23 Mar, 26

Weekly Crypto Market Wrap: 23 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

This is not financial advice. As always, do your own research.

Week in Review

- The US holds interest rates as the Iran war triggers inflation fears.

- The RBA increases the cash rate 25 basis points from 3.85% to 4.10%.

- Trump gives Iran 48 hours to open the Strait of Hormuz; Iran threatens to destroy energy, oil infrastructure; Israel strikes bridges in southern Lebanon.

- Bitcoin mining difficulty falls 7.7% as miner pressure persists.

- NYSE exchanges complete industry-wide removal of crypto ETF options caps.

- US securities regulator issues long-awaited crypto guidance.

Technicals & Macro

Markets

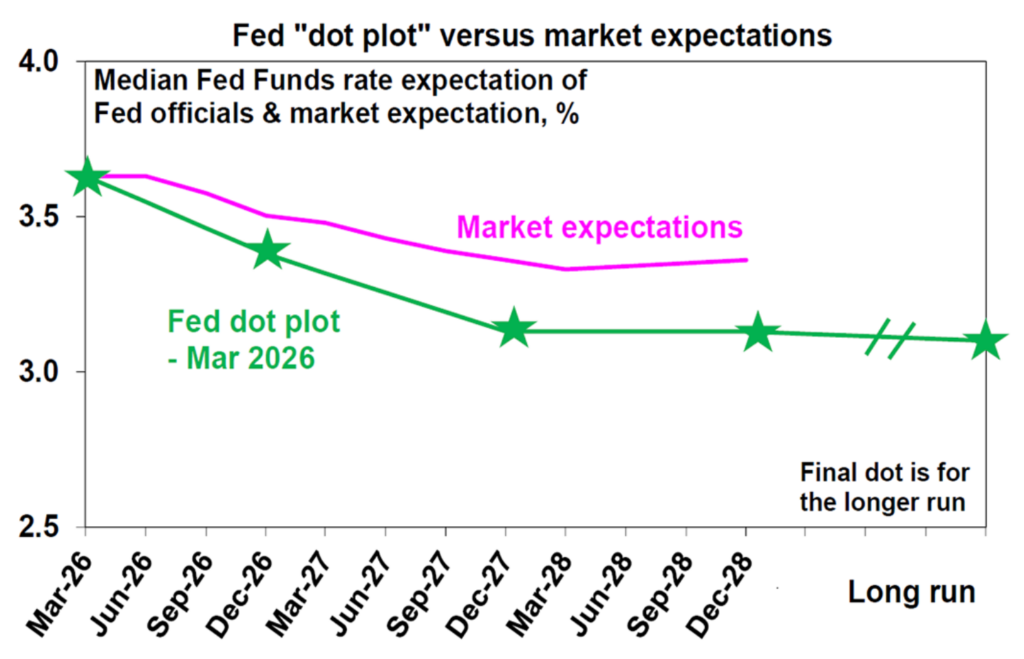

Last week, the Federal Reserve held rates on hold at 3.50%-3.75% as it remains firmly in wait-and-see mode, acknowledging the uncertain implications of the Iran conflict for both inflation and growth without committing to a direction. The dot plot still projects one more cut this year and another in 2027, but the distribution shifted meaningfully hawkish. 14 of 19 participants now see either no cut or just one in 2026, with four to five members downgrading from two cuts to one since December.

Source: AMP / Bloomberg

Powell was clear that any easing would require inflation to fall first, describing the current rate as sitting at the “high end of neutral” while characterising the labour market as stuck in a “zero employment growth equilibrium” with downside risk. The dovish camp has thinned considerably, only Miran now dissents in favour of a cut, and only for a modest 25bp, after Waller dropped his January push for easing and rejoined the consensus. Markets are pricing at most one cut this year, likely not before autumn, with some desks now questioning whether the Fed moves at all in 2026.

