Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the significant events in the crypto market during the week of 22nd November 2021?

- How did Bitcoin and Ethereum perform during the week?

- What were the winners and losers in the market?

- What are the key levels and trends for Bitcoin and Ethereum?

- What are some notable developments in DeFi and innovation?

- Disclaimer

22 Nov, 21

Weekly Crypto Market Wrap, 22nd November 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the significant events in the crypto market during the week of 22nd November 2021?

- How did Bitcoin and Ethereum perform during the week?

- What were the winners and losers in the market?

- What are the key levels and trends for Bitcoin and Ethereum?

- What are some notable developments in DeFi and innovation?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- President Biden signs the $1T infrastructure bill containing crypto broker reporting requirements, including reporting crypto transactions over $10k to the government within 15 days – Senator Lummis works on separate bill to narrow the regulatory scope.

- Fed Reserve governor Waller and St. Louis President Bullard urge faster tapering measures due to rapid inflation rise.

- US retail sales report climbs 1.7% in October, fastest gain since March, as Americans enter holiday season while inflation plays a role – at its highest in 31 years.

- Biden and Xi Jinping meet – leaders called for mutual respect during unexceptional meeting while Chinese officials warned the US against “playing with fire” on Taiwan.

- Commonwealth Bank CEO says the biggest risk of crypto is “missing out.”

- US Congress holds a “Demystifying Crypto” hearing, calling for crypto exchange regulations that match traditional finance’s and better oversight of stablecoins.

- U.S. Federal Reserve governor Waller’s speech praises stablecoins as genuine innovations, while claiming CBDCs are unnecessary as a payments system.

- Blueprint for CFTC regime over digital assets enters US Congress, while SEC’s Gary Gensler opposes their regulatory initiative.

- Former democratic US candidate Hillary Clinton warns that crypto can “destabilize nations”, potentially “undermining the role of the dollar as the reserve currency.”

- Winklevoss twins’ Gemini raises $400M to build Metaverse, a company valued at $7.1B.

- India set to ban cryptocurrencies as payment method, while regulating as assets – will reduce GST paid on crypto exchanges from 18 to 1%.

- Staples Center to become “Crypto.com Arena” after $700M naming rights deal.

- VanEck’s Bitcoin futures ETF launches with lower-than-expected reception.

Winners & Losers

- Bitcoin spent the week capitulating to under US$60,000 dragging the market with it. An unexpected building of elevated funding rates and an over-leveraged futures market caused liquidations, leading to profit-taking and short interest. The ratification of the US infrastructure bill likely impacted sentiment while the Taproot upgrade – an expected bullish catalyst – had little impact on price. Although the correction has many on the edge of their seats, resetting funding rates and open-interest is beneficial for the long term health of the market. Overall, BTC returned -10.43% and ETH -7.95% WoW.

- U.S. Tech stocks hitting all-time high once again. European growth sentiment took a backseat, with Austria entering a full lockdown due to rising COVID cases, and Germany might be following their path shortly. Travel and entertainment stocks hit hard, but the retail sector is watching this week’s Black Friday and Cyber Monday weekend sales to determine how 70% of the U.S. economy will perform going forward. Lower funding rate due to safe-haven flows into the government bond market also benefited the tech sector on a valuation basis. Earnings from the two of China’s biggest tech companies, Alibaba and Baidu, both disappointed, leading to worry about consumer growth from the world’s second-largest economy.

- Macroeconomic data focused on US retail sales print, which rose above expectation. This was an important confidence boost given the previous week’s weak consumer sentiment outcome. China’s regulators suggested the economy will face years of a stagflationary environment and that banks should limit their speculative activities on the RMB as both corporate and bank proprietary trading desk skews heavily on the RMB’s value. The PBoC released its quarterly monetary policy report and hinted at further stimulus policy targeting SMEs liquidity constraints.

