Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What led to the strong rally in Bitcoin this week, and how did Ethereum and other cryptocurrencies respond?

- How are the US SEC's approval of the first crypto ETF and other regulatory developments affecting the crypto market?

- What were the significant macroeconomic events and trends affecting the crypto and equity markets during the week?

- What are the technical indicators and on-chain signals suggesting about the current trends in Bitcoin and Ethereum?

- What are some notable developments in DeFi and innovation, and what should investors watch for in the coming week?

- Disclaimer

18 Oct, 21

Weekly Crypto Market Wrap, 18th October 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What led to the strong rally in Bitcoin this week, and how did Ethereum and other cryptocurrencies respond?

- How are the US SEC's approval of the first crypto ETF and other regulatory developments affecting the crypto market?

- What were the significant macroeconomic events and trends affecting the crypto and equity markets during the week?

- What are the technical indicators and on-chain signals suggesting about the current trends in Bitcoin and Ethereum?

- What are some notable developments in DeFi and innovation, and what should investors watch for in the coming week?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- US’ SEC approves the first crypto ETF, a bitcoin futures fund.

- September’s US CPI shows inflation rising at 5.4% yearly average, staying at 30-year high. FOMC Minutes records show Fed ready to reduce bond purchases in November with $15 billion monthly reductions set to end by mid 2022. Morgan Stanley CEO claims “this inflation is not transitory,” asks for Fed rate hikes.

- Biden approves debt ceiling extension by $480 million until early December.

- Australian Ransomware Action Plan; authorities will be able to freeze or seize digital currencies potentially linked to cybercrimes.

- ANZ settles debanking case with Australian bitcoin trader.

- US is now the largest bitcoin mining centre in the world – dominating mining hashrate distribution at 35.4% following China’s crackdown.

- Russian President Putin states that crypto technology “is legitimate and can be used in settlements,” Minister of Finance says Russia has no plans of banning digital assets.

- IMF releases report addressing challenges of global crypto implementation, stating it “may accelerate dollarization risks.”, at the same time downgrading the 2021 growth projection for major economies.

- Coinbase unveils Digital Asset Policy Proposal for comprehensive crypto regulations; seeks new frameworks, single regulatory agency, user protection and fair competition.

- G7 leaders issue guidelines for Central Bank Digital Currencies.

Winners & Losers

- Equity markets began the week on a weak note following a big miss in NFP data and global concerns escalating over price inflation due to supply chain disruptions and commodity constraints. However, as the week progressed, stock market focus turned to Q3 earnings reporting season. Out of 22% of all financial sector firms reporting from the S&P500, 92% has beat estimates. Within the reports, FICC and M&A dominated bottomline percentage performance beats.

- The VIX index retraced lower this week following better US Q3 reporting season and China’s PBoC confirming debt woes from Evergrande property to be “manageable” and not generate a contagion across sectors and credits. The CBOE VIX index opened the week at 20.00 but had retraced down to 16.30 by end of trading.

