Content

- How Does Uniswap V3 Work?

- Why Uniswap V3?

- What Does Uniswap V3 Offer?

- How Does Uniswap V3 Work?

- The Math Behind the Monolith

- A Brief Look at Uniswap V2

- Q Notation and Ticks

- So How Does Uniswap V3 Allocate Liquidity?

- The Symmetry Between Uniswap V3 Positions and Options

- Conclusion

- About Zerocap

- FAQs

- What is Uniswap V3 and how does it work?

- What is the concept of concentrated liquidity in Uniswap V3?

- What are the improvements in Uniswap V3 over its previous versions?

- What are the risks and challenges for liquidity providers in Uniswap V3?

- What is the role of Non-Fungible Tokens (NFTs) in Uniswap V3?

- DISCLAIMER

6 Jul, 23

Uniswap V3: Maximising Capital Efficiency

- How Does Uniswap V3 Work?

- Why Uniswap V3?

- What Does Uniswap V3 Offer?

- How Does Uniswap V3 Work?

- The Math Behind the Monolith

- A Brief Look at Uniswap V2

- Q Notation and Ticks

- So How Does Uniswap V3 Allocate Liquidity?

- The Symmetry Between Uniswap V3 Positions and Options

- Conclusion

- About Zerocap

- FAQs

- What is Uniswap V3 and how does it work?

- What is the concept of concentrated liquidity in Uniswap V3?

- What are the improvements in Uniswap V3 over its previous versions?

- What are the risks and challenges for liquidity providers in Uniswap V3?

- What is the role of Non-Fungible Tokens (NFTs) in Uniswap V3?

- DISCLAIMER

In the rapidly evolving landscape of decentralised finance (DeFi), Uniswap has emerged as the gold standard for decentralised exchanges (DEXs). Built as a public good, the exchange functions as a tool for the community to swap tokens without relying on centralised entities (market makers) to facilitate depth and liquidity. With the release of Uniswap V3 in May 2021, the platform once again raised the bar for DEXs. Packed with new developments aimed at maximising returns and capital efficiency for traders and liquidity providers alike, Uniswap V3 has seen the introduction of a labyrinth of mathematical models designed to deliver on the platform’s promise. These features introduced by Uniswap V3 have solidified its position at the forefront of DeFi, leading the charge to surpass centralised institutions.

How Does Uniswap V3 Work?

Uniswap is designed to provide a decentralised trading experience without relying on an order book. The launch of Uniswap V1 represented a proof of concept for automated market makers (AMMs). The launch of Uniswap V2 optimised this system, leading to the popularisation of AMM-based DEXs. Uniswap V3 iterates upon the success of V2, further optimising the Uniswap AMM and making the platform more flexible as well as efficient for traders and LPs alike. Accordingly, the V3 AMM can be classified as one of the most advanced market makers currently operating on a DEX, providing unprecedented capital efficiency and relatively low slippage. In this article, we delve into ‘what is Uniswap V3’, its groundbreaking features, and its impact on the DeFi landscape.

Why Uniswap V3?

Uniswap V3 emerged as a response to the challenges faced by its predecessors, Uniswap V1 and V2, which were instrumental in shaping the world of decentralised finance. While these earlier versions were innovative and groundbreaking, they also encountered certain limitations that hindered their ability to fully optimise the user experience. Among these limitations were capital inefficiency, slow transaction processing times, and high transaction costs, all of which were exacerbated by the platform’s growing popularity. As the number of users and transactions on Uniswap increased, so too did the strain on the Ethereum network, leading to skyrocketing gas fees and elongated transaction processing times. Recognising these challenges, the development team behind Uniswap embarked on a mission to create a more refined and efficient solution, which ultimately culminated in the development of Uniswap V3.

One of the primary motivations behind the creation of Uniswap V3 was the need to address capital inefficiency and enhance the platform’s security and resilience to code exploitation by competitors. In the case of Uniswap V1 and V2, liquidity was often underutilised, which meant that assets within the pools were not being optimally allocated. This inefficiency limited the potential returns for liquidity providers and led to higher slippage for users. Furthermore, Uniswap V1 and V2’s open-source code made it an attractive target for rival projects such as Sushiswap that aimed to replicate or build upon its success. By reimagining the platform’s AMM model, integrating new features that enhanced capital efficiency, and incorporating new security measures, the team behind Uniswap V3 created a better user experience, culminating in the present US $3 billion TVL.

What Does Uniswap V3 Offer?

