Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- Insights

- FAQs

- What significant regulatory and political events influenced the crypto market during the week of 21st February 2022?

- How did geopolitical tensions and macroeconomic factors impact Bitcoin and Ethereum's price action during the week?

- What were the major developments in the DeFi and Metaverse space during the week?

- What were the key market trends and movements in the winners and losers of the week?

- What are the essential factors and events to watch in the coming week that could influence the crypto market?

- Disclaimer

21 Feb, 22

Weekly Crypto Market Wrap, 21st February 2022

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- Insights

- FAQs

- What significant regulatory and political events influenced the crypto market during the week of 21st February 2022?

- How did geopolitical tensions and macroeconomic factors impact Bitcoin and Ethereum's price action during the week?

- What were the major developments in the DeFi and Metaverse space during the week?

- What were the key market trends and movements in the winners and losers of the week?

- What are the essential factors and events to watch in the coming week that could influence the crypto market?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- Biden expected to issue an executive order on crypto this week: Yahoo Finance report.

- Federal Reserve approves rules banning its officials from trading stocks, bonds and cryptocurrencies – restrictions will take effect on May 1st.

- FOMC January Minutes: Fed ready for rate hikes and reduction in asset holdings, members show great concern as inflation spreads beyond pandemic-related sectors into the broader economy.

- St. Louis Fed President Bullard: Inflation “could get out of control,” calls for immediate action on interest rates, previously mentioning full percentage point hikes by July.

- US retail sales beat expectations, surges 3.8% in January.

- Banning Bitcoin in Russia is the “same as banning the internet,” says Bank of Russia governor Elvira Nabiullina.

- US Treasury affirms crypto miners and ‘wallet operators’ are exempt from IRS reporting rules.

- Sequoia Capital launches a crypto fund worth up to $600 million.

- Warren Buffet invests an extra $1B into Nubank, Brazilian crypto-friendly neobank, increasing his total allocation to $1.5B from July’s $500 million investment.

- Canadian Prime Minister Trudeau invokes Emergency Act due to truckers protest, targets crowdfunding and crypto addresses.

- SEC hits BlockFi with $100 million penalty for unregistered lending product.

- NYSE files trademark application for trading NFTs.

- FBI launches cryptocurrency unit to deal with digital exploitations.

Winners & Losers

- The week’s fixed income market began on the backfoot as the market accelerated global unwinding of pandemic era stimulus. Ten-year UST yield pushed past the 2% level earlier on, while the 30-year hit 2.35%. The German bund went to a high of 0.35%, leaving the JGB curve as the only major developed yield curve below zero. Various FED speakers are now calling for an aggressive unwinding of the QE effort, starting with a 50bp hike in the March FOMC meeting. However, the yield curve collapsed towards the end of the week as geopolitical concerns escalated, with US president Biden calling for the imminent Russian invasion of Ukraine within days. The strategy seems quite similar to what happened with Crimea several years ago, which began with Russian backed and geared up rebels taking on the local government before Russian troops moved in to “help” loyal Russian citizens. On the other side of the world, China failed to meet market calls to cut rates to stabilise the property sector. This could be due to the news report that new home prices in the country had their first positive price rise since September 2021. The hawkish inaction led to a sell-off in both bonds and domestic stocks.

- Company earnings season is ending in the US, with 84% of reporting done and 78% beating expectations, while 19% performing poorly. Hence, earnings forecasting will now focus on how they’ll go given the inflation and higher interest rate environment in the coming quarter.

- Oil prices at a seven-year high also support Shale-related stocks on the S&P 500. However, the prospect of a major global geopolitical tension on the horizon is weighing on sentiment and will continue to do so until it subsides.

- Following the stronger than expected consumer inflation data last year, supply-side pressures also show up via the US PPI report. The headline shows the YoY figure at 9.7%, while ex-food and energy were 8.3%, beating market expectations. Chinese CPI came out lower than the previous record on Dec21. Month on month data was at 0.9% vs 1.5% previously reported, and food prices retraced lower to minus 3.8% YoY vs minus 1.2% in December.

