Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the major events in the crypto market during the week of 8th November 2021?

- How did Bitcoin and Ethereum perform during the week?

- What were the trends in the macroeconomic environment affecting crypto?

- What are the technical insights for Bitcoin and Ethereum?

- What are some notable developments in DeFi and Innovation?

- Disclaimer

8 Nov, 21

Weekly Crypto Market Wrap, 8th November 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the major events in the crypto market during the week of 8th November 2021?

- How did Bitcoin and Ethereum perform during the week?

- What were the trends in the macroeconomic environment affecting crypto?

- What are the technical insights for Bitcoin and Ethereum?

- What are some notable developments in DeFi and Innovation?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- US Federal Reserve’s tapering confirmed to begin in late November, with monthly reductions of $10B in Treasury and $5B in mortgage-backed securities purchases.

- US’ House of Senate passes $1T infrastructure bill to be delivered for US President Biden’s approval – document requires all crypto transactions over $10k to be reported to the IRS.

- Bank of England’s Monetary Policy report expects higher inflation and the need for increased rates, but failed to deliver the hike during a highly anticipated meeting.

- A new US’ Treasury report calls for “urgently needed” legislation of stablecoins – SEC no longer set to have regulatory monopoly over stablecoins, urging Congress to act.

- First Australian crypto stock based ETF smashes records on opening day on the ASX.

- Commonwealth Bank to enable crypto trading for its retail clients.

- Seven of Australians 87 richest entrepreneurs under 40 are crypto founders; AFR.

- New Miami and New York mayors vow to take their first paychecks entirely in bitcoin.

- US’ institutional managers bought $2B worth of bitcoin in October.

- Ethereum sees first consecutive week of deflationary issuance – $65M ETH burned daily.

- US’ Congressmen send requests for SEC’s Gary Gensler demanding spot BTC ETFs.

- NYDIG acquires bitcoin micropayments firm Bottlepay.

- Binance to spend $115 million in France to develop the European crypto ecosystem.

