Content

- What is InsurAce?

- How Does InsurAce Work?

- How do Claims Work?

- How are Products Priced?

- Advantages of InsurAce

- Disadvantages of InsurAce

- What’s Next for InsurAce

- Crypto Deposit Insurance Scheme

- DAO Governance and Tokenomics Redesign

- ETH2 Slashing Cover

- Conclusion

- About Zerocap

- FAQs

- What is InsurAce and what services does it provide?

- How does the InsurAce protocol work?

- What is the claims process on InsurAce?

- How does InsurAce price its products?

- What are the advantages and disadvantages of using InsurAce?

- DISCLAIMER

18 Jul, 23

Protecting the Unpredictable: A Review of InsurAce’s Decentralised Risk Protection Protocol

- What is InsurAce?

- How Does InsurAce Work?

- How do Claims Work?

- How are Products Priced?

- Advantages of InsurAce

- Disadvantages of InsurAce

- What’s Next for InsurAce

- Crypto Deposit Insurance Scheme

- DAO Governance and Tokenomics Redesign

- ETH2 Slashing Cover

- Conclusion

- About Zerocap

- FAQs

- What is InsurAce and what services does it provide?

- How does the InsurAce protocol work?

- What is the claims process on InsurAce?

- How does InsurAce price its products?

- What are the advantages and disadvantages of using InsurAce?

- DISCLAIMER

Mutuals are an essential component of the global financial infrastructure. Its purpose is to mitigate the risks of unexpected events. Cryptocurrency markets are particularly vulnerable to unpredictable events due to the lack of regulation, the permissionless nature of the technology, and the immaturity of the sector. In 2021, the DeFi sector experienced significant growth while also experiencing occasional implosions, with a total of $1.3 billion USD in exploits that year and over $3.8 billion USD the following year. Despite this, less than 1% of the total value locked in DeFi is covered. This raises the question: why is it socially acceptable to acquire financial protection for your car, house, or life but not your crypto? With that in mind, here we review the InsurAce Decentralised Risk Protection Protocol.

What is InsurAce?

InsurAce is a leading decentralised multi-chain protocol that provides risk protection services for cryptocurrency market participants. The platform offers coverage for 138 different protocols across 20 different blockchains, with over USD $365M total value covered across the entire industry, and a payout track record encompassing the high-profile UST De-Pegging event during the March 2022 Terra Luna crash, the Elephant Money hack, and more recently the FTX exchange collapse. The company was founded by Oliver Xie in November 2020 and funded by Hashed, DeFiance Capital, and ParaFi Capital among many others.

How Does InsurAce Work?