Source: YCharts

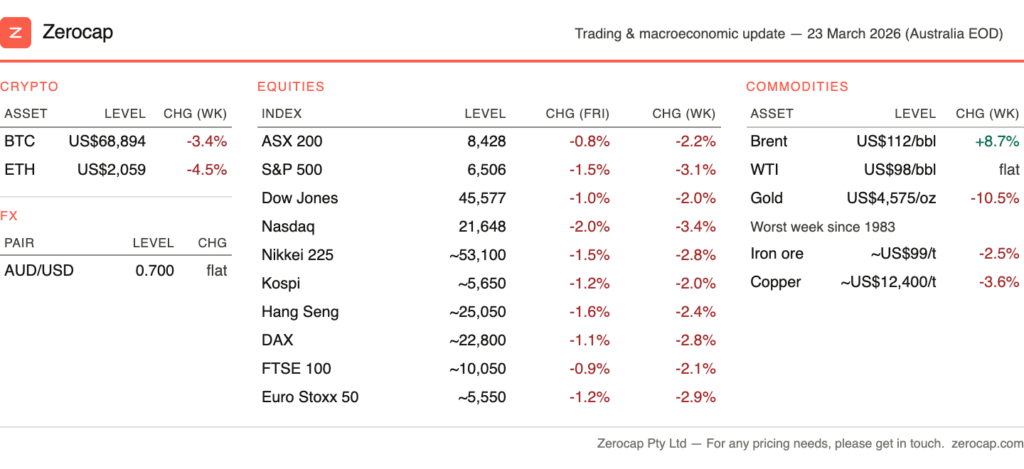

Equities had their worst week since the onset of the Iran conflict. The S&P 500 broke below its 200-day moving average for the first time since May 2025, which ended the 214-session streak above the trend line. The Nasdaq shed 2% alone to USD$21,648, with the Dow losing nearly 1% to USD$45,577.

Selling accelerated sharply on Friday after Iraq declared force majeure on all foreign-operated oilfields and drones struck two Kuwaiti refineries, broadening the supply disruption beyond the Strait of Hormuz. Energy names continued to benefit while rate-sensitive sectors were crushed, with utilities down 4.1%, real estate off 3.1% and tech losing 2.2% on the week.

