Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the major events in the crypto market for the week ending 4th October 2021?

- How did Bitcoin and Ethereum perform during the week?

- What were the significant developments in DeFi and Innovation?

- What are the key macro themes affecting equities and digital assets?

- What are the upcoming events to watch in the crypto market?

- Disclaimer

4 Oct, 21

Weekly Crypto Market Wrap, 4th October 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the major events in the crypto market for the week ending 4th October 2021?

- How did Bitcoin and Ethereum perform during the week?

- What were the significant developments in DeFi and Innovation?

- What are the key macro themes affecting equities and digital assets?

- What are the upcoming events to watch in the crypto market?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- Yellen warns that the United States government will run out of money by October 18 unless the debt ceiling is raised, despite a temporary measure to prevent government shutdown to December 2021. US’ House of Representatives delays vote on infrastructure bill.

- Japan and Germany each choose a new political leader, North Korea fires test missiles, Taiwan requests Australian intelligence aid given China’s accelerated military exercise within Taiwan’s jurisdiction.

- China’s Evergrande property Inc continues to weigh on global risk sentiment given the reluctance of servicing two offshore USD coupon payments on time. A grace period of 30 days begins prior to default.

- Federal Reserve Chair Jerome Powell says the US has no plans to ban cryptocurrencies.

- Global mega PE firm KKR joins the crypto space with its first blockchain investment on ParaFi Fund Stake.

- Europe becomes the largest crypto economy, with over $1 trillion in transactions in 2020.

- Morgan Stanley doubles exposure to bitcoin through Grayscale shares.

- US’ SEC delays decision deadline on four bitcoin ETF requests by 45 to 60 days.

- US’ CFTC charges 14 crypto businesses with failure to register as futures merchants, hits Kraken with $1.21 million in fines.

- IMF releases report recommending global standard for crypto regulations and CBDCs.

- New Zealand’s central bank issues a statement on the benefits of digital cash.

- Amazon, PayPal, Visa and Mastercard amongst companies that will aid the Bank of England on its CBDC research.

Winners & Losers

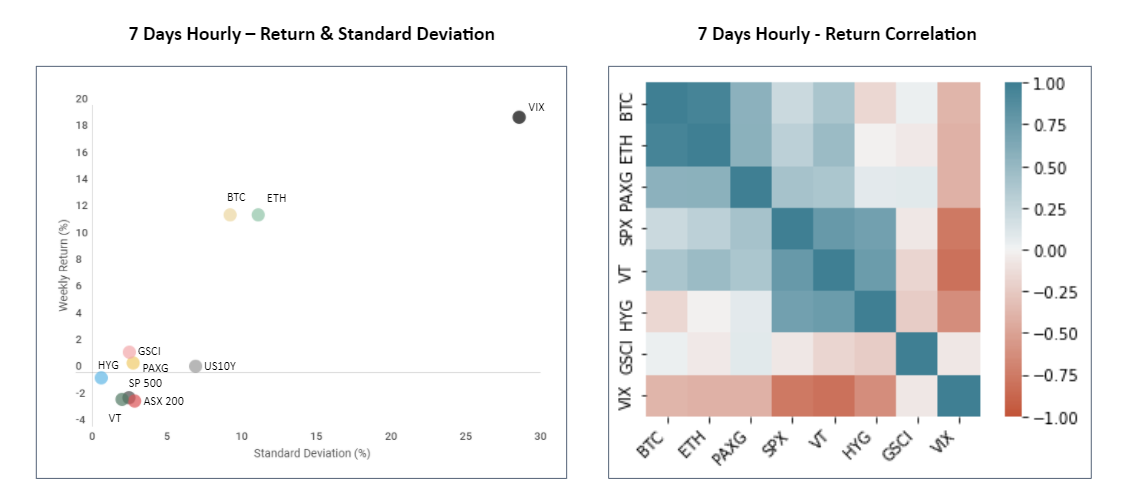

- Equities continued to fall as macro themes endured, the key drivers remain US economic stability; inflation, geopolitical risk around the APAC region, and asset purchase tapering risk. Value stocks outperformed growth this week as investors remain cautious by discounting the present valuation of the tech sector with a higher yield curve. PCE inflation was higher than expected, while housing starts and ISM beat forecasts. Stocks closing in the defensive but off the low for the week. The S&P 500 closed down -1.9%.