Winners & Losers

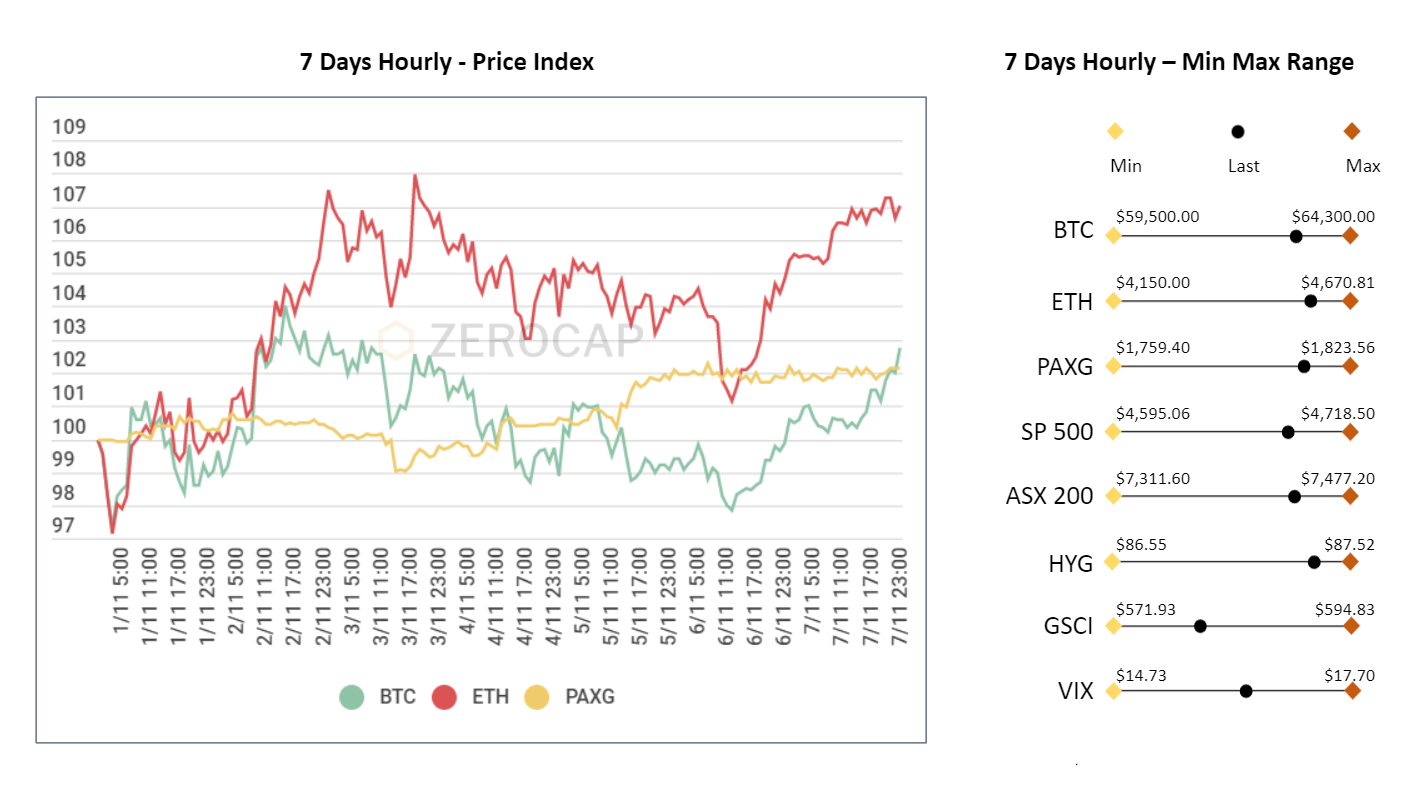

- Crypto markets saw high volatility across the board with continued gains across a number of subsectors. Bitcoin spent the week consolidating, with multiple leverage wipeouts for overleveraged participants. Despite continued headlines, newsflow appeared to have limited impact on the asset’s price action (until Sunday 7th – we are currently seeing a rally as we put this together.). ETH continued to set new ATHs throughout the week outperforming BTC. Overall, BTC returned 3.17% and ETH 7.57%.

- U.S. stocks hit another all-time high, with tech shares outperforming once again. With reduced expectations of immediate tightening from developed nations, the Bank of England surprised the market, helping to lower equity discount funding. Nasdaq 100 has been on an upward trend for ten straight trading days, and S&P 500 achieved five consecutive weekly gains.

- Macroeconomic data was generally positive, with the week ending on strong Non-farm payroll data from the U.S. The U.S. unemployment rate dropped to 4.6%, while average earnings were as expected at 4.9%. Previous month’s job gains were revised upwards, making the figure even stronger. Data counts were more mixed from China, as both export and import figures rose strongly, PMI slowdown had weighed on the asset markets in Asia. Domestically, several Australian mortgage lenders raised their fixed rate home loan rates following RBA’s failure to follow through with their three-year bond buying. One bank increased its two-year fixed mortgage rate by 50bp during the week.

- The bond market rallied on the back of dovish Bank of England commentary, despite a stream of hints towards early normalisation of interest rates. Ten year U.S. yield dropping from above 1.60% to a low of 1.45% by week’s end. At the same time, 30 year dropped from 2.04% to a low of 1.88%. On the credit front, the worry over Chinese property developers’ repayment ability has spilled over to builders and financial institutions associated with the industry. One example was Fujian province-based Yango Group Co. Ltd went into repayment extension talks with credits in their RMB denominated bonds during the week.

- The VIX index remained subdued as expected following another strong U.S. equity run. Cryptocurrency vol also retraced lower after a short period of consolidation in BTC and ETH throughout the week. The market is now anticipating the next leg of the run towards a Christmas trend; thus, actual volatility will likely start to catch up soon.

