Content

- What are CLOs?

- Where the CLO bubble issue lies

- How it affects you

- CLOs vs CDOs - The 2008 global financial crisis market collapse

- How COVID-19 affects the CLO bubble

- FAQs

- What are Collateralized Loan Obligations (CLOs) and How Do They Work?

- What is the Current Issue with the CLO Framework?

- How Does the CLO Bubble Affect the Global Economy?

- What is the Difference Between the Current CLO Bubble and the 2008 Global Financial Crisis?

- How Does the COVID-19 Pandemic Affect the CLO Bubble?

11 Nov, 20

The CLO Bubble – Global Financial Crisis of 2008 has a new name

- What are CLOs?

- Where the CLO bubble issue lies

- How it affects you

- CLOs vs CDOs - The 2008 global financial crisis market collapse

- How COVID-19 affects the CLO bubble

- FAQs

- What are Collateralized Loan Obligations (CLOs) and How Do They Work?

- What is the Current Issue with the CLO Framework?

- How Does the CLO Bubble Affect the Global Economy?

- What is the Difference Between the Current CLO Bubble and the 2008 Global Financial Crisis?

- How Does the COVID-19 Pandemic Affect the CLO Bubble?

Similar to the CDOs (Collateralized Debt Obligations) that helped to bring about the global financial crisis of 2008, CLOs (Collateralized Loan Obligations) have been quietly brewing beneath the surface. In this article, we cover how the current CLO bubble is growing, what caused it and how digital assets are a reliable haven to bring financial sovereignty into the hands of the people, rather than centralised banking authorities.

What are CLOs?

A CLO is a financial process to gather loans to many different companies in a single package, which is then leveraged and resold to several creditors under different rates. The goal is to make the financial system more efficient, overcoming the incompatibility between the diverse needs of mutuaries and creditors. CLO enhances the complexity of the market, much like the Collateralized Debt Obligations (CDO) that contributed to the 2008 crash. In theory, a CLO only involves commercial loans. Still, there are similar frameworks that combine different forms of loans, such as titles and mortgages.

The CLO was adopted in the same way as most frameworks in the market; by offer and demand. That’s because some debtors are more willing to pay than others. Banks who adopt CLOs are also inclined to agree to riskier loans if they can charge higher fees. At the same time, more conservative firms favour lower costs resulting in a more certain return on loan. Before the CLO, most of the global economy believed that the loan market was not sustainable. The task of creditors to always find appropriate loans to match with millions of individuals and businesses safely seemed like a very complicated and inefficient process.

Even with the necessary funds available to pay back the loans to all creditors, the money was not getting to where it was needed. The system was too complicated to negotiate thousands of individual loans; all analysed separately. That led to the development of the CLO where several different loans, from safe to risky, are compiled in packages. Creditors buy the rights to receive a share of the payments from all debtors, with the shares determined according to how much risk they’re willing to take. Suppose one of the debtors involved in a CLO fails to pay the loan, the loss deducts from the share attributed to the creditor who took the most significant risk. As more loan takers fail to pay their loans, the creditor might end up with no shares as the remaining losses transfer to creditors who took lower risks.

The first CLO contracts were established in the late 1980s, along with other forms of securitisations, as a way for banks to package loans and supply companies with a record of investment and their associated risks. Since then, the risk has become riskier and the classification for those risks, unreliable. But if CLOs have been around for nearly thirty years, what has caused them to become so dangerous in recent times?

Where the CLO bubble issue lies

Although CLOs were created as a strategic way to incentivise simple investments on loans, the long-term issue about the CLO framework is that it enhances the complexity of the loan system, making it difficult for big banks to follow the amount of risk introduced through those loans. Rating agencies such as Moody’s and S&P advise creditors about investment risks, classifying a certain CLO as safe because the loan takers involved are considered safe; triple-A companies with a reliable growth history, for instance. Those classifications have become increasingly less trustworthy throughout the years as both creditors and rating agencies have taken more significant risks with CLO packages, as they can provide much higher interest fees but lower chances of payment. The risky trend has resulted in a high rate of loan defaults. It is estimated that more than $US800 billion (as reported in 2019) is at risk within the CLO model, which with COVID-19 we expect this figure to surpass $US1 trillion.