- The VIX was naturally higher against this backdrop, touching on an 18% rally for the week.

- Digital assets similarly faced early headwinds amid the fallout from China’s crackdown on crypto entities, however this was saved by Jerome Powell’s positive clarification that the US does not seek to ban the asset class. The crypto market was further buoyed by headlines – from traditional banks and hedge funds, to Tether’s RICO case being dropped, all leading to a swift recovery. Great to see the diversification of this asset class playing out this week! Overall BTC returned 11.75% and ETH returned 11.75% WoW.

- The US10Y saw its highest point since June earlier in the week as inflation concerns amplified, with US30Y reaching a high of 2.08%. Modest retracement into the weekend with the 10 year closing up 2bp at 1.47.

- Gold price fluctuated between stronger real yield and the safe haven inflow effect. WoW the asset secured a 0.61% gain.

Macro, Technicals & Order Flow

Bitcoin

- Last week saw the on-chain factors; long-term holders accumulating supply and net outflows from exchanges. We also felt that Evergrande’s potential for contagion was less possible than the media was positioning. What a difference a week can make – the broader markets instead took cues from the inflation spikes and supply chain constrictions – further dipping, alongside a higher VIX.

- Against this backdrop, the crypto markets took a run to the topside – breaking short-term correlations with intermarket risk. Key technical levels for BTC are the Sep highs at 53,000. There is optionality and general derivatives barriers at 50,000 – but a break of this, and we are gunning for a run above 53,000.

