Content

- Liquidity, Distribution and Price Discovery

- Mining

- Pre-Mining

- Initial Coin Offering (ICO)

- Launchpad

- IEO

- IDO

- Airdrop

- Liquidity Bootstrapping Pool (LBP)

- Dutch Auction

- Fair Launch

- Novel Mechanic: Lockdrop + Liquidity Bootstrap Auction

- Regulatory Concerns

- Conclusion

- About Zerocap

- FAQs

- What is the evolution of token launches in the cryptocurrency industry?

- What are the key considerations for a successful token launch?

- What is a Liquidity Bootstrapping Pool (LBP) and how does it work?

- What is a Fair Launch in the context of token launches?

- What are the regulatory concerns associated with token launches?

- DISCLAIMER

12 Jun, 23

The Evolution of Token Launches

- Liquidity, Distribution and Price Discovery

- Mining

- Pre-Mining

- Initial Coin Offering (ICO)

- Launchpad

- IEO

- IDO

- Airdrop

- Liquidity Bootstrapping Pool (LBP)

- Dutch Auction

- Fair Launch

- Novel Mechanic: Lockdrop + Liquidity Bootstrap Auction

- Regulatory Concerns

- Conclusion

- About Zerocap

- FAQs

- What is the evolution of token launches in the cryptocurrency industry?

- What are the key considerations for a successful token launch?

- What is a Liquidity Bootstrapping Pool (LBP) and how does it work?

- What is a Fair Launch in the context of token launches?

- What are the regulatory concerns associated with token launches?

- DISCLAIMER

Despite the vast number of over 22,900 cryptocurrency tokens, only a small portion of them can truly be considered successful. It can be concluded that successfully launching a token and sustaining its value is no easy task. While traditional startups tend to just focus on building a great product that people want to use; token founders have to balance a fairly distributed cap table, sufficient liquidity and token unlocks, all the while trying to develop a great product. Over the years, the act of launching tokens has evolved towards maturity. Valuable lessons were learnt from the mania of the 2017 ICO bubble and the ecosystem continues to learn through experimentation of different economic designs.

Liquidity, Distribution and Price Discovery

There is no ‘one size fits all’ approach to launching a token. Various different token use cases require different approaches to token launches. However, a common theme between token projects is the aspiration for deep liquidity and fair token distribution which results in positive price discovery. For a token ecosystem to be successful over a sustainable period, it must be widely distributed to a large number of actively engaged users. Without careful consideration of this, the success rate of a token project diminishes significantly over a long period of time. The following research aims to outline the various techniques and mechanics for launching a token.

