7 Apr, 26

Weekly Crypto Market Wrap: 7 April 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- BTC spot ETFs recorded $1.32B in net inflows in March after four consecutive months of outflows, though April flows have cooled to just $69.6m so far,

- MicroStrategy purchased another $330m in BTC early this month, extending its position as the largest corporate holder;

- Strategy raised $1.56B via its preferred stock STRC in March alone to fund purchases,

- Coinbase received conditional OCC approval to operate as a national trust bank,

- BNP Paribas launched six Bitcoin and Ethereum ETNs for French retail and private banking clients from March 30,

- The US Department of Labor proposed a rule that would create a safe harbour for 401(k) fiduciaries adding crypto and alternative assets to retirement plans.

Technicals & Macro

Markets

Risk assets posted their first positive week in six as ceasefire diplomacy injected a dose of cautious optimism into markets battered by five consecutive weeks of selling. The narrative arc of the week was pure whiplash. Monday saw a sharp rally after reports that the US, Iran and regional mediators were discussing terms for a potential 45-day ceasefire and the reopening of the Strait of Hormuz. Dow futures surged 1,100 points overnight and Brent briefly dipped below $100 for the first time since early March. That optimism was abruptly reversed on Wednesday night when Trump delivered a primetime address vowing to continue strikes on Iran for “two to three more weeks,” threatening to hit power plants and bridges and send the country “back to the stone age.” Oil surged above $113 and equities tanked intraday. The Dow was down over 600 points before partially recovering after Iranian state media reported that Tehran was working with Oman on a protocol to allow some ships through the Strait.

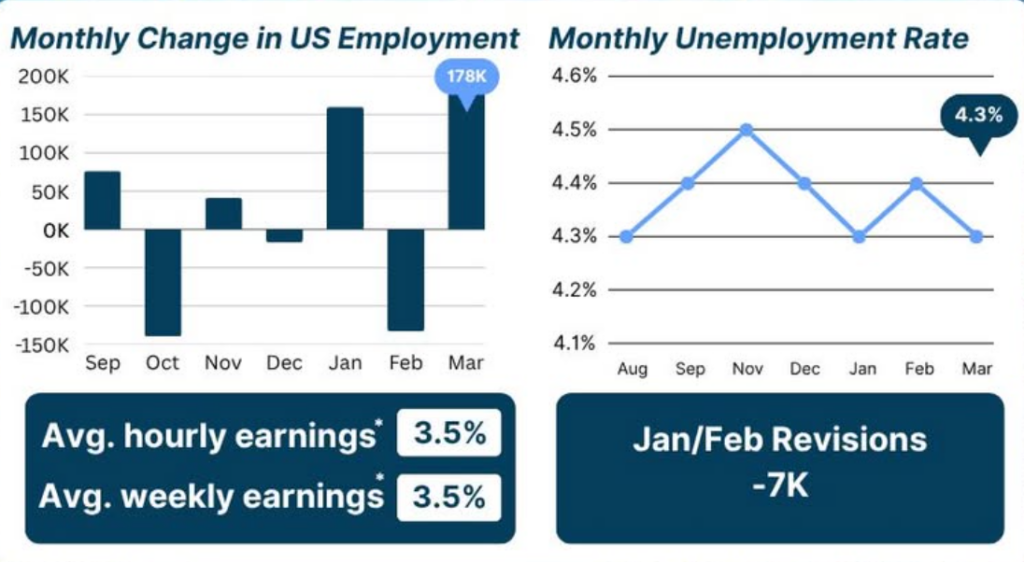

The week closed with Trump extending his strike pause deadline to April 8 (tomorrow) and floating the possibility of talks, leaving markets hanging on every headline. On the data front, March nonfarm payrolls printed a healthy +178,000 (released Good Friday with markets closed), with unemployment at 4.3%. The ISM Services PMI showed growth slowing to 54 from 56.1, but the prices paid component surged, reinforcing the theme that the war-driven energy shock is feeding through into broader inflation.

Source: TradingView

Equities rallied sharply in a shortened trading week (markets closed Good Friday). The S&P 500 gained 3.4% to close at 6,612, snapping its five-week losing streak. The Nasdaq outperformed with a 4.4% gain to 21,996, its best week since November 2025, while the Dow added 3.0% to 46,670. The recovery was broad-based but volatile, with Thursday’s session seeing a 600-point intraday Dow swing before major indices recovered from steep losses to close mixed. Despite the bounce, the S&P 500 remains roughly 6% below its January highs and all three major benchmarks still sit below their 200-day moving averages. Tech led the charge on the upside with Alphabet and Amazon each up over 1% on Monday, and Micron surging 3.2%. The VIX pulled back to 24.2 from its war-high above 31, but remains well above pre-conflict levels.