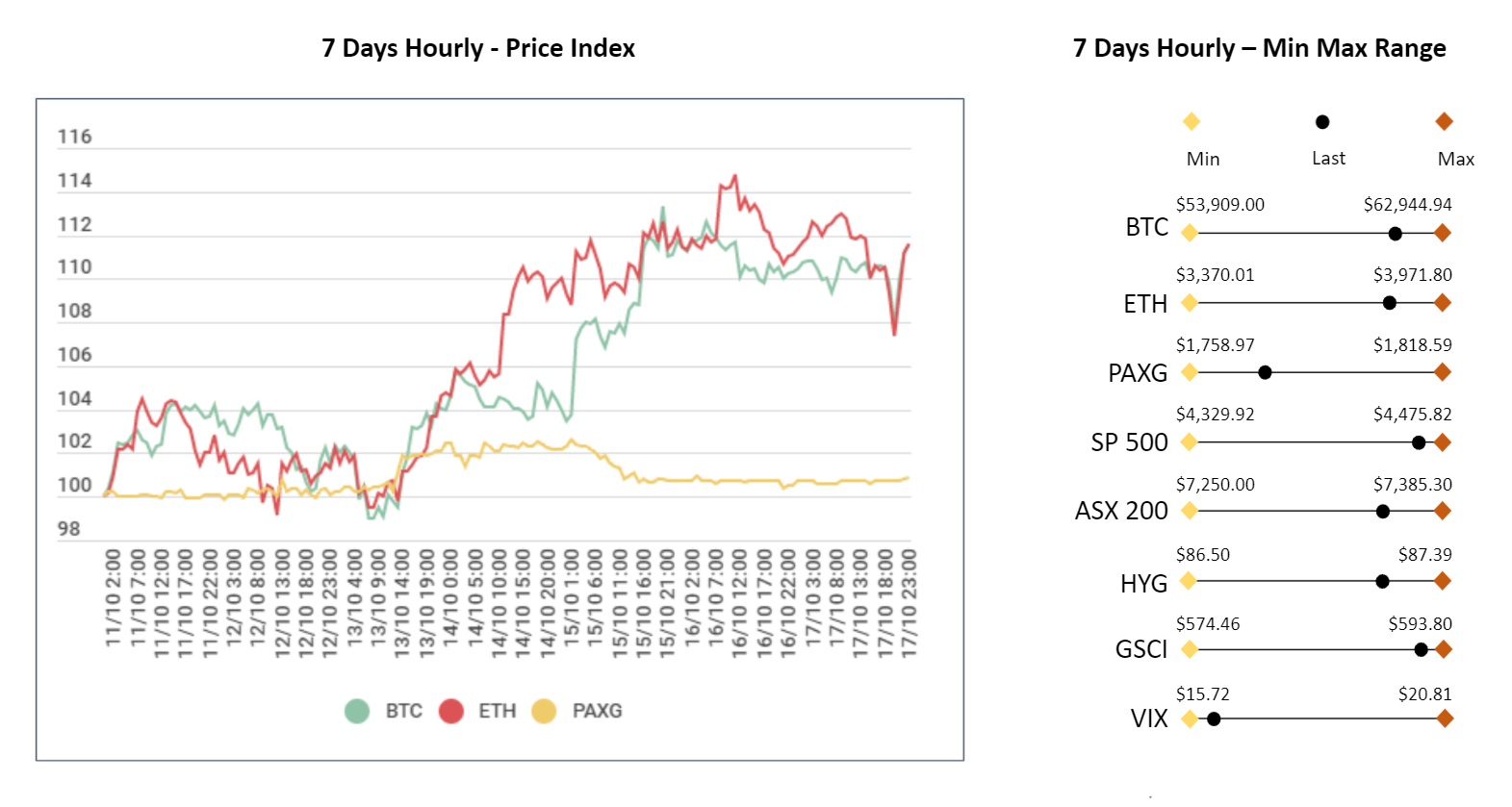

- BTC led a strong rally this week, predominantly fueled by speculation surrounding the potential for a BTC ETF to be approved in the US. Thursday evening (EST) saw the largest price surge as Bloomberg released news that the SEC would not oppose a BTC ETF from listing in the coming weeks. Ethereum followed suit, albeit showing a weaker performance. The rest of the market struggled to match price action as the majority of volume was directed to bitcoin. At the time of writing BTC’s price sits just US$2,500 under its ATH. Many are speculating over whether the BTC ETF is in fact a buy the rumour, sell the fact event. In any case, upon the launch of the product, we expect the volume of capital allocation to determine sentiment in the short-term. Overall, BTC and ETH both returned 12.59% WoW.

- US treasury yield curve bull steepening throughout the week, with the 10 year opening the week at 1.63% but dropping lower throughout to close at 1.59%. As markets now begin to price in a Jun 2022 FED rate hike, the 2 year yield pushed higher from opening of 0.35% towards 0.41% by Friday close. Following a RBNZ surprise hike, the BoE is due to follow with a potential pre-Christmas normalisation move of their own.

- There was little movement on Gold prices, but oil and coal prices reached multiyear levels. US WTI hit a seven-year high of $83.44 during the week, a level not seen since Nov 2014.