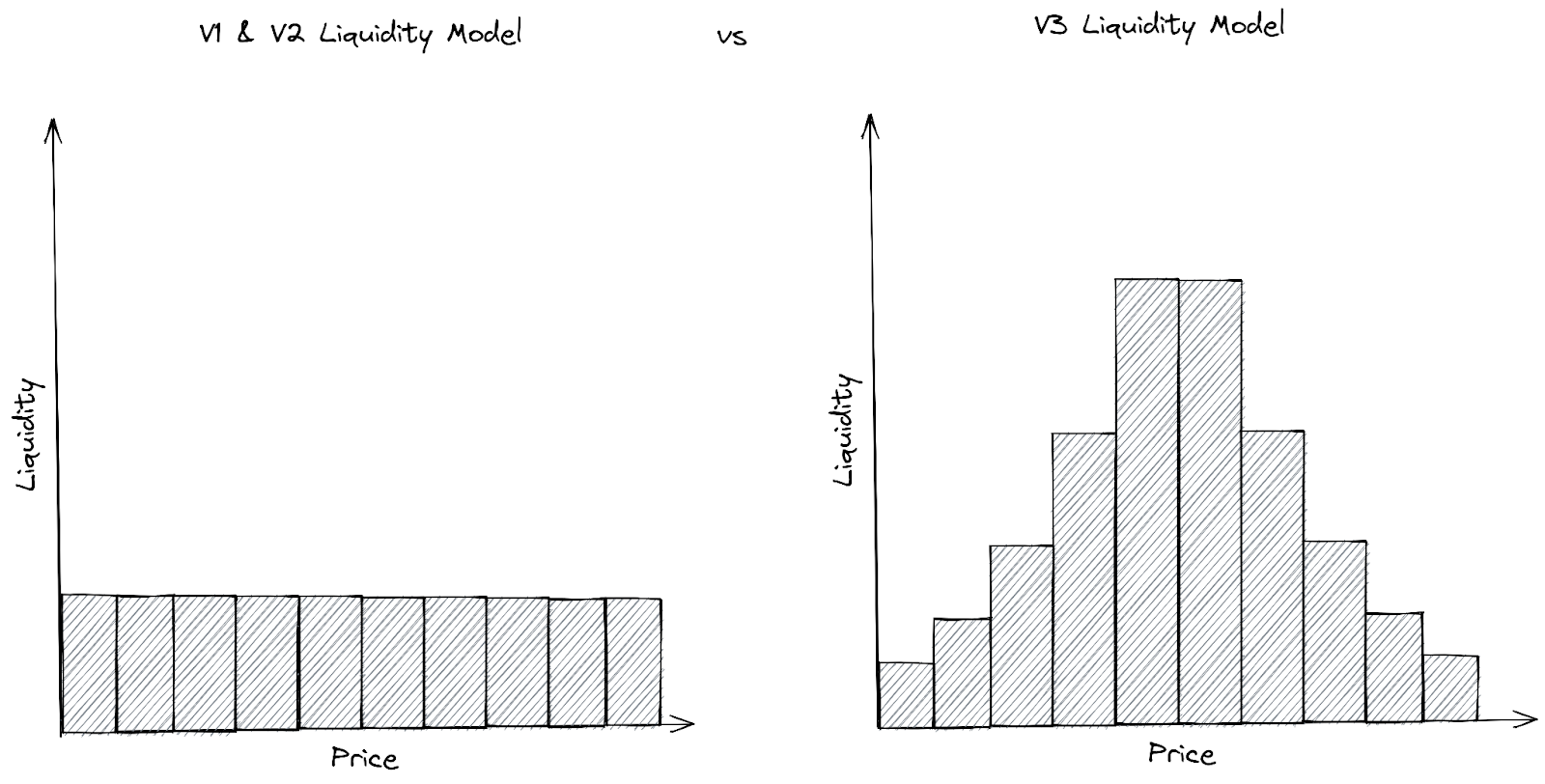

Uniswap V3’s most innovative feature, concentrated liquidity, is a game-changing concept that significantly enhances capital efficiency for LPs. Unlike previous versions, where liquidity was distributed uniformly across the entire price range, V3 enables LPs to allocate their liquidity to specific price ranges, as exhibited in the infographic below. This focused approach allows LPs to create “positions” that act as constant product pools with larger virtual reserves within their specified range, maximising the utilisation of their assets while minimising idle capital. The introduction of non-fungible tokens (NFTs) in V3 further adds a unique touch, as each position now represents an NFT with specific properties. By concentrating their liquidity in narrower bands around the current price, rational LPs can reduce their capital costs and adjust their positions as the price moves to keep their liquidity active. Moreover, this innovative approach allows LPs to have granular control over their risk exposure and tailor their positions to their specific risk tolerance and market outlook.

In addition to concentrated liquidity, Uniswap V3 introduces range orders, which closely resemble traditional limit orders. With the ability to create positions on very small ranges, LPs can convert their liquidity into a single asset once the price crosses the range, effectively executing the limit order. This functionality, however, comes with some caveats, such as the need to withdraw positions once they are crossed and a limit on how narrow a position’s range can be. Nonetheless, range orders provide an additional layer of flexibility for LPs looking to optimise their strategies. Furthermore, range orders can be combined with concentrated liquidity to create sophisticated, multi-layered strategies that enable LPs to take advantage of market opportunities, hedge risks, and efficiently allocate their resources. This powerful combination allows LPs to benefit from both active and passive income streams, tapping into the full potential of decentralised finance.

