Content

- Week in Review

- Winners & Losers

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- Insights

- FAQs

- What was the performance of Bitcoin and Ethereum in the week ending 2nd May 2022?

- What were the key macroeconomic factors affecting the crypto market during the week?

- What were the key developments in the DeFi and innovation space during the week?

- What were the key insights from the week?

- What should investors watch out for in the coming week?

- Disclaimer

2 May, 22

Weekly Crypto Market Wrap, 2nd May 2022

- Week in Review

- Winners & Losers

- Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- Insights

- FAQs

- What was the performance of Bitcoin and Ethereum in the week ending 2nd May 2022?

- What were the key macroeconomic factors affecting the crypto market during the week?

- What were the key developments in the DeFi and innovation space during the week?

- What were the key insights from the week?

- What should investors watch out for in the coming week?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- Dow tumbles 900 points, Nasdaq drops 4% on Friday – its worst month since 2008.

- Goldman Sachs offers its first Bitcoin-backed loan.

- US inflation rate surges to 6.6% based on Core PCE Index.

- Australian inflation reaches 20-year high ahead of election.

- Australia’s first Bitcoin and Ether ETFs delayed due to “standards check.”

- US Senate confirms Lael Brainard, crypto and digital dollar supporter, as FED vice chair.

- Bitcoin’s hash rate reaches a new all-time high amid volatility.

- Binance blocks crypto accounts tied to relatives of Russian officials.

- Sustainable energy usage for BTC mining grows nearly 60% in a year – NYSA passes ban on Proof of Work (PoW) crypto miners that don’t use green energy.

- Bitcoin whale holdings at seven-month highs despite recent volatility; Glassnode data.

- Meta’s metaverse-building unit Reality Labs at a $2.9 B loss in Q1 2022 – “I recognise it’s expensive to build this,” says Mark Zuckerberg.

- Brazilian Senate and Panama’s approve bills to regulate cryptocurrencies.

- Central African Republic becomes second country to adopt Bitcoin as legal tender.

- Edward Snowden revealed as key participant in creation of privacy crypto Zcash (ZEC).

Winners & Losers

Macro Environment

- Stocks worldwide experienced some of the worst selloffs during April than since the beginning of the COVID-19 pandemic in Q1/20. Nasdaq saw a net 13% retracement for the month with heavy selling during the final week of April. While over the previous decade, this would be a time to benefit from the portfolio diversification into the fixed income market. However, overextension of the money supply is finally bearing down on the bond market. For example, following a higher than expected German CPI report, the ten-year Bund sold off from 0.80% to 0.88%, a 10% movement in one of the most stable assets in the world. Positive correlation between stocks and bonds are dampening hopes of diversifying risk among the traditional risk parity portfolio.

- The second-biggest economy in the world, China, has begun a stream of fiscal and monetary stimulus to limit the fallout from its Zero COVID-19 policy. Not only have we experienced verbal intervention from a number of regulatory authority representatives on its easing of barriers for tech firm development. But there was a rumour that “team China” (a group of SoE brokerages employed to facilitate MoF intentions) have been actively buying up stocks using government portfolios. On Friday alone, the Hang Seng Tech index, which has seen up to 63% liquidation since the beginning of 2022, rallied by 11% in a day. China’s top leaders also promised a stream of fiscal stimulus to spur growth in the coming weeks following the Mayday holiday.

- The Bank of Japan’s monthly meeting confirmed a double down of the central bank’s willingness to ignore inflationary pressures and continue its negative interest rate and QQE policy. In response to the dovish announcement, USDJPY broke through the 130 barrier resistance, reaching a high of 131.13 before consolidating lower. Potential central bank intervention to limit the topside rally was not explicitly announced, but the fear of USD selling from the authorities had limited further rally into the weekend.

- The Reserve Bank of Australia will meet in the coming days to decide for the first time since the pandemic, on normalising the interest rate upwards. Currently, two out of the top four local banks expect them to move by raising rates in the realm of 15 to 25 bp. The rest of the market believes that political pressure will cause the central bank to stay on hold given the federal election place later in the month. The AUDUSD is retracing from recent highs to close in the 70 cents support line, which seems to be vulnerable given the Chinese economy’s hostile risk atmosphere (Australia’s largest customer country for exporting), falls on risky assets portfolio values and risk of a hung parliament in the upcoming election.

