar 25, 2022 illustrates heavy emphasis at the 15,000 level for calls, with growth of open interest at 3,000 for puts.

ETH Open Interest by Strike: Mar 25, 2022

- ETHBTC experienced a sharp drawdown following the release of the FOMC minutes, showing BTC’s relative resilience during risk-off events. On-chain data shows a continued supply expansion for ETH on exchanges, as net inflows continue into 2022.

ETHBTC Daily Chart

- On-chain data clearly showing inflows into exchanges, echoing uncertainty in the current moves.

Ethereum Exchange Net Position Change

- Funding rates remained near 0 on aggregate throughout the week, pushing negative today, implying short-term uncertainty amongst traders.

ETH Perpetual Funding Rates

- The futures basis curve consistently declined over the last week, with CME becoming negative towards the second half of the week following the FOMC minutes release.

ETH Futures Annualised Rolling 1 Mth Basis

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,966,003. This represents 7.53% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- Whilst ETH remains as the king of DeFi in TVL and several other areas, if its persistently high gas fees remain unchanged, moving forward the interest in L1 and ETH-centric L2 alternatives may increase even more rapidly. This said, institutional adoption will likely back the most secure, proven incumbent. And given ETH’s roadmap is building to scale further, we still view ETH as holding long-term value. Upcoming short-term price action for ETH will be dictated by popularity of its direct L1 competitors, and whether they’re able to consistently provide faster, cheaper and convenient infrastructure for users and developers, and ss liquidity remains suppressed, BTC may tend to outperform ETH during negative newsflow.

DeFi & Innovation

- AAVE launches Arc, a permissionless lending pool for institutions, with 30 organisations already joining its whitelist – AAVE is part of our DeFi Index Fund.

- China’s central bank releases digital yuan wallet apps for Android.

- OpenSea raises $300 million for encrypted NFT marketplace, now valued at $13.3B.

- Australian Open becomes first grand-slam to join NFTs and metaverse trends.

- Samsung launches a metaverse store on Decentraland, replica from its NYC flagship store.

- Bored Ape Yacht Club crosses $1B in total NFT sales – OpenSea freezes over $2.2 million of stolen Bored Apes.

What to Watch

- Health reports on Omicron, travel restrictions with focus on the US and Europe as Covid-19 surge continues to concern global markets.

- Fed Chair Powell’s testimony on its renomination tomorrow – will potentially discuss rate hikes and current economic uncertainty.

- US’ CPI and Retail Sales, on Wednesday and Friday respectively.

- ECB President Lagarde speaks on Friday, following the Eurozone hitting a new record high for inflation in December.

FAQs

Q: What were the key highlights in the crypto market for the week of 10th January 2022?

A: The key highlights include the Fed’s indication of earlier and faster rate hikes, Bitcoin’s hash rate dropping due to Kazakhstan’s internet shutdown, Goldman Sachs’ prediction of Bitcoin taking a share from gold, and PayPal’s plans to launch a stablecoin. The crypto market saw a sell-off, with BTC returning -11.45% and ETH returning -17.65% week-over-week.

Q: How did the macroeconomic factors affect the crypto market during the week?

A: The Fed’s announcement of multiple rate hikes in 2022 correlated with a sell-off in the crypto market. Other factors such as US job growth coming in below estimates, Euro zone inflation hitting a new record high, and Kazakhstan’s internet shutdown also influenced the market.

Q: What were the significant developments in Bitcoin and Ethereum during the week?

A: Bitcoin faced volatility around the 46,000 mark, with key support at 40,000 and resistance at 46,000. On-chain indicators showed a supply squeeze on exchanges. Ethereum experienced a drawdown following the FOMC minutes, with key support levels breached and a sharp increase in gas fees on Polygon.

Q: What are some notable trends and innovations in the DeFi space?

A: AAVE launched Arc, a permissionless lending pool for institutions. OpenSea raised $300 million for its encrypted NFT marketplace. Samsung launched a metaverse store on Decentraland, and Bored Ape Yacht Club crossed $1B in total NFT sales.

Q: What are the key events and data to watch in the coming weeks?

A: Key events to watch include health reports on Omicron, travel restrictions, Fed Chair Powell’s testimony on his renomination, US’ CPI and Retail Sales data, and ECB President Lagarde’s speech. These events could have significant impacts on the global markets, including cryptocurrencies.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 3 Jan. 2022 0:00 UTC to 9 Jan. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 16 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 10 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 2 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.