- The Investment-grade bond fluctuated between inflation worries and stagnation following Europe’s renewed lockdown concerns. S&P’s headline announcement regarding default risk for China’s Evergrande property weighed down Junk bond markets. The international rating agency said Evergrande has “lost the capacity to sell new homes, which means its main business model is effectively defunct” and that S&P still believe the developer is likely to default on its outstanding debt. Another major Southern China property developer, Kaisa, failed to service its coupon payments due during the week.

- The VIX index jumped on Friday as economic concerns from European COVID cases and Austria’s lockdown weighed on reopening stocks. Equity futures in the US also saw the second-largest options expiry date, which generated a stream of delta hedging activities in the cash arena. Front end VIX futures were closing above 20 after opening the week below 16.

- Gold prices continue to benefit from inflation concerns on the top level. Portfolio allocation could see the precious metal price taking another leg up towards the 2,000 level by year-end if momentum is maintained. Oil prices traded lower through the week, with travel and holiday activities slowing down with European COVID cases concerned. Few COP26 headlines impacted the commodities market following a watered-down conclusion to the summit.

Macro, Technicals & Order Flow

Bitcoin

- We were not expecting the downside liquidations that occurred last week from fast building leverage near the highs. Volatility is always possible up at these levels, and it’s important to watch not only static leverage, but also the velocity at which funding rates and leverage is building. Definitely not the ‘buoyant week’ we called for!

- The move took out stops below prior lows, before trading back into the range. Key levels for BTC sit at 57,500 and 55,500. If we get a break lower, the next major support is down at 53,000. However, BTC fundamentals and on-chain data are supportive of a move higher in the medium-term.

BTC Perpetual Swaps Funding

Fast money getting long (circled).

BTC Perpetual Liquidations 1W

- On-chain data is still clearly showing outflows from exchanges, indicating potential supply constraints and general bullish sentiment.

Bitcoin Net Position Change

- Option strikes out to Dec 31 are clearly weighted to calls at 80,000 / 100,000 and… 200,000. The crowd is still alive and well. This all bodes well for general sentiment.

OI Interest by Strike – Dec 31, 2021

- Bitcoin supply held by long-term holders continues to slow, indicating some profit-taking at these levels by the longer-term investors. As mentioned last week, there is generally a time lag between the slowing of accumulation by these holders and a turn in the market, very similar to the Commitments of Traders (COT) report released by the CFTC in the traditional world, tracking commercials vs speculators. This shows a longer-term potential shift in sentiment, however the correlation is tenuous in the face of broader macroeconomic forces (think inflation).

Bitcoin: Total Supply Held by Long-Term Holders

- The on-chain UTXO price distribution shows the depth of bitcoin activity at certain price levels. Despite last week having a clear run at highs, leverage won the race, liquidating to prior orderflow levels and building price distribution higher. We are seeing a ranging pattern for the UTXO with clear price distribution on either side of current pricing.

UTXO Realised Price Distribution

- The futures basis curve has compressed further this week on the back of the move lower. Open interest levels are still elevated, but falling against the liquidations. The combination of falling open interest and outflows from exchanges is generally associated with spot buying. Price is still hanging around the lows, if we hold here until Europe and US sessions open (Monday), we may go higher given these on-chain factors.

BTC Futures Annualised Rolling 1 Mth Basis

Bitcoin Futures Open Interest

- In summary, leverage has been reset, although futures open interest is still elevated. On-chain data is strong, and with the retail sales numbers out of the US, we are looking at more potential inflationary pressures. On that note, I was at the local market on Sunday – the butcher told me that he is expecting a 25% hike in meat prices by January given energy costs and supply chain issues. The central bank data on inflation is retrospective – look around and see what you can find now for clues. We see bitcoin being treated as a hedge in the medium to long term.