- Risk aversion intensified into the weekend; with Monday’s US presidential day holiday, money flow concentrated on safe haven migration. Ten year UST yield dropped by 10bp from weekly peak to close at 1.95%, while GOLD prices remained elevated near $1,900. VIX stayed high, but BTC and ETH implied Vol was subdued despite higher realised selling in the spot market. With its weekend trading hours, cryptocurrency provided the optimal geopolitical headline hedging tool. With French President Macron meeting up with Russian President Putin in the later hours of Monday European time, in a continual effort to de-escalate the tension, the market could be looking for a positive rebound in thin liquidity during the US holiday session.

Macro, Technicals & Order Flow

Bitcoin

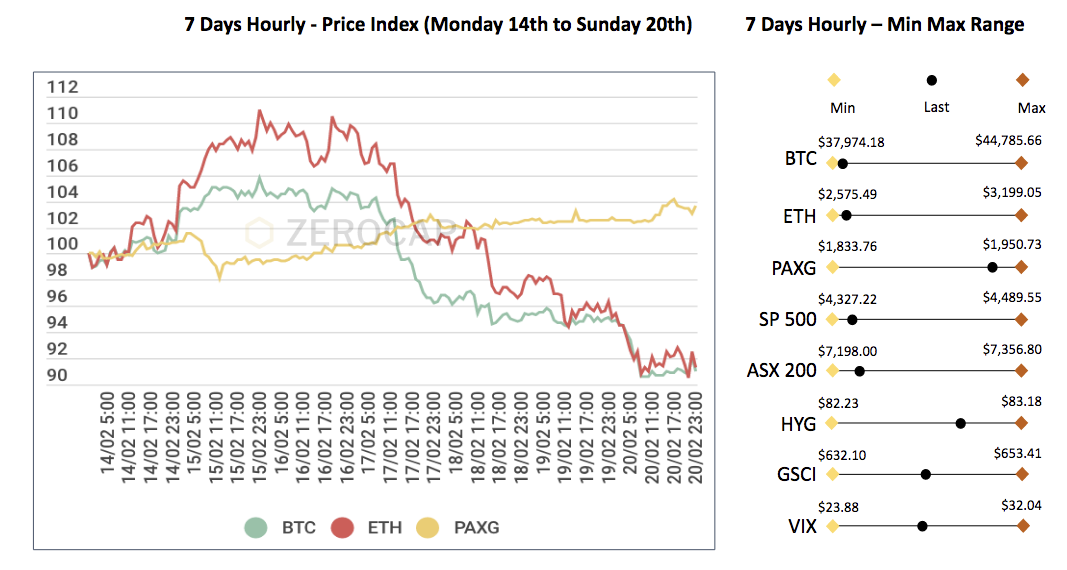

- This week, Bitcoin’s price action was dictated by news out of the current geopolitical conflict in Ukraine. An early push to weekly highs around 44,000 was prompted by a partial withdrawal of troops.

- Whilst news out of the January FOMC minutes caused some bearish price action, heightened geopolitical tensions came into the spotlight late last week resulting in de-risking into the weekend. The resultant sell off in the crypto markets and a rally in bond markets reaffirmed the continuing theme of de-risking into weekends when markets are fragile.