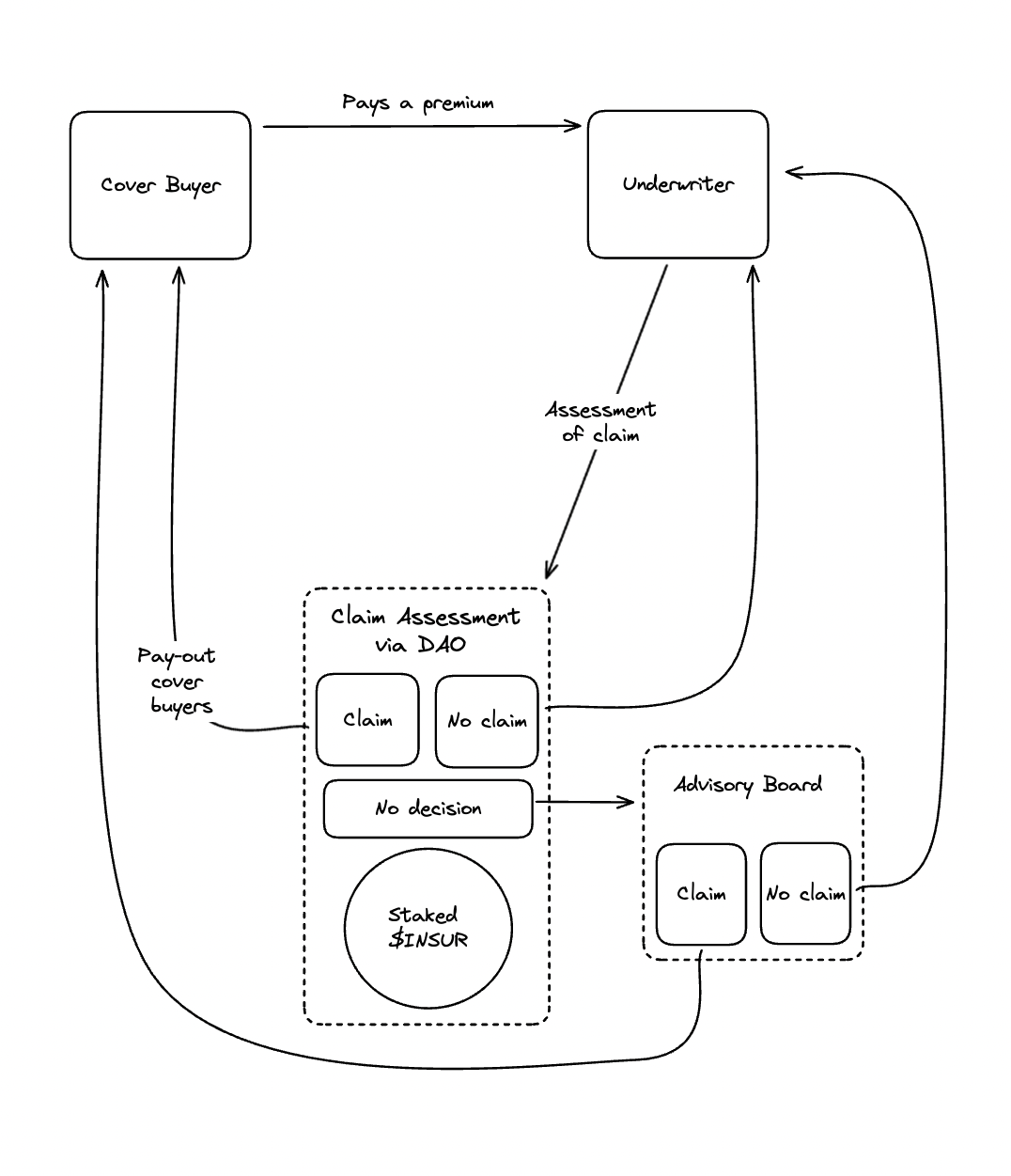

Traditional mutuals offer direct coverage against risks in exchange for a premium. It limits or fully compensates for the cover holder’s financial losses according to the terms of the cover. InsurAce operates as a two-sided marketplace. Users can take on the role of either a cover buyer or underwriter. The cover buyer purchases coverage for specific products and claims compensation when a claimable risk event hits his or her funds. Meanwhile, the underwriter acts as the counterparty to the agreement. To manage risk, the underwriter signs and accepts liability over a pool of products, rather than just one product at a time. InsurAce users can access yields and INSUR token rewards as underwriters by staking their funds on the Mining page and purchasing coverage through the Buy Covers page.

How do Claims Work?

Voting incentives for claims assessments are integrated into the INSUR token design to encourage active participation from token holders in the claims process. The claims process on InsurAce is governed by INSUR token holders who have staked their tokens to be Claim Assessors with voting rights to determine claims. When a claim is filed, the Advisory Board, consisting of external experts and some representation from the InsurAce team, will investigate the claim and draft a payout proposal if the claim is valid. All payout proposals are made publicly available to users. The Claim Assessors can review the details of the Advisory Board’s investigation in the proposal before casting their vote on the proposed payout amount. The results of this transparent voting process are securely recorded on-chain, ensuring a fair and unbiased decision-making process.