Source: YCharts

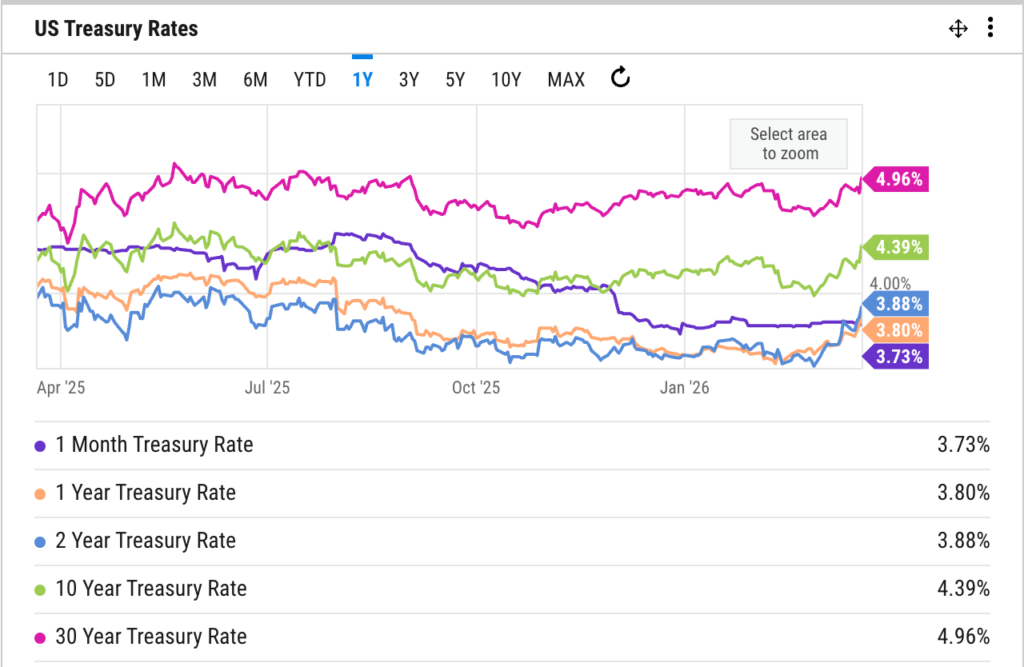

The rates complex repriced aggressively. The US10Y surged 13.5bp on Friday alone to 4.39%, the highest since August 2025, as traders de-rate near-term easing expectations and priced a higher-for-longer regime. The US30Y pushed through 4.96%. The moves were driven by a confluence of factors. Namely the hawkish dot-plot as discussed above, elevated energy-driven inflation breakevens and the realization that the stagflationary impulse may not be as transitory as the committee’s base case assumes.

Source: AMP / Bloomberg

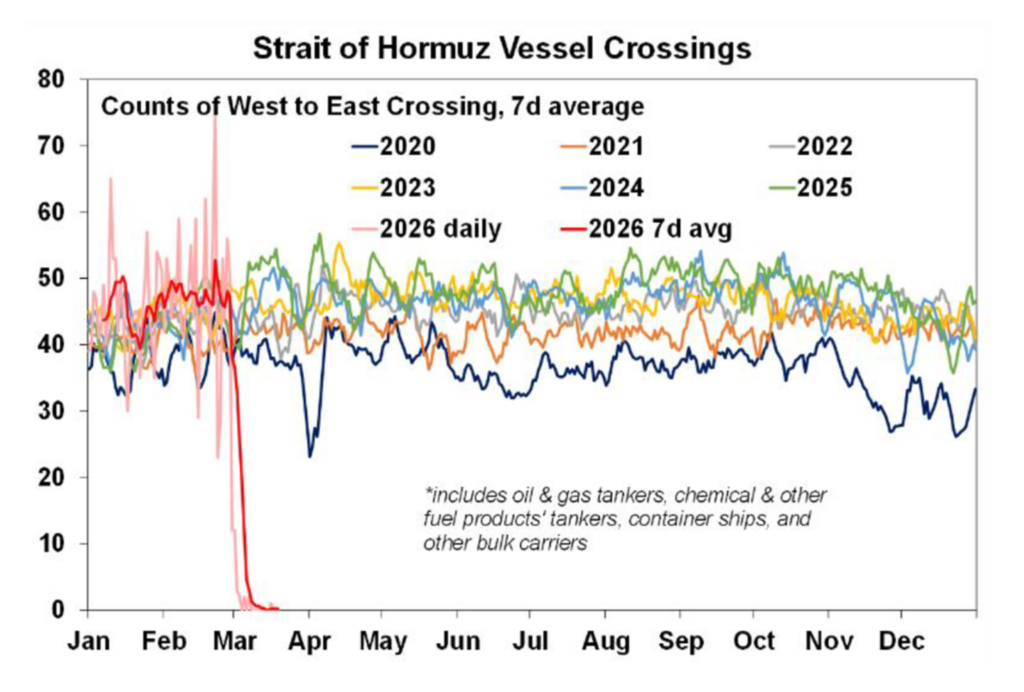

Oil remained the epicentre of global macro, as Brent surged nearly 9% on the week to close above USD$112/barrel, that is, the highest settlement since mid-2022 after briefly touching USD$113 intraday on reports of expanding conflict across the Persian Gulf. Iran continues to refuse to discuss reopening the waterway, and Trump rejected calls for a ceasefire, stating “you don’t go for a ceasefire when you are literally destroying the other side”.

On the other hand, Gold suffered its worst weekly selloff since 1983, collapsing 10.5% to around USD$4,575/oz. This move was driven by USD strength, with the DXY pushing to its highest level of the year above 100, surging real yields and forced liquidation in paper markets (margin-call cascade where leveraged gold longs were stopped out despite the geopolitical environment being fundamentally supportive of the metal). Similarly, Silver fell around 6.8%.