Technicals & Order Flow

Bitcoin

- This week a temporary relief rally pushed Bitcoin to weekly highs of 40,800. However, bulls met strong resistance above 40,500 resulting in a retracement back below the key support level 39,200. Subsequent action ranged around the 39,000 zone with all moves higher being met with immediate topside resistance. Downside bias resulted in a weekly close below 38,500, although the 37.500 level is now firmly established and holding against a see of risk from Friday’s equity markets close.

- Bitcoin’s correlation with tech stocks, which now resides above 0.8, benefitted action early in the week. Elon’s acquisition of Twitter strengthened sentiment in the crypto space. This, paired with Fidelity Investments allowing Bitcoin allocations to 401(k) accounts prompted the move to weekly highs.

- Later, an influx of positive news including Goldman Sachs offering their first Bitcoin-backed loan, and 21 Shares launching a Bitcoin/Gold ETP, proved frivolous. The USD Currency Index (DXY) reached 20-year highs and the market pricing in the forthcoming FOMC meeting prevented any notable moves toward the topside.

- Bitcoin’s correlation with the Nasdaq continues to edge higher. This coming week’s FOMC meeting and its results will almost certainly have an effect on risk assets, and given recent correlations, we expect this to spill into BTC.

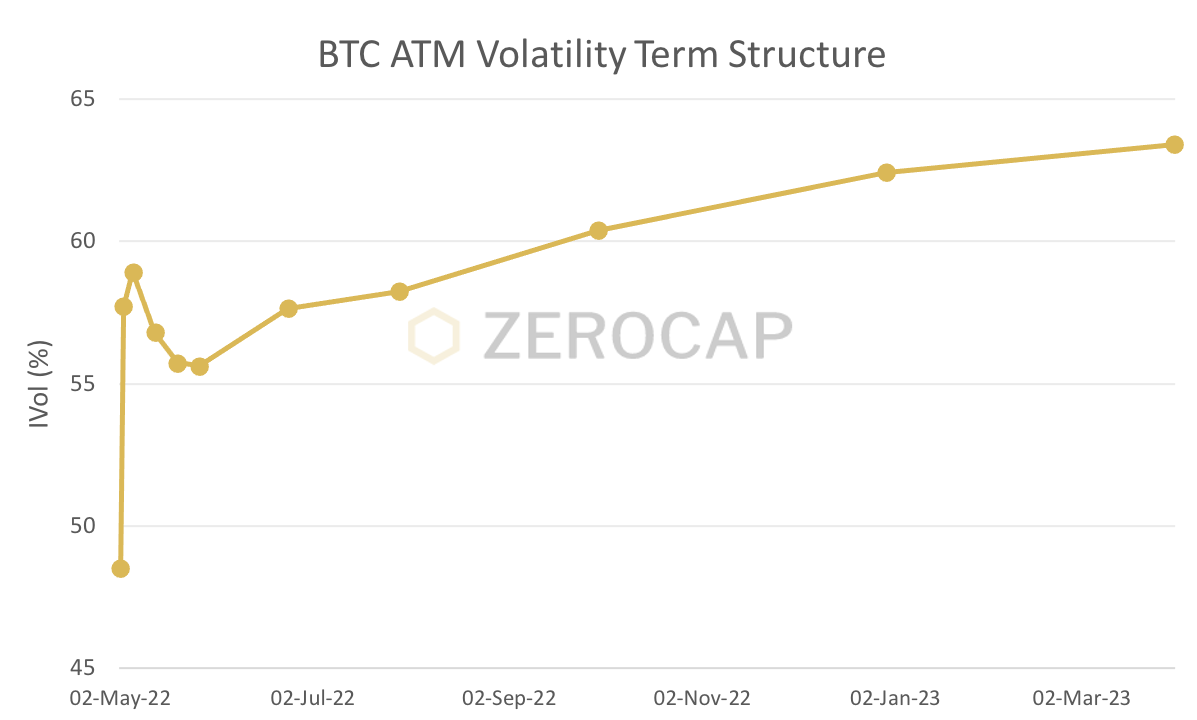

- Looking at Bitcoin’s at-the-money (ATM) volatility term structure, there is a notable uptick in implied volatility placed around the time of the upcoming FOMC meeting. Market participants are pricing expected volatility.