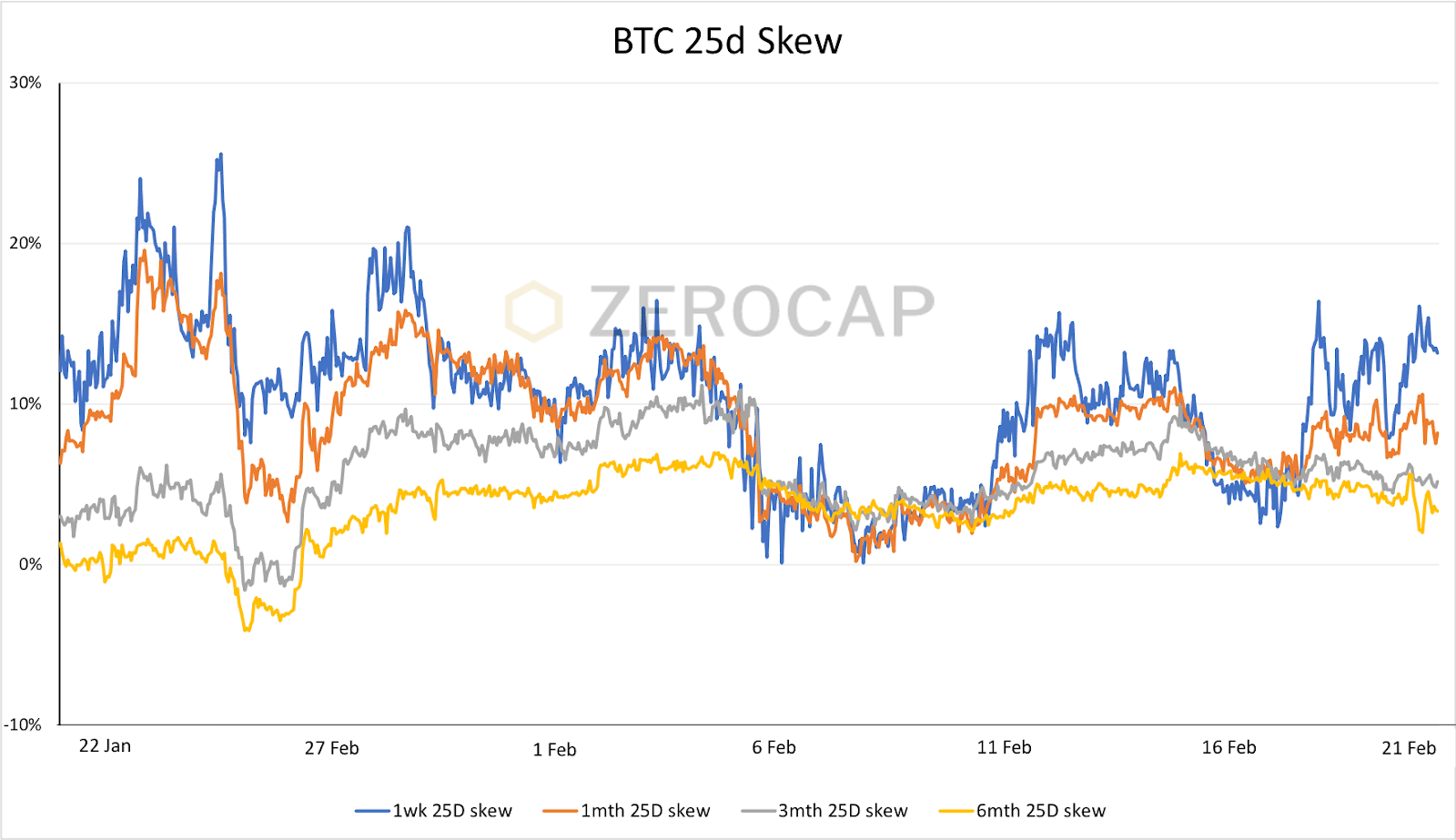

- Bitcoin’s 25-day skew depicts the difference between a 25-delta put and a 25-delta call in terms of implied volatility. Moves away from 0%, like those seen subsequent to Thursday’s action, are indicative of option players favoring short term bearish plays or bidding for protection.