- Oil prices retraced lower from a seven-year high as the market’s anticipation of certain supply ports to run dry failed to materialise. Gold could not take advantage of stronger inflation data during the week but did follow through higher as the DXY weakened after yields dropped.

Macro, Technicals & Order Flow

Bitcoin

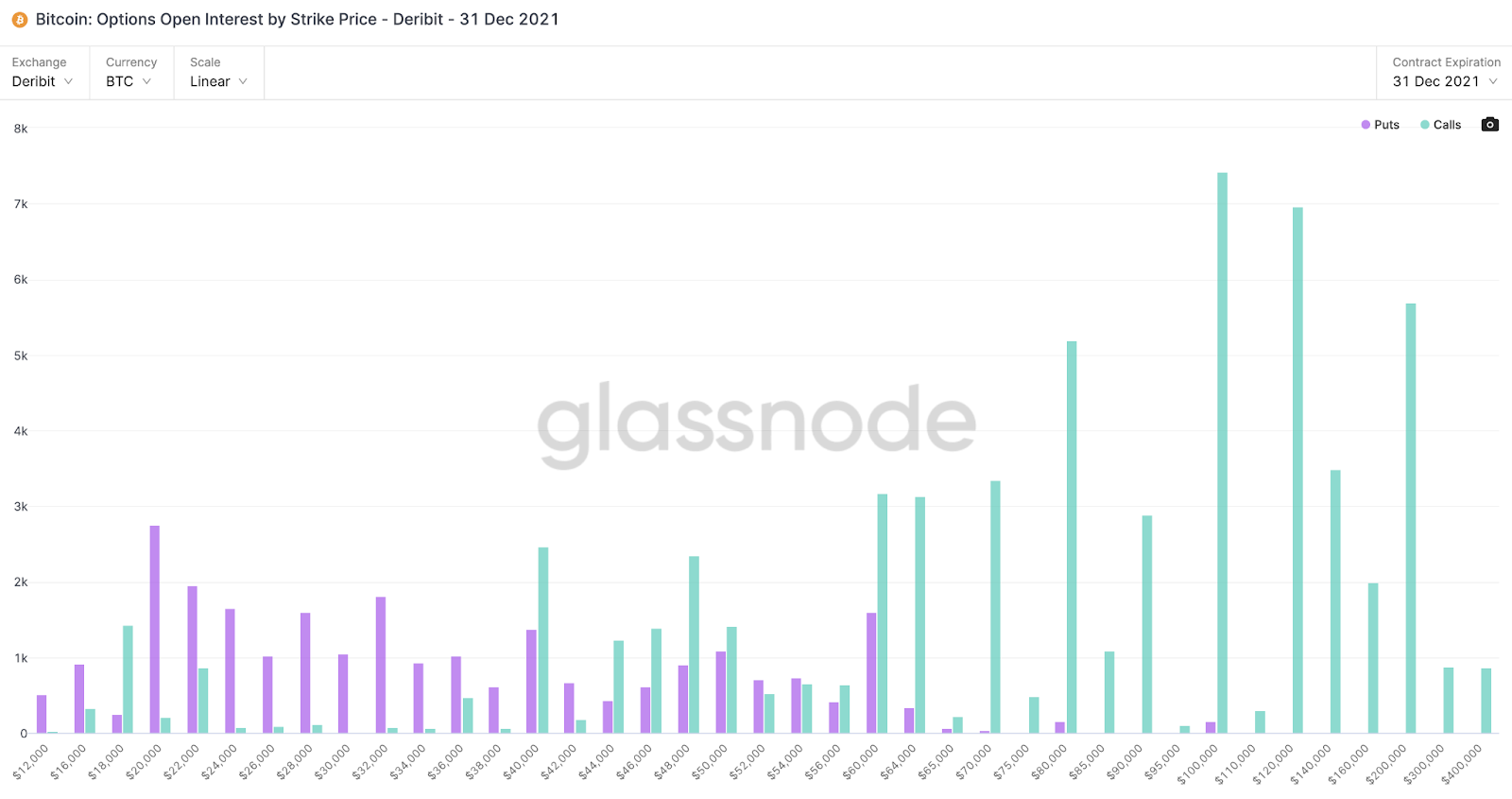

- We were gunning for a topside break on macroeconomic factors and strong optionality aiming for the 70,000 level. We got the break on Sunday, and are now seeing strong follow-through. There is no resistance from here to the highs, and Europe is waking up after a weekend of digesting the dovish Central Bank rate hold. A break of all-time highs could be on the cards this week.

