Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the key inflation figures in the US and Euro zone in December 2022?

- What are some notable developments in the crypto space mentioned in the report?

- How did Bitcoin and Ethereum perform during the week of the report?

- What are some key trends and events in the DeFi and Innovation space?

- What are some key events to watch for in the future according to the report?

- Disclaimer

17 Jan, 22

Weekly Crypto Market Wrap, 17th January 2022

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What were the key inflation figures in the US and Euro zone in December 2022?

- What are some notable developments in the crypto space mentioned in the report?

- How did Bitcoin and Ethereum perform during the week of the report?

- What are some key trends and events in the DeFi and Innovation space?

- What are some key events to watch for in the future according to the report?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- US Consumer Prices for December reach 7% inflation (5.5% ex Food and Energy), the highest rate in close to 40 years.

- Jerome Powell testimonial for his second mandate as Fed Chair:

- States a cryptocurrency report from the Reserve will be released “within weeks.”

- Believes the US economy no longer needs “aggressive stimulus.”

- The Fed is ready to act in controlling increasing price pressures if high inflation levels last beyond mid-2022.

- ECB President Lagarde states the European central bank will “do everything it takes” to get inflation down to 2% – Euro zone rates hit 5% last December.

- US FDIC-backed US banks form consortium to release new “USDF” stablecoin.

- US Fed’s Lael Brainard calls for Congress to decide on creating a CBDC to compete with China’s digital yuan.

- Crypto funds outperformed traditional hedge funds in 2021; HFR data.

- IMF research states that “crypto assets […] have matured from an obscure asset class with few users to an integral part of the digital asset revolution” – affirms positive regulatory adoption will greatly improve the ecosystem.

- Over 24% of small to mid-sized businesses plan to accept crypto payments; Visa survey.

- Square’s Cash App integrates Bitcoin’s Lightning Network for crypto payments.

- Tether (USDT) freezes $150 million from three addresses to allegedly comply with US law enforcement requirements.

- Pakistan’s government plans to ban cryptocurrencies; local industrialists oppose potential decision.

- Tesla to accept dogecoin payments for company merchandise.