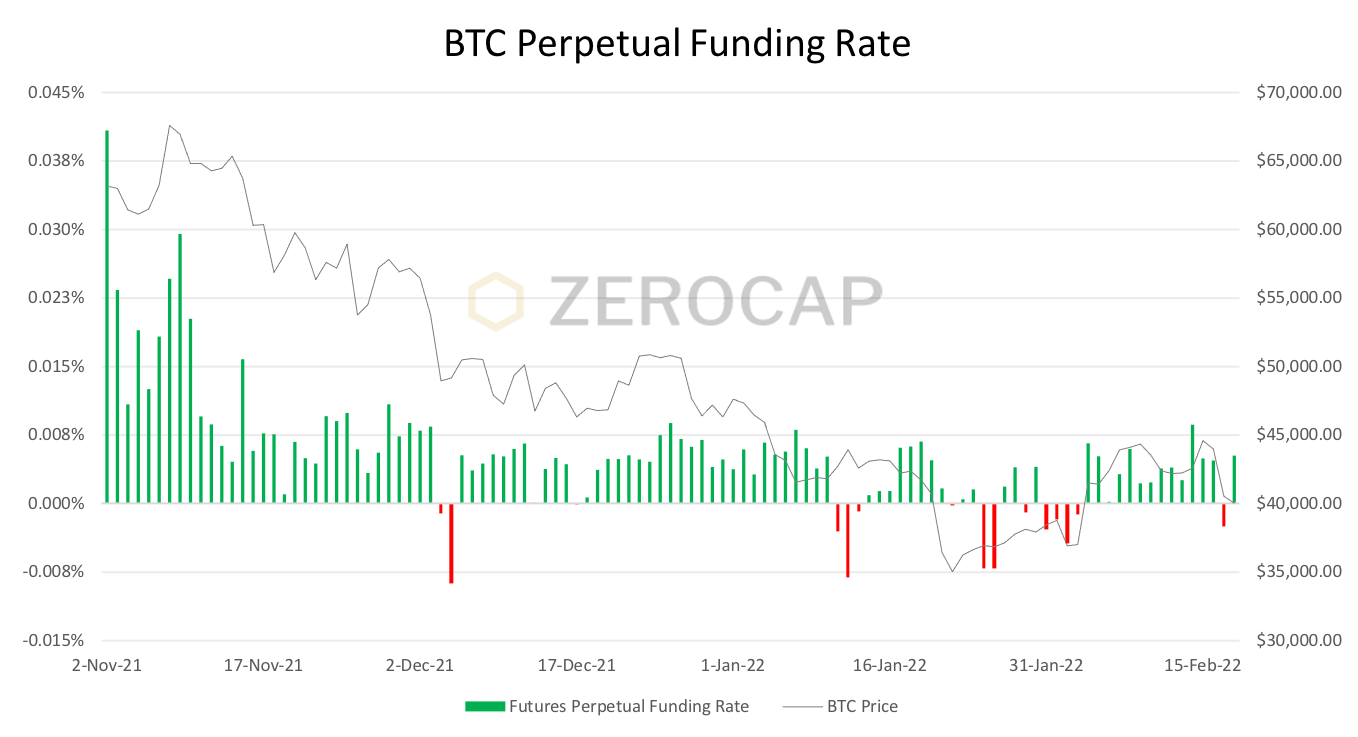

- Conversely, perpetual funding rates are on-balance positive, favoring short-term longs. That said, those playing the futures markets with leverage may soon feel the pain in the context of any near-term risk moves against the backdrop on Russia and Ukraine.