- The derivatives markets are favouring 100,000 strikes before Dec 31 – which is a real stretch, but indicative of building sentiment.

OI Interest by Strike – Dec 31, 2021

- The bid by funds continues to rise, steadily accumulating. However, we are seeing the total supply held long-term holders begin to roll over. This has been a very strong accumulation period since the fall in May.

Bitcoin Held By Funds

Bitcoin: Total Supply Held by Long-Term Holders

- On-chain data is showing net-outflows from exchanges, with velocity accelerating (indicating a contraction in supply). We are still at a moderate level here, with room to further contain supply. This bodes well for a topside break.

Bitcoin Net Position Change

- The on-chain UTXO price distribution shows the depth of bitcoin activity at certain price levels. Last week, we had built some near term levels up to 64,000, but above 64,000 we positioned a clean run to break highs. This thesis is playing out for now, with the 64,000 level providing a quick move above. UTXO is now showing very little activity, which coincides with the chart gap at these levels previously. The barrier to a break won’t be orderflow driven, but rather newsflow.

UTXO Realised Price Distribution

- The futures basis curve continues to hold above the 15% level across derivative exchanges, although the CME is showing increased volatility. This could be a function of balancing requirements on the ETF, and the sudden volume increases BTC futures on the CME. Open interest across exchanges remains predictably elevated at current price levels.

BTC Futures Annualised Rolling 1 Mth Basis

Bitcoin Futures Open Interest

- Perpetual funding rates have had a few resets this week, with some liquidations today on the current break higher. Despite short-term liquidations throughout the week, the current estimated leverage ratio (which tracks spot balances on exchanges vs the current open interest in derivatives) is relatively contained, suggesting that it’s unlikely that we get too many exacerbated liquidations against the current leverage structure this week.

BitMEX BTC Perpetual Liquidations Mon 08/11/21

BTC Perpetual Swaps Funding

Bitcoin Futures Estimated Leverage Ratio

- In summary, the thesis continues to play out on bitcoin. The Commonwealth Bank news here in Australia has made some huge waves, with other financial institutions keenly eyeing the space. When you look at the adoption curve across, we are still very early on legacy financial institutions adopting frameworks for crypto asset adoption. As we mention most weeks, the big test will be a stagflationary environment – which we believe will lead to widespread traditional firm allocation in BTC as the hedge.

Ethereum

- Last week we called for a break of highs from ethereum given the momentum behind the risk environment. This has clearly been another positive risk week for risk assets, bringing ETH to a break of highs early on in the week, with momentum building above the top now. Open interest has clearly been focused on the 5,000 psychological level. Our OTC desk is seeing profit taking between 4,800 and 4,950 with some trades playing the break above 5,000. It’s a huge milestone for the asset to be at these levels, and the entire space will be cheering on a break.

ETH Open Interest by Strike: Dec 31, 2021

- We are again seeing strong outflows from exchanges (indicating contraction in supply).

- On-chain data is continuing to show larger wallet holders with supply held of 10 to 100 ETH continuing to increase, although this is beginning to slow. Smart money is still accumulating, with a focus on the ETH 2.0 rollout as the investment case.

Ethereum Exchange Net Position Change

Supply Held by Wallets with Balances of 10-100 ETH

- Perpetual funding rates, like BTC, are relatively moderate compared to where price action is.

ETH Perpetual Swaps Funding

- The futures basis curve is holding steady, but seeing some wild volatility on the CME – coinciding with the launch of ‘micro-futures’. Price discovery is definitely in focus here on the CME, with lots of expectation around the next potential ETF.