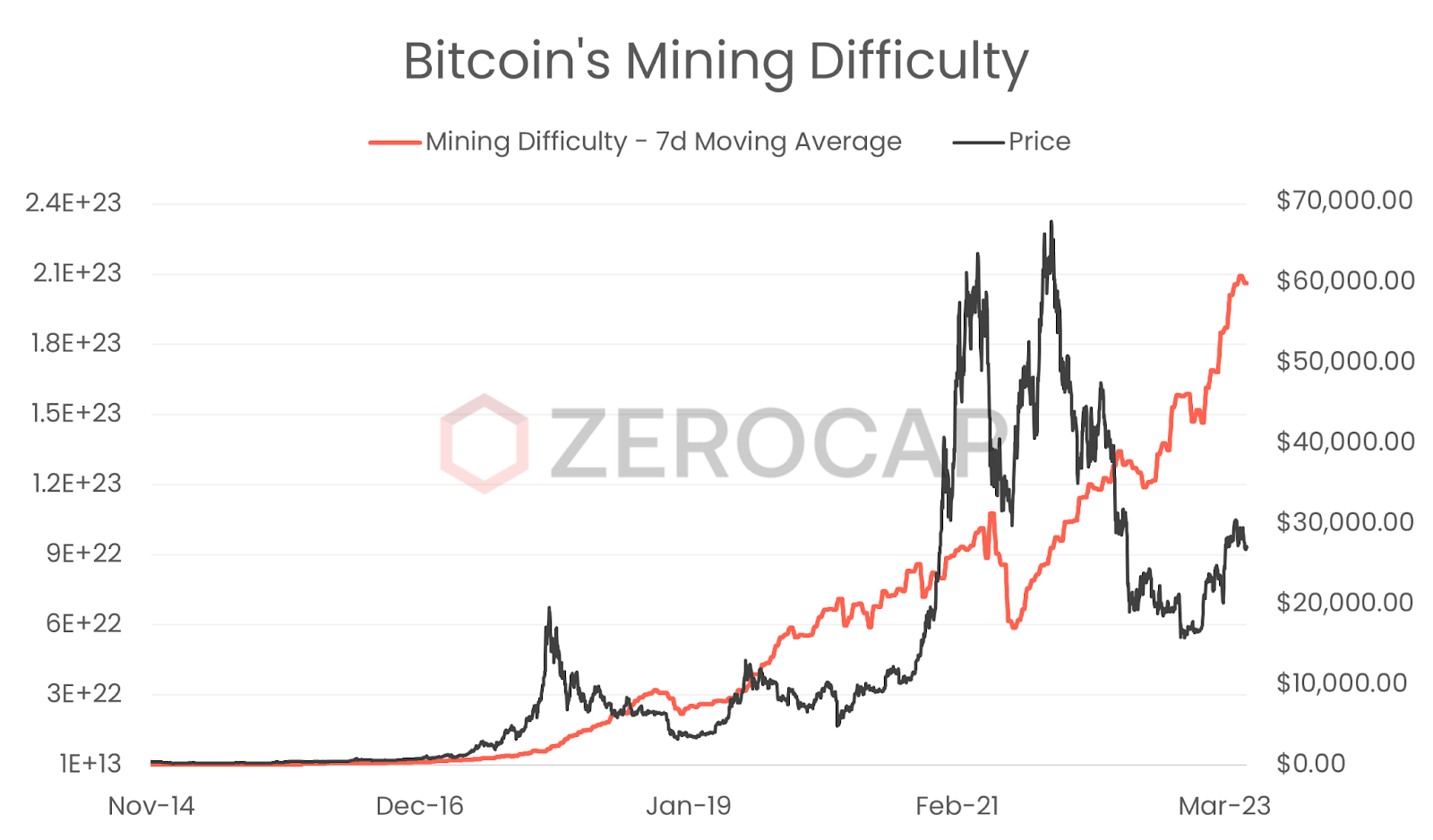

Mining

Mining is the first iteration of token distribution, which was first demonstrated upon the unveiling of Bitcoin in 2008. Mining refers to the Proof of Work (PoW) consensus mechanism. In PoW, network participants, known as miners, must perform a specific amount of computational work to validate and compete for the opportunity to propose new blocks of transactions on the blockchain. To perform the required computational work, miners solve a complex mathematical puzzle by repeatedly calculating cryptographic functions, or hash functions, on a block of transactions until a specific target is met. The first miner to solve the puzzle can propose the next block and earn a reward, usually in the form of cryptocurrency. This process, known as mining, is the key component of PoW consensus.

While miners do not directly purchase cryptocurrency in exchange for another asset, there is still an exchange in value taking place. The act of mining cryptocurrency relies on the fact that miners are expending energy in the form of computing power in order to redeem cryptocurrency. The exchange rate of the cryptocurrency mined can be measured by determining ‘mining difficulty’. A higher difficulty translates to the requirement of more computing power to mine the same number of blocks. The difficulty adjustment is tied to the estimated total mining power depicted in the hashrate chart.

Pre-Mining

Pre-mining was a common practice in the early days of alt-coins such as Litecoin and Tenebrix, used to reward developers despite the fact that the bulk of the work was just a copy/paste of Bitcoin with minimal alterations. Although pre-mining was looked down upon at the time, it is now commonplace to compensate protocol developers with the cryptocurrency they created. Nevertheless, the collective intelligence of the cryptocurrency community has evolved over time, leading to a better understanding of the acceptable levels of token pre-allocation.