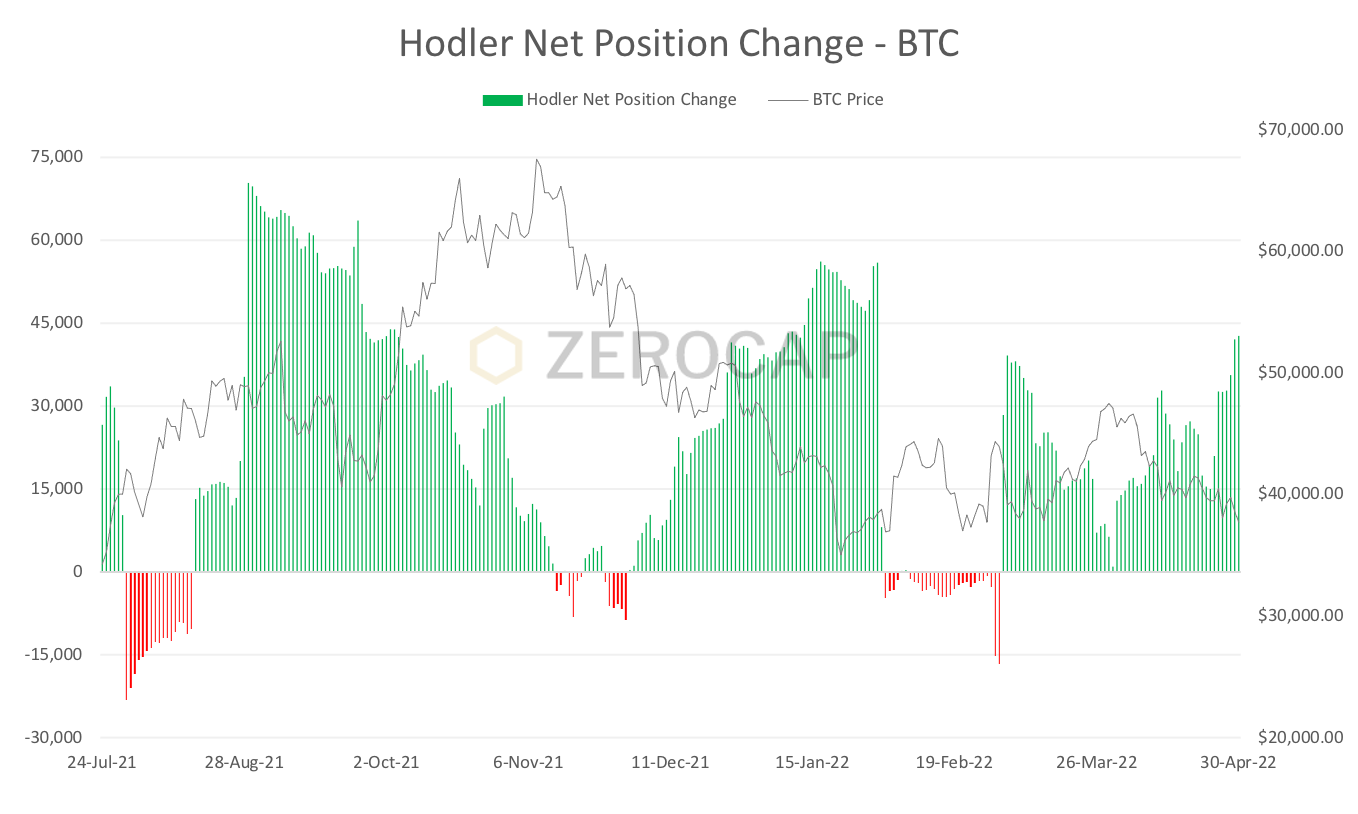

- Despite the prevalence of bearish macro forces in 2022 thus far, long term holders continue to accumulate. This accumulation is contributing to the formation of strong support around current levels.