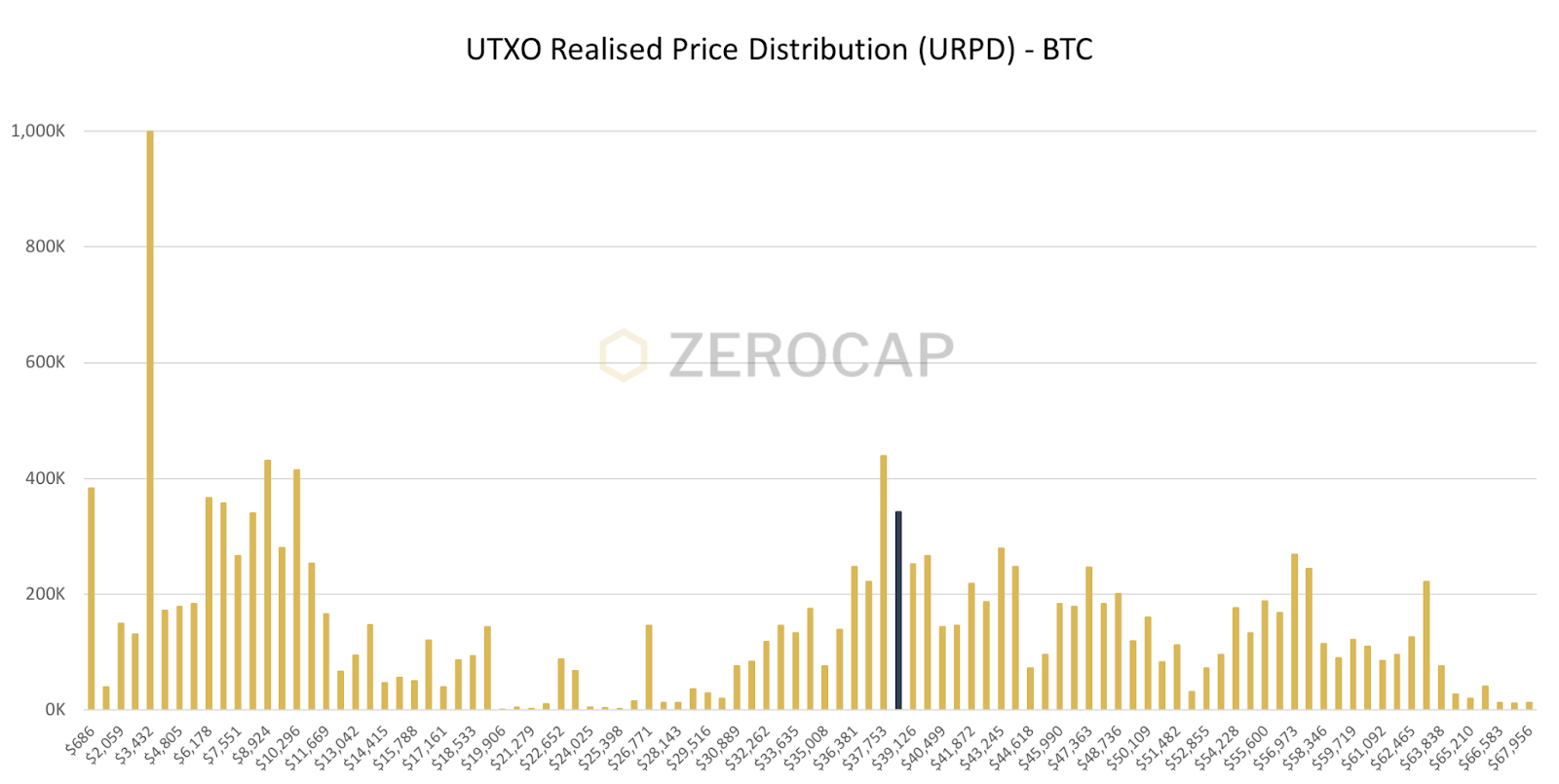

- URPD shows the prices in which BTC supply was transacted on-chain. Large volumes of BTC realized at certain levels can provide indication of support and resistance levels. Solid support has developed at current levels, where orderflow is clearly changing hands against the shifting backdrop.