Initial Coin Offering (ICO)

The term ‘Initial Coin Offering’, or ICO was created to define the act of raising capital through selling tokens to the public in a fixed price sale. While this term is relatively broad, today’s ICOs are better known as a capital raising event in the form of a token sale, that is hosted on a token project’s own domain and is managed internally by the founding team of the token project. While the first ICO was held by a project called Mastercoin (now Omni Layer) in July 2013, the term was not popularised until 2017 when Ethereum provided additional accessibility of tokens through the development and launch of the ERC-20 token standard. Throughout 2017 an estimated US$ 4.9 billion was reportedly raised via initial coin offerings.

By 2018, it was obvious that the adverse effects of abundant crowdfunded capital through unregulated token sales started to take effect. A report by Status Group highlighted that almost 80% of ICOs conducted in 2017 were scams. Since then, the market has organically approached ICOs with more scepticism, as alternative methods of capital raising such as Initial Exchange Offerings (IEOs) and third-party launchpads have become more standardised given that it is expected for the third parties facilitating token sales have performed sufficient due diligence on the token projects they work with. Additionally, regulatory bodies such as the Securities Exchange Commission (SEC) have been keeping a close eye on the asset class with the aspiration to crack down on malicious activity in the space.

Launchpad

A ‘Launchpad’ is a platform that facilitates the token sale of new crypto assets that are not yet publicly traded. It is expected that shortly after raising capital via a launchpad, the cryptocurrency is expected to be listed on a decentralised exchange (DEX) or centralised exchange (CEX) allowing the asset to reach price discovery based on public supply and demand. Launchpads are generally not permissionless, meaning that in order for a project to be listed on a launchpad, the token project will need to seek the approval of the launchpad platform administrators. For this reason, launchpads act as a trusted third party with the responsibility of conducting a fair token sale event as well as conducting the necessary due diligence regarding the projects offered on the platform. Platforms such as DAO Maker and Polkastarter have gained significant traction in the world of launchpads, being well-trusted due to their history of successful token sales.

IEO

An ‘Initial Exchange Offering’ or IEO is essentially a launchpad that conducts token sales through a centralised cryptocurrency exchange partner. The role of the centralised exchange is to provide an additional level of certification to the offering while additionally driving traffic through their pre-existing user base. The idea is that the cryptocurrency exchange puts its reputation on the line to help facilitate a token sale event. This instils speculators with a level of trust that may be seen as less of a risk as opposed to lesser-known third-party launchpads. The concept of IEOs was popularised in 2019 upon the launch of Binance Launchpad, which fostered successful projects such as Axie Infinity (AXS) and Polygon (MATIC). The reason that a token project might choose to launch a token on a cryptocurrency exchange could be to foster community through the exchange user base, driving awareness for the project and hence demand for the token.