Ethereum

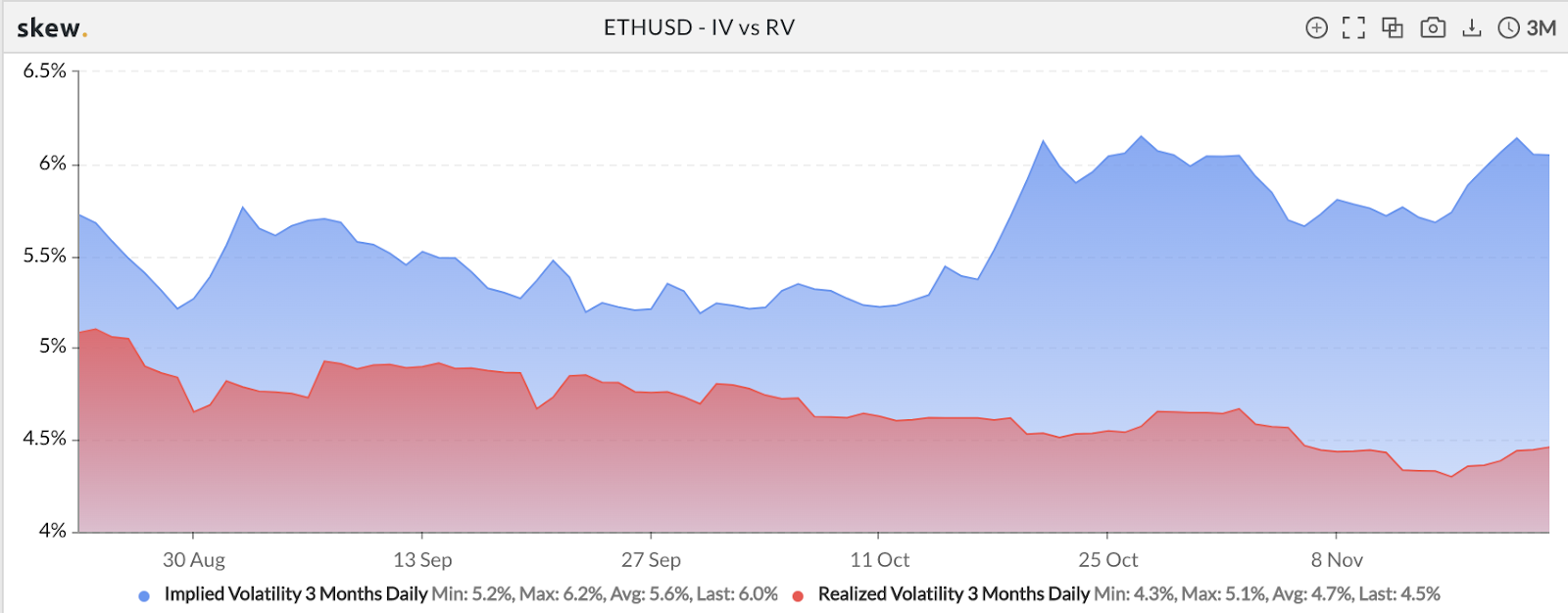

- Ethereum equally felt the force of liquidations this week, breaking the ascending trendline from late September. Price has respected the prior highs early Sep at 4,000 the figure. There is much orderflow between 4,000 and 5,000 – with significant options call interest at 5,000. Our OTC desk has seen significant profit-taking up to 4,950 – with customers taking advantage of our structured products (primarily covered calls in this case) to take advantage of high-yield plays on Dec 31 strikes. The implied volatility levels are outta this world – it pays to be a contrarian here, sell the vol and earn yield whilst waiting for your levels to hit. Key levels are clearly 4,000 to the downside, with the prior highs and ascending trendline coalescing at the 5,000 level.