To accommodate the diverse needs of different token pairs, Uniswap V3 offers multiple pools per pair, each with a distinct swap fee. This architectural change allows for a more tailored approach, addressing the limitations of the uniform 0.30% fee applied to all swaps in V1 and V2. V3 supports pools with three initial fee tiers: 0.05%, 0.30%, and 1%, with UNI governance having the authority to enable additional fee tiers. This customisable fee structure ensures that pools with varying characteristics, such as stablecoin pairs or highly volatile tokens, can optimise their fees for better market performance. For example, pools swapping low volatility assets such as stablecoins may implement the lowest fee tier as liquidity providers are not exposed to price risk and those swapping will be motivated to pursue an execution price closest to 1:1 as they can get. By offering different fee tiers, Uniswap V3 caters to the needs of a wide range of users, including casual traders, arbitrageurs, and institutional investors. The end result is an ecosystem that balances the incentives for liquidity provision and trading, fostering healthy market dynamics and organic growth.

Finally, Uniswap V3 introduces significant improvements to the time-weighted average price (TWAP) oracle. By incorporating accumulator checkpoints directly into the core, V3 eliminates the need for users to track previous accumulator values externally. It also shifts from tracking the sum of prices to the sum of log prices, allowing users to compute the geometric mean TWAP. This change offers a more accurate and reliable price reference for users, reducing the impact of extreme price fluctuations. Furthermore, the introduction of a liquidity accumulator alongside the price accumulator offers valuable information for external contracts implementing liquidity mining on Uniswap V3 or determining the most reliable TWAP among multiple pools for a given pair. These enhancements to the oracle system make Uniswap V3 even more robust and versatile, catering to a wide range of use cases and user preferences, such as on-chain derivatives, lending protocols, and synthetic asset issuance.

How Does Uniswap V3 Work?

To understand ‘how does Uniswap V3 work’, we need to explore its unique features and underlying mechanisms. Delving deeper into Uniswap V3’s inner workings, the constant product market maker formula (x * y = k) remains the cornerstone of the protocol. However, the novel concentrated liquidity and customizable price ranges transform the way liquidity providers engage with the platform. “Ticks” are key components in V3, representing equally spaced price points along the entire price range. Each tick acts as an exclusive range boundary, allowing LPs to define their liquidity range by selecting any two ticks. As swaps are executed, the protocol processes transactions in segments, navigating through available liquidity in each price range and adjusting the reserves accordingly, all the while maintaining the invariant (k). This mechanism ensures that V3 effectively manages liquidity across multiple price ranges, providing both efficient trading and granular control for LPs.

When an LP supplies liquidity within a specific price range, they receive an NFT that represents its unique position. Each NFT contains essential information about the position, such as token pair, price range, and the amount of liquidity provided. NFTs in V3 replace the traditional ERC-20 pool tokens from previous versions, and since each position is unique, they cannot be pooled or traded like their fungible counterparts. The introduction of NFTs in Uniswap V3 as a representation of liquidity positions allows for much more flexible and personalised position management. This opens up opportunities for secondary markets and nuanced risk management. However, this flexibility comes with a greater need for active position management, particularly to mitigate impermanent loss.

Impermanent loss refers to the loss a liquidity provider can experience when the price ratio of the token pair in a liquidity pool deviates significantly from when they deposited their assets. In the context of Uniswap V3, this deviation can lead to liquidity becoming inactive if it falls outside the specified price range, hence increasing the risk of impermanent loss. In Uniswap V3, liquidity providers choose the price range they want to provide liquidity for. If the market price of the token pair moves outside of this range, their liquidity will not be used for trades and will earn no fees, effectively becoming inactive. This could lead to an opportunity cost or even a loss if the market price moves far from the chosen range and does not return before the liquidity provider withdraws their assets. Active position management is therefore crucial in Uniswap V3 to mitigate these risks. LPs may need to frequently adjust their price ranges to keep their liquidity active and to align with market conditions. They may also need to withdraw their liquidity if it is no longer active, to avoid incurring losses.

Uniswap V3 also significantly enhances its native Oracle system, providing users with more accurate and efficient price feeds. The protocol integrates accumulator checkpoints directly into its core, ensuring that external contracts can access TWAP data without requiring any additional external storage. The updated Oracle system calculates the geometric mean of accumulated prices, resulting in more accurate price reference data that is less susceptible to extreme price fluctuations. This system is aided in large part by the aforementioned liquidity accumulator.

The Math Behind the Monolith

The Uniswap AMM is the defining feature of the protocol, relying on its liquidity pools and their associated providers to fill orders. However, with the introduction of Uniswap V3, the AMM has undergone a significant transformation, evolving beyond its origins as a simple x * y = k formula. Instead of allocating liquidity uniformly across the entire price range for each asset in a pool, Uniswap V3 has implemented a more sophisticated approach to optimise capital efficiency. At the heart of this AMM design lies the concept of capital efficiency, which focuses on maximising the liquidity provided while utilising a smaller amount of capital. While the trading experience provided by this system remains user-friendly, the underlying mathematics employed to facilitate this interaction is complex.