IDO

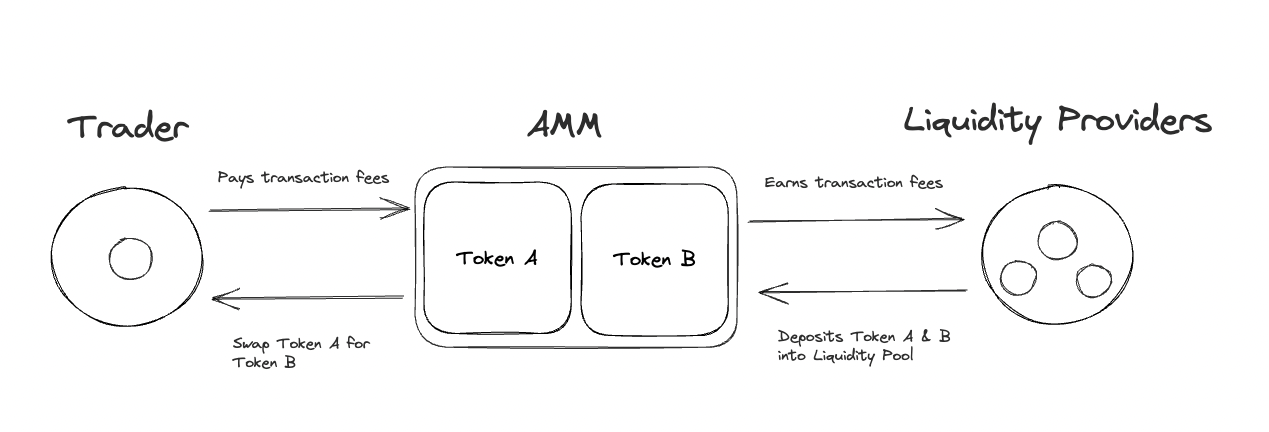

In an Initial Decentralised Exchange Offering (IDO), the token issuer provides liquidity to a DEX, and users can buy the token directly from the DEX using other cryptocurrencies. Automated Market Makers (AMMs) are a core innovation that enables trading within DEXs in a way that doesn’t rely on a centralised order book. They use preset mathematical formulas to discover and maintain the price of digital assets. AMMs work by allowing users to deposit two different cryptocurrencies into a Liquidity Pool (LP) which facilitates liquidity across trading pairs, allowing users to trade freely.

It’s important to understand that IDOs are not a means of directly raising capital, but actually a means of providing liquidity for an asset without the need for a centralised third party. While the primary purpose of an IDO is to distribute tokens to users, the token issuer could also use an IDO to simply provide liquidity to a DEX, without the aspiration to raise capital for the project. If a token project wants to raise capital and launch via an IDO, it will likely look toward utilising a third-party launchpad to facilitate the token sale, creating a liquidity pool on a DEX thereafter the token sale has commenced.

Airdrop

An airdrop is a token distribution strategy that involves issuing free tokens to the public. While some utilise this strategy for marketing purposes, this method is best utilised as a form of community building to appropriately incentivise users to participate in decentralised governance and other forms of token-gated protocol activities. Airdrops do not explicitly aim to raise capital for the project initiating them, the team issuing the tokens is often allocated a portion of the total token supply. As a result of airdropping tokens to the public, a market is created of buyers and sellers and thus liquidity for the tokens, allowing the founding team to sell tokens on the free market as a non-dilutive method of raising capital.

Example: Arbitrum token distribution

Arbitrum, the leading layer 2 blockchain atop Ethereum by total value locked airdropped parties who interacted with the protocol prior to the announcement of the token launch. These parties were airdropped 11.61% of the total token supply in addition to 1.13% of the total token supply being allocated to relevant DAOs in the Arbitrum ecosystem. Controversially, the team proposed to unlock 750m ARB tokens (currently worth roughly one billion US dollars) on the public market. Despite the proposal receiving an overwhelmingly negative response, with 76.67% of token holders voting against the proposal, 50M ARB tokens had already been sent to a sophisticated actor in the financial markets space for the purpose of liquidity provision.

Liquidity Bootstrapping Pool (LBP)

LBPs were created to assist projects launch tokens with low capital requirements. As opposed to launching a traditional liquidity pool which involves a 50:50 balance between trading pairs; liquidity bootstrapping pools are achieved through variable weighting in assets of a pool. The weights are initially set in favour of the project token. For instance, the LBP might open at 5:95 balance and gradually increase with the demand for the token. Over a set period, a gradual flip occurs where the collateral token becomes favoured. LBPs also have the unique feature of being able to pause swapping whenever needed. This allows for more fluid price discovery for the token and makes it harder for whales to profit from sudden price volatility.

For example, a new project can hold a token sale and build deep liquidity by enabling a custom weight/ratio and setting a fee charged by the pool. This makes it easier for everyone else to get in during the course of the sale, as whales are forced to split their trades into separate, smaller trades over a longer period of time. LBPs are a great solution for distributing tokens to a user base without the limitations of a rapidly increasing price curve. They represent the future of fundraising for small projects struggling with liquidity, as they ensure maximum distribution unless people buy tokens faster than the price decreases.

Dutch Auction

Traditionally, the term ‘Dutch Auction’ refers to a type of auction in which an auctioneer starts with a very fairly high price, subsequently lowering the price until someone places a bid. The first bid wins the auction (assuming the price is above the marked reserve price). This mechanism helps in avoiding bidding wars, which is the case with other auction mechanisms, where the price starts low and then rises as multiple bidders compete to be successful buyers. In the context of token launches, Dutch auction mechanics are recreated in the form of a smart contract. Initially used in the context of a token sale by Gnosis in 2016, it is still one of the less common token launch mechanisms. With that said other notable blockchain projects such as Algorand, Gnosis and Polkadot have utilised the Dutch auction mechanic to find the fair market value for their token sale. This method is best utilised when the founding team is confident that the public market is able to make an informed decision about the valuation of the asset they are selling; as opposed to lesser-known startups who might feel more comfortable coming to a valuation on their own terms.