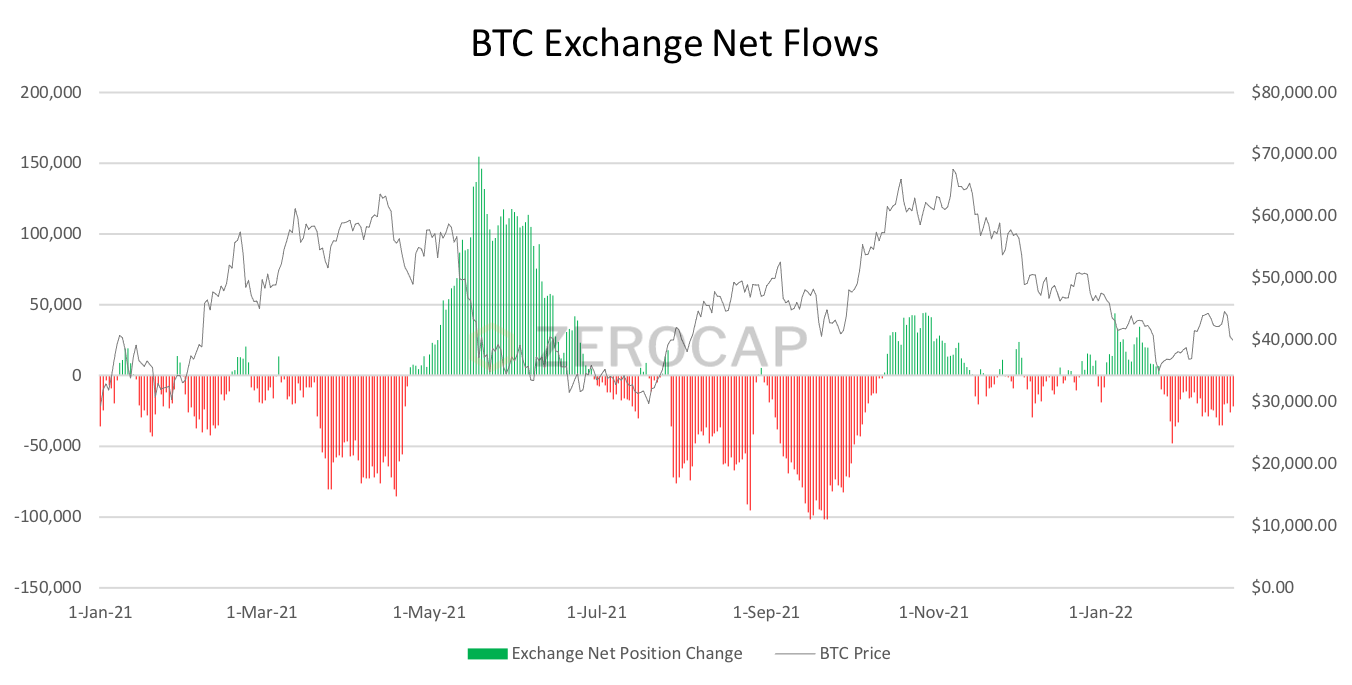

- In addition to the growing support depicted by URPD, we can see that on-chain supply on exchanges is in decline, providing bullish market structure for BTC.

- Attention has diverged from interest rates and the market now waits and watches for changes in the geopolitical environment. Risk will always trump monetary policy in the short-term. Whilst on-chain continues to paint a bullish picture, some investors are taking advantage of the current market fragility, favoring bearish options structures. Taking a step back and looking beyond short term price determinants, it’s worth noting Bitcoin’s growing relative resilience to risk moves and that the clear bidding at current levels.

Ethereum

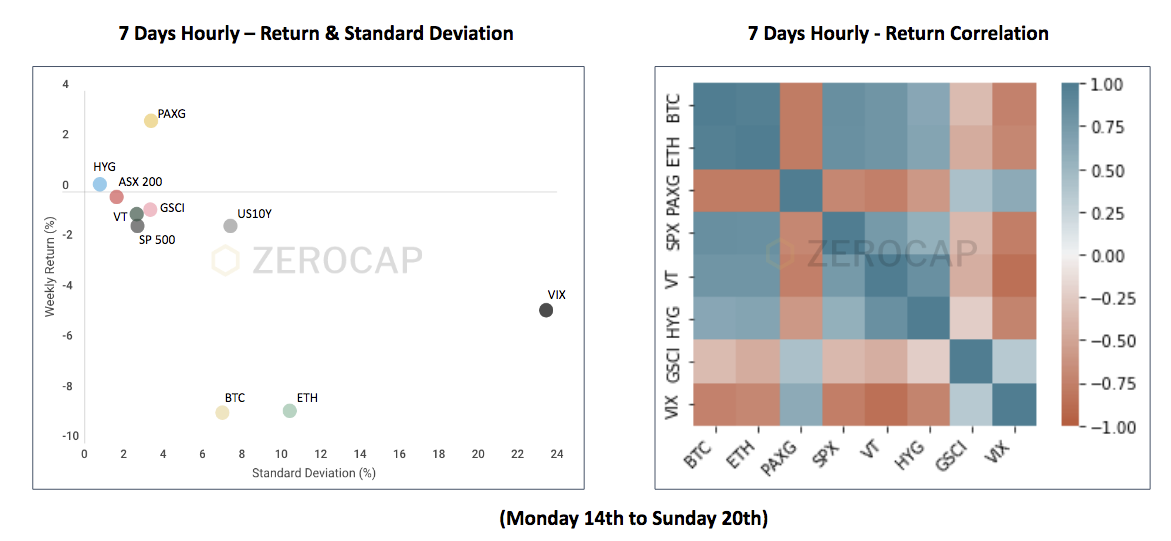

- Early on, as the FOMC minutes release drew closer and with tensions calming around the Ukraine border, ETH alongside other on-risk assets rallied, setting weekly highs around 3,200.

