Content

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the significant developments in the Federal Reserve's monetary policy, and how did they impact the crypto market?

- How did the global macroeconomic environment affect cryptocurrencies, especially Bitcoin and Ethereum, during the week?

- What are the latest updates on Ethereum's transition to Proof of Stake, and how might it impact the market?

- What are some notable trends and innovations in the DeFi space, and how are major companies and governments responding?

- What are the key factors to watch in the coming weeks that could influence the crypto market?

- Disclaimer

21 Mar, 22

Weekly Crypto Market Wrap, 21st March 2022

- Week in Review

- Winners & Losers

- Macro Environment

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the significant developments in the Federal Reserve's monetary policy, and how did they impact the crypto market?

- How did the global macroeconomic environment affect cryptocurrencies, especially Bitcoin and Ethereum, during the week?

- What are the latest updates on Ethereum's transition to Proof of Stake, and how might it impact the market?

- What are some notable trends and innovations in the DeFi space, and how are major companies and governments responding?

- What are the key factors to watch in the coming weeks that could influence the crypto market?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- Federal Reserve officially approves first interest rate hike in more than three years:

- The hike is 0.25 percentage points.

- Market and FED’s dot plot prices have factored in hikes during each and every one of the six remaining Fed meetings of 2022.

- Fed Governor Waller states 0.5% rate hikes may be needed as “inflation is raging.”

- Forward expectation by FED dot plot projects up to 11 rate hikes through to the end of 2023.

- Bank of England hikes rates for third time in a row, taking current official cash rate to 0.75% – inflation at risk of hitting multi-decade high.

- European Union’s proposal to limit Proof of Work cryptos like Bitcoin in the territory officially rejected in Parliament Committee vote.

- Ukraine officially legalises cryptocurrencies as donations continue to pour into the nation. The Ukrainian government launches a crypto donation website in partnership with FTX, Everstake and Kuna.

- Ethereum’s “Merge” update taking the network from Proof of Work to Proof of Stake passes tests, nearly ready to go live.

- Ethereum’s co-founder Vitalik Buterin named “Prince of Crypto” in TIME Magazine’s upcoming cover and interview, says crypto has an image problem and important projects are being overtaken by quick profits.

- Reserve Bank of India releases another bulletin calling for ban on all cryptocurrencies as they threaten local sovereignty and the rise of India as a global power.

- Over 100 illegal crypto mining farms shut down in Kazakhstan after a recent police raid.

Winners & Losers

Macro Environment

- Despite global scale geopolitical concern, both the US Federal Reserve and Bank of England hiked their official interest rate this week. It’s the third round of normalisation for the UK central bank, which makes the Fed a bit behind the curve in a relative sense. After over a decade of monetary stimulus, both via traditional and extraordinary means, the world is now looking at an era of tightening liquidity in response to runaway inflationary expectations. The only major economy that’s going against the trend at the moment is China, which loosened its monetary policy in response to supply-side disruption due to its close trade link with Russia, which is under heavy international sanction over its war in Ukraine.

- The credit market saw plenty of volatility this week. First, we have the base USD yield pushing to levels not seen since the taper tantrum of 2019. Ten-year UST yield hit a high of 2.24% this week, following a false retracement as geopolitical concerns pushed aside inflationary expectations and dropped to 1.68% recently. In addition to a higher base rate, credit spreads have widened out as the result of the Russian debt downgrade and talk of default on its USD obligations. On top of that, corporations are in a hurry to lock in their annual funding needs and costs by issuing fixed income papers through respective pipelines. All factors generate more supply than investor demands.

- The Japanese Yen has not been much of a headline in the trading world in recent years. The majority of forecasters had presumed little to no changes to BoJ’s QQE operations, and that interest rates will remain at between minus to zero percent for a long long time. USDJPY’s fair value expectation has been targeted at around 100 by most researchers and it has not been updated since the last decade. However, all these expectations have changed this week, and that makes “Mrs Watanabe” advisors very nervous. While inflation in the world’s third-largest economy is seen to exceed the 2% target in 2022, there is little appetite for the BoJ to shift its extraordinary eases monetary policy. That in line with the US Fed’s first move on normalising its interest rate curve had elevated USDJPY from its sleeping 100 average towards 120 level. Since the Japanese retail investor holds one of the world’s largest AUM books, a 20% depreciation in their balance sheet currency means a lot of money. Expectation from here is that once we reach between 125 to 130 levels, investment advisors will trigger the panic button and advise strategic hedging out of the YEN, thus forcing massive outflow into an alternative shelter, that in itself could be a huge turning point for cryptocurrencies.

