Content

- Webinar: Mawson x Zerocap

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- Article

- FAQs

- What were the significant events in the crypto market during the week of 7th February 2022?

- How did Bitcoin and Ethereum perform during the week, and what were the key factors influencing their prices?

- What were the major winners and losers in the fixed income market, and how did the US employment data impact the market?

- What are the latest developments in DeFi and Innovation in the crypto space?

- What are the key events and trends to watch in the crypto market in the coming days?

- Disclaimer

7 Feb, 22

Weekly Crypto Market Wrap, 7th February 2022

- Webinar: Mawson x Zerocap

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- Article

- FAQs

- What were the significant events in the crypto market during the week of 7th February 2022?

- How did Bitcoin and Ethereum perform during the week, and what were the key factors influencing their prices?

- What were the major winners and losers in the fixed income market, and how did the US employment data impact the market?

- What are the latest developments in DeFi and Innovation in the crypto space?

- What are the key events and trends to watch in the crypto market in the coming days?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Webinar: Mawson x Zerocap

Join us for our upcoming Webinar with the Mawson Infrastructure Group on 10th February, 11 am – 12 pm AEDT. On one side, you have those interested to invest in Bitcoin infrastructure, picks-and-shovels or mining technology and on the other side you have those who want to own Bitcoin, invest in a fund, or Structured Product in the crypto space.

Speakers: Toby Chapple – Head of Trading at Zerocap, Nicholas Hughes-Jones – Chief Commercial officer at Mawson.

Week in Review

- Meta shares nosedive -26% after company published report of user decline, shedding up to $230B of its value in the worst single-day loss in all stock markets’ history – PayPal loses 25% also in one day as company reports pessimistic revenue forecasts for 2022.

- US president Biden’s America Competes Act passes the House of Representatives without the inclusion of provisions on crypto surveillance.

- US employment results were better than expected with 467k jobs added in January – JOLTS job openings climbed to a surprising 10.9 million openings against expected 10.3 million.

- Bitcoin had more transactions volume in Q4 2021 than all credit card networks combined for the entire year: NYDIG report.

- US lawmakers issue warnings for American tourists to “not accept any digital yuan” during their visits to the Winter Olympics – based on data privacy concerns.

- Russia’s official Kremlin records estimate that citizens own approximately $200B in cryptocurrencies.

- Facebook’s Meta joins Crypto Open Patent Alliance (COPA), vowing to make core crypto patents accessible to all.

- Mark Zuckerberg’s stablecoin project Diem officially shuts down.

- CoinShares report: Bitcoin mining accounts for 0.08% of world’s CO² production, with 49% of BTC mining coming from the US.

- Australian billionaire Andrew “Twiggy” Forrest takes Facebook to court over fraudulent crypto ads in the platform featuring his image.

Winners & Losers

- The fixed income market began the week attempting to rebound on both economic and geopolitical uncertainties. Yields on the ten year UST fluctuated between 1.78% to 1.86% for the majority of the week prior to the US employment report on Friday. The better than expected US Non-farm payroll data helped secure an affirmative March hiking cycle from the FEd and lifted the ten-year curve from 1.86% to a high of 1.99% during the trading session. Markets now have priced in a 50bp lift off during the March FOMC meeting, and bond prices are at their cheapest level since the beginning of 2020, just before the Pandemic risk selloff.

- Company earnings season continues in the US, and Amazon was one of the bright stars with a positive reporting card. The online retailer saw its shares surging by 10% after beating estimates. On the other hand, Meta platform had disappointed market analysts on their Q4 reporting. The stock lost over 26% of its value, accounting for almost USD 230 billion of market capitalisation (the biggest single move by a company ever). There was little to no activity out of Asian markets during the week of the lunar new year, but the S&P 500 had lifted from 4,325 to close more than 100 points higher for the week despite Meta’s selloff.

- This week, the anticipation and aftermath of trading on Friday’s US employment data dominated market volatility. The VIX eased off into the week from 28 towards low 24 levels, but bond and FX intraday volatility had maintained momentum. BTC and ETH vols were relatively contained, with BTC vol closing the week at low 70s and ETH at low 80s. Both Vol curves dropped by 7-10 vol during the week to fully recover to opening levels.