Fair Launch

While many cryptocurrency projects allocate a considerable amount of tokens to the founding team or early investors, a “Fair Launch” aims to distribute tokens transparently and equitably, with no one group having an undue advantage or significant control over the protocol. Generally speaking, the method of acquiring tokens upon the initial token launch event is the same for everyone across the board, including the founding team.

An example of a fair token launch can be seen with Yearn Finance’s token: YFI. Yearn Finance is a DeFi platform that provides a suite of financial products governed by Yearn DAO. YFI token holders can submit, discuss and vote on proposals to change the protocol via the Yearn Improvement Proposal (YIP) process. The YFI token was distributed to parties who participated in a week-long liquidity bootstrapping event where participants received the entire circulating supply totalling 30000 YFI tokens over the liquidity bootstrapping event period. With no further YFI tokens set to be generated, the sole means of acquiring additional YFI tokens became purchasing them on the open market. This resulted in an explosive growth of not only the YFI token value but additionally the total value locked within the protocol and community governance participation.

Novel Mechanic: Lockdrop + Liquidity Bootstrap Auction

The Lockdrop + Liquidity Bootstrap Auction is a novel token lock mechanism developed by Delphi Labs with the focus of distributing tokens to protocol users and reaching fair and sustainable price discovery via liquidity bootstrapping. This mechanism has two phases:

Phase 1 (Lockdrop): This is the distribution phase. The lock-drop phase can be seen as similar to an airdrop but instead of rewarding users for previous actions taken, it instead rewards users for a forward-facing commitment to use the protocol in the future. At the end of the predetermined time window, individuals receive a pro-rata share of the total tokens being distributed based on the size and length of their commitment. The amount of tokens that people earn should be proportional to the value they bring to the token ecosystem. These tokens remain locked until the end of Phase 2.

Phase 2 (Liquidity Bootstrap Auction): This is the price-discovery phase. During this phase, participants who took part in the Lockdrop and wish to be liquidity providers can choose to deposit all or part of their ASTRO into one side of a stablecoin pair, such as the ASTRO-UST, liquidity pool. Other users can then commit UST into this liquidity pool, effectively purchasing ASTRO from Phase 1 participants. At the end of the time period, the following events occur:

- Native tokens and stablecoins are deposited into a liquidity pool.

- The ratio of native tokens to stablecoins determines the final price of the native token.

- Auction participants receive LP shares proportional to their deposits, with the LP shares being locked and vesting linearly over three months.

- Assuming there is enough participation in Phase 2, this ensures immediate, deep liquidity at the market price.

- All tokens given out in Phase 1 that were not committed to the Liquidity Auction in Phase 2 will unlock and become freely tradable.

Regulatory Concerns

Despite facing stringent regulatory scrutiny, the precise regulatory status of token sales remains relatively ambiguous. Gary Gensler, the Chair of the Securities and Exchange Commission (SEC), has previously asserted that “every ICO is a Security,” emphasising the significance of the “security” classification in light of the rigorous regulatory guidelines imposed by securities laws. However, there is currently no official legislation that explicitly prohibits the sale of cryptocurrency tokens through token sales, nor have there been any definitive measures to standardise and regulate Initial Coin Offerings (ICOs) or the process of conducting an ICO. Gensler’s handling of ICOs and cryptocurrencies, in general, has recently drawn criticism from the White House, highlighting the existing regulatory uncertainty surrounding these matters.