- Economic data took a backseat this week as the central bank and Ministry of Finance department activities monopolised media headlines. The US published its monthly PPI data, which had met expectations of a 10% YoY increment. At the same time, in addition to the central bank normalisation moves mentioned above, China’s state council verbally intervened in both the stock and property market during the week. The so-called “Team China” is often made up of state-owned banks and brokerages which helps the authorities to buy and support the asset markets during periods of economic stress. This was what happened during the week, with both verbal and rumoured intervention to lift the asset markets. Some of the biggest tech stocks rallied as much as 20%, and the offshore Hang Seng Index jumped almost 10% in one day.

Technicals & Order Flow

Bitcoin

- Bitcoin started off with a brief re-test of 38,000 before bullish momentum drove subsequent price action. BTC broke 40,000 mid-week, continued to reach highs of 42,250 and closed out the week at the 42,000 level.

- Price action benefited from an improving geopolitical risk and regulatory climate. President Zelensky affirmed that Ukraine would not become a member of NATO. Additionally, Zelensky signed a bill legalising virtual assets in Ukraine.

- The Fed lifted rates by a quarter-point on Wednesday, coming in lower than expected, and signalled numerous hikes to come in 2022. Nonetheless, Bitcoin edged higher toward the latter part of the week following reassurance from Fed Reserve Chairman Jerome Powell, who stated the US economy was strong enough to weather tightening monetary policy.

- Bitcoin’s action was closely tied to that of equities. Notably, the geopolitical risk was dampened this week and monetary policy became the focus. On the back of this, we saw an increasing correlation with BTC and equities throughout this week.

