9 Feb, 26

Weekly Crypto Market Wrap: 9 February 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- BlackRock’s spot Bitcoin ETF IBIT trades over US$10bn in daily notional volume during peak volatility

- RBA delivers 25bp rate hike to 3.85%, with hawkish guidance reinforcing AUD strength and policy divergence

- Senator Cynthia Lummis urges banks to embrace digital assets, as stablecoin yield disputes continue to delay U.S. market structure legislation

- Tether expands headcount to ~300 employees amid continued infrastructure growth

- Strategy (formerly MicroStrategy) reports one of the largest quarterly losses in U.S. public market history; reaffirms indefinite holding horizon

Technicals & Macro

Markets

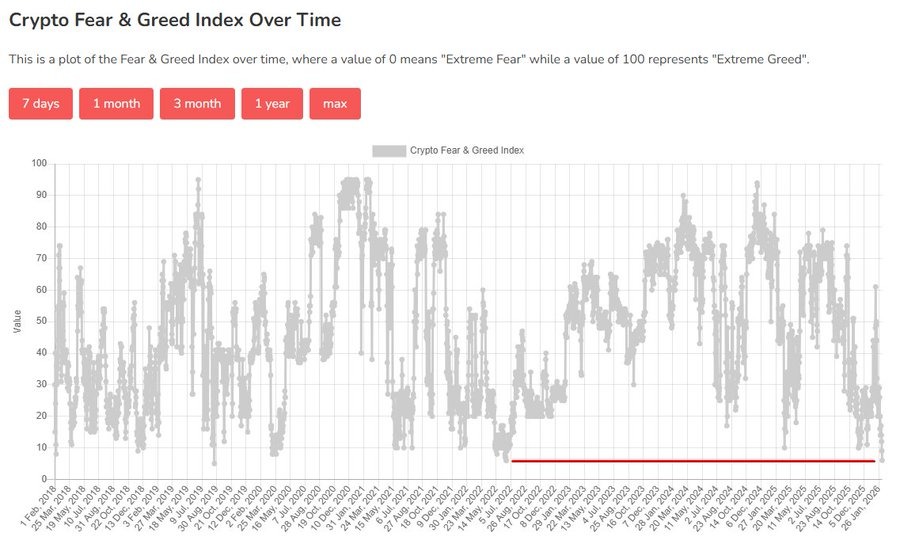

The tape last week was still defined by a sharp rotation out of risk, but it’s worth reframing it as a positioning reset rather than structural break. Crypto and growth finally took the air pocket that had been building after years of one-way crowding, while the broader index complex stayed resilient. The divergence made the drawdown feel uniquely painful, but it also argues this wasn’t a macro “system event” in the 2022 sense (last week the Crypto Fear & Greed Index has hit 6, the lowest since June 2022), we view it as more a re-rating of the most crowded risk while capital rotated into ‘sleepy’ defensives and “hard economy” exposure.

Source: X.com (@i_am_jackis)

This week’s macro focus is straightforward: jobs/NFP (Wednesday) and CPI (Friday). With unemployment expected to be steady and CPI seen around +0.3%, the base case is the Fed stays in wait-and-see mode, rates likely unchanged unless markets destabilise materially. Right now, the two political overhangs for crypto remain the Warsh nomination narrative (markets will keep debating what that means for policy reaction function) and the Clarity Act timeline, with stable yield distribution still the key sticking point.

The important point for us is the second-order effect: if broader equities finally roll over, crypto’s idiosyncratic drawdown can quickly become a correlated one. If equities stay supported, then crypto’s path has room to base without fighting a collapsing risk tape.

Source: Deribit.com

On BTC, last week was the “real” vol event in a while. DVOL ripped into the highs, the front end went into meaningful backwardation, and the market started to look two-sided again as overwriters and underwriters stepped in and vols began to crush from the peak.