Digital assets did give back a portion of the prior week’s gains as the post-FOMC repricing and broader risk-off tone weighed on. Bitcoin fell around 3.4% on the week back to USD$68,900, retreating from a brief push above USD$74,000 mid-week before the Wednesday selloff. The FOMC-driven sell pattern held true, BTC has now dropped after seven of the last eight Fed meetings, a persistent “sell the news” dynamic.

Source: Longtermtrends

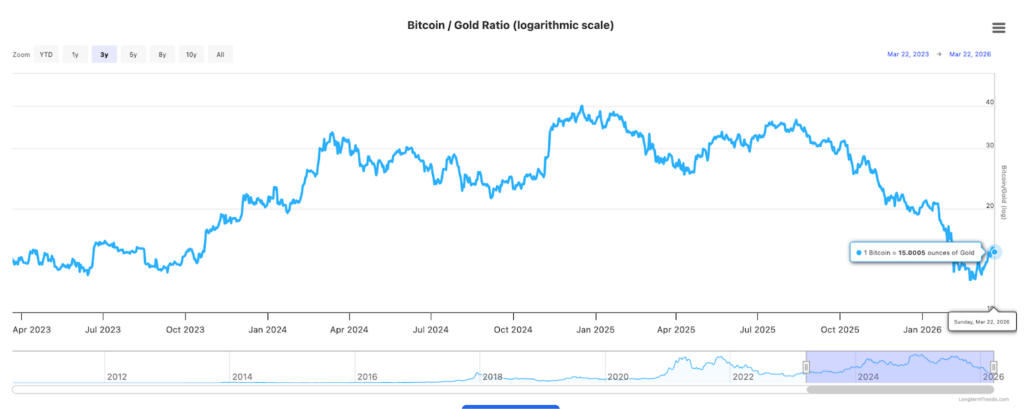

That said, the relative value picture is shifting in Bitcoin’s favour, particularly against gold. Gold surged more than 20% from the start of the year through the onset of the war on a wave of central bank buying, inflation hedging and de-dollarisation flows, while BTC lagged sharply, falling over 45% between last year’s October 10th liquidation event and the start of the conflict. What looked like an insurmountable performance gap just six weeks ago has narrowed by more than 20 percentage points in the past three weeks due to the recent move in gold.

Source: YChart

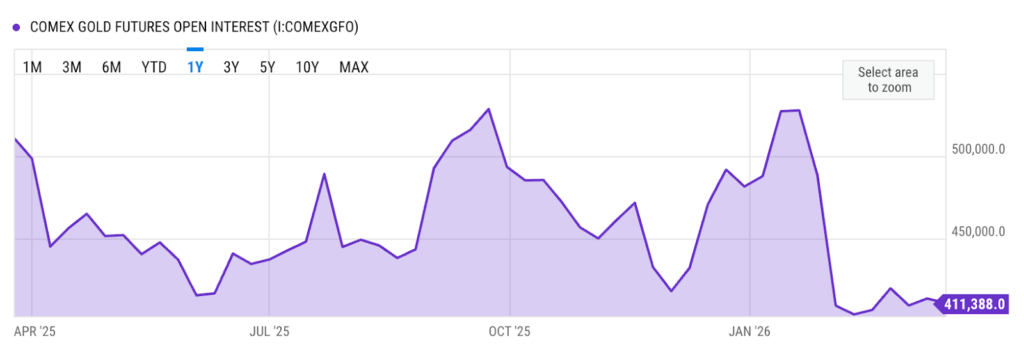

COMEX gold open interest has collapsed to multi-year lows of around 411,000 contracts even as spot prices surged around $5500. Meanwhile, the Bitcoin derivatives market has been more resilient, holding steady in a range since the start of the war.

ETF flows held positive heading into the decision, and BTC is still outperforming the S&P 500 on a one-month basis despite this week’s pullback. GLD ETFs saw outflows of about 2.7% of assets while IBIT took in roughly 1.5%. This erased gold’s earlier year-to-date lead over bitcoin ETFs, though gold still outperformed in late 2025.