Macro, Technicals & Order Flow

Bitcoin

- BTC is on the move. Early indications that we were seeing an ETF approval were apparent in CME Futures open interest. The spike led by large firms building up their books in preparation. We then saw the speculation build, with the twitterverse blowing up on Bloomberg tickers being released and a host of other early indicators. Price naturally rallied on this, breaking the key 58,000 level and settling currently above all-time-highs. We are looking very bullish here – technically we’ve had the retest of the break, and price is well-bid.

- There was a question in the back of our minds – buy the rumour, sell the news? It was a risky long playing the break, but for those who did, the entry is sitting nicely with protection below the break and ascending topside trendline. Momentum is clearly behind this move, and given how close we are to all-time-highs, we could see a break this week.

- There are some caveats to this though – the futures ETF is far from perfect. Investors will be buying BTC at a premium, which begs the question as to whether we see strong expected volumes from day one of trading. Anything that indicates muted demand could bring BTC back into the range given the recent run it’s had.

CME Futures Open Interest (from Digital Gamma)

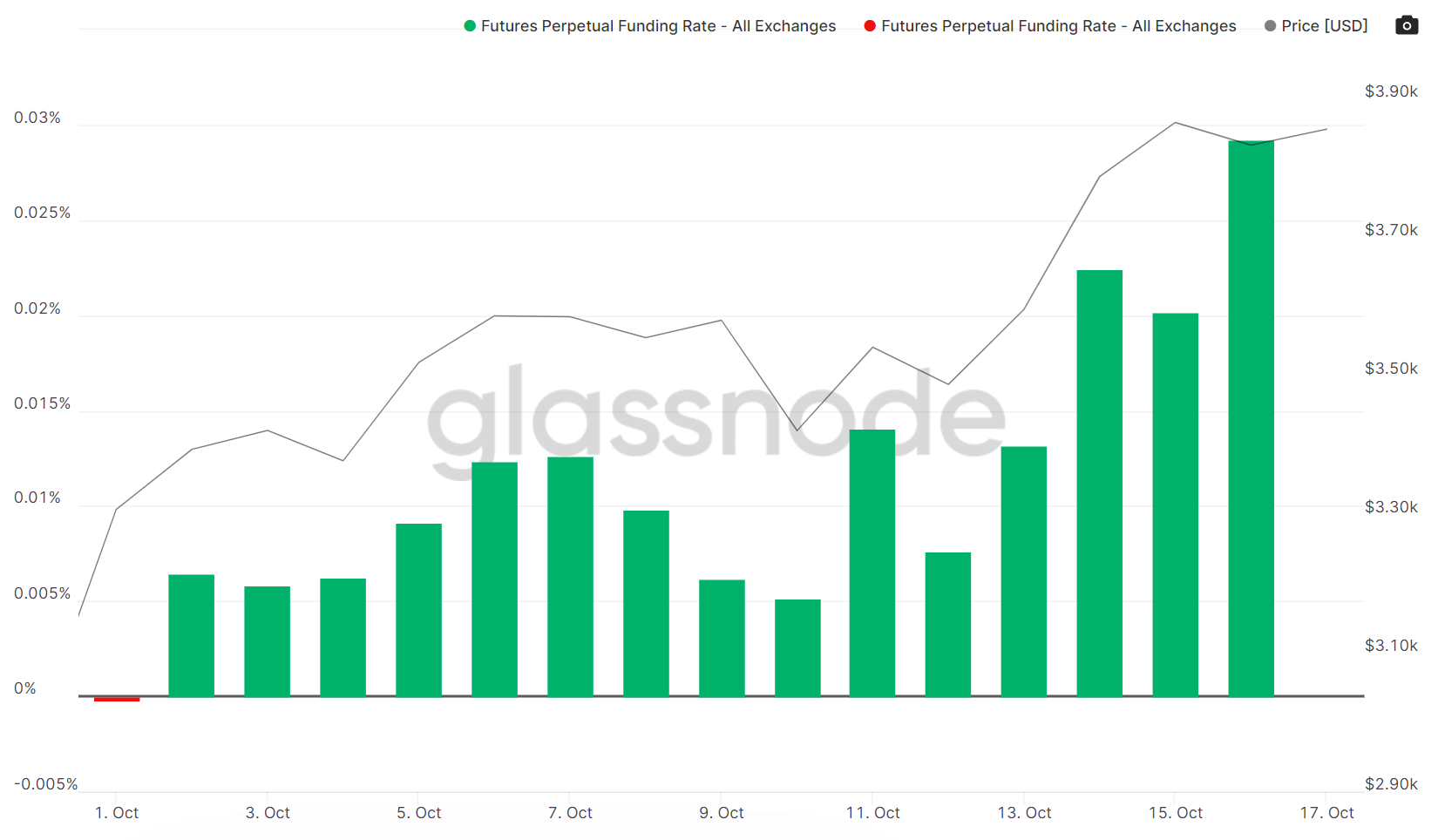

- Perpetual swaps funding rates are on the move. Retail is now joining the move, where fund flows and institutions have largely driven BTC to this point over the past few months. Open interest is also climbing, and is now above liquidation levels that we saw in the May and September drop. Liquidations would probably require a stimulus (newsflow) to drive a downward squeeze at this point, and given where we are sitting against a strong earnings season and some risk-on flows, it looks like we are moving toward a break rather than downside risk in the short-term.

BTC Perpetual Swaps Funding

Bitcoin Futures Open Interest

- Estimated Futures Leverage Ratio takes into account the exchange’s reserve balances as a function of open futures positions. Notably, whilst this is climbing, we are not seeing the highs we saw in May and September.

Bitcoin Futures Estimated Leverage Ratio

- We are still clearly seeing inflows from funds and institutional interest, even at these levels. Long-term holders continue to accumulate at a similar rate as they have been in the run-up over the past month.