Source: MBS Highway

Yields eased modestly on ceasefire optimism before reversing. The 10-year pulled back to around 4.34% after touching 4.48% the prior week, while the 30-year settled below 5% after briefly breaching that threshold. Friday’s strong jobs print (+178k) pushed yields higher in Good Friday bond trading, with the 10-year jumping 3bp immediately on the release. The IBKR rates team highlighted a bear-flattening dynamic, with shorter tenors leading the move higher as markets price out any remaining rate cut expectations. Fed funds futures now imply zero cuts for 2026, which is a dramatic shift from the two cuts priced before the war began. The ISM Services prices paid surge to 70.7 will reinforce the FOMC’s caution: even if oil normalises, the second-round effects are already embedded in services prices, making the bar for easing even higher.

Source: Bloomberg

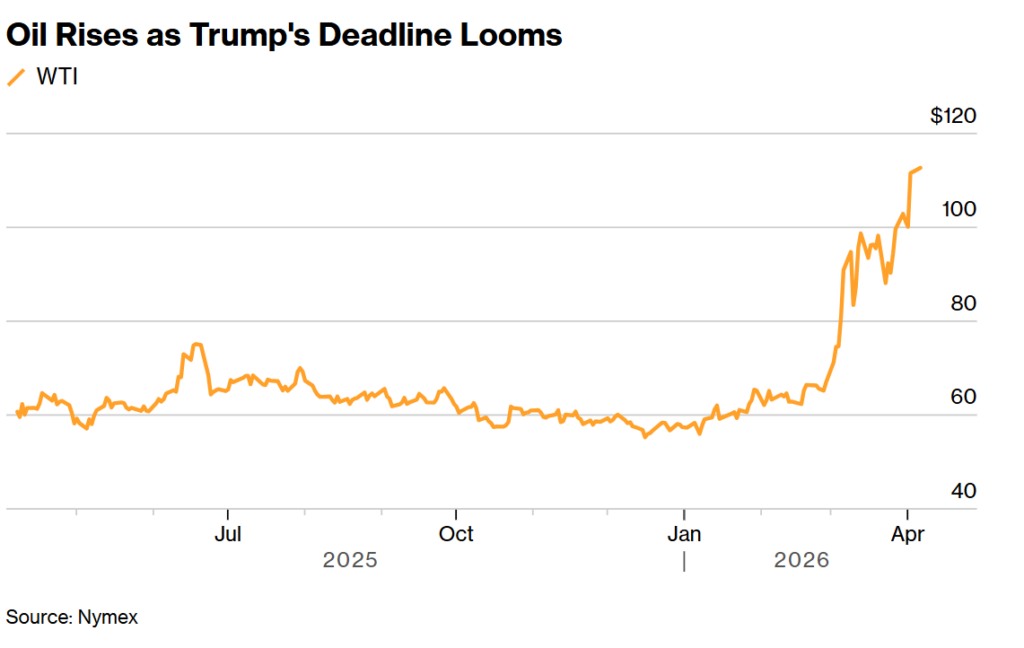

Oil remained elevated but showed its first sustained pullback from war highs. Brent settled around $110, down from last week’s $113 close but still up approximately 60% since the conflict began. WTI hovered near $96. Monday’s ceasefire reports briefly knocked Brent below $100 for the first time since early March, before Trump’s “Power Plant Day” rhetoric on Sunday pushed it back above $110. The Strait of Hormuz saw 21 ships pass over the weekend, the highest traffic since the war began — but this compares to a normal daily throughput of 135 ships. Oil inventories have declined by roughly 155 million barrels in the first three weeks of conflict, according to Zerohedge, underscoring the magnitude of the physical supply loss.