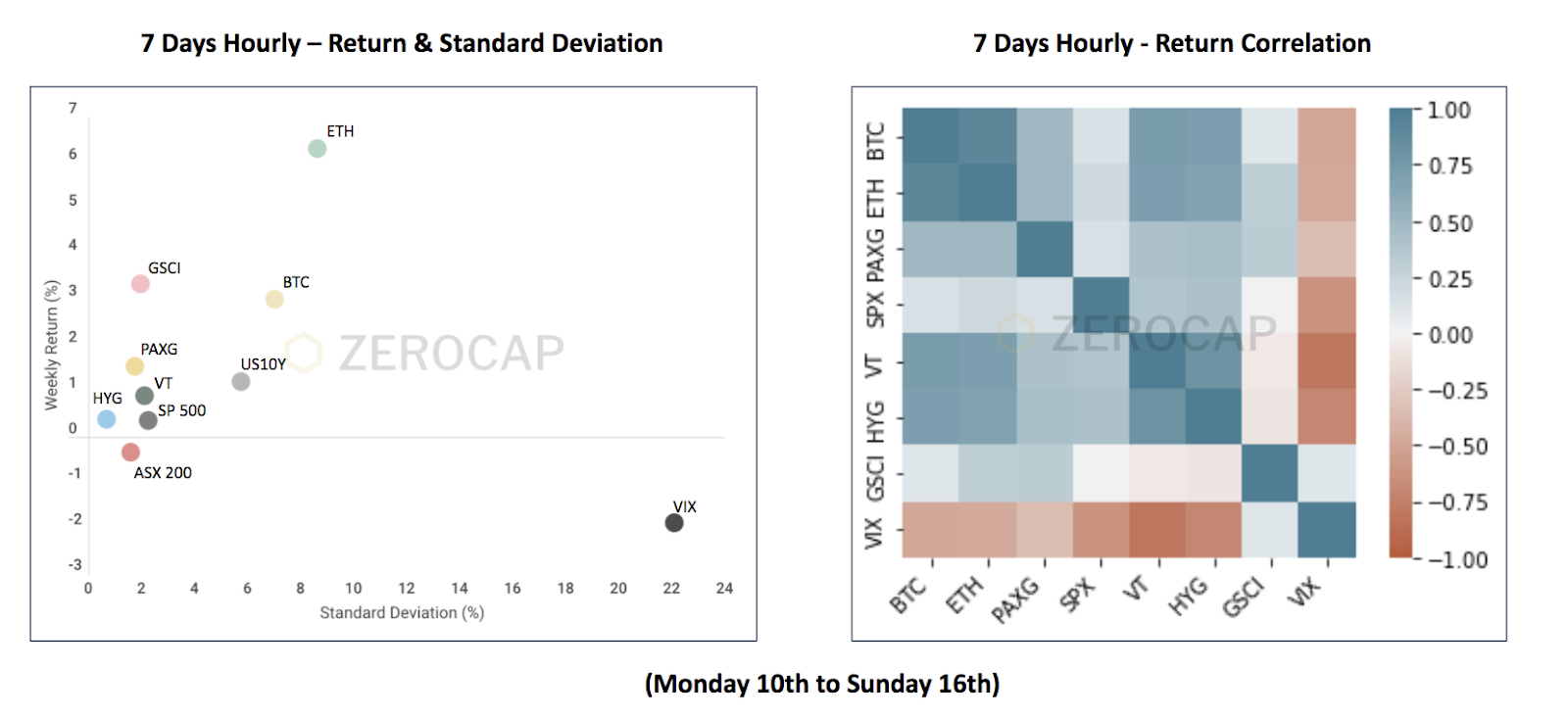

Winners & Losers

- After setting a weekly low around 39,500 early in the week, BTC alongside other risk-on assets rallied as inflation data came through inline with expectations. Crypto market liquidity remains thin on the short rally. Overall, BTC returned 3.00% and ETH returned 6.30% WoW.

- The US reporting season began with the banking sector, and it was not pretty. Both Citibank and JP Morgan disappointed analyst’s expectations, with their share price reflecting the disappointment – JPM dropping from around the $170 mark to a low of $157 following the announcement. While growth and tech stocks attempted to recover from the previous week’s selloff, momentum did not last – with the Nasdaq index closing the week close to its monthly low. Conversely, the MSCI Asia ex-Japan index performed better than its developed market counterparts, with the index climbing 2% for the week. The higher US yield curve has impacted emerging markets with depreciative pressure on the currency and outflow from asset markets.

- The fixed income market continues to take a beating as more institutional portfolios reduce their allocation for 2022. The 10-year UST sold off aggressively following the US CPI report, bringing inflation to a 39-year high. The 10-year yield curve climbed above 1.80% before settling the week at 1.77%. At the same time, the more speculative 30-year yield has risen from the year-end closing of 1.90% to a high of 2.13% in the last two weeks. On the credit side, Chinese property developers were again on the headline for the wrong reasons. Despite an agreement to extend payment terms for Evergrande, another developer Yuzhou attempted to delay payment on USD582 million to avoid default, sending its bonds and shares tumbling. The central bank, PBoC, cut rates on their one year lending rates for the first time since early 2020 when the pandemic first hit economic growth.

- Volatility levels were supported due to both the bond and tech shares selloff, geopolitical concerns from Russia, and North Korea’s renewed projectile launch in the Japanese sea. The CBOE VIX index swung between 17.5 to a high of 23 during the week, moving in phase with attempted risk recovery, but overall remained well supported by fear.

- The FX and commodity markets played the role of risk indicator this week. The USD index started on a positive note at above 96, then quickly retraced below 94.60 as risk parity trades unwind. AUDJPY cross was under pressure for most of the week, dropping towards 82 at one stage, the lowest in 2022. Gold prices fluctuated around the $1,800 mark with little directional trend. Despite supply-side disruptions due to workers’ absence, the longer-term prediction is for economic activity to slow down from central bank tightening of monetary conditions, thus leading to weaker commodity prices and demand for the rest of the forecast period.

Macro, Technicals & Order Flow

Bitcoin

- Last week, BTC resided within the 42,000 – 43,000 range. Unsettled markets, still feeling the effects from last week’s minutes on the Fed’s December meeting caused enough bearish pressure to set a temporary weekly low below 40,000.

- The bulls did not give up easily, quickly reverting the price to 41,000. The bearish sentiment apparent early in the week was short-lived. The mood transitioned to risk-on mid-week when investor’s inflation expectations were met, despite inflation printing at extremely elevated levels. The on-expectation news flowed into the crypto space where BTC reached weekly highs around the 44,000 level. BTC has consolidated around 43,000 forming an important support at the 42,000 mark. On the topside, resistance sits around 46,000.

- Where to from here? We’ve got leverage building in different parts of the space and market structure beginning to form what could lead to a short-squeeze.