Bitcoin Held By Funds

Bitcoin: Total Supply Held by Long-Term Holders

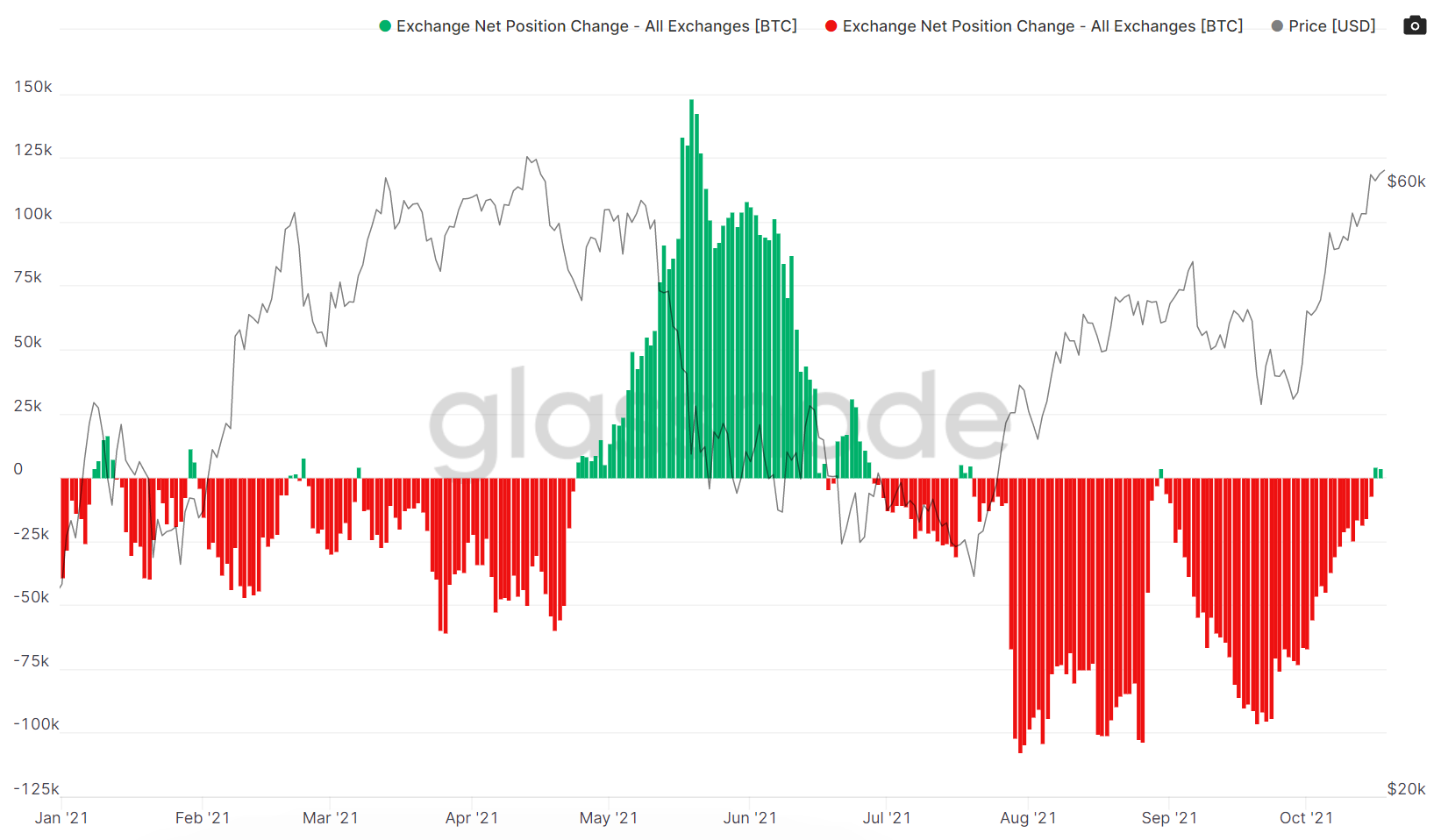

- On-chain signals, however, are beginning to show signs of moderation – or at least caution. Exchange flows have just turned positive, meaning that on-balance, more BTC is flowing into exchanges than out of them. This could be market makers and bigger players preparing for any signs of cyclical rotation, or traders ready to fade moves above highs. Tough to tell what’s behind the market structure – but if this continues to build, it could be a signal.

Bitcoin Net Position Change

- The futures basis curve is trading higher on the CME given ETF news. We’ve had a volatile week for the basis across crypto derivatives exchanges, settling at around 12% annualised now. The market is watching the CME basis for indications on the size of expected flow. A very real arbitrage opportunity exists if the flow into the CME futures outstrips supply, and the basis moves considerably higher. Large arbitrage opportunities by selling the CME future and buying spot may present themselves in the coming weeks. This arbitrage opportunity could directly position spot to move higher given contango dynamics. Keep an eye on this – we are largely in uncharted waters here.

BTC Futures Annualised Rolling 1 Mth Basis

Ethereum