A Brief Look at Uniswap V2

Uniswap V2, one of the most successful DEXs of all time, priced assets using the same product algorithm as Uniswap V1, the x * y = k curve, where x and y are the balance of crypto in the pool and k is a constant value. Operating using this algorithm, Uniswap V2 would perform a swap of token x for token y as follows:

y=y-kx+x

Where = change in value

Assuming the swap occurred correctly then the following equation should equate to a constant value:

(x+x)(y-y)=k

The price of each respective token can be calculated simply based on the token swap or their respective pools:

p=yx=yx

While this simple and elegant solution functioned effectively in its intended role as a DEX, it also included a number of inherent inefficiencies, particularly in relation to the liquidity spread. As discussed in prior sections, Uniswap V2 spreads liquidity across prices rather than concentrating it where it is needed most. Since most of the assets in a pool are not contributing to swaps, capital is being allocated inefficiently and higher slippage arises.

Q Notation and Ticks

Before discussing the mathematics behind Uniswap’s liquidity allocation, it is important to grasp the concept of ticks and Q notation is foundational to the Uniswap V3’s implementation of ticks. Q notation is a fixed point arithmetic representation that offers an effective way to handle fractional numbers while maintaining precision and computational efficiency. In traditional fixed point arithmetic, numbers are represented using a fixed number of bits, with a predefined binary point that separates the integer and fractional parts of the number. Q notation builds upon this concept, using the form Qm.n, where ‘m’ represents the number of integer bits and ‘n’ is the number of fractional bits, as demonstrated in the infographic below.

Source: Rounding Algorithms 101

This system allows the encoding of real numbers as integers, making calculations with them more efficient and precise. In the context of Uniswap V3, Q notation is heavily utilised to maintain the necessary precision when performing mathematical operations, such as calculating exchange rates, managing liquidity, and ensuring that the platform’s smart contracts function correctly. Given that Q notation saves storage space, it is better used for representing numbers in solidity, considering the implication of gas.

Uniswap V3 incorporates Q notation in its implementation by utilising variables that end with X96 or X128, which indicate the number of fractional bits in the Q notation. For example, the sqrtPriceX96 represents the square root of the price multiplied by 296, ensuring a high degree of precision. This high precision is essential for Uniswap V3, as it deals with large numbers and complex calculations, which could otherwise result in significant rounding errors and loss of precision. Uniswap V3 maintains this precision by using 256-bit variables, carefully managing the risk of overflow and potential rounding issues. By employing Q notation, Uniswap V3 guarantees that the necessary granularity is maintained, allowing for accurate and reliable calculations.

In addition to ticks, one practical application of Q notation in Uniswap V3 is the calculation of the current exchange rate between two tokens. The exchange rate is crucial information for users and developers interacting with the platform, as it determines the value of tokens being traded. In Uniswap V3, the exchange rate is represented as sqrtPriceX96, which is stored in the slot0 data structure along with most other commonly accessed values. This structure is used to store frequently accessed values, optimising data retrieval and gas efficiency. To calculate the actual exchange rate, the sqrtPriceX96 value must be divided by 296, converting the Q notation value into a standard floating-point number. This number can then be squared to obtain the final exchange rate. Uniswap V3’s utilisation of Q notation allows for the accurate representation and calculation of exchange rates, even when dealing with large numbers and small price differences.

Another aspect of Uniswap V3 that benefits from Q notation is the interplay between tick and tick spacing, which are related to the sqrtPrice. Ticks are foundational in Uniswap V3, with ‘tick spacing’ playing a crucial role in determining liquidity ranges. The tick represents the current price level within a liquidity pool, while tick spacing indicates the minimum price increment between adjacent ticks. By using Q notation, Uniswap V3 ensures that the tick and tick spacing values maintain a high level of precision, allowing for accurate calculations and efficient management of liquidity pools. The efficient handling of ticks and tick spacing is vital to the functionality of the platform, as it directly impacts the incentives for providing liquidity and the distribution of fees among liquidity providers. In this way, Q notation serves as a critical tool for enabling precise mathematical operations within Uniswap V3, ultimately ensuring a robust and reliable platform for decentralised finance.

Ticks are the foundation of Uniswap V3’s model of concentrated liquidity, without which its unprecedented levels of capital efficiency would be impossible. A tick represents a discrete point on the price axis, dividing the price spectrum into uniform intervals. Each tick is assigned an integer index, with the tick spacing determined by the square root price. The square root price is the square root of the ratio between the two assets in a trading pair.