Here is a typical example of the CLO problem in action: let’s say a creditor is looking to invest in the American market. The US treasury as of 2020 currently has a meagre return of about 2%, which is not ideal for investors that are willing to take some risks, especially for companies with limited liquidity to invest and turn a profit. The current CLOs, on the other hand, can range from 3% from triple-A-rated loans or even up to 13% for the riskiest ones. It depends on how much the companies are willing to risk on the investments. Based on the current debt, the willingness is relatively high. After the company settles on a particular setup, the creditor agrees on the loan which should be paid under an interest rate matching the profile of that company.

The problem with this setup revolves around two main factors. Not only are CLOs given to troubled businesses which no longer qualify for traditional banking loans, but offered to insolvent companies; businesses who are classified as unable to pay loans in time. That is usually defined through the company’s liabilities exceeding its assets or if their net assets are negative. Basically, creditors are offering loans to those who evidently cannot afford them. Not only is the setup doomed to crash, but some of the world’s most influential banks are heavily exposed to varying levels of CLOs.

A December 2019 report from the Financial Stability Board estimated that the 30 biggest banks in the world have an average of 60% exposure to leveraged loans, providing unregulated loans to distressed companies. Banks in the US, EU, UK and Japan combined an exposure to leveraged loans of roughly US$1.4 trillion as of January 2019. According to the report, such disclosure is mostly from large direct holdings, and its impact on the banks will depend on whether banks have prepared for a severe downturn in their leverages. Indirect CLOs can also affect their liquidity since a significant portion of contracts executes through funding facilities for under triple-A investors.