- Ethereum is catching a bid on the back on BTC’s move, but definitely not as much as we would’ve expected. Particularly on the back on earnings results in equities and the risk-on sentiment toward the end of the week. Technically the pair saw a nice break above recent highs, and a similar rejection of prior resistance turned support. We are not convinced that ETH runs to all-time highs on the back of a BTC break. The market is not bidding aggressively, and transaction fees and congestion on the network have come back again given NFT flows. This week we paid $120 per transaction on a couple at the wrong time.

- The ETH/BTC trade we mentioned a while back is playing out nicely. ETH has broken below the 200-SMA, and despite an initial shaky break, we now look to be trading consistently below this level.

- On-chain data is still showing net outflows for ETH from exchanges, but nothing aggressively bullish.

Ethereum Exchange Net Position Change

- Perpetual funding rates are climbing, again showing retail’s participation in this move. It looks like the perps market is playing for a break alongside BTC – but again, I think we are seeing divergence that could last a few weeks between BTC and ETH.

ETH Perpetual Swaps Funding

- ETH basis curve trading above the CME on crypto derivatives exchanges, validating the book building theory on BTC CME futures. The curves are printing above 14% annualised which is good news for delta-neutral traders. Is this a resurgence of the market’s favourite yield play over the past few years? We hope so.