The March 27th quarterly options expiry (with roughly $14B in BTC notional open interest) is the next key positioning event and could drive meaningful volatility as dealers rebalance gamma exposure. While crypto continues to trade as a high-beta macro asset, it is showing early signs of structural decorrelation during quieter periods as it carves out a relative strength case versus traditional havens. This narrative could accelerate if gold’s paper market liquidation continues while institutional crypto flows remain constructive. I would closely monitor this dynamic as the conflict grinds on.

Emir Ibrahim, Analyst

Spot Desk

The U.S. – Israel – Iran war is the primary macro driver – and the markets are highly sensitive to the headlines – with sentiment shifting rapidly on each escalation/ de-escalation update. Oil is the key driver across all asset classes right now, and developments in the Middle Eastern conflict are essential for the outlook of the global economy.

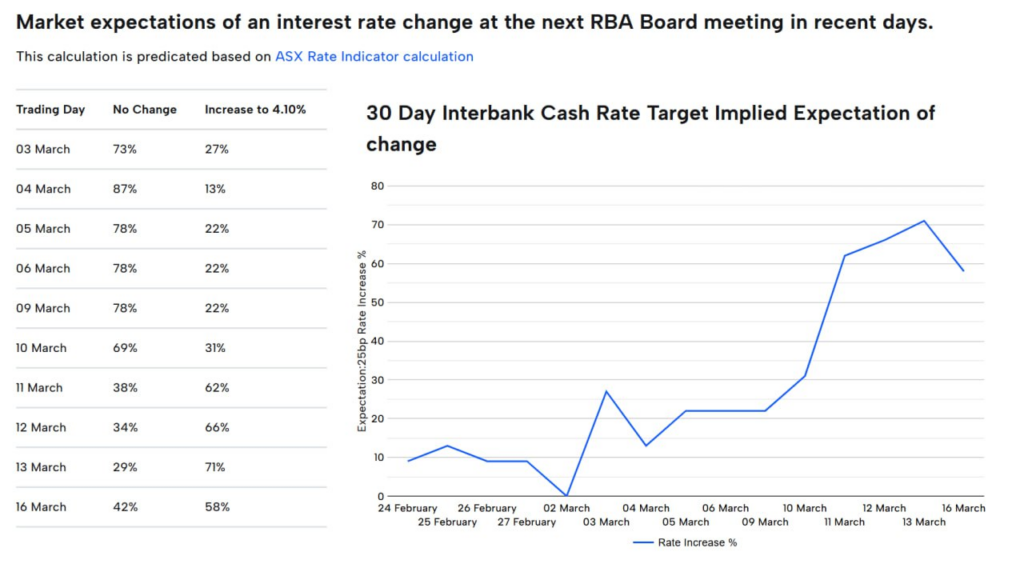

Locally in Australia, there were some interesting movements in the implied probabilities in market expectations of an interest rate change leading up to the RBA’s interest rate decision on the 17th, directly related to the war and the outlook for Oil. Early in the month, the market was pricing in a modest 27% chance of a 25 basis point increase in the cash rate. As the conflict in the Middle East developed, there were some concerning shifts in probabilities as the market began to lean towards an increase.

Source: https://www.asx.com.au

The cash rate was ultimately lifted to 4.10% on the 17th, and for the RBA, the market is still pricing a hawkish path – with current data indicating a 72% chance of another hike to 4.35% in May. The Aussie Dollar is being capped by the stronger U.S. Dollar, struggling to hold above the 0.70 handle. Additionally, fears that a prolonged oil shock that could hurt global growth and reduce Australia’s terms of trade despite local policy support is further adding pressure to the currency.

On the desk, flows in BTC, ETH and SOL were skewed on the bid, with SOL attracting particularly strong interest from clients. Activity in smaller-cap altcoins remained relatively muted – although we observed clients utilising TWAPs to gradually exit positions while minimising market impact.

In stablecoins, USDT/USD and USDC/USD flows were primarily on the bid, consistent with our flows over the past months. We noticed a decline in AUDD trading activity, although we do not expect this to develop into a sustained trend. We have excellent liquidity in AUDD, so please do not hesitate to come through the live chat in the Zerocap portal to discuss any enquiries surrounding AUDD.