Source: Zerohedge

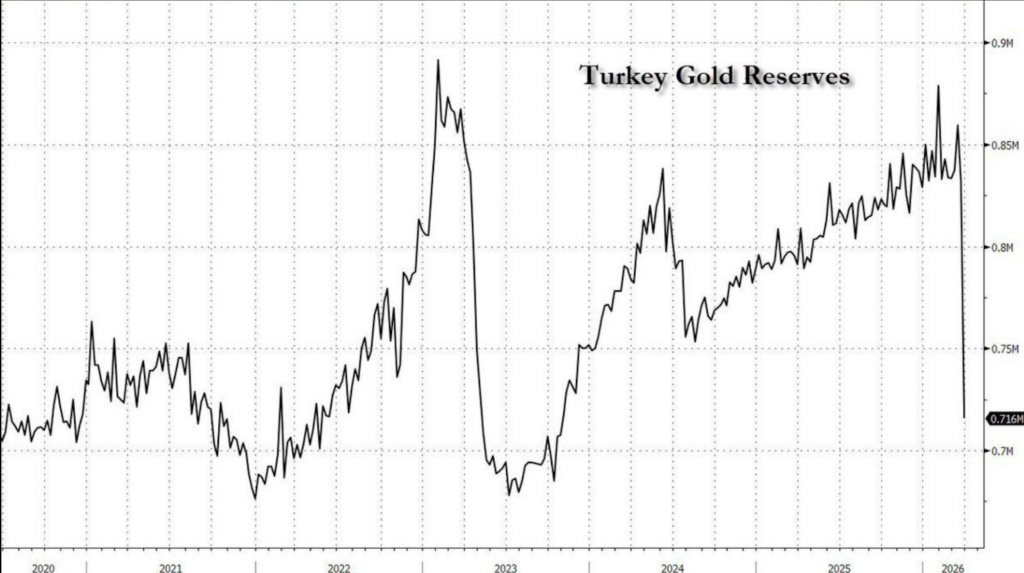

Gold stabilised around $4,680, recovering modestly after its 13% decline from the March highs. Some note that Turkey sold 120 tonnes of gold ($20B) in late March as part of reserve management under disinflation stress , a potential contributor to the severity of the paper market selloff.

Crypto participated in the risk-on trade but the real story this week is structural, not price. BTC gained roughly 4.6% to ~$69,800, approaching the $70k level that has been resistance for weeks. ETH rallied around 8% to ~$2,149, reclaiming $2,100. BTC spot ETFs recorded $1.32B in net inflows in March after four consecutive months of outflows, while long-term holder supply has been rising since mid-February despite a 46% drawdown from the October ATH. Strategy raised $1.56B through its preferred stock STRC in March alone, funding 50% of monthly BTC purchases. However, April flows have cooled sharply to just $69.6m so far, a fraction of March’s pace.

Source: Coinmarketcap

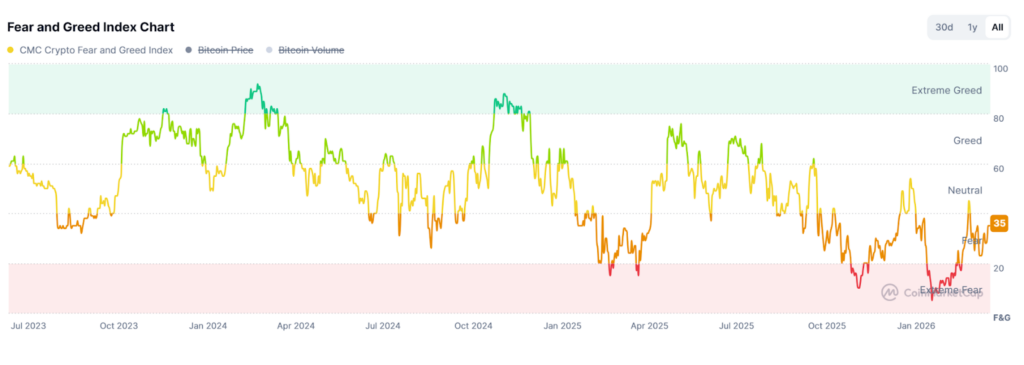

Currently, BTC remains range-bound between $66k and $73k, with $71,500 as stubborn resistance. The Crypto Fear & Greed Index sits at 29 (“Fear”), the lowest sustained period since the 2022 bear market.