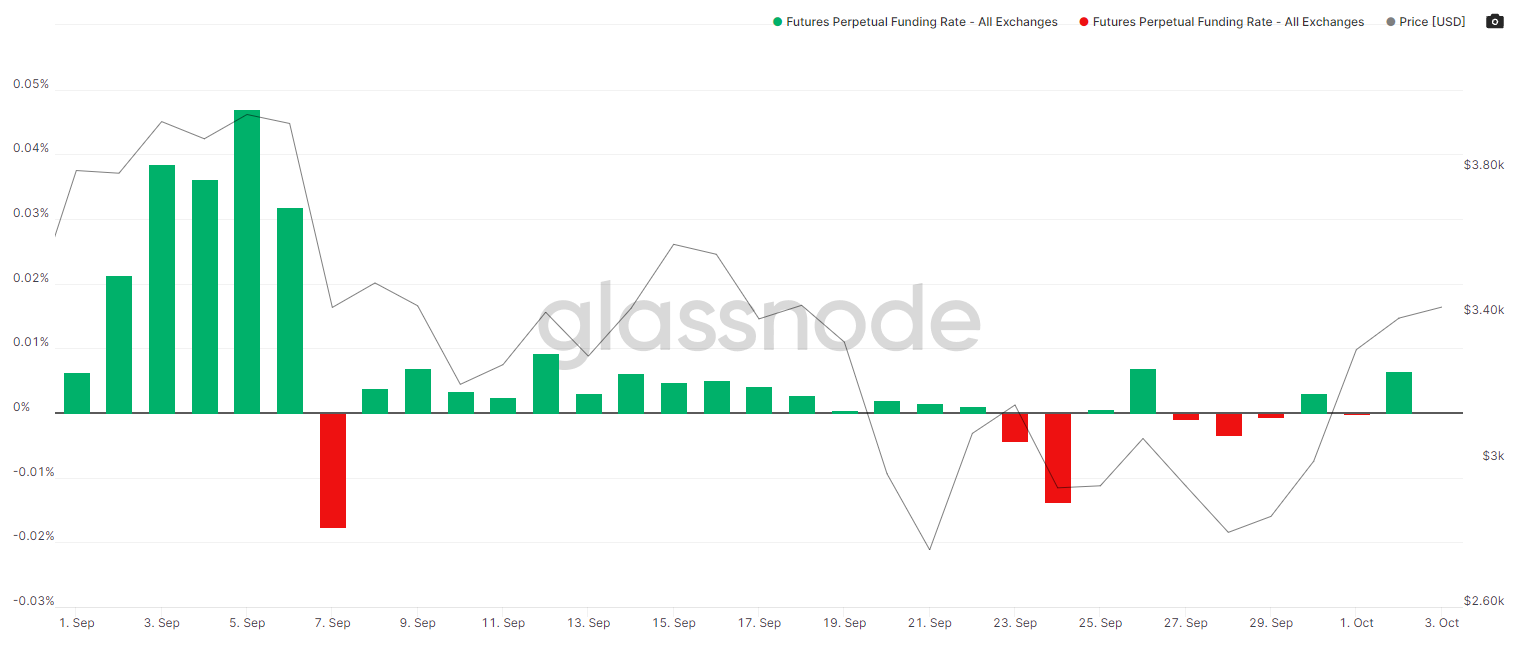

- Perpetual funding rates have turned positive, but not showing excessive leverage in the system.

BTC Perpetual Swaps Funding

Bitcoin Futures Estimated Leverage Ratio

- Institutional interest is on the move – fund flows have been building throughout September and Morgan Stanley has doubled its exposure to BTC via the Grayscale Trust. Although we are still showing a negative premium here – the hedge fund sellers seem to be absorbing any bullish inflows at this stage.

Bitcoin Held By Funds

Grayscale BTC Trust Premium

- On-chain data still showing that long-term holders continue to accumulate against this rally