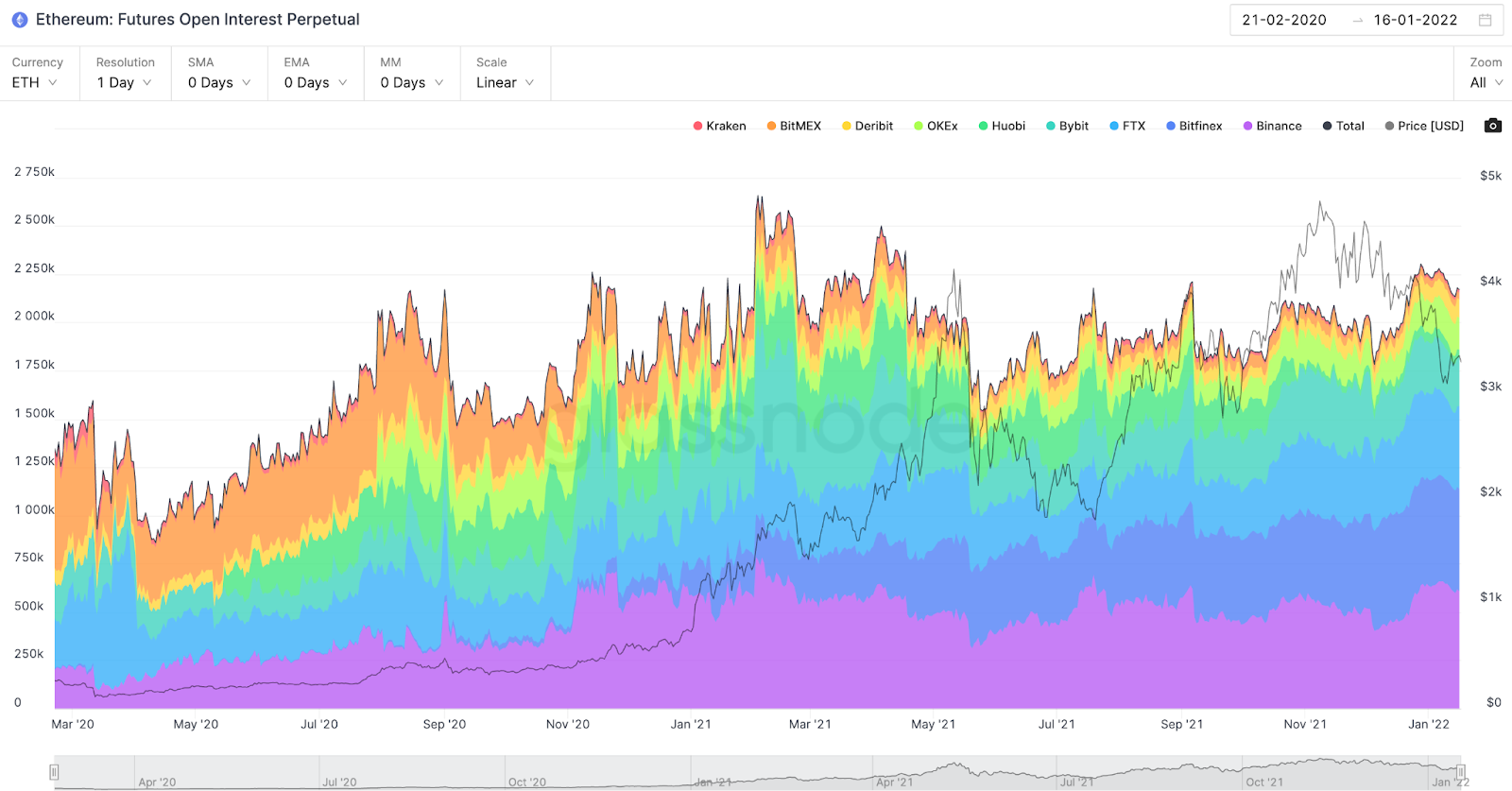

- BTC futures open interest is close to highs.

- BTC futures open interest leverage ratio, which tracks the market open contract value divided by the market cap of the asset, is hovering at just under 2.0%. Glassnode’s recent memo notably commented last week that this level has been a precursor to contract liquidations.

- This leverage is dominated by Binance (retail focused).

BTC Futures Open Interest

BTC Futures + Perpetual Open Interest Leverage Ratio

- Perpetual funding rates (majority short-term traders) are weighted to the short-side, with notable on-chain metrics showing accumulation by longer-term holders.