Our USDT/AUD book was more balanced this week, with a modest skew to the offer – characterised by higher frequency lower volume buy side orders, versus the less frequent but larger tickets on the bid. Across other fiat currencies, NZD and EUR were the most actively traded, with NZD predominately being bought while EUR experienced more selling pressure.

The OTC desk continues to offer tailored cryptocurrency liquidity solutions and competitive pricing across majors, stablecoins, and altcoins, paired with key fiat currencies. With T+0 settlement, we ensure seamless trading and settlement.

Oliver Davis, OTC Trader

Derivatives Desk

WHOLESALE INVESTORS ONLY

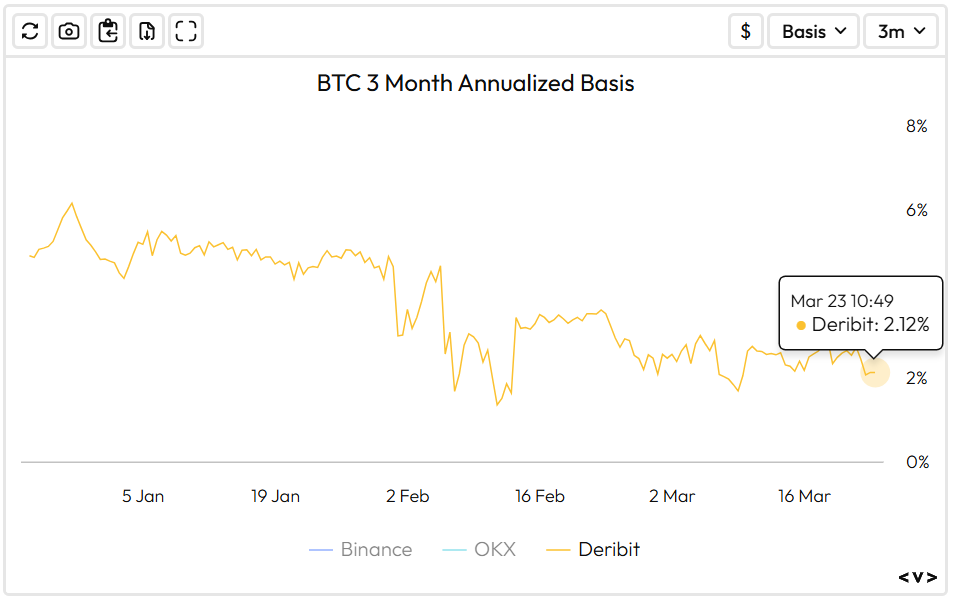

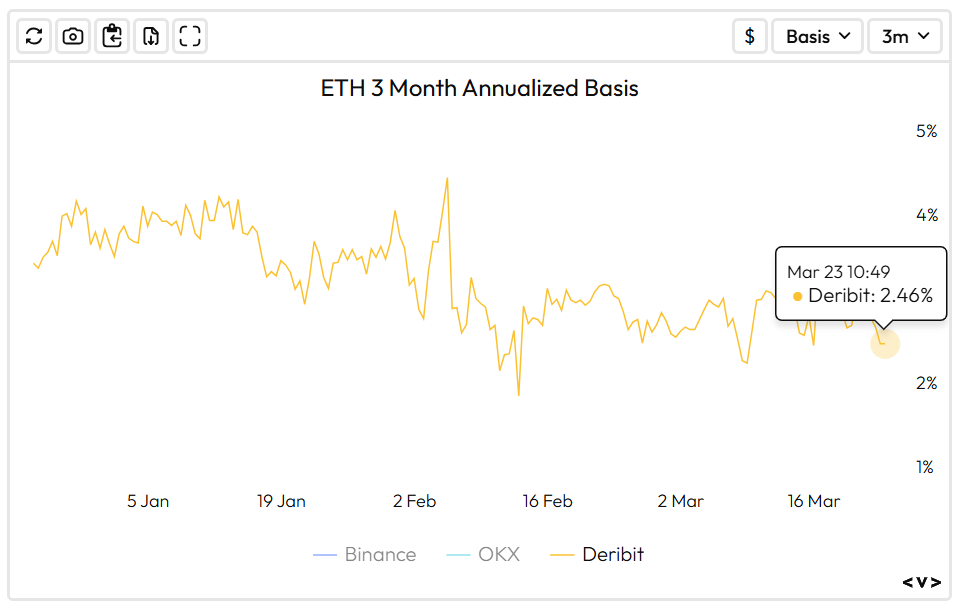

We are observing a rare decoupling in the basis markets: ETH is now yielding a higher basis rate than BTC, a reversal of historical norms. Despite the inherent ‘staking yield’ hurdle that typically discounts ETH futures, ETH’s 90-day annualized rate expanded by 22 bps this week to 2.46%, while BTC continues to trend toward multi-year lows at 2.15%.