ETHUSD Implied Volatility vs Realised Volatility

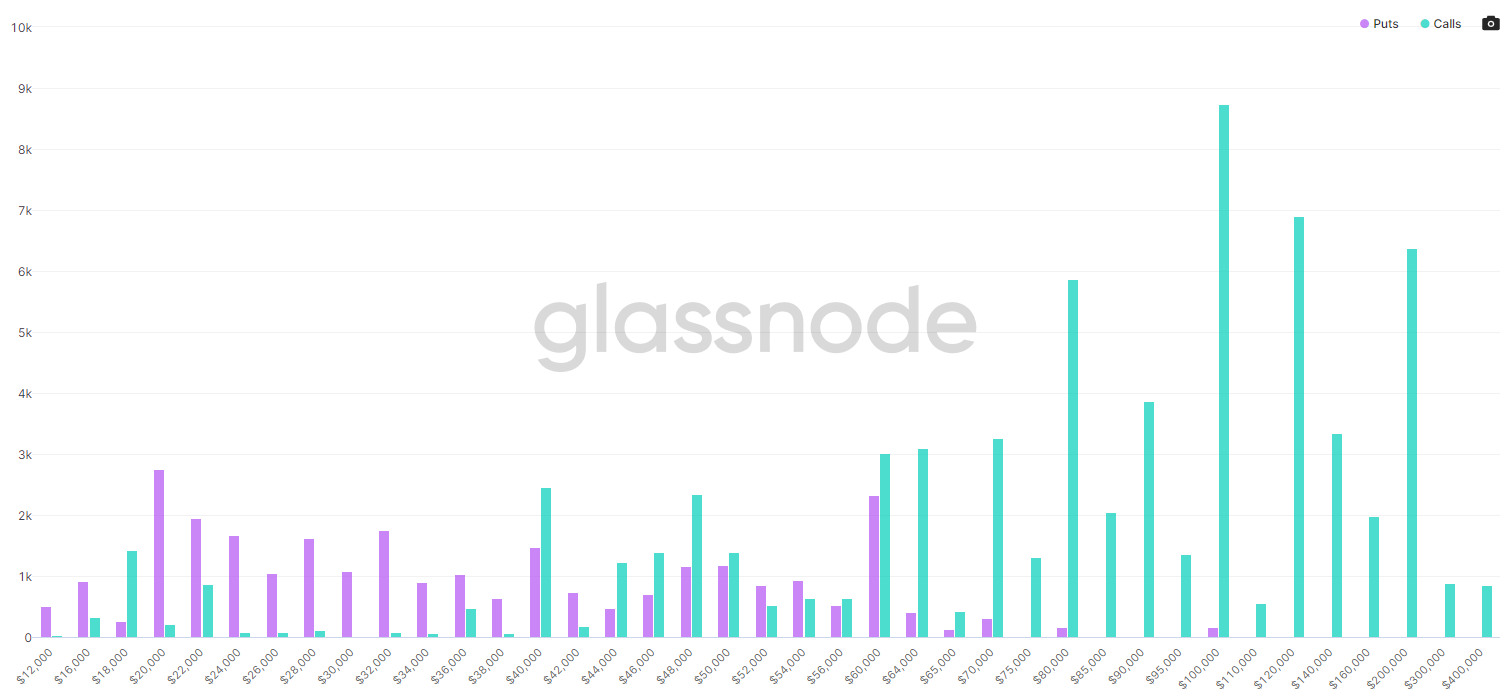

- Open interest is still favouring 5,000 the figure with call interest substantial at these levels.

ETH Open Interest by Strike: Dec 31, 2021

- The ETHBTC has managed to find its legs again, with ETH outperforming BTC during the liquidity moves.

ETHBTC Daily Chart

- Strong outflows from exchanges (indicating contraction in supply) are persisting, however, on-chain data is showing that some larger wallet holders with a supply held of 10 to 100 ETH have suddenly liquidated alongside the drop.

Ethereum Exchange Net Position Change

Supply Held by Wallets with Balances of 10-100 ETH

- Perpetual funding rates, like BTC, had a sudden spike before the move.

ETH Perpetual Swaps Funding

- The futures basis curve is ranging, showing more promise than BTC.

