Content

- Week in Review

- Winners & Losers

- Macro Environment

- Market Analysis

- BTC/USD

- ETH/USD

- ETH/BTC

- Derivatives

- Ecosystem Highlights

- What to Watch

- DISCLAIMER

- FAQs

- What significant partnerships were announced in the crypto space this week?

- What are the implications of Societe Generale minting a $7 million loan in DAI stablecoin?

- What changes are expected in the Ethereum scaling project Polygon?

- What was the performance of BTC and ETH in the market this week?

- What are some key macroeconomic factors to watch in the coming week?

16 Jan, 23

Weekly Crypto Market Wrap, 16th January 2023

- Week in Review

- Winners & Losers

- Macro Environment

- Market Analysis

- BTC/USD

- ETH/USD

- ETH/BTC

- Derivatives

- Ecosystem Highlights

- What to Watch

- DISCLAIMER

- FAQs

- What significant partnerships were announced in the crypto space this week?

- What are the implications of Societe Generale minting a $7 million loan in DAI stablecoin?

- What changes are expected in the Ethereum scaling project Polygon?

- What was the performance of BTC and ETH in the market this week?

- What are some key macroeconomic factors to watch in the coming week?

Zerocap provides digital asset investment and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets with industry-leading security, contact our team at [email protected] or visit our website www.zerocap.com

Week in Review

- Avalanche (AVAX) partners with Amazon in efforts to bring blockchain technology to enterprises and governments.

- UK prime minister states stablecoins are gateways to Central Bank Digital Currencies – BIS economists suggest using CBDCs to improve traditional finance against crypto.

- Societe Generale mints $7 million in DAI stablecoin, uses housing loan as collateral.

- FTX has located more than $5 billion in cash and crypto.

- Binance states its BUSD lacked USD-backed stability initially, issues allegedly fixed – Binance US receives initial approval to acquire Voyager Digital for $1 billion.

- DCG’s broker Genesis owes creditors over $3 billion – Winklevoss twins and DCG CEO Barry Silbert argue online as fraud accusations pile up.

- Genesis and Gemini charged by US SEC for selling unregistered securities.

- US House Republicans seek to establish crypto-focused subcommittee.

- Polygon undergoing hard fork tomorrow to reduce gas fees and improve performance.

- Frankfurt, Germany has the largest city-wide distributed network of Bitcoin nodes.

- FED may make unpopular decisions to stabilise prices – “[The FED]” is not, and will not be, a ‘climate policymaker’,” stated Chair Jerome Powell.

- US inflation retreating as consumer prices fall, labour market still faces challenges.

- UK’s monthly GDP shows surprising 0.1% growth – recession still seen as inevitable.

Winners & Losers

Macro Environment

- Despite Monday’s rocky open taking much of the steam out of Friday’s Non-Farm Payroll equities rally – risk-on market sentiment continued to permeate through broader markets. Analysts were cautiously optimistic, juggling the prospects of a cooling global economy with the risk that the FED maintains the use of restrictive monetary policy – Money markets moving on Monday to price in a 77% chance for the United States Federal Reserve (US FED) to put forward a lesser 25 basis point hike in the February FOMC meeting.

- Oil was a standout performer amongst commodities last week due to a much anticipated, yet delayed response to China’s recent reversal of its Zero COVID policy. The policy reversal saw the resumption of mainland tourism, coinciding with news of Pfizer-China negotiations for a generic version of its COVID-19 vaccine, easing fears of further lockdowns. Crude oil prices climbed steadily upwards throughout the week, WTI and BRENT cemented weekly gains in excess of 8%. GOLD showed strength back above the 1,900 mark with a weekly maximum of 1921.86, however paled in comparison to Copper – up over +6% WoW.