Source: Velo.xyz

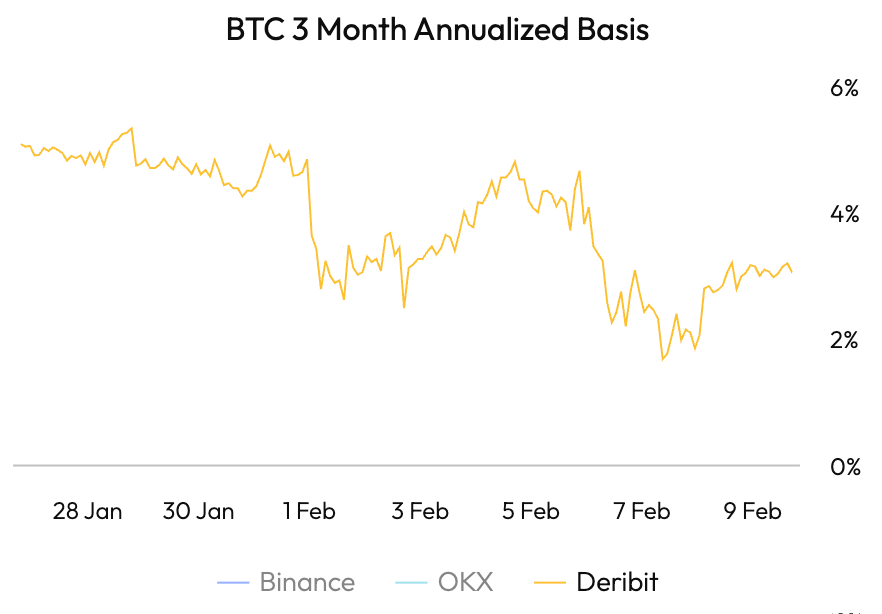

But the bigger tell is what didn’t happen: futures basis didn’t implode the way it does in a true capitulation moment. The basis compressing is consistent with deleraging, but not with the kind of forced, indiscriminate liquidation that clears the deck. That’s why the bounce of ~US$60k does read more like tactical reflex than a definitive cycle low.

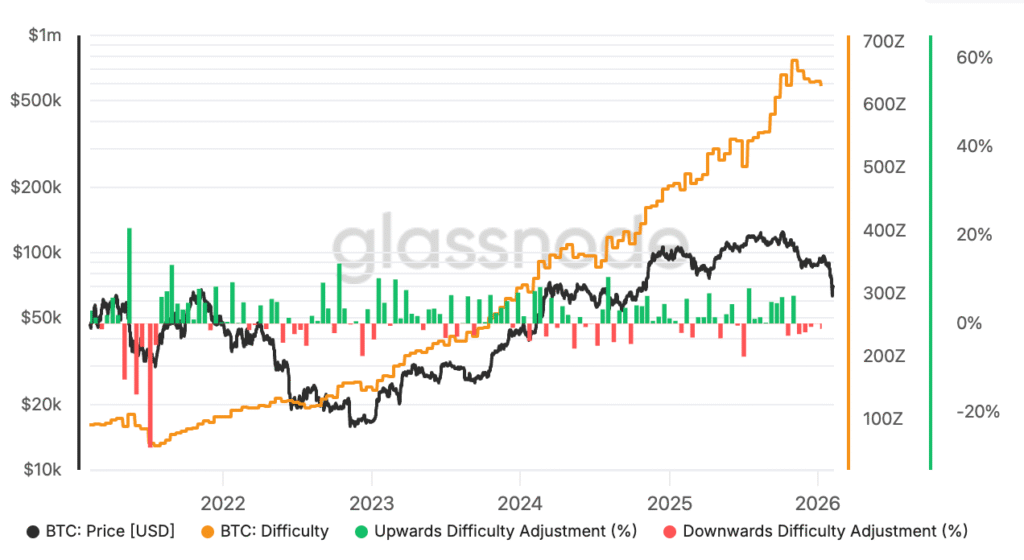

Source: Glassnode.com Bitcoin: Difficulty Adjustment Percent Change (5-year)

The ~US$60k level matters because it lines up with a widely used anchor: mining cost. Historically, Bitcoin tends to trough just below mining costs. Q1 2026 estimates range from ~$60k for lowest-cost miners. When price trades down to where a chunk of miners are near break-even, behaviour tends to shift where fresh selling pressure eases at the margin, hedging flows change and dip buyers get more comfortable stepping in around a “fair value” narrative. But one thing to note is that mining cost is support, not a hard floor. So these costs help explain why we bounced there, but it doesn’t confirm where we bottom.

In the past, BTC had spent extended stretches well below cost in prior cycles (2018-2019 bear market saw Bitcoin spend ~6 months and 20% below mining costs), and in 2026 it’s even less of a mechanical trigger because mining costs are a wide distribution (low-cost operators survive far lower than legacy fleet), and with ~20 million of 21 million Bitcoin already circulating, supply dynamics are less impactful than in prior cycles (only 5% incremental supply remaining vs. 25% in 2018) which makes it increasingly a demand and flow market (not a new supply one).