- Biden’s statement regarding a likely Ukraine invasion during the latter half of the week then fueled the risk-off atmosphere, with cryptocurrencies being the primary de-risking asset choice for investors during the weekend, setting weekly lows for ETH around 2,600.

- As expected, ETHBTC declined, aligning with expectations that BTC tends to outperform ETH during risk-off moves, and vice-versa.

ETHBTC Daily Chart

- Implied volatility remained relatively stable throughout the week, despite a -8% drawdown in ETH.

ETH ATM Implied Volatility

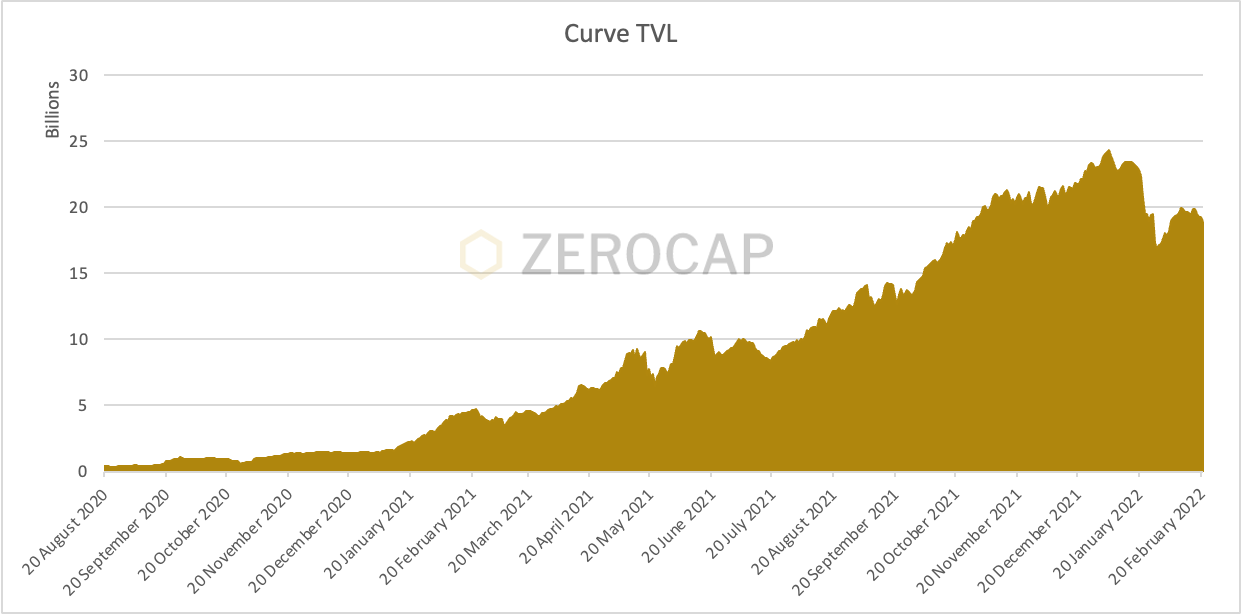

- The largest DeFi protocol in terms of Total Value Locked, Curve, offers low-fee and low-slippage DEX services for stablecoins. There are several projects designed to accumulate CRV (Curve’s governance token) in order to maximize boosted returns, and direct CRV emissions through their voting power. Currently, there exist 4 major projects, and 19 major DAO’s consistently accumulating CRV tokens. With its recent bridge into Polkadot facilitated by Moonbeam, the Curve wars are heating up.

Curve Total Value Locked (TVL)

- In contrast to BTC, net exchange inflows persisted throughout the week, with investors de-risking against looming geopolitical uncertainty. The supply expansion continues while funding rates oscillate, indicating that traders are undecided in the current atmosphere.