- The FX and commodity markets saw intraweek movements only to recover back to opening levels. USDJPY dropped from 115 to a low of 114.20 following Wednesday’s weak ADP data, only to close the week back above 115. AUD rallied from below 0.7000 to a high of 0.7160 before closing back in the mid 70 cents. RBA meeting gave little hint to when the first hike will emerge, but a flip from the Central bank on its promise not to normalise until 2024 initially induced short covering in the currency. Gold volatility crashed this week, with the market ranging between 1785 to 1810 for most trading. Despite a selloff in the bond market, thoughts of inflation led inflow did not materialise into the precious metals market.

Macro, Technicals & Order Flow

Bitcoin

- Bitcoin started this week out of the gates with an early push upwards where price consolidated around the 38,500 mark. The bulls and bears played around these levels until the release of ADP data on Wednesday, with missed expectations pushing BTC to its weekly low around 36,500. The release of Non-Farm Payroll data on Friday, beating expectations, provided stimulus for a strong upside move to 41,500, forming a near-perfect technical break, where BTC closed out the week.

- The bullish on-chain data is finally playing out with decidedly positive price action. Funding rates have shifted into the positives from where they had recently hovered near zero or were negative, outlining a change in short-term market sentiment.

BTC Perpetual Funding Rate

- URPD shows the prices in which BTC supply was last on-chain. Large volumes of BTC realised at certain levels can provide indication of support and resistance levels. Last week, we saw increased bids into the apparent weakness which have now formed solid support. A void between current levels and 47,000 has formed, creating a gap zone. If market conditions hold out, this is the path of least resistance higher.

UTXO Realised Price Distribution (URPD) – BTC

- Bitcoin 25-day skew depicts the difference between a 25-delta put and a 25-delta call in terms of implied volatility. Moves towards 0% from above like those experienced after Friday are suggestive of players making moves away from bearish plays and towards bullish plays, further contributing to the developing narrative.

BTC 25-Delta Skew

- Taking into consideration a potential shift in sentiment and growing support at lower levels, plays favouring the upside are growing in attractiveness especially when you consider the current cheaper levels of volatility in the options markets. All in all, we could be in for further upside from here.

BTC ATM Implied Volatility

Ethereum

- Despite persistently negative funding rates in the first half of the week, ETH set its weekly lows on open at 2,480. As anticipation surrounding the ADP and NFP employment data grew, ETH was subject to increased volatility, with a minor sell-off on Wednesday’s ADP report following the first job loss in the private sector since December 2020.

- Suppressed market expectations for Non-Farm Payroll figures following earlier results, were unexpectedly beaten by over 3 times, sparking an aggressive upside move across crypto assets. ETH gained over +10% in the following 24 hours, marking the weekly highs around 3,080. ETHBTC rallied following the release of employment data, aligning with our expectations that ETH outperforms BTC during on-risk moves.

ETHBTC Daily Chart

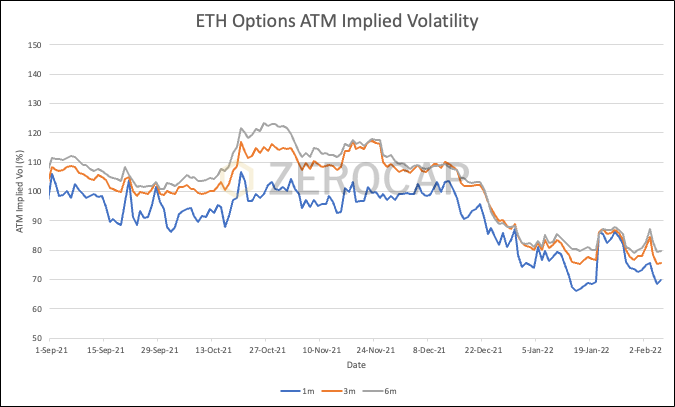

- Implied volatility fell during the upside move on Friday. It is now showing signs of potentially returning to pre-event levels. Notably (like BTC), options are becoming cheaper with time.

ETH ATM Implied Volatility

- Due to the significant mismatch between SLP minted (Smooth Love Potion – the in-game Axie Infinity token), SLP burned and the rapid growth of players from 38k in April 2021 to 2.7M in November 2021, SLP has been subject to hyperinflation. The increased selling pressure, caused by more frequent minting, has caused prices to drop over -95% since its highs in July 2021.