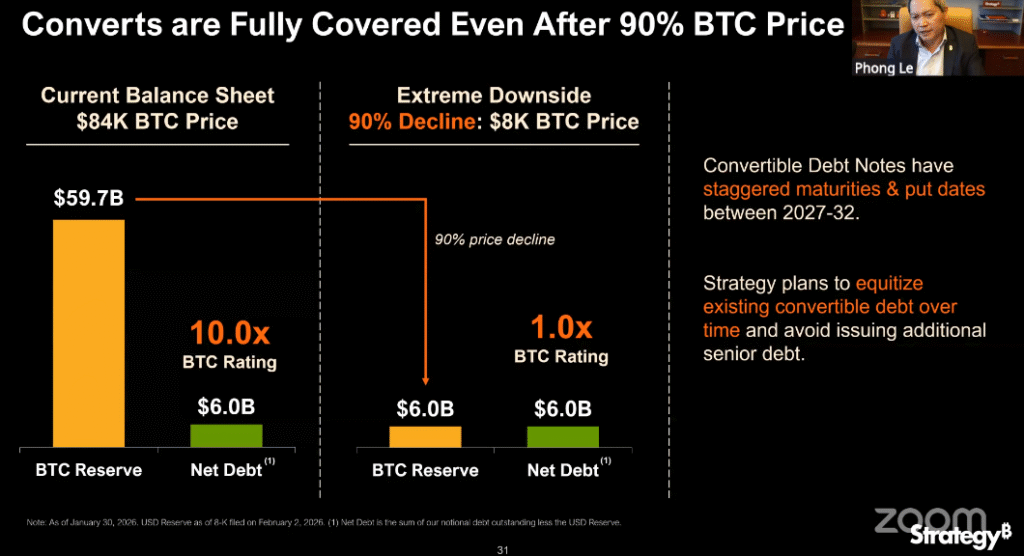

Source: X.com (@Strategy) Strategy Q42025 Earnings Call

That demand and flow lens is also why the Strategy / DAT complex matters here. Strategy’s Q4 print landed right in the middle of the flush and acted as a real-time stress test of the “Bitcoin treasury” bid. Saylor’s message was steady. BTC would need to fall to ~$8k and stay there for five years before MSTR would struggle to cover its debt. The market seemed to take that as reassurance at the margin as BTC stabilised off that ~$60k zone and worked back toward ~$70k.

DAT land remain underwater

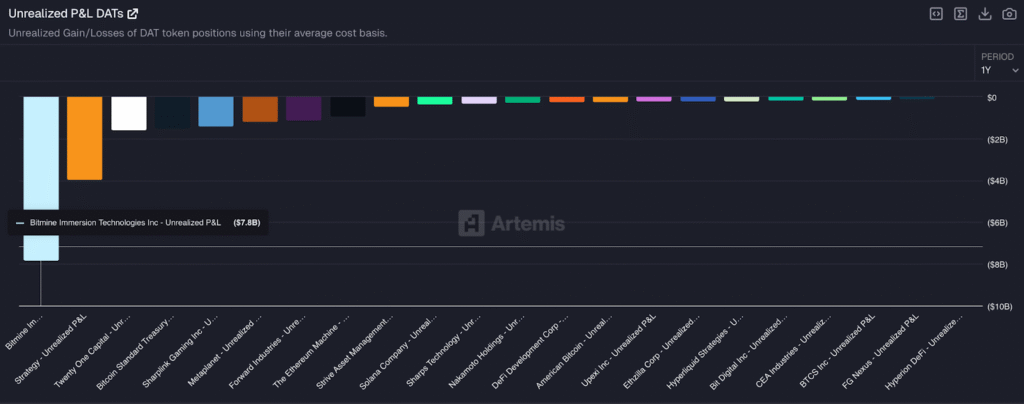

As I touched on last week, the bigger implication is reflexivity from here. Cumulative losses across DATs are now estimated around $25bn, led by Bitmine and Strategy, with average cost bases roughly $3.9k (BMNR) and $76k (MSTR). Bitmine’s mark to market losses alone are being framed as larger than the headline FTX loss figure (around $8bn), which is a sobering comparison even if the nature of the loss is very different (unrealized versus missing assets).

Source: Artemis.com Unrealized P&L DATs

With BTC (similarly ETH and SOL) below many treasury cost bases and mNAV materially compressed, DATs in this current landscape start to look less like the marginal buyer that pushes prices up but more like sticky holders. This is not necessarily because they are forced sellers, but because raising fresh capital becomes less attractive when equity and preferred markets are under pressure.