Bitcoin: Total Supply Held by Long-Term Holders

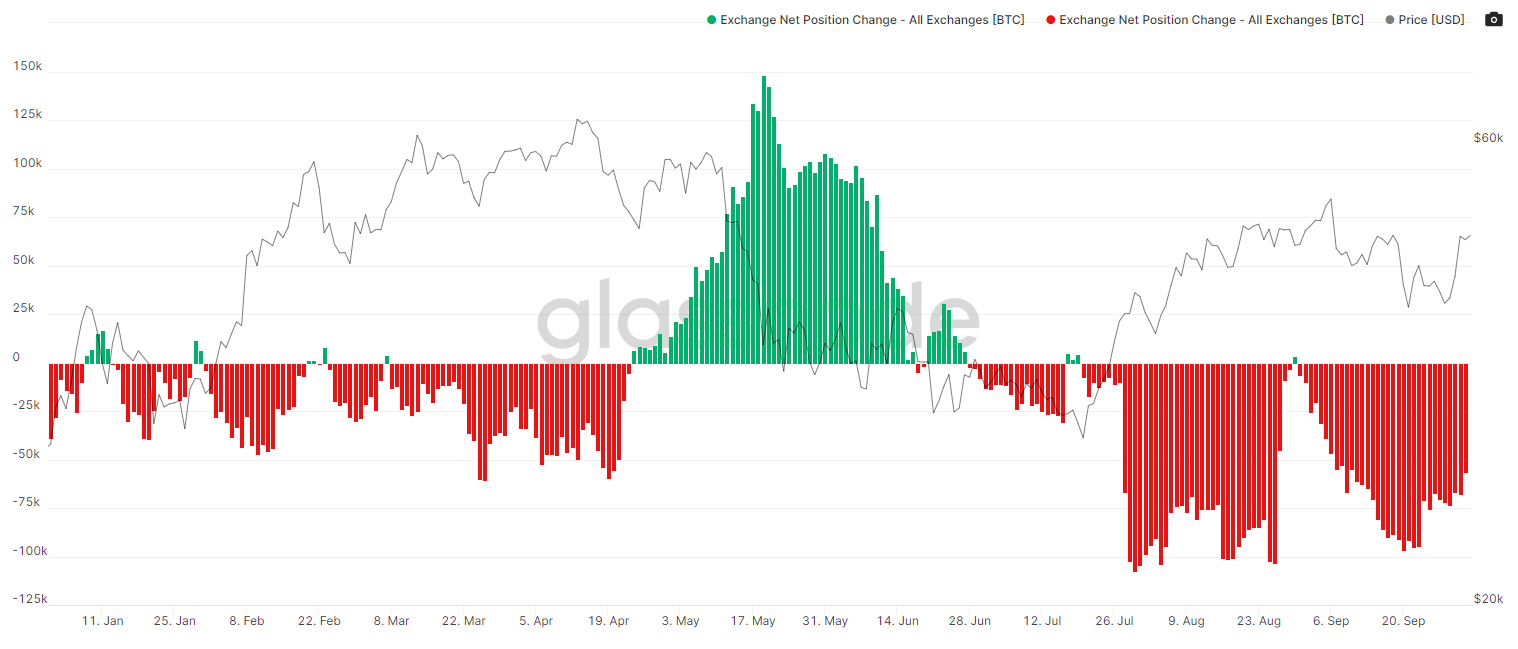

- Net outflows from exchanges holds strong – indicative of buoyant and or/bullish supply structures.

Bitcoin Net Position Change

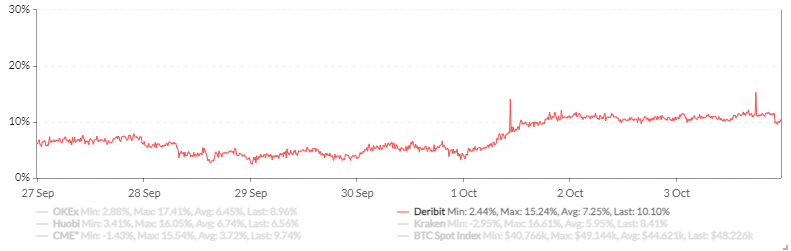

- Futures curve had a beautiful spike on a key level break. Our Head of Trading caught the move. Nice one Toby! We expect this to expand as we reach higher in the range, and could see a 15%+ annualised basis curve if we get a break of 50,000.

BTC Futures Annualised Rolling 1 Mth Basis

- In summary, this recent market is not driven by derivatives leverage. It was clearly a spot driven move – seeing uptick in fund flows and into ETFs, which means retail is not dominating this move higher. There’s been a major risk reversal swing, with put buying slowing and the market now buying calls. On newsflow, the Fed is not trying to kill crypto, with accompanying moderated sentiment on stablecoin regulation. Both are large shifts in messaging from the US authorities and important to legitimising growth in the space.

- Reposting seasonality here – this is clearly playing out in early October. What could November bring if the rally continues?

BTC Seasonal Returns

Ethereum

- Ethereum, and a chunk of the broader crypto market, followed the sentiment shift. ETH has broken above 3,330, and is holding above support. If we can get a clean break above 3,680, we have a good chance of running to 4,000. Technically, there is not much in the way, and the prior gap seems there to be filled. Decentralised Exchange (DEX) and Decentralised Finance (DeFi) flows played a strong part in the recent move – with concerns over China and US regulatory tightening leading to strong inflows into decentralised platforms, primarily via ETH based protocols.

- Conversely though, in the face of a continued downside move in equities on risk, we feel ETH may face a tougher run than BTC. Although at this stage, indicators are pointing to strength this week.

- On-chain indicators now clearly showing outflows from exchanges, and holding.

Ethereum Exchange Net Position Change

- Leverage is moderate, with positive funding rates on the perpetuals.

ETH Perpetual Swaps Funding

- ETH basis curve expanding – good news for yield plays.