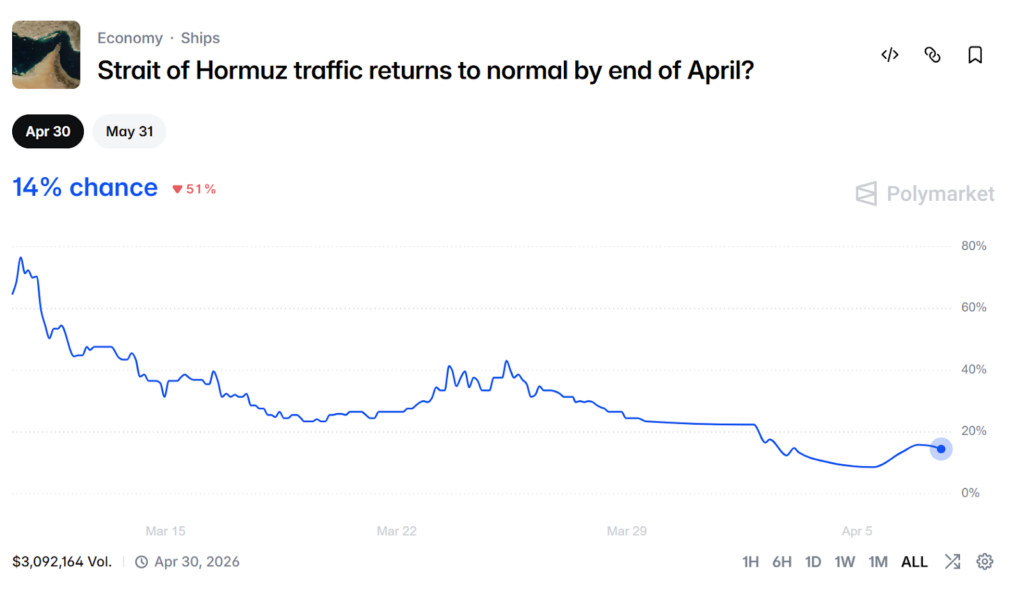

Source: Polymarket

With Polymarket pricing just 14% odds of Strait of Hormuz traffic normalising by month-end, the ceasefire catalyst that could break the range higher remains binary.

For any pricing needs, please get in touch with the Zerocap desk.

Emir Ibrahim, Analyst

Spot Desk

Market conditions over the past week remained firmly macro-driven, with digital assets continuing to trade as high-beta expressions of broader risk sentiment. Geopolitical tensions and associated disruption in energy markets kept inflation expectations sticky and reinforced a “higher-for-longer” rates narrative in both the US and Australia, with sovereign yields remaining elevated and liquidity conditions tight.

In commodities, Brent crude remained a key macro barometer, trading a volatile USD ~98–112 range, stabilising toward the USD 108–110 area into the weekend as supply disruption risks persisted. This reinforced the inflation impulse feeding through broader risk markets and supported continued USD strength.

FX markets reflected the same regime, with AUD/USD trading a 0.6950/0.7070 range. Early week ‘risk on’ saw AUD/USD initially rally toward 0.7060/0.7070, before reversing lower into the 0.6950/0.6970 area as sentiment deteriorated. The range for AUD/USD remains tight underscoring the AUD’s continued sensitivity to global risk and commodity price swings.

Within crypto markets, spot flow has remained broadly balanced across majors, consistent with a market still lacking directional conviction but highly reactive to macro headlines. Bitcoin (BTC) has continued to see strong two-way interest, with persistent dip-buying in the mid to high 60k region. Rally into the low 70k’s delivering sell side supply and reinforcing the resistance band. Ethereum (ETH) remained comparatively softer, with continued relative underperformance versus BTC and ongoing pressure in the ETH/BTC cross (current trading 0.03070). Solana (SOL) maintained a more constructive tone, with steady accumulation on pullbacks suggesting continued preference for high-beta liquid alts despite broader caution and trading down circa 3% on the week.

It would appear that crypto flow this week has been increasingly defined by carry and balance-sheet optimisation rather than directional positioning (outside of the tight trading range). BTC in particular saw increased utilisation in structured yield strategies, with covered call overwriting and delta-neutral carry trades remaining prevalent as investors monetised volatility within the range. At the same time, crypto lending markets recorded a modest pickup in BTC and ETH-backed borrowing demand, driven largely by collateral recycling rather than incremental leverage expansion. This points to a more tactical use of balance sheets rather than outright risk-on positioning.

In DeFi and stablecoin markets, activity remained defensive in tone. Stablecoin usage stayed elevated – base collateral in yield strategies and consistent flow from the remitter base. PAX Gold (PAXG) flows were intermittent, reinforcing the view that macro hedging remains opportunistic rather than structural within crypto-native portfolios given the current landscape.