Ethereum Exchange Net Position Change

Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 9,485,647. This represents 7.93% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.- The highly anticipated Proof of Stake (Pos) transition in June 2022 is a primary incentive for ETH holders to continue accumulating for the mid-term, as the persistently high gas fee remains a fundamental bottleneck. However, a shift in short-term sentiment is evident, as the TVL of competitor L1 protocols is rising, consequently decreasing ETH’s market share in the DeFi ecosystem. While interoperability with ETH remains a priority for most L1 protocols, short-term sentiment remains geopolitical and macro reliant. If risk holds out, keep an eye on US GDP growth set to be released later this week.

DeFi & Innovation

- OpenSea suffers $1.7 million phishing attack targeting NFT migrations as the company establishes a platform-wide smart contracts upgrade – CEO speaks out.

- Binance Smart Chain becomes BNB Chain – the move is seen as strategic to distance the exchange from the decentralized network.

- JPMorgan opens an expo branch in Decentraland’s metaverse, after releasing a report describing Metaverse investments as a “$1T opportunity.”

- More than $300k in Digital Yuan was spent daily at the Winter Olympics.

- Twitter enables crypto users to give and receive Ethereum tips natively.

What to Watch

- Biden’s alleged executive order on cryptocurrencies.

- Russia x Ukraine conflict updates.

- US Preliminary GDP, on Thursday.

- US Core PCE, on Friday.

Insights

Article on Smart Beta – We have launched the Smart Beta Bitcoin Fund, offering balanced risk exposure to Bitcoin in a regulated unit trust. This piece explains the reasoning behind our unique new product, with data on how it performs against Bitcoin itself and the S&P 500.

FAQs

What significant regulatory and political events influenced the crypto market during the week of 21st February 2022?

The week saw several key events, including Biden’s expected executive order on crypto, the Federal Reserve’s approval of rules banning officials from trading cryptocurrencies, Russia’s stance on Bitcoin, and the Canadian Prime Minister’s invocation of the Emergency Act targeting crowdfunding and crypto addresses. Additionally, the SEC imposed a $100 million penalty on BlockFi, and the NYSE filed a trademark application for trading NFTs.

How did geopolitical tensions and macroeconomic factors impact Bitcoin and Ethereum’s price action during the week?

Bitcoin and Ethereum’s price action was significantly influenced by the geopolitical conflict in Ukraine and the anticipation of the FOMC minutes. An early push in Bitcoin’s price was prompted by a partial withdrawal of troops, but heightened tensions later led to a sell-off in the crypto markets. Ethereum followed a similar pattern, rallying early on and then facing a risk-off atmosphere due to Biden’s statement regarding a likely Ukraine invasion.

What were the major developments in the DeFi and Metaverse space during the week?

The DeFi and Metaverse space saw several key developments, including OpenSea’s $1.7 million phishing attack, Binance Smart Chain’s rebranding to BNB Chain, JPMorgan’s expo branch in Decentraland’s metaverse, and Twitter’s enablement of Ethereum tips. Additionally, more than $300k in Digital Yuan was spent daily at the Winter Olympics, and Curve’s Total Value Locked (TVL) continued to grow.

What were the key market trends and movements in the winners and losers of the week?

The fixed income market began on the backfoot, with ten-year UST yield pushing past 2%, and the German bund reaching 0.35%. The yield curve collapsed towards the end of the week due to escalating geopolitical concerns. Oil prices reached a seven-year high, supporting Shale-related stocks, while the prospect of global geopolitical tension weighed on sentiment.

What are the essential factors and events to watch in the coming week that could influence the crypto market?

Investors should keep an eye on Biden’s alleged executive order on cryptocurrencies, updates on the Russia-Ukraine conflict, US Preliminary GDP on Thursday, and US Core PCE on Friday. These factors, along with ongoing geopolitical and macroeconomic developments, could significantly influence market sentiment and price action in the crypto space.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 14 Feb. 2022 0:00 UTC to 20 Feb. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Hong Kong Approves Spot Bitcoin and Ether ETFs

Hong Kong’s recent approval of the first spot Bitcoin and Ether exchange-traded funds (ETFs) marks a significant milestone in the financial industry. These approvals position

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.