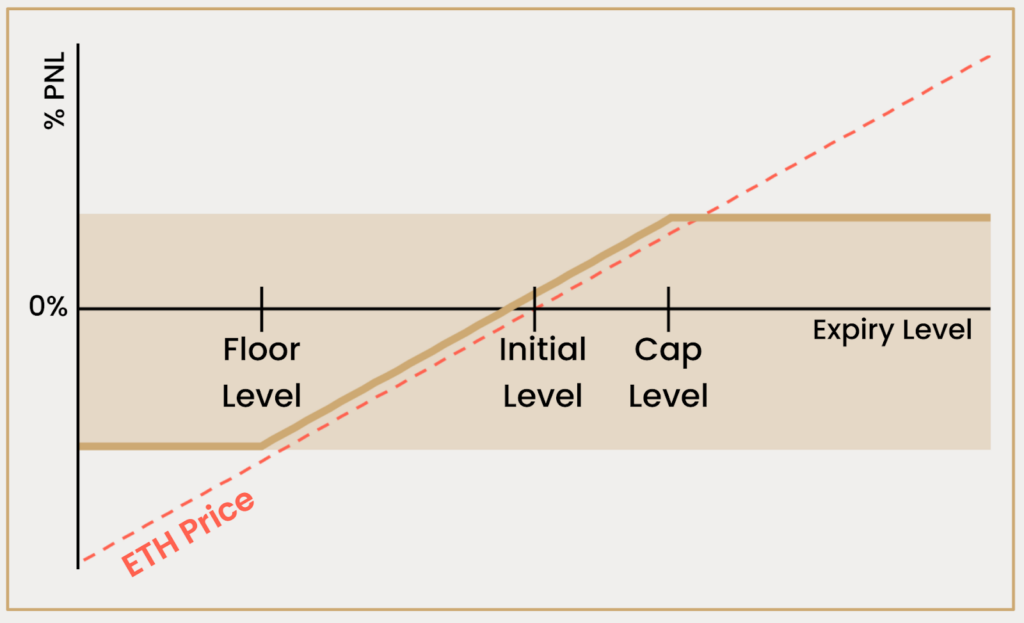

This Week’s Trade Idea – ETH Zero-Cost Collars

With global turbulence anticipated this week across global markets, now might be the time to lock in downside protection on crypto positions while maintaining upside participation.

Trade Idea: ETH Zero-Cost Collars

Zerocap can structure a Zero-Cost Collar on ETH with:

- Downside protection at USD $1,500 (guaranteed sell price if ETH settles below USD $1,500 at expiry).

- Capped upside at USD $3,400 (receive USD $3,400 if ETH settles above this level at expiry).

- Expiring end of September 2026.

This structure allows investors to secure a floor (price protection) on their holdings while still participating in potential further upside — all at zero upfront premium.

Trade Recommendation and Payoff Structures

- Implement a Zero-Cost Collar on ETH – a simple options strategy to simultaneously limit downside and cap upside at zero net cost.

Mechanics of the Collar

- Protective Put at USD $1,500 – this ensures a minimum floor: regardless of how far ETH might drop, the investor retains the right to sell at USD $1,500 at expiry.