SOL

Across the majors, SOL was the weak link again, closing around $87.81 (-14.2% / 7D) and behaving like the funding leg of the complex.

The Multicoin headline/rumour cycle certainly didn’t help sentiment into thin liquidity, but the more important datapoint is what’s happening inside the ecosystem: risk appetite has been clearing out of the most speculative pockets, and DeFi collateral composition is shifting sharply away from meme-driven leverage. That’s painful short-term, but it’s also the type of internal “clean-up” that tends to make the next base more durable.

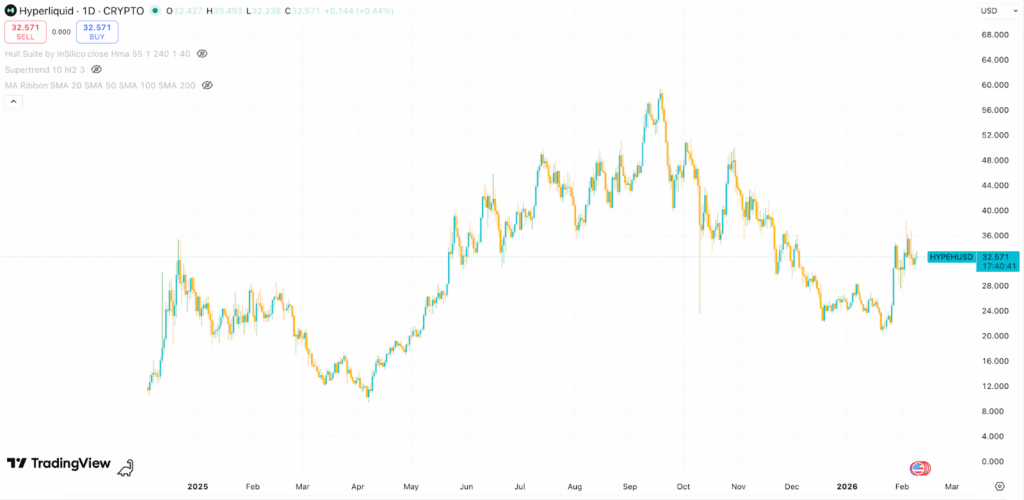

Hyperliquid (HYPE)

Source: Tradingview

HYPE was the exception and the signal. While most majors were de-grossing, HYPE gained ~7% on the week and printed new weekly highs, largely because the market could point to real fundamentals and a clear product catalyst. HIP-4 (prediction markets + options) landed at exactly the right time: sentiment was fragile, and the tape rewarded teams shipping into demand. The Coinbase listing also added legitimacy and widened the buyer base, but the real anchor was operational strength, revenue holding around ~$3m/day, perps volume expanding materially, and OI stable. The unlock reduction story also helped, alignment matters most when the market is stressed!

The takeaway is that HYPE is not immune to beta, nothing is if BTC re-breaks lows, but we see that the fundamental differentiation is starting to matter again, and that’s a healthy sign for the broader market once the leverage cycle finishes washing out.

Keep pushing!

Emir Ibrahim, Analyst

Spot Desk

The crypto asset complex endured a multi-stage deleveraging event this week, marked by over $2.6 billion in liquidations. Trading desk flows mirrored the volatility; while client dynamics for the year have been characterised by guarded behavior and suppressed risk appetite, last week saw significant outlier selling volumes in majors (BTC/ETH) as the desk serviced a number of large block trades into both stable and fiat crosses. Volumes were largely skewed to the sell-side as the “dash for cash” in risk markets triggered by the Warsh pivot and explosion in volatility (amplified by cross-asset funding dynamics and derivatives positioning) left few stones unturned. PAXG remained a significant accumulation favorite, as we saw sizable buying against stables as well as block trades against BTC as the pair continued to attract rotation interest. In altcoins, we saw a mixed pickup in activity – SOL saw buying while names like AVAX, AERO, and Arweave (AR) faced derisking.

In a week of price action to remember, Bitcoin fell from an open of $76,968 to lows at US$60,000, levels not seen since October 2024, driven by record-breaking volumes in BlackRock’s IBIT as it traded over $10 billion in notional value on Thursday. Ethereum followed a similar path, sliding from US$2,270 to US$1,747 in the chaos. The volatility coincided with an 11.16% drop in mining difficulty, the largest decline since the 2021 China ban – underpinned by a combination of falling prices and the Winter Storm Fern, which has forced U.S. miners to curtail operations to support residential power grids. As the dust settled in the weekend session, both assets reclaimed key psychological levels, with BTC stabilizing above $70,000 and ETH reclaiming $2,000 – traders now look to the new week for signs of this being the requisite capitulation event to clear leverage and find demand to underpin the next rally.