ETH Futures Annualised Rolling 1 Mth Basis

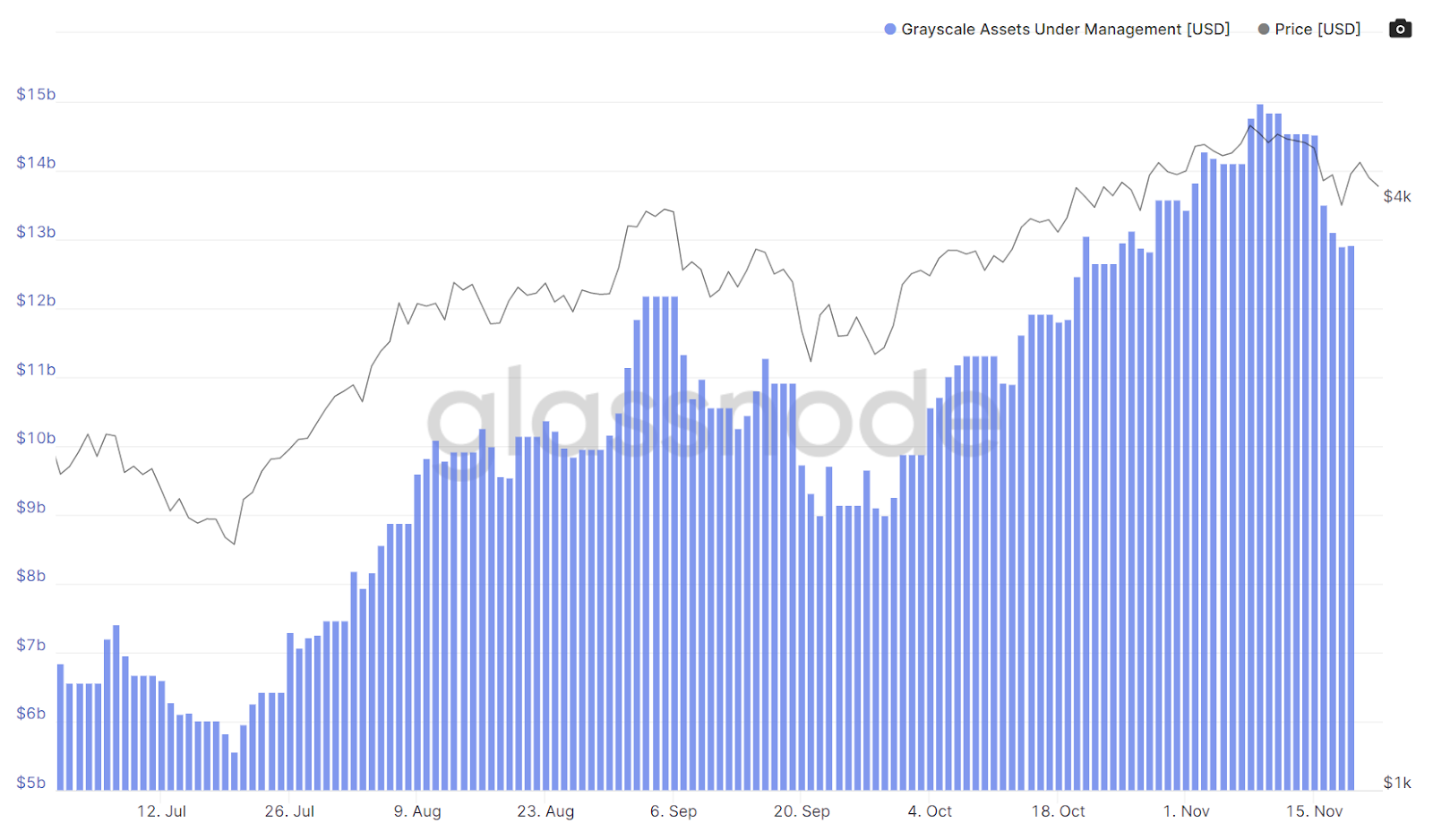

- Grayscale AUM is beginning to roll over, showing waning institutional interest after its bit run from early October.