P=x / y

In this equation, ‘x’ and ‘y’ represent the quantities of the two assets in the trading pair. The tick index is calculated using the following formula, where the tick index is equivalent to the floor, or the output of the log rounded down to the nearest integer, of the log of the square root of the price ratio between each asset in the trading pair:

index=floor(log1.0001(P))

By using the logarithm base 1.0001, Uniswap V3 ensures a high-resolution tick spacing, allowing liquidity providers to concentrate their capital within specific price ranges. The price (P) corresponding to each tick is calculated using a simple formula:

P(index)=1.0001index

Source: V3 Core

The tick index’s primary function is to facilitate the allocation of liquidity within specified price ranges. When a liquidity provider stakes their assets in a liquidity pool, they choose a lower and an upper tick, defining the price range within which they will be providing liquidity. Each tick stores the net change in liquidity (ΔL), allowing the protocol to track the liquidity changes across the entire price spectrum efficiently.

When a trade occurs, the protocol must traverse the tick range impacted by the trade, updating each tick’s net liquidity accordingly. Specifically, each trade executed changes the ratio of the two assets in the liquidity pool and potentially alters the square root price. This alteration may cause the price to move across multiple ticks, for each of which the protocol must adjust the liquidity value stored at that tick, thereby maintaining an accurate representation of available liquidity at different price levels. To manage this process efficiently, Uniswap V3 organises ticks in a data structure called a “tick bitmap,” allowing the protocol to quickly identify and update the relevant ticks affected by a trade. This streamlined process minimises the computational overhead, ensuring fast and cost-effective transactions.

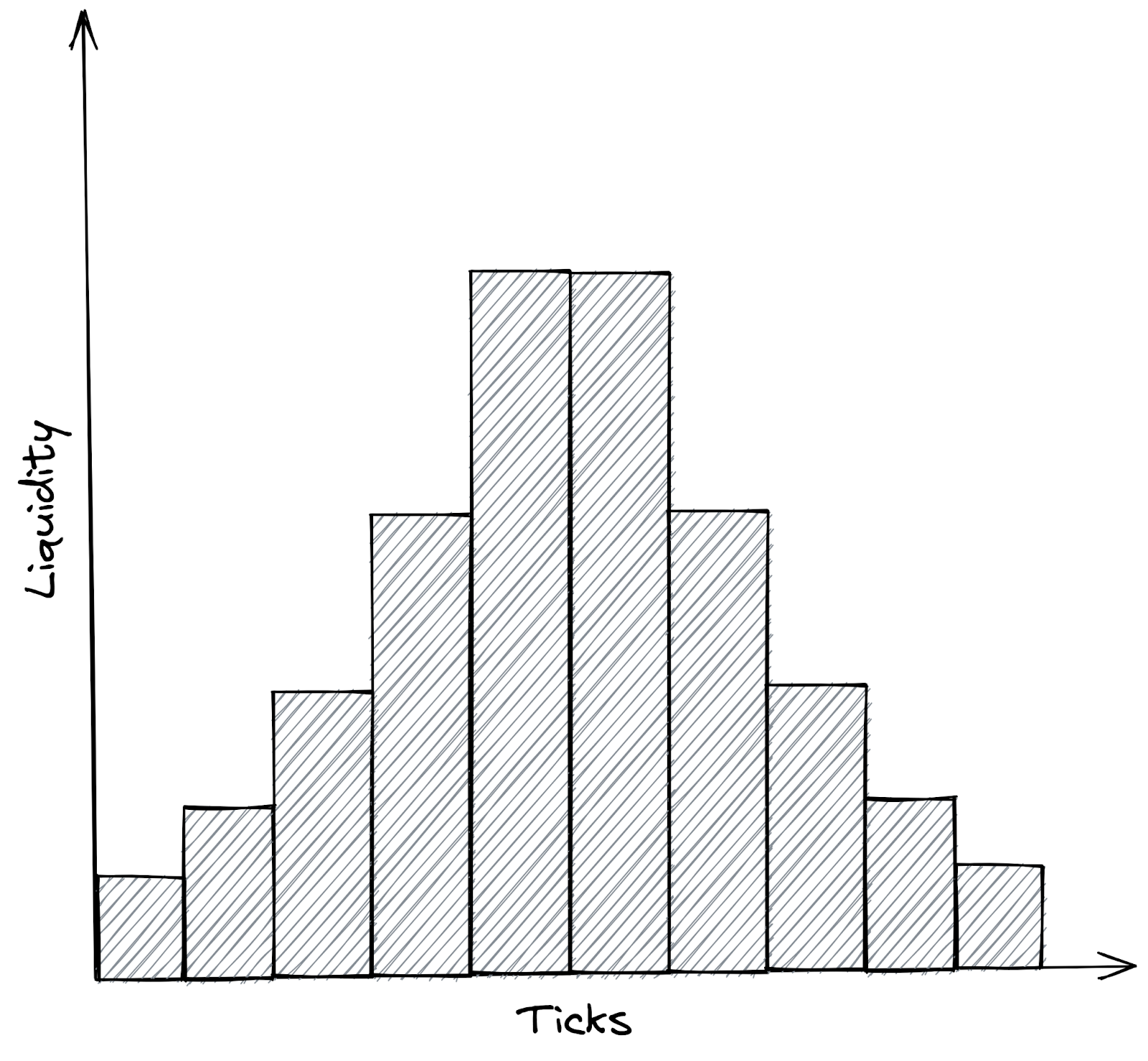

One of the critical aspects of ticks in Uniswap V3 is the virtual price, which represents the effective price considering the ticks and liquidity concentration. The virtual price is calculated by integrating the square root price over the range of active ticks:

virtual price=lower tickupper tickP

This integration considers the concentrated liquidity within the specified tick range, providing a more accurate representation of the effective price at which assets are traded in the liquidity pool. This virtual price calculation is essential for ensuring that the protocol can determine the proper exchange rate for each trade, taking into account the liquidity concentration and the current market conditions. The equation can be visualised in the diagram below, whereby the liquidity in each tick is equivalent to the area under the curve.

So How Does Uniswap V3 Allocate Liquidity?

Liquidity is the fundamental concept in the Uniswap V3 protocol and plays a crucial role in determining the efficiency and effectiveness of the platform. In Uniswap V3, LPs can allocate their capital within ticks, concentrating liquidity and maximising capital efficiency. The liquidity provision process in Uniswap V3 involves staking two assets in a liquidity pool, effectively creating a market for the asset pair.

When an LP provides liquidity within a specific range, they deposit a quantity of each asset, x and y, according to the current pool’s price ratio. The amount of liquidity provided (L) is proportional to the amount of assets deposited, as shown in the following formula:

L=k / (upper tick-lower tick)

Here, k is the constant product of the assets’ quantities, which remains invariant throughout the trading process. The constant product formula ensures that the pool always maintains sufficient liquidity to accommodate trades, albeit with slippage for larger trades. As the price moves within the specified range, the LP’s position earns trading fees proportional to the liquidity provided. The trading fee calculation takes into account the pool’s fee tier, which ranges from 0.05% to 1%, and the LP’s share of the total liquidity within the range. The larger the LP’s share and the higher the fee tier, the more significant the trading fees earned.

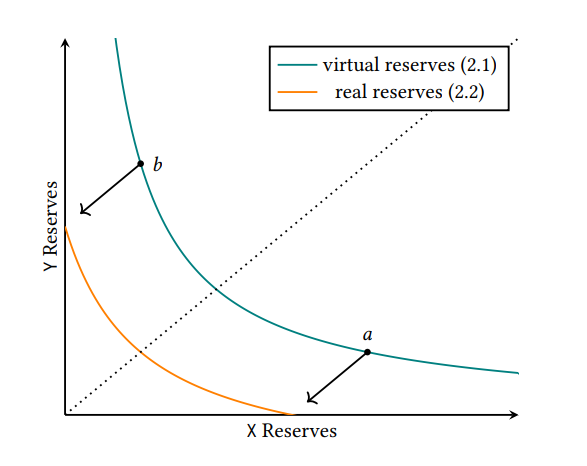

By concentrating liquidity within this range, LPs can optimise the use of their capital and achieve better returns on their investment. This concept, referred to as concentrated liquidity, uses a more complicated implementation of the x * y = k algorithm, with L referring to the virtual liquidity, x and y referring to the reserves of each token in the pool and P referring to the price:

L=xvirtualP = yvirtualP

This equation can be translated onto the graph below, whereby the virtual liquidity (L) is concentrated between points a and b, while c denotes the current price, meaning the pool is maintaining the necessary reserves to cover price movement so that token x and token y cannot be depleted within this specified price range:

Source: V3 Whitepaper

As indicated in the above equation x and y indicate the virtual amounts of tokens, not the real amounts. In order to calculate the real amounts for each token, the following equation can be used, with the additional variables Pa and Pb referring to the lower and upper bounds of a price range respectively:

(xreal+LPb)(yreal+LPa)=L2

This equation shows how the reserves of the two tokens change as the price moves. When the price is within the position’s range (between Pa and Pb), the position is active, and its reserves are determined by both x and y. If the price moves outside of this range, the reserves of one token are entirely depleted, and the position becomes inactive. The equation is expressed in the figure below whereby the position is solvent within the lower and upper bounds of the specified price range:

Source: V3 Whitepaper

In Uniswap V3, the concept of virtual liquidity is introduced to account for the concentrated liquidity within specified price ranges. Virtual liquidity represents the effective liquidity available for trades at the current price, considering the liquidity concentration and active ticks. It is calculated using the following formula:

virtual liquidity=L(current tick-lower tick)(upper tick-current tick)

Virtual liquidity is crucial for determining the actual slippage and price impact of a trade. Since the liquidity is concentrated within specific ranges, the virtual liquidity may be significantly different from the total liquidity provided in the pool. As the price moves closer to the edges of a specified range, the virtual liquidity decreases, potentially resulting in higher slippage and price impact for trades. The relationship between liquidity and trading fees is an essential aspect of Uniswap V3’s design, as it incentivizes LPs to provide liquidity in ranges where it is most needed. In a scenario where the price is close to the edge of a liquidity provider’s specified range, a large trade could cause the price to move beyond that range, leading to an immediate drop in liquidity. This drop increases the slippage for the remaining part of the trade, causing a greater price impact than would be expected in a pool with constant liquidity.