ETH Futures Annualised Rolling 1 Mth Basis

- Institutional interest in ETH continues to grow, furthering this case. The Grayscale AUM is on an absolute tear.

Ethereum Grayscale AUM

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,180,759. This represents 6.92% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- Despite all the focus on disruptive blockchain protocols, ETH is still clearly in the lead when it comes to adoption and protocol revenue. Couple this with JP Morgan’s recent take that ETH is a better inflation hedge than BTC, and you have the potential for continued upside into Q1 next year. We disagree with JPM’s take on this, but hope they are right!

Protocol Revenue (cryptofees.info)

DeFi & Innovation

- Layer-2 and multi-chain DeFi platforms saw record inflows in October.

- Bitcoin network is ready to have its Taproot update starting in the next seven days.

- AAVE’s V3 update ready for voting approval – targets cross-chain supplied liquidity.

- El Salvador set to build 20 public schools with surplus from bitcoin trust.

- BitMEX exchange goes carbon-neutral, also vowing to offset all carbon from bitcoin transactions in and out of the platform.

- Burger King partners with Robinhood to offer free BTC, ETH or DOGE with meal purchases.

What to Watch

- A consensus in the US for regulatory oversight – SEC, Treasury and Congress still lack a clear understanding of which agencies will oversee crypto regulations. With SEC’s previous stablecoin regulation leadership now allegedly withdrawn, will there be another proposal over the upcoming week?

- Fed Chair Powell speeches – set to speak in two conferences this week, we expect Powell to provide more details regarding tapering and its timeline – set to conclude in mid 2022.

- Bitcoin’s Taproot update – Its first network update since August 2017, Bitcoin’s Taproot will begin implementation in the next 7 days and is set to conclude on November 14th if things run smoothly.

- US’ October Consumer Price Index – released on Wednesday.

FAQs

What were the major events in the crypto market during the week of 8th November 2021?

The week saw several significant events, including the US Federal Reserve’s tapering confirmation, the passing of a $1T infrastructure bill in the US, the Bank of England’s Monetary Policy report, and the launch of the first Australian crypto stock-based ETF. Additionally, there were developments related to stablecoins, crypto trading by Commonwealth Bank, and new mayors in Miami and New York vowing to take their paychecks in Bitcoin.

How did Bitcoin and Ethereum perform during the week?

Bitcoin spent the week consolidating, returning 3.17%, while Ethereum set new all-time highs, outperforming Bitcoin with a return of 7.57%. Ethereum also saw its first consecutive week of deflationary issuance, with $65M ETH burned daily.

What were the trends in the macroeconomic environment affecting crypto?

The macroeconomic data was generally positive, with strong Non-farm payroll data from the U.S. and a drop in the U.S. unemployment rate to 4.6%. The bond market rallied on dovish Bank of England commentary, and oil prices retraced lower from a seven-year high. There were also concerns over Chinese property developers’ repayment ability.

What are the technical insights for Bitcoin and Ethereum?

Bitcoin broke on the upside, aiming for the 70,000 level, with strong follow-through and no resistance to the highs. Ethereum broke its highs early in the week, with momentum building above the top. Both assets showed strong outflows from exchanges, indicating a contraction in supply.

What are some notable developments in DeFi and Innovation?

Layer-2 and multi-chain DeFi platforms saw record inflows in October. Bitcoin’s Taproot update is set to begin in the next seven days. AAVE’s V3 update is ready for voting approval, targeting cross-chain supplied liquidity. BitMEX exchange went carbon-neutral, and Burger King partnered with Robinhood to offer free crypto with meal purchases.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 1 Nov. 2021 0:00 UTC to 7 Nov. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Hong Kong Approves Spot Bitcoin and Ether ETFs

Hong Kong’s recent approval of the first spot Bitcoin and Ether exchange-traded funds (ETFs) marks a significant milestone in the financial industry. These approvals position

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.