AUD/USD demonstrated notable resilience, opening the week at 0.6953 and rallying behind Tuesday’s RBA interest rate decision. The pair saw significant intra-week volatility, surging over 100bps in the hour following the decision as the market digested the 25bp hike to 3.85% and Governor Bullock’s hawkish commentary. While the pair cooled mid-week, it ultimately showed significant strength to range and consolidate near the highs, reclaiming 0.7000 into Friday’s New York close. With annual inflation jumping to 3.8% and the RBA’s updated outlook projecting a peak of 4.2% by mid-year, the market has started to price in a more aggressive policy path; global central bank policy divergence and widening yield differentials look set to remain structural tailwinds for the currency and momentum has carried into the new week as AUD/USD currently trades at 0.7043.

In the news, institutional expansion continues to drive forward despite market turbulence. Tether is expanding its global workforce to 300, with plans to add 150 more specialized roles over the next 18 months to support its growing infrastructure. Strategy (formerly MicroStrategy) reported one of the largest quarterly losses ever recorded by a public entity but reaffirmed its resilient capital structure and indefinite holding horizon. In Washington, Senator Cynthia Lummis highlighted a bright future for the sector, advocating for banks to embrace digital assets as a core growth opportunity; while stablecoin legislation currently works through delays over yield provisions, the ongoing dialogue is being viewed as a constructive step toward a regulatory framework that continues to bridge the gap between traditional finance and digital asset innovation.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and altcoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Ben Mensah, Trading Analyst

Derivatives Desk

WHOLESALE INVESTORS ONLY

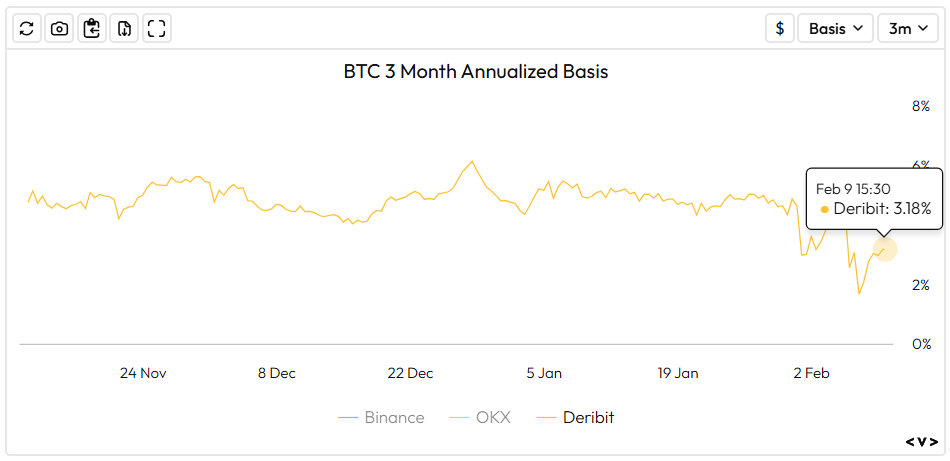

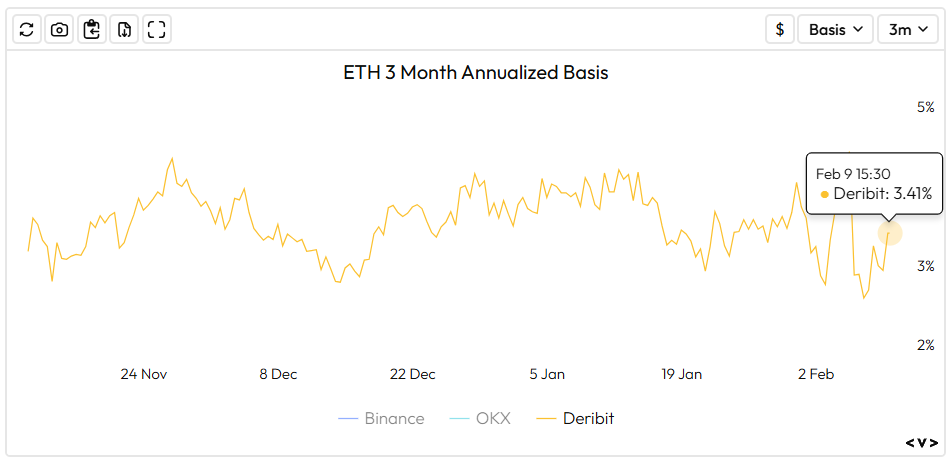

Basis rates continued their downward trend this week, with the BTC 90-day basis retracing to 3.18%. In a notable shift, ETH is currently commanding a premium over BTC at 3.41%, despite slipping 10 bps over the period. This inversion is particularly rare, as ETH’s native staking yield typically exerts downward pressure on its basis relative to Bitcoin.