ETH Futures Annualised Rolling 1 Mth Basis

- The amount of ETH in the ETH 2.0 staking contract currently sits at 7,817,146 . This represents 6.64% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- Despite ETH out rallying against BTC on positive news, we still think that we could be the early stages of hedge vs risk asset playing out.

ETH/BTC

DeFi & Innovation

- Total value locked in DeFi grew by 936% in 12 months.

- DeFi and decentralised exchanges (DEXs) volumes soar amid China’s crypto ban and US regulations.

- White hat hacker has been paid DeFi’s largest bounty ever, $1.05 million, for finding a crucial vulnerability in a crypto’s protocol.

- Visa working on an blockchain interoperability hub for crypto payments.

- Ripple launches a $250 million fund to support NFT creators on its platform.

- A $1 billion scientific fund seeks to use blockchain technology to expand human lifespan.

What to Watch

- China’s recent crackdown is being received with a softer tone by the market than May’s bitcoin mining ban announcement. Are crypto investors becoming more resilient to China news? Regulation concerns in the US are present but mixed with very positive newsflow, as Fed chair Powell stated that the government has no intentions of banning cryptocurrencies. With the SEC wanting to take more time analyzing the bitcoin ETF applications, it seems like regulators are taking the next wave of innovation seriously. Will that remain the case?

- The Fed’s upcoming tapering remains a concern, but the week’s market focus shifted into the debt ceiling deadline and the possibility of a US government shutdown. While the latter has been resolved at least until December, the 18th October looms over the American government and we expect more discussions on the matter this week. Upcoming decisions on the debt ceiling could impact tapering plans, as will September’s US jobs report, which will be released next Friday.

FAQs

What were the major events in the crypto market for the week ending 4th October 2021?

Yellen warned about the U.S. government running out of money by October 18, China’s Evergrande property Inc continued to impact global risk sentiment, Federal Reserve Chair Jerome Powell clarified that the U.S. has no plans to ban cryptocurrencies, and Europe became the largest crypto economy with over $1 trillion in transactions in 2020.

How did Bitcoin and Ethereum perform during the week?

Bitcoin and Ethereum both returned 11.75% WoW. Bitcoin saw on-chain factors like long-term holders accumulating supply and net outflows from exchanges. Key technical levels for BTC are the Sep highs at 53,000. Ethereum broke above 3,330 and is holding above support, with a good chance of running to 4,000 if it breaks above 3,680.

What were the significant developments in DeFi and Innovation?

Total value locked in DeFi grew by 936% in 12 months. DeFi and decentralized exchanges (DEXs) volumes soared amid China’s crypto ban and U.S. regulations. Visa is working on a blockchain interoperability hub for crypto payments, and Ripple launched a $250 million fund to support NFT creators on its platform.

What are the key macro themes affecting equities and digital assets?

Equities continued to fall due to concerns about U.S. economic stability, inflation, geopolitical risk around the APAC region, and asset purchase tapering risk. Digital assets faced early headwinds amid China’s crackdown on crypto entities but recovered swiftly due to positive clarification from Jerome Powell and other positive headlines.

What are the upcoming events to watch in the crypto market?

China’s recent crackdown and its impact on crypto investors, regulation concerns in the U.S., the Fed’s upcoming tapering, the debt ceiling deadline, and the possibility of a U.S. government shutdown are key events to watch. Upcoming decisions on the debt ceiling and September’s U.S. jobs report could also impact the market.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 27 Sep. 2021 0:00 UTC to 3 Oct. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

What is the Base Blockchain? The Coinbase Layer 2

The Base blockchain, introduced by Coinbase, represents a significant development in the realm of cryptocurrency and blockchain technology. It is a layer-2 solution built on

Bitcoin Mining in the US: Main Challenges

Bitcoin mining in the United States has recently faced a range of challenges, from regulatory hurdles to community and environmental concerns. As a significant hub

Bitcoin Halving: Market Reacts

The 2024 Bitcoin halving, a significant event for the cryptocurrency world, marked a notable shift in the market dynamics of Bitcoin. As the block reward

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.