How it affects you

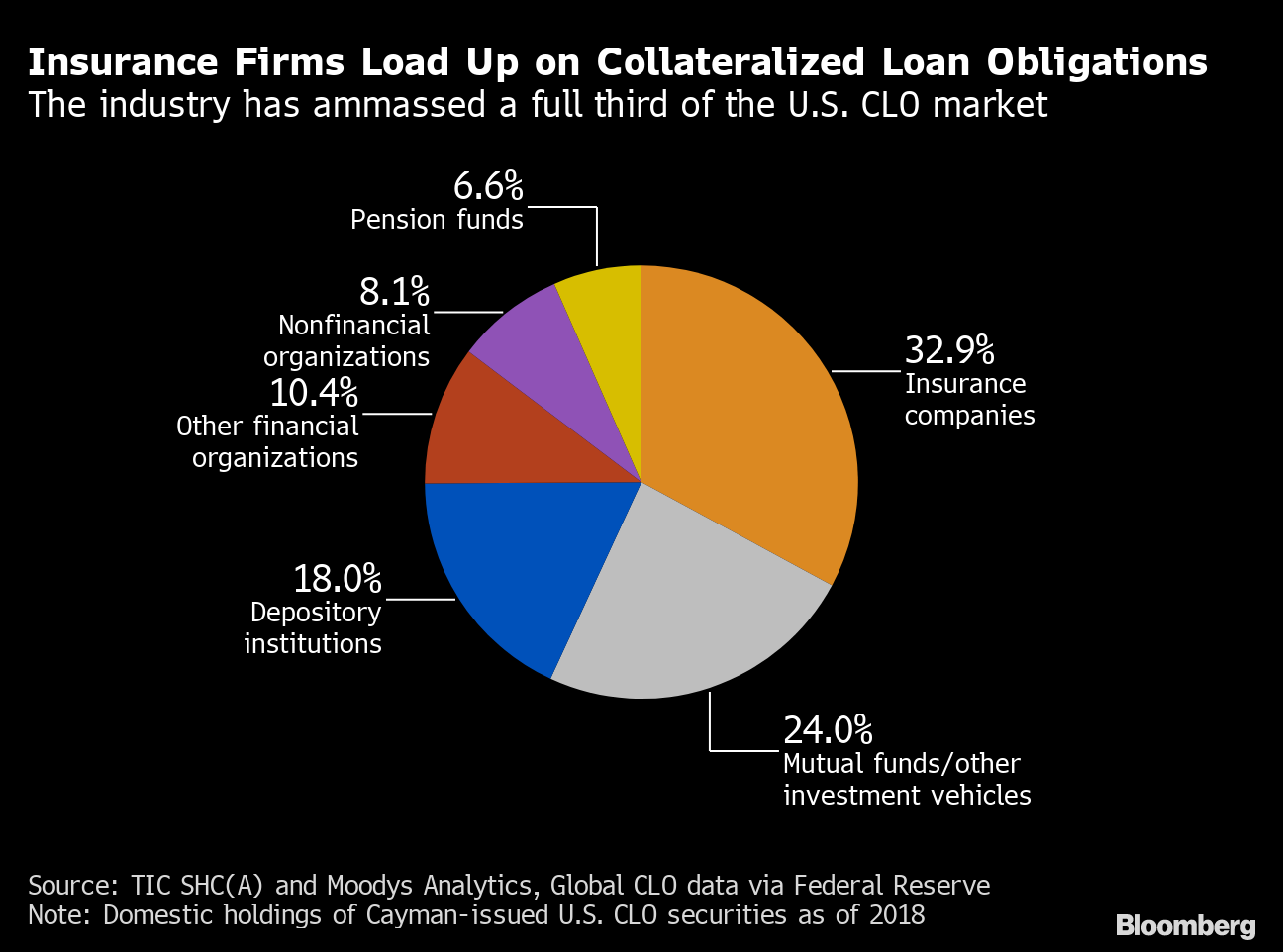

So who will suffer from a downturn in the CLO bubble? Although the 30 biggest banks in the world economy have over half of their assets exposed to leveraged loans, the official direct exposure to collateralized loan obligations does not seem worrisome. A June report from S&P Global Market states that out of the US$700 billion in American-issued CLOs, bank holdings reached US$98.8 billion in the first quarter of 2020, just a bit less than Q4 2019’s US$99.5 billion. The biggest holder of direct CLO leverages in banking is JP Morgan, with 1.3% of its US$2.69 trillion in assets invested in the loans. The banks will not be the ones to suffer the most from a contraction in the system, but rather the investors themselves, mainly pension funds, hedge and mutual funds, also bringing the ripple effects onto the market participants rather than the centralised bank loan providers. An S&P report from late 2019 show that bank-owned CLOs represent merely 15% of the total US-issued market, while the rest is held mostly by insurance companies (20%), asset managers (30%) and the remaining 35% splits into mutual funds, depository institutions, pensions and non-financials.

The latest Federal Reserve report on CLO accounts for securities where insurance companies represent the largest share of the holdings; 32.8%. The 2020 S&P report on the issue estimates that out of all insurance company holdings, 68% are rated AAA to BBB while 32% have not been rated, almost a third of all securities. As the loans become riskier and more debt accumulates, the downturn is an inevitable matter of time. We recognise that even digital assets, an alternative system against the imprudent strategies of centralised finance, will potentially suffer the effects of this massive global liquidity crunch.

A financial bubble caused by the accumulation of high-risk leveraged loans seems familiar, and it certainly is, since the current CLO crisis holds more similarities than differences to the 2008 Global Financial Crisis (GFC). The difference lies in the numbers, and this time it is much worse.

CLOs vs CDOs – The 2008 global financial crisis market collapse

As discussed, the Collateralized Loan Obligations are securities where several loan payments for different-sized companies in distress are grouped and reprocessed to different classes of creditors under various risks and interest rates. That is the system which expanded to the financial bubble that we are covering in this article. During the GFC, on the other hand, it was Collateralized Debt Obligations (CDOs) that catalysed the bursting of the 2008 bubble. The reasoning behind CDOs is essentially the same as CLOs; to simplify securities and facilitate loans to arrive where they’re needed. But in this case, the loans distributed to homebuyers instead of companies in distress. As lenders grew a stable profit with CDO interest rates over grouped mortgages, the real estate market began accepting mortgage deals with homebuyers who did not have the requisite credit score or liquidity to pay back the loans, especially with ballooning interest rates after the first year of payments. Rating agencies turned a blind eye on the issue leading up to September 2008, the largest bankruptcy in US history, as Lehman Brothers went under and several leading firms followed.