The interplay between liquidity, slippage, trading fees, and price ranges forms a vital component of Uniswap V3’s design. It creates an economic incentive for LPs to supply liquidity where it’s most likely to be utilised, that is around the current price. This is because they earn more trading fees when trades occur within their chosen ranges, compensating them for the potential risk of price volatility. By concentrating liquidity within specific price ranges and allowing LPs to earn trading fees proportionate to their provided liquidity, Uniswap V3 achieves a more efficient use of capital and creates a more competitive trading platform.

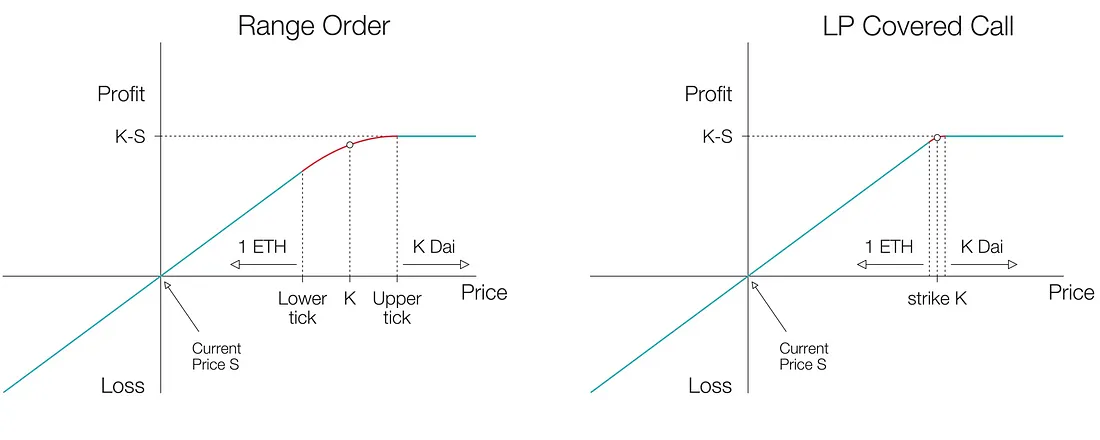

The Symmetry Between Uniswap V3 Positions and Options

As well as the intended benefits of Uniswap’s concentrated liquidity pool design, the NFT LP position feature has a particularly unique unintended outcome; they operate like options. If a LP position is not rebalanced it has a noticeably similar payoff effect to options. In his article, Guillaume Lambert discusses how concentrated liquidity acts as a boundary between which tokens can generate fees, yet outside, the value of the position is entirely traded into one pair. In this way, with relation to the upper and lower bound of the NFT LP position, the payoff structure can be visualised this way.

Source: Guillaume Lambert

However, this appears very similar to the option payoff structure. Discussed further in this article, covered calls are a type of option whereby an investor holds a long position in an asset and simultaneously sells call options on the same asset, generating income from the option premiums. The term “covered” originates from the investor already owning the underlying asset, providing coverage if the call options are exercised, and the asset must be sold. Importantly, the call option lets the owner decide whether to purchase or not purchase the underlying asset.

Source: Guillaume Lambert

In a traditional covered call strategy, the strike price is the predetermined price at which the option can be exercised. Beyond the strike price, the covered call is likely to be purchased when the option expires and subsequently sold to the option writer – in a single asset. The reverse occurs if the strike is never breached or returns below the strike price during which the option was never exercised. In Uniswap V3, the equivalent of the strike price would be the upper bound of the liquidity provider’s position. This upper bound represents the highest price at which the liquidity provider’s assets will be used to facilitate trades, essentially determining the point at which their long position is “called away.”

The underlying asset in a covered call is the asset held by the investor, which is being used to “cover” the sold call options. Likewise, in Uniswap V3, the underlying assets are the tokens in the liquidity pool that the provider has added within the specified price range. These are “covered” in a similar manner to covered calls within the NFT LP position.

In addition, the options premiums in a covered call strategy represent the income generated from selling the call options. With concentrated liquidity AMMs, this income is analogous to the trading fees collected by the liquidity provider within their specified price range. These fees serve as both an incentive and compensation for the risk taken by providing liquidity within that range. By maintaining a position in a Uniswap V3 liquidity pool with defined price bounds, that is, in the money, liquidity providers can essentially replicate a covered call strategy. They benefit from the trading fees generated within their specified price range, while the upper bound serves as the “strike price” at which their long position may be called away. Mirroring this payoff period, when an option is ‘in the money’, it is favourable for the option holder to exercise their right to buy or sell the asset based on the current market price of the underlying token.