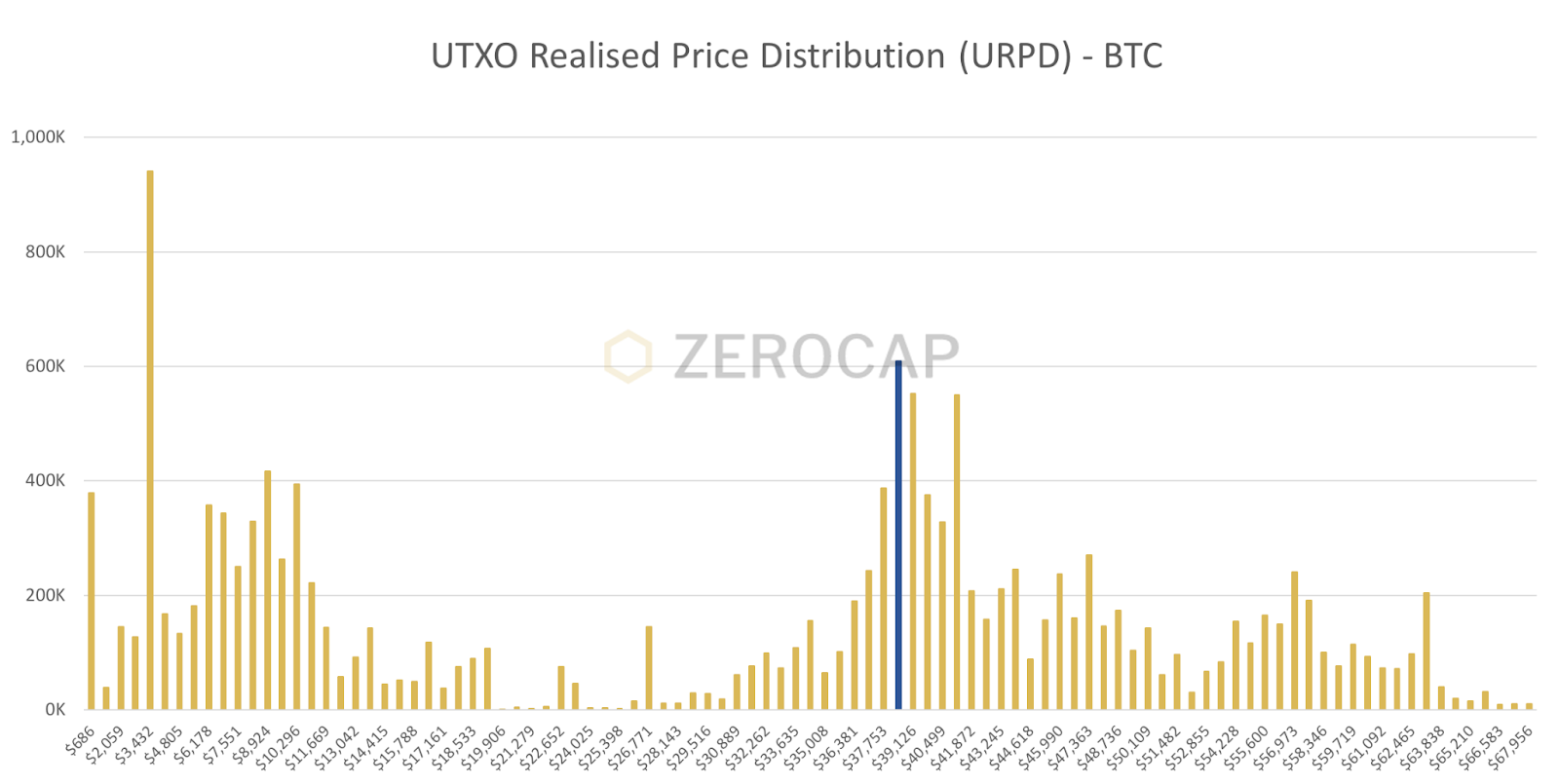

- Looking on-chain and toward URPD (on-chain price distribution levels), the theme of growing support around current levels is affirmed. Since the start of April, there has been a significant growth in volume between 37,500 – 42,000.

- This week, despite the sustained positive news around institutionalisation, Bitcoin suffered from the overarching weight of the macroeconomic environment. Long term holders have been accumulating for the most part in 2022, and have contributed to relative buoyancy against the rest of the market. Currently, US equities and crypto are at critical levels. Given the significant correlation between the Nasdaq and Bitcoin, directionality will be driven by the upcoming announcements from the FOMC. It is a slippery slope around current levels and participants should expect some significant price volatility around the meeting.

Ethereum

- This week, Ethereum struggled to turn the tide and bears remained in control of the action. Sell-offs at the week open proved true once again, a growing trend in the asset. On Monday, Ethereum fell 4.4% in tandem with significant selling in US equities. Ethereum regained its losses after a show of strength during the US session on Monday, before losing territory over the remainder of the week. ETH closed the week down 3.24%, resulting in four consecutive weeks of declines.

- The correlation between the Nasdaq and Ethereum edges higher, with the 30d correlation hitting 0.85 midweek. Macro themes continue to be the driving factor behind cryptocurrency price fluctuations. The FOMC meeting is fast approaching and we expect this thematic will persist in the near term.

ETHBTC Daily Chart

- After an initial fall during the week’s early activity, WoW price action for the pair ETH/BTC remained relatively flat. Price found strong support marginally above the previously rock-solid resistance of 0.0720. Price rebounded back into another tight range to close the week down 0.83%. The ETH/BTC pair generally provides a clear view of current market dynamics, with compressed market-wide volumes and reduced volatility inherent in the price action of ETH/BTC.