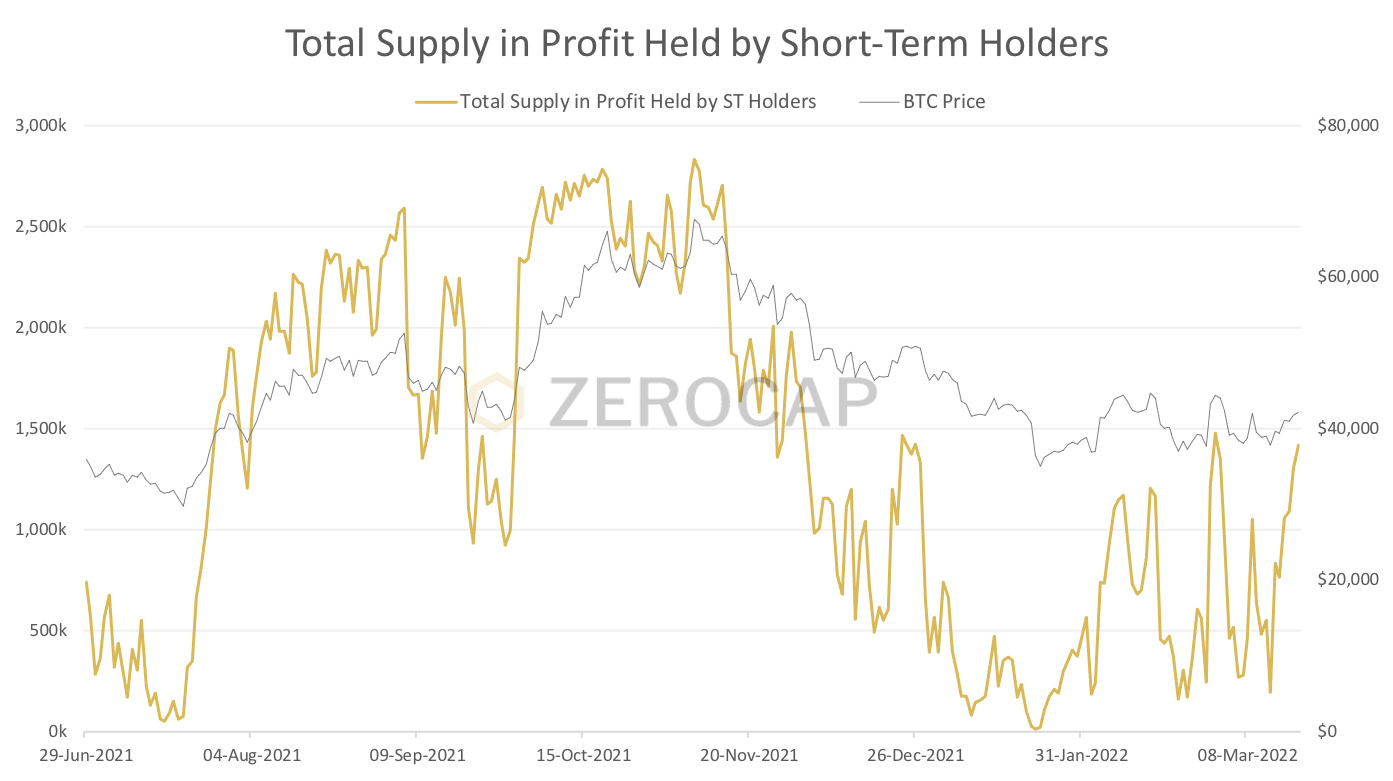

- Analysing on-chain data and specifically Hodler Net Position Change (which shows the monthly position change of long term investors), it can be seen that long term holders are taking advantage of current price levels and accumulating.

- Conversely, short term holders who have largely experienced losses since November 2021 caught a breath of fresh air this week. The recent up-move directly contributed to an increase in short term holder profit. It is likely that short term holder profit-taking, in the face of long term accumulation, could be the cause for the flattened price volatility apparent in the latter part of the week.

- Looking at options derivatives expiring March 25th, we can see significant levels for calls residing at 45k and 50k.

- This week, Bitcoin’s price action ran up off the back of diminished geopolitical tensions and positive announcements out of the Fed. Notably, equities moved in a similar fashion, bringing correlations back in line with recent moves. With a moderating risk environment, and the hiking cycle on the way, the next few months will be critical to understanding BTC’s role in this ever-evolving context.

Ethereum

- This week, Ethereum’s action favoured the bulls reaching highs slightly under 3,000, closing the week out around 2,850, a 13.5% return by comparison to the week’s open. Risk-on sentiment prompted a push to levels Ethereum last saw at the beginning of March.

- Like Bitcoin, Ethereum’s price action retained a high correlation with the Nasdaq, mirroring price moves throughout the week. Ethereum’s inherent risk-on characteristics will be pivotal to its return profile if markets are to eventuate higher.

- ETH is scheduled to complete its transition to PoS by the end of Q2 2022. That said, over 10.5m ETH is now locked in Ethereum’s Eth 2.0 Staking contract. As we edge closer to the finalised transition, we may see investors look to accumulate in preparation for what is suggested to be a more secure, sustainable and scalable model. Importantly, supply dynamics are shifting which should create buoyancy.

- In line with its historical behaviour, this week ETH outperformed BTC in the presence of risk-on sentiment. Ethereum’s market capitalization climbed to $345bn, outpacing Bitcoin’s price appreciation. As a result, ETH’s market dominance grew by 18.86%. Upward resistance at 0.0720 will act as a key hurdle for any further price appreciation between the pair.

ETHBTC Daily Chart

- This week there were sizable Ethereum outflows from exchanges, with an outflow on March 15th being the largest since July 2021. On the same day, an inflow of ETH of similar magnitude was made to the Lido platform. Lido is a liquid staking solution for Ethereum 2.0 and allows users who stake to monetise their staked assets. This behaviour plays into the aforementioned theme of accumulation.

- This week’s price appreciation resulted in a minor uptick in Ethereum short-term holder net unrealised profit/loss (NUPL). This metric assesses and showcases short-term investors’ profitability. The last time NUPL broke through zero was in late December 2021 when the price was above $4,000. Like Bitcoin, Ethereum’s short term holders are feeling the pain.