Ethereum Grayscale AUM

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,327,126. This represents 7.03% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- The big media narrative over the past two weeks in cryptoland has been around transaction fees (again), and further into ethereum’s value proposition. AK (one of our proprietary trading friends) gave his opinion on the network which is worth posting here (thanks AK!):

- ETH – unusable for most people with the current gas fees, and thus the network is currently favouring the bigger holders.

- Against the DeFi proposition – which was originally ‘bank the unbanked’ in the early ethereum days, is now totally unattainable.

- Deflationary elements seem to optimise for wealth, not utility at times. Deviating from their original mission.

- This casts doubts as to its future, but despite this, the charts are looking wildly positive.

- It’s worth looking at the other side of the coin – there are certainly some headwinds for ETH, but also some pretty serious institutional flows and its place as the incumbent. Keep an eye on the media and growing interest in chains such as Solana, Avalanche and Fantom for signs of the next wave of adoption.. or maybe that comes in the next cycle?

DeFi & Innovation

- Polkadot network has its first parachain auction, $1.3B in DOT committed.

- Binance Smart Chain hits record-high daily transactions.

- El Salvador to build crypto-fueled “Crypto City” – backed by BTC bonds.

- Twitter releases whitepaper for its decentralized exchange (DEX) project.

- Brave’s web browser now includes a built-in crypto wallet, no extension required.

- Australian baseball club Perth Heat to pay athletes in bitcoin.

What to Watch

- Further developments on crypto directives of the $1T infrastructure bill.

- Will the Federal Reserve adopt faster tapering due to inflation rise concerns?

- US’ preliminary GDP, Core PCE Price Index and FOMC meeting minutes on Wednesday.

- Bank of England governor Bailey conference at the Cambridge Union on Thursday.

FAQs

What were the significant events in the crypto market during the week of 22nd November 2021?

During this week, President Biden signed a $1T infrastructure bill with crypto broker reporting requirements, the Federal Reserve urged faster tapering measures, U.S. retail sales climbed, and the Commonwealth Bank CEO emphasized the risk of missing out on crypto. Other highlights include a “Demystifying Crypto” hearing in Congress, Hillary Clinton’s warning about crypto’s potential to destabilize nations, and India’s move to regulate cryptocurrencies as assets.

How did Bitcoin and Ethereum perform during the week?

Bitcoin experienced a drop to under US$60,000, leading to liquidations and profit-taking. The ratification of the U.S. infrastructure bill and the Taproot upgrade had little impact on the price, with BTC returning -10.43% for the week. Ethereum also felt the force of liquidations, breaking an ascending trendline from late September, with ETH returning -7.95% WoW.

What were the winners and losers in the market?

Bitcoin and Ethereum were among the losers, with significant drops in their prices. U.S. Tech stocks hit an all-time high, and gold prices continued to benefit from inflation concerns. The property market in China faced challenges, with Evergrande’s default risk and another major property developer, Kaisa, failing to service its coupon payments.

What are the key levels and trends for Bitcoin and Ethereum?

For Bitcoin, key levels sit at 57,500 and 55,500, with the next major support at 53,000. On-chain data supports a medium-term move higher. For Ethereum, key levels are 4,000 to the downside and 5,000 to the upside. On-chain data shows strong outflows from exchanges, but some larger wallet holders have liquidated.

What are some notable developments in DeFi and innovation?

Polkadot network had its first parachain auction with $1.3B in DOT committed. Binance Smart Chain hit a record-high in daily transactions. El Salvador announced plans to build a crypto-fueled “Crypto City.” Twitter released a whitepaper for its decentralized exchange (DEX) project, and Brave’s web browser now includes a built-in crypto wallet.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 15 Nov. 2021 0:00 UTC to 21 Nov. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Ethereum Smart Contracts: How They Changed Crypto

Ethereum, launched in 2015, revolutionized the digital world by introducing “smart contracts,” self-executing contracts with the terms of the agreement directly written into code. This

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.