- Perpetual futures volumes have declined considerably since last year. Often indicative of retail market sentiment, higher volumes are correlated with momentum-driven moves toward the upside. Reduced market speculation has impacted these volumes month-on-month, providing an accurate reflection of the present market sentiment.

- Looking toward the options space, there is a continuation of suppressed ETH volatility term structures. Current ETH implied volatility (IV) levels are the lowest they have been since April 2021. This has been impacted by the systematic selling of options through decentralised option vaults (DOVs). The relative cheapness compared to historical IV is attractive for traders looking to speculate on bullish appreciation by buying calls in longer-dated terms.

- Last week we spoke about ApeCoin’s cumulative return exceeding 1,500% since its listing on March 17th. However, a mismatch of expectations surrounding the Otherside Metaverse land sale resulted in a drawdown of 39% from its ATH on April 28th. The sale was expected to be designed as a Dutch Auction. Instead, the NFT mint cost a flat 305 APE. While BAYC sold over $100m of digital real estate in 45 minutes, Ethereum gas fees rose to as high as 2.5 ETH. Notable backlash as a result of the network inefficiencies and numerous cases of failed transactions from the Yuga Labs community, contributed to the downward action. There is a growing community voice demanding for BAYC to establish their own chain in order to avoid similar issues moving forward.

- The FOMC meeting on Wednesday (ET time) is primed to shape the next moves for Ethereum and broader risk assets. The market expects a 50bp hike from this week’s meeting, and with 218bp of hikes priced in throughout 2022. Participants eagerly await Powell’s speech which will provide an outlook on the possibility of future hikes.

DeFi & Innovation

- Ethereum 2.0 deposit contract now holds more than 10% of all ETH in circulation.

- European Central Bank begins prototype of digital euro through customer interface.

- Binance announces crypto card for Ukrainian refugees.

- Meta to open physical metaverse-themed store in San Francisco.

- Elon Musk strikes deal to buy Twitter for $44 B.

What to Watch

- FOMC press conference and Federal Funds rate, on Wednesday.

- US unemployment rate, on Friday – is the “great resignation” still going strong?

- Updates on the first Australian crypto ETFs, postponed last week.

Insights

Can cryptocurrencies give the world capital markets a level playing field? In this piece by treasurer William Fong and trader Joe Wilson, we discuss the potential cryptocurrencies have of providing a level playing field to world capital markets – through the variables of CBDCs and stablecoins.

FAQs

What was the performance of Bitcoin and Ethereum in the week ending 2nd May 2022?

During the week, Bitcoin experienced a temporary relief rally pushing it to weekly highs of 40,800. However, it faced strong resistance above 40,500 resulting in a retracement back below the key support level of 39,200. Ethereum, on the other hand, struggled with bearish control, experiencing a 4.4% fall at the week’s start, but managed to regain its losses later.

What were the key macroeconomic factors affecting the crypto market during the week?

The Dow tumbled 900 points, Nasdaq dropped 4% on Friday – its worst month since 2008. The US inflation rate surged to 6.6% based on the Core PCE Index, and Australian inflation reached a 20-year high ahead of the election. These factors, along with geopolitical tensions and tightening global monetary policy, impacted the crypto market.

What were the key developments in the DeFi and innovation space during the week?

The Ethereum 2.0 deposit contract now holds more than 10% of all ETH in circulation. The European Central Bank began a prototype of the digital euro through a customer interface. Binance announced a crypto card for Ukrainian refugees, and Meta planned to open a physical metaverse-themed store in San Francisco.

What were the key insights from the week?

The week’s insights included the potential of cryptocurrencies to provide a level playing field to world capital markets through the variables of CBDCs and stablecoins. Also, the correlation between the Nasdaq and Bitcoin continued to edge higher, with the 30d correlation hitting 0.85 midweek.

What should investors watch out for in the coming week?

Investors should watch out for the FOMC press conference and Federal Funds rate on Wednesday, the US unemployment rate on Friday, updates on the first Australian crypto ETFs, and the performance of Bitcoin and Ethereum.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 25 Apr. 2022 0:00 UTC to 1 May. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Bitcoin Mining in the US: Main Challenges

Bitcoin mining in the United States has recently faced a range of challenges, from regulatory hurdles to community and environmental concerns. As a significant hub

Bitcoin Halving: Market Reacts

The 2024 Bitcoin halving, a significant event for the cryptocurrency world, marked a notable shift in the market dynamics of Bitcoin. As the block reward

Weekly Crypto Market Wrap, 22nd April 2024

Download the PDF Zerocap provides digital asset liquidity and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.