In the event of a failed vote due to a lack of quorum or consensus, the Advisory Board can step in to determine the claim. Should a claimant be unhappy with the outcome of a decision by the Claim Assessors, he or she can appeal to the Advisory Board to overturn the Claim Assessors’ decision where applicable and with fresh evidence. Upon approval of payout, funds are deposited into a smart contract which users can withdraw from with the LP tokens distributed by InsurAce to their wallet addresses. Overall, the InsurAce protocol aims to provide a transparent and equitable insurance experience through the participation of its users in the claims process.

Expanding further on the role of the Advisory Board, in addition to the above, this group is also responsible for notifying or updating claimants on the status of their claims through official community channels and ensuring that claim submissions are valid with the necessary evidence, fee payments and deadlines in place.

How are Products Priced?

InsurAce uses actuarial pricing models to assess the expected loss and determine cover prices fairly. This approach evaluates price and risk scores at a portfolio level and incorporates expected losses into each protocol’s risk factors. The Aggregate Loss Distribution model is used to estimate expected loss based on historical data. Dynamic pricing is used to adjust the final price based on supply and demand, with 65% of each product’s total capacity at a constant price and the remaining 35% using a dynamic pricing model. This method minimises overcharging and improves cover provision. In contrast, many competitors use pricing models that are based largely on the value of assets staked on their platform as opposed to actual protocol risk factors, potentially resulting in these platforms overcharging for their covers.

Advantages of InsurAce

Firstly, InsurAce provides competitive pricing through its use of actuarial models to determine cover prices. This approach minimises the potential for overcharging and ensures a fair assessment of expected loss. Adding to this is InsurAce’s shopping basket feature allowing cover buyers to purchase multiple covers in a single session and at a discount. At the same time, cover buyers receive INSUR tokens on a successful purchase.

As a multichain protocol, InsurAce allows users to access cross-chain coverage and secure their assets on multiple blockchain networks. Other benefits of going multichain include lower gas fees on cheaper networks when purchasing covers, as well as accessing and managing covers across various networks. Lastly, the platform aims to provide sustainable returns, offering a long-term solution for users seeking to secure their assets in the blockchain space.

Disadvantages of InsurAce

InsurAce, like other blockchain-based cover providers, faces certain disadvantages that users should consider when evaluating its services. The InsurAce protocol has a security feature called SecurityMatrix which manages access to important functions in the protocol such as asset management and the regulation of protocol-wide operations. While control over the SecurityMatrix is under the InsurAce team at the moment, there are plans to place it under DAO governance in the future. Furthermore, the Advisory Board is currently delegated by the InsurAce team. Although this may again pose some level of centralisation risk, fortunately, the team has plans to delegate Advisory Board appointments to the DAO as well.

Additionally, the platform’s tokenomics may experience considerable sell pressure due to inflationary tokenomics, negatively impacting its overall performance and stability. Moreover, the rapidly evolving and largely unregulated nature of the blockchain market means that there is a risk of regulatory changes that could impact the operation and future of InsurAce. Hence, the InsurAce team is working on addressing these issues and plans to develop a token design that provides sustainable value to its token holders. In the meantime, users interested in using the platform’s services ought to bear these factors in mind.

What’s Next for InsurAce

Crypto Deposit Insurance Scheme

Crypto Deposit Insurance Scheme (CDIS) is an FDIC-inspired and industry lead mutual setup aimed at protecting a fixed amount of users’ deposits on centralised crypto custodial services and exchanges.

DAO Governance and Tokenomics Redesign

The DAO model aims to prioritise the security of capital deposited by underwriters and encourage maximum community participation in the protocol’s governance and development. The governance framework comprises of community voting and an advisory board, with INSUR tokens representing member voting rights. The governance process involves proposal raising, advisory board review, members voting, and execution, all of which are designed to achieve InsurAce’s ultimate goal of building a vibrant protocol that is governed by and for the community. In order to achieve their goals, the InsurAce team intends to introduce a more sustainable token design so as to encourage governance participation from INSUR token holders.