Visualising all of these similarities in a payoff structure, the most critical similarity emerges:

Source: Guillaume Lambert

One key and fundamental difference between options in traditional finance (TradFi) and those that leverage the Uniswap V3 liquidity pool design, is that TradFi options expire. At a certain date, the option contract ceases to be valid; this indicates that the option holder loses their right to buy or sell the underlying asset at the specified strike price. In essence, the expiration date serves as a deadline for the option holder to exercise the contract. Conversely, Uniswap V3 positions do not expire automatically; the fees generated are not compounded and the LP does not unlock when the price crosses the tick representing the upper and lower bound.

It is not impossible for options to continue operating – this process is known as “rolling the option” – however, each periodic purchase requires the holder of the option to pay a premium. Further, when the option is repurchased, they are taking on novel risks with respect to the new strike price. The concept of everlasting options foregrounds a structure for options that never expire. Correspondingly, this makes pricing Uniswap V3 positions as options challenging as the traditional Black Scholes model is difficult to apply given a key factor, the time to expiry, cannot be accounted for.

Accordingly, with mastery over the Uniswap V3 concentrated liquidity pools, unique financial instruments, including options and structured products, can be designed – however, they will not expire but rather roll continuously until liquidity is withdrawn. Built upon the application layer that is a dominant DEX like Uniswap, holding over US$4 billion in its contracts, these options can tap into sufficient liquidity to remain decentralised and on-chain. In the DeFi sector, creating fairly priced option trading protocols has necessitated some utilisation of off-chain, and hence centralised services. The existing DApps deployed in this field use market-making bidding wars or capital-inefficient AMMs that most frequently result in LPs incurring severe losses.

Conclusion

Uniswap V3 represents a major leap forward in the world of DeFi, iterating upon the industry standard for capital efficiency and pushing the boundaries of user experience. The platform achieved this via the introduction of innovative features such as concentrated liquidity, empowering liquidity providers with unprecedented control and simultaneously enhancing the trading experience for users through reduced slippage and better price discovery. Enabled via the platform’s AMM from its origins as a simple x * y = k formula to a more sophisticated mathematical foundation. In doing so, Uniswap V3 has solidified its position as the gold standard for DEXs, contributing significantly to the ongoing democratisation of finance and redefining the way users interact with digital assets.

About Zerocap

Zerocap provides digital asset liquidity and custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

FAQs

What is Uniswap V3 and how does it work?

Uniswap V3 is the third iteration of the Uniswap protocol, a decentralized exchange (DEX) built on the Ethereum blockchain. It uses an automated market maker (AMM) system to facilitate trades between users directly from their wallets. Uniswap V3 introduces a novel concept of concentrated liquidity, which allows liquidity providers (LPs) to specify a price range for their liquidity, thereby maximizing capital efficiency. This is a significant shift from the previous versions where liquidity was spread uniformly across all price ranges.

What is the concept of concentrated liquidity in Uniswap V3?

Concentrated liquidity is a feature introduced in Uniswap V3 that allows liquidity providers to specify a price range for their liquidity. This means that instead of their assets being used across the entire price spectrum, they can choose to provide liquidity only within a specific price range. This approach allows LPs to maximize the utilization of their assets and potentially earn more fees.

What are the improvements in Uniswap V3 over its previous versions?

Uniswap V3 introduces several improvements over its predecessors. The most significant one is the concept of concentrated liquidity, which allows LPs to provide liquidity within specific price ranges, thereby maximizing capital efficiency. Additionally, Uniswap V3 introduces range orders, which resemble traditional limit orders, and multiple fee tiers for different types of pools, allowing for more tailored trading strategies. It also enhances its oracle system, providing more accurate and efficient price feeds.

What are the risks and challenges for liquidity providers in Uniswap V3?

While Uniswap V3 offers potential benefits in terms of capital efficiency and fee earnings, it also introduces new risks and challenges for liquidity providers. One of these is the risk of impermanent loss, which can occur when the market price of the token pair moves outside the specified price range. In such cases, the liquidity provided becomes inactive and earns no fees. Therefore, active position management is crucial in Uniswap V3 to keep liquidity active and align with market conditions.

What is the role of Non-Fungible Tokens (NFTs) in Uniswap V3?

In Uniswap V3, each liquidity position is represented by a Non-Fungible Token (NFT) with specific properties. When a liquidity provider supplies liquidity within a specific price range, they receive an NFT that represents this unique position. Each NFT contains essential information about the position, such as the token pair, price range, and the amount of liquidity provided. This allows for much more flexible and personalized position management, opening up opportunities for secondary markets and nuanced risk management.

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

All material in this website is intended for illustrative purposes and general information only. It does not constitute financial advice nor does it take into account your investment objectives, financial situation or particular needs. You should consider the information in light of your objectives, financial situation and needs before making any decision about whether to acquire or dispose of any digital asset. Investments in digital assets can be risky and you may lose your investment. Past performance is no indication of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 10 August 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 3 August 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 27 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.