- US CPI data came out at par with market expectations, having slowed for a sixth consecutive month to +6.5% in December, following a +7.1% reading in November. The energy index experienced a decline of 4.5%, building upon the 1.6% decrease seen in the previous month. This trend was primarily driven by a 9.4% fall in the gasoline index. On the other hand, the index for natural gas exhibited an upward trend, increasing by 3.0% after decreasing by 3.5% in November. Over the past 12 months, the index for all items less food and energy has seen an overall increase of 5.7%. A significant contributing factor to this increase was the shelter index, which rose by 7.5% over the last year. This accounts for more than half of the total increase seen in all items less food and energy.

- Positive CPI results and almost uniformly better-than-expected bank earnings pushed markets higher, and the dollar (DXY) lower into the weekend. The S&P 500, and NASDAQ 100 returned a healthy 2.67% and 4.82% WoW, with Asian markets experiencing similar momentum – the Hang Seng and Nikkei 225 each climbing 3.56 and 1.16%.

Market Analysis

BTC/USD

- BTC entered the week in a relatively conservative manner, edging higher yet remaining confined below topside resistance placed at 17,500. An influx of bids on Wednesday initiated a move above 18,000 with the upper band of a descending wedge drawn from August 2022 highs temporarily slowing BTC’s ascension. However, soon after and alongside growing positive sentiment, BTC rode momentum higher until it encountered resistance at the 21,000 level, a level we can expect to hold relevance into the short term. BTC closed +21.96% WoW, its best weekly return since February 2021.

ETH/USD

- In a similar fashion, ETH initiated last week’s action with an inclination toward the bulls. However, until late Wednesday ETH struggled to find bids above the 1,332 level, the top of the 2018 bull run. In tandem with BTC, ETH pushed higher halting prior to weekly resistance placed at 1,610. Into the weekend ETH remained range bound with bids lacking above 1,560 and the 1,525 level forming as downside support. ETH returned 20.44% WoW and we can expect sideways action with eyes set on a re-test of the 1,610 resistance.

- Early on, speculation on favourable U.S. inflation data, which would allow the Fed to slow the pace of interest rate hikes, saw bond yields fall and equities lift higher with BTC and ETH following suit. Soon after, any doubts surrounding the move higher were put to rest with U.S. inflation data coming in better than expected. High beta assets, such as BTC and ETH promptly ascended higher.

- Outside of the macro, Galaxy Digital Holdings CEO Mike Novogratz stated his expectations that the issues facing DCG and related companies will fizzle out over the next quarter and will pose a minimal impact on price action. Additionally, El Salvador passed a landmark crypto bill that provided the legal framework for a Bitcoin-backed bond. A continuation of diminishing fears surrounding DCG, paired with continued institutionalisation ultimately fairs well for near-term price action.

ETH/BTC

- Coming off ETH’s prior week’s outperformance, which resulted from building anticipation regarding ETH’s Shanghai upgrade, ETH/BTC shifted lower last week. The downward move represents a rare breakdown in the pair’s historical behaviour of ascending during periods of risk-on and diminishment in periods of risk-off. Notably, having already accounted for some gains, Ethereum’s recent move higher may pose an explanation for BTC’s outperformance last week.

- Nonetheless, the pair continues to respect an ascending triangle pattern drawn from June’s lows. In the presence of continued risk-on appetite and a reversion to the pair’s historical behaviour, we’ll likely see action ascend higher into the short term with the 0.07575 level acting as topside resistance.

- Off the back of last week’s positive move, a notable percentage of supply moved into profit. Notably, since the start of this year, 13% of all circulating supply has moved back into profitability. While this significant shift may mark the move from market capitulation to a new stage of the current market cycle, it may also suggest some short-term profit-taking.

- Alongside an easing macroeconomic outlook is growing anticipation surrounding Ethereum’s Shanghai Upgrade, scheduled for March 2023. Toward the latter parts of 2022, this metric increased significantly due to anticipation surrounding the upgrade and as participants moved funds off the exchange following FTX’s collapse. Recently, however, this metric has halted its ascension and even decreased following last week’s price action. This is indicative of some participants taking profits and potentially forms precedence for behaviour we can expect in the lead-up to the Shanghai upgrade.