ETH2 Slashing Cover

InsurAce’s ETH2 Slashing Cover is a business-to-business (B2B) product for validator operators of the Ethereum blockchain. It is designed to cater to the ETH staking industry’s need to protect their users’ ETH assets from slashing penalties, all at affordable prices to the validator operators.

Conclusion

The InsurAce protocol offers a unique solution to the problem of uninsured risk in the cryptocurrency industry. Its use of actuarial pricing models, a two-sided marketplace, and voting incentives provides a transparent and equitable experience for users. Additionally, the platform’s multichain capabilities offer users access to cross-chain coverage and sustainable returns. While control over the SecurityMatrix and Advisory Board has yet to be placed under a DAO, it is nevertheless a promising platform with an impressive track record of mitigating unexpected risks in the DeFi space. As the cryptocurrency market continues to evolve, decentralised risk protection protocols like InsurAce may become an increasingly essential component of the global financial infrastructure.

About Zerocap

Zerocap provides digital asset liquidity and custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

FAQs

What is InsurAce and what services does it provide?

InsurAce is a leading decentralised multi-chain protocol that provides risk protection services for cryptocurrency market participants. The platform offers coverage for 138 different protocols across 20 different blockchains, with over USD $365M total value covered across the entire industry. It has a payout track record encompassing high-profile events like the UST De-Pegging event during the March 2022 Terra Luna crash, the Elephant Money hack, and the FTX exchange collapse.

How does the InsurAce protocol work?

InsurAce operates as a two-sided marketplace where users can take on the role of either a cover buyer or underwriter. The cover buyer purchases coverage for specific products and claims compensation when a claimable risk event hits his or her funds. The underwriter, on the other hand, acts as the counterparty to the agreement. To manage risk, the underwriter signs and accepts liability over a pool of products, rather than just one product at a time.

What is the claims process on InsurAce?

The claims process on InsurAce is governed by INSUR token holders who have staked their tokens to be Claim Assessors with voting rights to determine claims. When a claim is filed, the Advisory Board investigates the claim and drafts a payout proposal if the claim is valid. The Claim Assessors can review the details of the investigation in the proposal before casting their vote on the proposed payout amount. The results of this transparent voting process are securely recorded on-chain.

How does InsurAce price its products?

InsurAce uses actuarial pricing models to assess the expected loss and determine cover prices fairly. This approach evaluates price and risk scores at a portfolio level and incorporates expected losses into each protocol’s risk factors. Dynamic pricing is used to adjust the final price based on supply and demand, with 65% of each product’s total capacity at a constant price and the remaining 35% using a dynamic pricing model.

What are the advantages and disadvantages of using InsurAce?

Advantages of InsurAce include competitive pricing through its use of actuarial models, a shopping basket feature allowing cover buyers to purchase multiple covers in a single session and at a discount, and cross-chain coverage. Disadvantages include a level of centralisation risk as control over the SecurityMatrix and Advisory Board is currently under the InsurAce team, and potential sell pressure due to inflationary tokenomics. However, the team has plans to address these issues and place control under DAO governance in the future.

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

All material in this website is intended for illustrative purposes and general information only. It does not constitute financial advice nor does it take into account your investment objectives, financial situation or particular needs. You should consider the information in light of your objectives, financial situation and needs before making any decision about whether to acquire or dispose of any digital asset. Investments in digital assets can be risky and you may lose your investment. Past performance is no indication of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Zerocap Partners with Singapore Gulf Bank to Solve Institutional Fiat Settlement

How Zerocap and Singapore Gulf Bank are solving institutional crypto fiat settlement with real-time USD rails during Asia hours. The Problem With Legacy Settlement Institutional

Weekly Crypto Market Wrap: 30 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

AI Tokens Now Available on Zerocap

Decentralised AI tokens are emerging as one of the most compelling investment themes of this crypto cycle. A new class of blockchain-native protocols has been

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.