So what is the difference between the 2008 crisis and the current bubble forming with CLO? In a nutshell, CDOs loan to homebuyers while CLOs loan to troubled businesses. Although the frameworks are inherently similar, some argue that the 2008 crisis won’t repeat itself because CLOs are safer and better reviewed by the credit rating firms, who seemingly have a better grasp on how to rate packages as opposed to the last decade when the financial crisis imploded. According to an analysis from PineBridge Investments, although the loans available in CLOs are leveraged, they allegedly cannot be executed over a six-fold leverage. They also seem to present low levels of default, since most tranches are allegedly either AAA or AA rated. At the same time, each credit is analysed individually by countless firms seeking to execute the best loans possible for the most reliable companies that are facing financial hardship. As shown by the Federal Reserve report, that is not necessarily true, since 6/10 of loans range from AAA to BBB and more than a quarter of those don’t register in any category.

After the economy collapsed in 2008, movements such as Occupy Wall Street rose from the financial chaos to demand more regulations against central and private banks, who were not held accountable for their predatory lending and greed-driven experiments. In fact, out of the dozens of banks and firms involved during the mortgage-loan scheme of the 2000s, one single banker was sentenced to jail in the United States for manipulating bond prices. Iceland, in contrast, is considered the only country in the global economy to have held all responsible bankers accountable for their crimes.

The global financial collapse of 2008 re-enforced that financial systems can indeed fail, no matter how traditional and presumably safe they seem to be. The economic crash also gave light to a different type of realisation into the world, one that had never been conceived before; that maybe society shouldn’t rely on traditional banks at all. That’s because, on October 31st of 2008, the Bitcoin Whitepaper was uploaded into the digital sphere, permanently changing the way people view money, value and trust.

When Bitcoin and other digital assets first surfaced in mainstream media, banks took pride in implying that their system provides more stability for those looking to invest and keep their assets stored safely. Although it is a centuries-old system, it is still one run by people, centralised and controlled by such. In a mere span of the past 12 years, we can observe how the banking governance has taken unacceptable risks that gradually imploded into the most significant financial crisis of the past century, in 2008. The cycle repeats, and it seems like the lessons supposedly learned after the GFC are in the past. Fortunately, digital assets are taking the opposite road, having emerged during an economic collapse and under constant development so investors can protect their funds against them.

How COVID-19 affects the CLO bubble

As stated in the previous section, COVID-19 caused the US Reserve to revoke the reserve requirements of 10%. That’s just one of a few dangerous changes that the pandemic has brought to financial systems. When it comes to the current and future scenarios of the CLO bubble, the predictions of the pandemic’s impact are not looking great.

In a July report, Moody’s Analytics made the argument that CLO packaging in Europe and the US is much less likely to have their loans honoured during the current crisis. The risk for CLOs packaged for companies in below BBB rating has increased significantly, with non-rated loans having their loss increased by 73.38% for the month of May. Upon analysing current CLOs through over-collateralization failures (test for value of CLO x issued debt), the numbers are even more haunting; 89.9% for April packages and 89.5% for May’s. The report shows that the overall risk of CLO packages in the US and Europe has substantially increased during the first few months of the pandemic.

It also doesn’t help the case for CLOs being safer when a CLO failed its AAA overcollateralized test last April, for the first time since 2008. In other words, a CLO package that was considered extremely safe and low-risk failed its assessment of having its contract value higher than the issued debt of the assets. Analysts from S&P global attribute this unforeseen result to the constant downgrades of the loan obligations, who are now reaching for CCC and non-rated companies for high-risk loans, as described by Moody’s analytics reports.