Altcoin participation continues to favour liquid majors over fragmented long-tail exposure. Overall, positioning remains balanced but cautious, with flows driven more by yield extraction and relative value positioning than by conviction driven directional exposure.

John Toro, Head of Trading

Derivatives Desk

WHOLESALE INVESTORS ONLY

Derivatives markets remained in consolidation following the recent (large) Bitcoin month end options expiries, with open interest continuing to drift lower across perps and listed futures. Positioning now remains cleaner, with fewer liquidation cascades and more balanced two-way flow, consistent with a post-deleveraging regime.

Funding weakened over the week. BTC perp funding shifted from mildly positive to neutral-to-negative into the close, signalling rebuilding short interest and reduced long crowding. Ethereum funding remained structurally softer throughout, reinforcing relative underperformance and weaker speculative demand versus BTC.

Volatility continues to compress. BTC ATM vols sit broadly in the low-50s on 1W, with the curve relatively flat into 1–3M and only a mild upward slope at the long end. Skew remains put leaning but has normalised, with downside demand concentrated in ~USD 60k equivalent delta puts, while upside supply remains heavy into USD 70k – 75k calls, reflecting continued overwriting pressure.

The cryptocurrency derivatives ecosystem remains defined by systematic call overwriting and structured premium selling, which continues to cap upside convexity and reinforce range-bound price action. ETH skew remains more negative than BTC, with downside demand clustered around USD 1.8k – 2.0k strikes, consistent with weaker relative spot support.

Crypto credit remains stable, with flat haircuts and no stress in margin utilisation. Borrow demand is dominated by BTC/ETH collateralised lending, largely for liquidity recycling rather than leverage expansion. Overall, the derivatives complex reflects a de-risked equilibrium: lower leverage, compressed vol, and balanced but fragile positioning, leaving price action highly sensitive to macro catalysts.

This Week’s Trade Idea – BTC Yield Entry Notes

Leveraging the current put skew and tight BTC trading range, we see a compelling opportunity to implement Yield Entry Notes. This strategy monetises the higher cost of downside protection by selling puts at attractive levels.

Yield Entry Note sample terms:

For a 1-month BTC Yield Entry Note with 60k Strike Price one can generate 1.98% Yield (~26.9% annualised). There are two possible outcomes at expiry:

- BTC expires above 60k: investment paid back in cash + earns 1.98% yield (~26.9% annualised, paid in cash).

- BTC expires below 60k: investment used to buy BTC at 60k + earns 1.98% yield (~26.9% annualised, paid in BTC).

Risk Considerations:

- Even if BTC was to trade below the strike on expiry, you would buy at the strike. This exposes the position to larger downside moves (short gamma and short convexity).

- In stressed conditions, liquidity in downside strikes can reduce, increasing hedge slippage and exit costs.

What to Watch

Mon 6 Apr US ISM Services PMI (Mar) — first major post-NFP read on the services sector; watch closely given S&P Global flash already printed an 11-month low at 51.1.

Tue 7 Apr RBNZ Rate Decision — unanimous hold expected at 2.25% (97% market probability), but the statement is the focus.

Wed 8 Apr FOMC Minutes (Mar 18 meeting) — the week’s centrepiece. The FOMC left rates at 3.50–3.75% with the median still projecting one cut in each of 2026 and 2027.

The minutes will reveal the internal debate on tariff pass-through, oil-price modelling, and how much weight was placed on labor market deterioration.

Thu 9 Apr US PCE (Feb/Q4)

Fri 10 Apr US CPI (Mar) — The week’s headline risk event. March CPI consensus is +1.0% MoM / 3.4% YoY, which would be the largest single-month headline jump since the 2022 energy crisis, driven by Hormuz-related gasoline and energy price surges.

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Zerocap Partners with Singapore Gulf Bank to Solve Institutional Fiat Settlement

How Zerocap and Singapore Gulf Bank are solving institutional crypto fiat settlement with real-time USD rails during Asia hours. The Problem With Legacy Settlement Institutional

Weekly Crypto Market Wrap: 30 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

AI Tokens Now Available on Zerocap

Decentralised AI tokens are emerging as one of the most compelling investment themes of this crypto cycle. A new class of blockchain-native protocols has been

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.