In the aftermath of the 2017 ICO boom, regulators around the world have taken a cautious approach towards token launches. One of the key issues in this area is the difference between accredited or sophisticated investors, who are deemed to have the knowledge and experience to understand the risks associated with investing in cryptocurrency, and retail investors, who may not. Token launches have made investment opportunities more accessible and helped create a more inclusive financial system. However, regulatory bodies, such as the SEC, view inclusivity as the root of the problem. This is because their primary concern is to protect retail investors, with the goal of protecting “mum and dad” type investors from losing their life savings on highly speculative investments. On the other hand, they seem to have issues with allowing accredited investors to freely speculate on these types of assets. However, the decentralised and anonymous nature of blockchain technology means that non-compliant protocols may still exist, albeit in a less accessible form. Ultimately, the regulatory status of token launches can have a significant impact on the cryptocurrency market, with clear rules and guidelines helping to promote confidence and stability.

Conclusion

Over time, token launches in the cryptocurrency industry have grown and transformed quickly. It’s evident that this area has experienced significant development. Token generation events such as Mining, Pre-mining, and ICOs were prevalent during the early days. However, as the market changed, new approaches like IEOs, IDOs, LBP’s, and different kinds of auction mechanics emerged. The cryptocurrency ecosystem continues to evolve to these changes and strives for continuous innovation in the field of token launches. Despite the challenges and controversies that have emerged along the way, token launches have helped to democratise access to investment opportunities and have paved the way for a more decentralised and inclusive financial system. However, as with any emerging technology, there is still much room for improvement and refinement.

About Zerocap

Zerocap provides digital asset liquidity and custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

FAQs

What is the evolution of token launches in the cryptocurrency industry?

Token launches in the cryptocurrency industry have evolved significantly over time. The first iteration was mining, demonstrated by Bitcoin in 2008. This was followed by pre-mining, used to reward developers in the early days of alt-coins. The term ‘Initial Coin Offering’ (ICO) was created to define the act of raising capital through selling tokens to the public in a fixed price sale. As the market evolved, new methods such as Initial Exchange Offerings (IEOs), Launchpads, Initial Decentralised Exchange Offerings (IDOs), Airdrops, Liquidity Bootstrapping Pools (LBPs), Dutch Auctions, and Fair Launches emerged. Each method has its own unique characteristics and is suited to different types of projects and market conditions.

What are the key considerations for a successful token launch?

A successful token launch requires careful consideration of several factors. These include deep liquidity, fair token distribution, and positive price discovery. For a token ecosystem to be successful over a sustainable period, it must be widely distributed to a large number of actively engaged users. Without careful consideration of these factors, the success rate of a token project can diminish significantly over a long period of time.

What is a Liquidity Bootstrapping Pool (LBP) and how does it work?

Liquidity Bootstrapping Pools (LBPs) were created to assist projects launch tokens with low capital requirements. Unlike traditional liquidity pools which involve a 50:50 balance between trading pairs, LBPs are achieved through variable weighting in assets of a pool. The weights are initially set in favor of the project token and gradually increase with the demand for the token. LBPs also have the unique feature of being able to pause swapping whenever needed, allowing for more fluid price discovery for the token and making it harder for whales to profit from sudden price volatility.

What is a Fair Launch in the context of token launches?

A Fair Launch aims to distribute tokens transparently and equitably, with no one group having an undue advantage or significant control over the protocol. The method of acquiring tokens upon the initial token launch event is the same for everyone across the board, including the founding team. An example of a fair token launch can be seen with Yearn Finance’s token: YFI.

What are the regulatory concerns associated with token launches?

The regulatory status of token sales remains relatively ambiguous. While there is currently no official legislation that explicitly prohibits the sale of cryptocurrency tokens through token sales, regulatory bodies such as the Securities Exchange Commission (SEC) have been keeping a close eye on the asset class with the aspiration to crack down on malicious activity in the space. The regulatory status of token launches can have a significant impact on the cryptocurrency market, with clear rules and guidelines helping to promote confidence and stability.

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

All material in this website is intended for illustrative purposes and general information only. It does not constitute financial advice nor does it take into account your investment objectives, financial situation or particular needs. You should consider the information in light of your objectives, financial situation and needs before making any decision about whether to acquire or dispose of any digital asset. Investments in digital assets can be risky and you may lose your investment. Past performance is no indication of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 13 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 6 July 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 29 June 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.