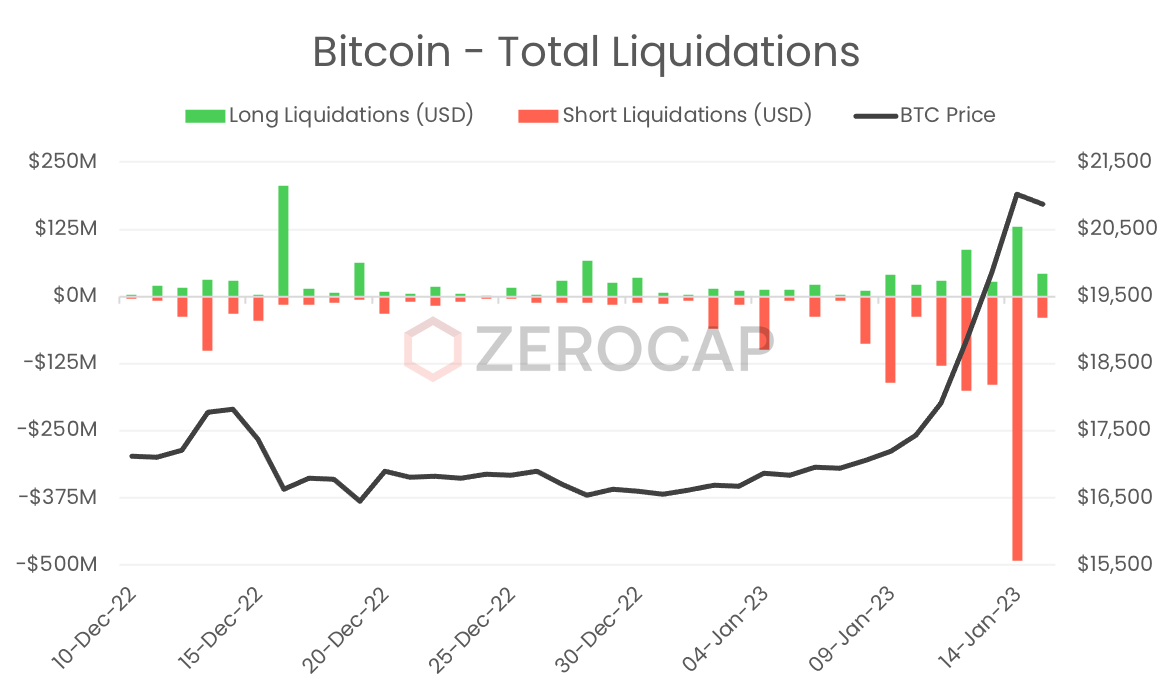

Derivatives

- On Saturday, alongside Bitcoin’s surge in value was the forced and significant closure of a number of short futures positions. Nearly $500m USD of shorts were liquidated on Saturday alone which boasts a similar figure to that seen during FTX’s collapse.

- The difference in implied volatility (IV) between out-of-the-money (OTM) put and call options for Bitcoin, measured by the 25-delta skew, has dropped to its lowest point in over a year. This metric can be useful in identifying overall market sentiment and trading activity which influences the current price of Bitcoin. The recent shift in skew below zero is due to put options being priced lower than call options and can be viewed as a positive change in the overall structure of the options market for Bitcoin.

- A less-hawkish outlook induced risk-on appetites across risk assets with BTC and ETH being primary beneficiaries. Moreover, newsflow specific to the digital asset space such as diminishing concerns surrounding DCG and continued institutionalisation outlines continued development and potentially promotes positive price action in the short term. While some on-chain metrics suggest a transition at play in the market cycle, other metrics suggest the possibility of profit-taking in the near term. Additionally, off the back of last week’s action we saw historically significant liquidations in the futures market and a healthier option market structure. In tandem with a less hawkish outlook, participants are now strongly pricing in a 25bp hike during February’s interest rate decision. However, we can expect macroeconomic expectations to dictate price action with any notable changes resulting in increased volatility.