Some argue that CLOs might be riskier now, but COVID-19 is slowing down the market bubble, lowering the chances of the loan-obligations market to have the same fate as the 2008 crisis. An August analysis from the Wall Street Journal states that the feared downgrade in package ratings has not happened, as the three major rating firms in the US finished the spring without any significant downgrade on their rating standards. Even through the positive light, 22% of Moody’s 1,500 bonds have downgraded this year, which is still a substantial number considering how the market sees such results as “better than we thought,” as stated by David Preston, one of Wells Fargo’s leading CLO analysts. But they are not finished with the review; around 51% of the bonds are still waiting to be analysed.

The COVID-19 pandemic has set the entire global economy into a path of uncertainty, and that includes collateralized loan obligations. Its similarities to the frameworks that lead to the 2008 crash are evident, and most data point towards an economic burst in the upcoming years. It is just a matter of time to know whether the predictions will come true or if the market will learn to adapt and learn from its past mistakes. Nonetheless, the growing bubble created by CLOs is just one of many examples of how the centralised global economy often returns to a cycle of unethical margins of profit into financial collapse. Those who suffer the most from those scenarios are agents responsible for such catastrophes, but people under their leadership.

This article is not only an assessment of the CLO bubble but a reminder that traditional banking has and always will be prone to human error where profit values above society. Bitcoin was created in the height of the last financial collapse to bring monetary control into the hands of society, those who develop and move the world. A central system does not govern it, and a country or corporation does not own it. It is here for the people who seek freedom, and it will not go anywhere.

FAQs

What are Collateralized Loan Obligations (CLOs) and How Do They Work?

CLOs are a financial process where loans to many different companies are gathered into a single package, which is then leveraged and resold to several creditors under different rates. The goal is to make the financial system more efficient by overcoming the incompatibility between the diverse needs of borrowers and creditors. However, the complexity of CLOs, much like the Collateralized Debt Obligations (CDOs) that contributed to the 2008 crash, can increase the risk in the financial system.

What is the Current Issue with the CLO Framework?

The long-term issue with the CLO framework is that it enhances the complexity of the loan system, making it difficult for big banks to follow the amount of risk introduced through those loans. Rating agencies such as Moody’s and S&P advise creditors about investment risks, but these classifications have become increasingly less trustworthy as both creditors and rating agencies have taken more significant risks with CLO packages.

How Does the CLO Bubble Affect the Global Economy?

The CLO bubble affects the global economy by increasing the risk of loan defaults. It is estimated that more than $US800 billion (as reported in 2019) is at risk within the CLO model, which with COVID-19 is expected to surpass $US1 trillion. This could potentially lead to a financial crisis similar to the 2008 Global Financial Crisis.

What is the Difference Between the Current CLO Bubble and the 2008 Global Financial Crisis?

The 2008 Global Financial Crisis was catalysed by Collateralized Debt Obligations (CDOs) that were given to homebuyers, while the current CLO bubble involves loans given to troubled businesses. The frameworks are inherently similar, but the current CLO crisis holds more similarities than differences to the 2008 Global Financial Crisis, with the difference lying in the numbers, which are much worse this time.

How Does the COVID-19 Pandemic Affect the CLO Bubble?

The COVID-19 pandemic has set the entire global economy into a path of uncertainty, including collateralized loan obligations. The pandemic has increased the risk for CLOs packaged for companies in below BBB rating, with non-rated loans having their loss increased significantly. The downturn in the CLO bubble due to the pandemic is an inevitable matter of time.

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

What is the Base Blockchain? The Coinbase Layer 2

The Base blockchain, introduced by Coinbase, represents a significant development in the realm of cryptocurrency and blockchain technology. It is a layer-2 solution built on

Bitcoin Mining in the US: Main Challenges

Bitcoin mining in the United States has recently faced a range of challenges, from regulatory hurdles to community and environmental concerns. As a significant hub

Bitcoin Halving: Market Reacts

The 2024 Bitcoin halving, a significant event for the cryptocurrency world, marked a notable shift in the market dynamics of Bitcoin. As the block reward

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.