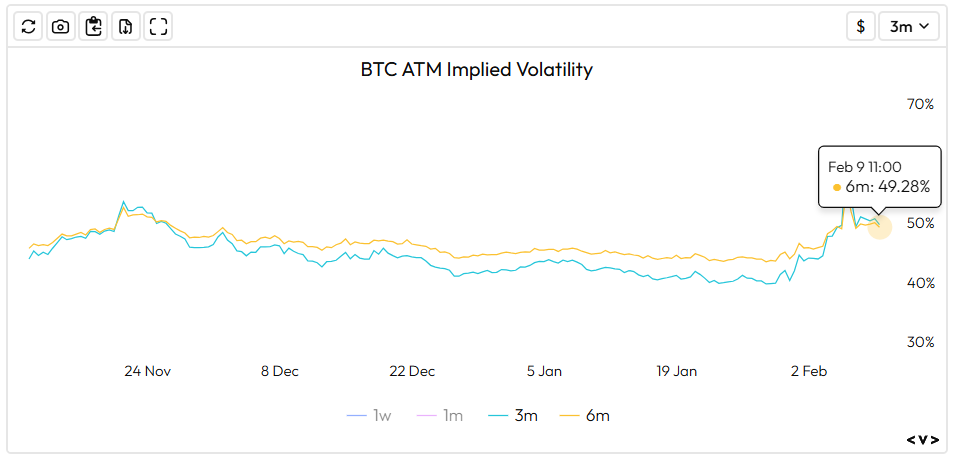

BTC ATM IV is up again over the week, roughly by 3.5 vol points on the 90-day contracts:

Source: Velodata

This Week’s Trade Idea – Zero Cost Collar

Implement a Zero-Cost Collar on ETH – a simple options strategy to simultaneously limit downside and cap upside at zero net cost.

Mechanics of the Collar

- Protective Put at USD $1,500 – this ensures a minimum floor: regardless of how far ETH might drop, the investor retains the right to sell at USD $1,500 at expiry.

- Covered Call at USD $3,000 – this caps the upside. The premium from writing the call offsets the cost of the put.

- Expiry is at the end of June 2026.

Payoff Profile:

- If ETH ≤ USD $1,500 at expiry → downside is fully hedged; the investor sells at USD $1,500.

- If USD $1,500 < ETH < USD $3,000 → they capture spot market gains (ETH trade value minus option costs = zero upfront cost).

- If ETH ≥ USD $3,000 → maximum payoff is capped at USD $3,000.

Risk Considerations:

- Opportunity cost: Upside beyond $3,000 is foregone for downside protection.

- Regulatory shifts: New laws (Clarity Act, Project Crypto) may drive sudden shifts in ETH price or volatility.

- Alternative altcoin moves: Unexpected narratives (e.g., revenue meta/Ai hype) could redirect capital away from ETH, increasing relative risk towards downside.

Why the Collar Makes Sense Now:

- Secures present gains while retaining material upside.

- Neutral capital deployment: No immediate net premium means the investor doesn’t deploy additional funds while locking a favorable risk profile.

What to Watch

TUE: Fed Waller Speech, ECB President Lagarde Speech, US Retail Sales MoM

WED: CN Inflation aRate YoY, US Non Farm Payrolls, US Unemployment Rate

THUR: GB GDP Growth Rate YoY

FRI: US Core Inflation Rate YoY

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Zerocap Partners with Singapore Gulf Bank to Solve Institutional Fiat Settlement

How Zerocap and Singapore Gulf Bank are solving institutional crypto fiat settlement with real-time USD rails during Asia hours. The Problem With Legacy Settlement Institutional

Weekly Crypto Market Wrap: 30 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

AI Tokens Now Available on Zerocap

Decentralised AI tokens are emerging as one of the most compelling investment themes of this crypto cycle. A new class of blockchain-native protocols has been

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.