- Since the start of 2022, stablecoin supply has grown by 21.8B. USDT is outperforming in terms of growth, having grown 51% since the start of the year. In terms of volume, USDC has expanded its supply by over 10B, contributing to nearly half of total supply expansion. The magnitude of growth this year can be attributed to a shifting market structure that is seeing DeFi and risk moves maintain assets within the cryptocurrency ecosystem – which is different to what we saw in 2018 on the back of blowoff tops. Stablecoins have clearly become a dominant safe-haven asset in the digital asset space.

- Ethereum’s outperformance, relative to BTC, in risk-on moves continues to prove true. Moving closer to the finalisation of its highly anticipated transition to its Proof-of-Stake consensus mechanism, Ethereum is growing in market capitalisation dominance and growing in the magnitude of ETH locked in its Eth 2.0 Staking contract.

- Ethereum’s short term price action will be dictated by the macro environment. Moving forward, if sentiment proves to be risk-off, it is likely we will see flows away from Ethereum into BTC and stablecoins. However, given the overarching theme of accumulation and the upcoming supply dynamics with the network upgrade, Ethereum will likely outperform if bullish sentiment persists.

DeFi & Innovation

- Instagram will soon have NFTs in the platform, according to CEO Mark Zuckerberg – Spotify also plans to add NFTs to its platform.

- Bank of Canada currently collaborating with MIT on CBDC research.

- City of Austin, Texas to research capabilities of using Bitcoin as a payment option.

- HSBC partners with metaverse platform Sandbox to offer educational finance games.

What to Watch

- Repercussions and potential statements from government officials and Fed governors on rate hikes.

- Statements from Fed Chair Jerome Powell, on Monday and Wednesday.

- UK’s CPI and statements from BOE’s Governor Bailey, on Wednesday.

- Upcoming updates on Ethereum’s Proof of Stake implementation.

FAQs

What were the significant developments in the Federal Reserve’s monetary policy, and how did they impact the crypto market?

The Federal Reserve officially approved the first interest rate hike in over three years, increasing it by 0.25 percentage points. The market has factored in hikes for all six remaining Fed meetings of 2022. Despite these changes, Bitcoin and other cryptocurrencies edged higher, benefiting from an improving geopolitical risk and regulatory climate.

How did the global macroeconomic environment affect cryptocurrencies, especially Bitcoin and Ethereum, during the week?

The global macroeconomic environment, including interest rate hikes by the US Federal Reserve and Bank of England, affected cryptocurrencies. The Japanese Yen’s depreciation and China’s loosening of monetary policy also influenced the market. Bitcoin started with a re-test of 38,000 and reached highs of 42,250, while Ethereum favored bullish trends, reaching highs slightly under 3,000.

What are the latest updates on Ethereum’s transition to Proof of Stake, and how might it impact the market?

Ethereum’s “Merge” update, taking the network from Proof of Work to Proof of Stake, has passed tests and is nearly ready to go live. Over 10.5 million ETH is now locked in Ethereum’s Eth 2.0 Staking contract. The transition is expected to create a more secure, sustainable, and scalable model, potentially leading to increased accumulation and market buoyancy.

What are some notable trends and innovations in the DeFi space, and how are major companies and governments responding?

Innovations in the DeFi space include Instagram and Spotify’s plans to add NFTs to their platforms, the Bank of Canada’s collaboration with MIT on CBDC research, and HSBC’s partnership with metaverse platform Sandbox. Cities like Austin, Texas, are also exploring the use of Bitcoin as a payment option, reflecting growing interest and integration of crypto technologies.

What are the key factors to watch in the coming weeks that could influence the crypto market?

Key factors to watch include potential statements from government officials and Fed governors on rate hikes, statements from Fed Chair Jerome Powell, UK’s CPI and statements from BOE’s Governor Bailey, updates on Ethereum’s Proof of Stake implementation, and the overall macroeconomic environment. These factors could significantly influence the direction of the crypto market.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 14 Mar. 2022 0:00 UTC to 20 Mar. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Zerocap Shines at Blockies & Australian Crypto Convention

This past weekend marked a significant milestone for Zerocap as we participated in two of Australia’s premier crypto events: the prestigious Blockies Awards and the

Weekly Crypto Market Wrap: 25th November 2024

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Weekly Crypto Market Wrap: 18th November 2024

Zerocap is a market-leading digital asset firm, providing trading, liquidity and custody to forward-thinking institutions and investors globally. To learn more, contact the team at

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.