- Covered Call at USD $3,400 – this caps the upside. The premium from writing the call offsets the cost of the put.

Payoff Profile:

- If ETH ≤ USD $1,500 at expiry → downside is fully hedged; the investor sells at USD $1,500.

- If USD $1,500 < ETH < USD $3,400 → they capture spot market gains (ETH trade value minus option costs = zero upfront cost).

- If ETH ≥ USD $3,400 → maximum payoff is capped at USD $3,400.

Risk Considerations:

- Opportunity cost: Upside beyond $3,400 is foregone for downside protection.

- Regulatory shifts: New laws (GENIUS Act, Project Crypto) may drive sudden shifts in ETH price or volatility.

- Alternative altcoin moves: Unexpected narratives (e.g., revenue meta/Ai hype) could redirect capital away from ETH, increasing relative risk towards downside.

Why the Collar Makes Sense Now:

- Secures present gains while retaining material upside.

- Neutral capital deployment: No immediate net premium means the investor doesn’t deploy additional funds while locking a favorable risk profile.

What to Watch

TUE: JP Inflation Rate YoY

WED: U.S. API Crude Oil Stock Change, AU Inflation Rate (MoM, YoY), AU RBA Trimmed Mean CPI (MoM, YoY)

THU: U.S. EIA Crude Oil Stocks Change, U.S. EIA Gasoline Stocks ChangeFRI: FED governors Miran, Jefferson and Barr speeches

Contact Us

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at [email protected]

DISCLAIMER

Zerocap Pty Ltd carries out regulated and unregulated activities.

Spot crypto-asset services and products offered by Zerocap are not regulated by ASIC. Zerocap Pty Ltd is registered with AUSTRAC as a DCE (digital currency exchange) service provider (DCE100635539-001).

Regulated services and products include structured products (derivatives) and funds (managed investment schemes) are available to Wholesale Clients only as per Sections 761GA and 708(10) of the Corporations Act 2001 (Cth) (Sophisticated/Wholesale Client). To serve these products, Zerocap Pty Ltd is a Corporate Authorised Representative (CAR: 001289130) of AFSL 340799

This material is intended solely for the information of the particular person to whom it was provided by Zerocap and should not be relied upon by any other person. The information contained in this material is general in nature and does not constitute advice, take into account financial objectives or situation of an investor; nor a recommendation to deal. . Any recipients of this material acknowledge and agree that they must conduct and have conducted their own due diligence investigation and have not relied upon any representations of Zerocap, its officers, employees, representatives or associates. Zerocap has not independently verified the information contained in this material. Zerocap assumes no responsibility for updating any information, views or opinions contained in this material or for correcting any error or omission which may become apparent after the material has been issued. Zerocap does not give any warranty as to the accuracy, reliability or completeness of advice or information which is contained in this material. Except insofar as liability under any statute cannot be excluded, Zerocap and its officers, employees, representatives or associates do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this material or any other person. This is a private communication and was not intended for public circulation or publication or for the use of any third party. This material must not be distributed or released in the United States. It may only be provided to persons who are outside the United States and are not acting for the account or benefit of, “US Persons” in connection with transactions that would be “offshore transactions” (as such terms are defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)). This material does not, and is not intended to, constitute an offer or invitation in the United States, or in any other place or jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or invitation. If you are not the intended recipient of this material, please notify Zerocap immediately and destroy all copies of this material, whether held in electronic or printed form or otherwise.

Disclosure of Interest: Zerocap, its officers, employees, representatives and associates within the meaning of Chapter 7 of the Corporations Act may receive commissions and management fees from transactions involving securities referred to in this material (which its representatives may directly share) and may from time to time hold interests in the assets referred to in this material. Investors should consider this material as only a single factor in making their investment decision.

Past performance is not indicative of future performance.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

AI Tokens Now Available on Zerocap

Decentralised AI tokens are emerging as one of the most compelling investment themes of this crypto cycle. A new class of blockchain-native protocols has been

Weekly Crypto Market Wrap: 16 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 10 March 2026

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.