Ecosystem Highlights

- Avalanche (AVAX) has announced a partnership with Amazon Web Services (AWS) that will allow developers to launch Avalanche nodes directly within AWS to support their decentralised apps (dApps). Ava Labs, the Avalanche development studio, is now part of AWS’ member network and AWS Activate, giving the Avalanche platform access to over 100,000 partners in 150 countries. The partnership has caused a spike in the AVAX token, with a 38.96% increase WoW.

- Ethereum scaling project Polygon has announced a proposed hard fork to its proof-of-stake blockchain, set to take place on January 17, 2023. The fork aims to address gas spikes and chain reorganisation issues by making adjustments to how it sets gas fees and reducing the amount of time it takes to finalise a block to verify successful transactions. The first change involves smoothing out spikes in gas prices, while the second proposed change addresses reorgs by reducing the amount of time it takes to finalise a block and shortening the “sprint length” from 64 to 16 blocks. The fork was first introduced to the Polygon community in December 2022.

- Ethereum layer-2 rollups Arbitrum and Optimism have seen a rise in daily transactions and active users over the past few months, while Ethereum is seeing a slight downtrend. The increase in activity can be attributed to the development of these ecosystems, including the Nitro upgrade of Arbitrum and the recent launch of new projects on the network. Additionally, the DeFi protocols on these networks such as GMX, Perpetual Protocol and Velodrome are driving the adoption of these chains.

- Societe Generale, a French multinational investment bank, has minted a $7 million loan in the form of stablecoin DAI on the MakerDAO platform, using tokenized home loan bonds as collateral. This is one of the first examples of how traditional financial firms can leverage decentralised finance (DeFi) as a new source of borrowing in a simple and efficient way. The bank’s digital asset-focused subsidiary, Societe Generale–Forge, was added to MakerDAO’s vault last August and given a credit limit of $30 million in DAI. SG-Forge has an additional $23 million in funds that it can borrow, which means that the debt position is overcollateralized with a 10 million euro buffer.

What to Watch

- China’s quarter GDP, on Monday.

- Bank of Japan’s outlook report and UK’s CPI, on Wednesday.

- US’ retail sales and change in price of goods and services report, also on Wednesday.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice,take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

FAQs

What significant partnerships were announced in the crypto space this week?

Avalanche (AVAX) announced a partnership with Amazon Web Services (AWS) to support the development of decentralized apps (dApps). This partnership has given the Avalanche platform access to over 100,000 partners in 150 countries.

What are the implications of Societe Generale minting a $7 million loan in DAI stablecoin?

Societe Generale, a French multinational investment bank, minted a $7 million loan in the form of stablecoin DAI on the MakerDAO platform, using tokenized home loan bonds as collateral. This is one of the first examples of how traditional financial firms can leverage decentralized finance (DeFi) as a new source of borrowing in a simple and efficient way.

What changes are expected in the Ethereum scaling project Polygon?

Polygon, an Ethereum scaling project, has announced a proposed hard fork to its proof-of-stake blockchain. The fork aims to address gas spikes and chain reorganization issues by making adjustments to how it sets gas fees and reducing the amount of time it takes to finalize a block to verify successful transactions.

What was the performance of BTC and ETH in the market this week?

BTC had its best weekly return since February 2021, closing at +21.96% WoW. ETH also had a positive week, returning 20.44% WoW. The upward trend in these cryptocurrencies was driven by a less-hawkish outlook and diminishing concerns surrounding DCG, among other factors.

What are some key macroeconomic factors to watch in the coming week?

The article suggests keeping an eye on China’s quarter GDP, the Bank of Japan’s outlook report, UK’s CPI, and US’ retail sales and change in price of goods and services report. These factors could potentially influence the crypto market.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Weekly Crypto Market Wrap: 16 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 10 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 2 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.