ETH Futures Annualised Rolling 1 Mth Basis

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 7,966,904 . This represents 6.75% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- Some of the layer 1 and 2 blockchains are continuing to hold their value – Fantom being another standout here, alongside Solana that seems to be floating at a happy level. Continued innovations and product launches against Ethereum’s transaction fees could very well lead to another pump in layers 1 and 2’s, particularly if the risk-on intermarket mood hangs around this week. Keep an eye on the risk environment for clues.

DeFi & Innovation

- Driven by DeFi, crypto volume in North America rose by 1000% year-over-year; Chainalysis report.

- Binance launches a $1 billion fund to fast-track crypto adoption.

- Canadian city becomes first to supply heat with bitcoin mining.

- Jack Dorsey’s Square plans to build an open-source bitcoin mining system.

- BitMEx’s CEO predicts bitcoin will be legal tender in five countries by 2022.

What to Watch

- It is now official: crypto ETFs are in the US. With their approval, regulatory concerns have been set aside for the moment as the big picture clearly shows governance support for the asset class. However, confusion around which government agencies should be in charge of crypto regulations remains. While the US’ SEC, Treasury, CFTC and more debate on the matter, the moment is one of celebration – we look forward to seeing the first crypto ETF begin trading this week, and monitor how the markets react to this important moment in history.

- A debt ceiling approval is not out of the ordinary in the US. With the Fed’s tapering structure well defined and national debt limit dealt with (for now), we’ll keep an eye on the Treasury’s release of their semiannual report on Friday and further Fed tapering statements following last week’s FOMC Minutes.

FAQs

What led to the strong rally in Bitcoin this week, and how did Ethereum and other cryptocurrencies respond?

The strong rally in Bitcoin was predominantly fueled by speculation surrounding the potential approval of a BTC ETF in the US. Ethereum followed suit but showed a weaker performance, and the rest of the market struggled to match Bitcoin’s price action.

How are the US SEC’s approval of the first crypto ETF and other regulatory developments affecting the crypto market?

The approval of the first crypto ETF in the US has set aside regulatory concerns for the moment, showing governance support for the asset class. However, confusion remains around which government agencies should be in charge of crypto regulations. The market is celebrating this moment and looking forward to the first crypto ETF trading.

What were the significant macroeconomic events and trends affecting the crypto and equity markets during the week?

Significant events included the US SEC’s approval of the first crypto ETF, US CPI showing inflation rising at 5.4%, Morgan Stanley’s CEO calling for Fed rate hikes, Biden’s debt ceiling extension, and the US becoming the largest Bitcoin mining center. Equity markets began weak but turned to Q3 earnings reporting season, with 92% of financial sector firms from the S&P 500 beating estimates.

What are the technical indicators and on-chain signals suggesting about the current trends in Bitcoin and Ethereum?

For Bitcoin, technical indicators are looking very bullish, with momentum behind the move and a potential break of all-time highs. On-chain signals are showing signs of caution with more BTC flowing into exchanges. For Ethereum, there’s a break above recent highs, but the market is not bidding aggressively, and transaction fees have returned.

What are some notable developments in DeFi and innovation, and what should investors watch for in the coming week?

Notable developments in DeFi include a 1000% year-over-year rise in crypto volume in North America, Binance’s $1 billion fund for crypto adoption, and Canadian city mining Bitcoin for heat supply. Investors should watch for the trading of the first crypto ETF, further Fed tapering statements, and the Treasury’s semiannual report.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 11 Oct. 2021 0:00 UTC to 17 Oct. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

What is the Base Blockchain? The Coinbase Layer 2

The Base blockchain, introduced by Coinbase, represents a significant development in the realm of cryptocurrency and blockchain technology. It is a layer-2 solution built on

Bitcoin Mining in the US: Main Challenges

Bitcoin mining in the United States has recently faced a range of challenges, from regulatory hurdles to community and environmental concerns. As a significant hub

Bitcoin Halving: Market Reacts

The 2024 Bitcoin halving, a significant event for the cryptocurrency world, marked a notable shift in the market dynamics of Bitcoin. As the block reward

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.