SLP’s Hyperinflation

- The start of 2022 has seen an influx of worldwide interest into NFT’s, with google trends illustrating the search term “NFT’” overtaking “Crypto”. Led by Asian nations such as Japan, Taiwan and South Korea, NFT’s have experienced major mainstream coverage and consistently rising volumes since the start of this year.

Worldwide Interest in search terms “Crypto” and “NFT”

- While net exchange outflows were evident early in the week, the double digit rally led to net inflows, implying some profit taking activities or caution in the latter half of the week, although the shift was not significant.

Ethereum Exchange Net Position Change

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 9,314,193. This represents 7.80% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- Despite ETH consistently outperforming BTC during risk-on moves, the continued rise and adoption of Layer 1 protocols has been a direct competition to ETH. However, with a planned transition into a Proof of Stake (PoS) blockchain in June 2022, Vitalik has also announced the integration of “blob-carrying transactions” in a near-future hard fork, aimed to increase scalability and reduce fees. While long-term fundamentals remain solid, short-term price action will likely be dictated by the release of inflation data later this week.

DeFi & Innovation

- US Court DeFi case: After a Tezos validator’s taxing battle, IRS decides that staking rewards will not be taxed until sold – validator declines refund, seeks to regulate staking rewards as “created property.”

- First cross-chain governance proposal passes on AAVE, a major step for the project’s adoption – AAVE is part of Zerocap’s DeFi Index product.

- Google’s Alphabet is reportedly exploring blockchain technology for flagship services.

- Ethereum x Solana bridge Wormhole loses $321 million in one of the biggest crypto hacks recorded.

- NFL to offer NFT Super Bowl tickets for upcoming event next Sunday.

What to Watch

- US CPI report, on Thursday.

- Russia x Ukraine ongoing tensions, which are not de-escalating.

- Meta and PayPal’s performance – where will the recent crash lead?

- Russia’s further statements on crypto regulations – an all-out ban is now very unlikely.

Article

Bitcoin is still the King, and here’s why:

In this article, Zerocap Research Analyst Parth Singhal explains the reasons why Bitcoin is still the King, even as the digital assets market grows into new proportions and functionalities for global finance.

FAQs

What were the significant events in the crypto market during the week of 7th February 2022?

Meta’s shares plummeted by 26%, PayPal lost 25% in one day, Bitcoin’s transaction volume in Q4 2021 surpassed all credit card networks for the year, and Russia’s citizens were estimated to own approximately $200B in cryptocurrencies. Additionally, Mark Zuckerberg’s stablecoin project Diem was shut down, and Bitcoin mining was reported to account for 0.08% of the world’s CO² production.

How did Bitcoin and Ethereum perform during the week, and what were the key factors influencing their prices?

Bitcoin started the week with a push upwards, consolidating around the 38,500 mark, and closed at 41,500. Ethereum set its weekly lows at 2,480 and marked the highs around 3,080. Factors like ADP data, Non-Farm Payroll data, and market sentiment played a role in their price movements.

What were the major winners and losers in the fixed income market, and how did the US employment data impact the market?

The fixed income market attempted to rebound on economic and geopolitical uncertainties. Yields on the ten-year UST fluctuated, and better-than-expected US Non-farm payroll data helped secure an affirmative March hiking cycle from the Fed. Amazon surged by 10%, while Meta lost over 26% of its value.

What are the latest developments in DeFi and Innovation in the crypto space?

A US Court decided that staking rewards will not be taxed until sold. AAVE passed its first cross-chain governance proposal. Google’s Alphabet is exploring blockchain technology, and Ethereum x Solana bridge Wormhole lost $321 million in a hack. Additionally, the NFL is offering NFT Super Bowl tickets.

What are the key events and trends to watch in the crypto market in the coming days?

Watch for the US CPI report, ongoing Russia x Ukraine tensions, Meta and PayPal’s performance, Russia’s statements on crypto regulations, and the release of inflation data. Also, keep an eye on the continued rise and adoption of Layer 1 protocols and Ethereum’s planned transition into a Proof of Stake blockchain.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 31 Jan. 2022 0:00 UTC to 6 Feb. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Ethereum Smart Contracts: How They Changed Crypto

Ethereum, launched in 2015, revolutionized the digital world by introducing “smart contracts,” self-executing contracts with the terms of the agreement directly written into code. This

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.