BTC Funding Rate Across Exchanges

Bitcoin Net Position Change of long-term wallets

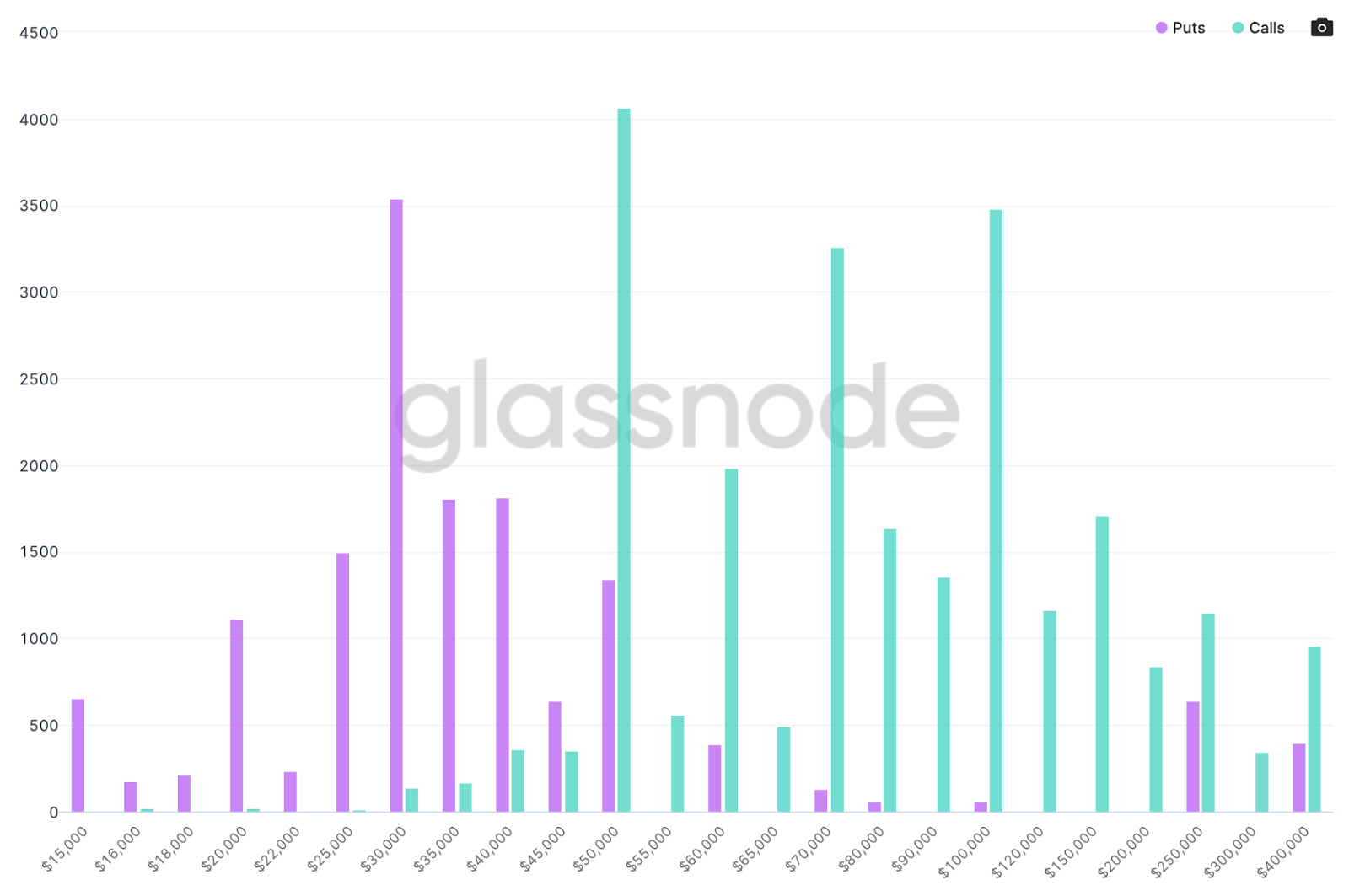

- Out to Mar 25, 2022, open interest is growing in weight at the 50,000, 70,000 and 100,000 levels. Emphasis is growing at the 30,000 level for puts. Implied volatility is compressing – we are at some cheap levels for volatility right here.

OI Interest by Strike – Mar 25, 2022

BTC Implied Volatility

- The futures basis curve’s recent decline has slightly recovered this week, although we are still at historically low levels.. Basis curves in CME dipped into the negatives, closing out the week around 3%. USD funding rates have dropped alongside the curve.

BTC Futures Annualised Rolling 1 Mth Basis (Deribit & CME)

Bitcoin Futures Open Interest

- Moving into the latter part of January, bullish plays are starting to look very good. Bitcoin has fallen significantly over the last few months. From its high in early October 2021, it has lost over 40% of its value. Implied volatility is so low (historically), there are some great ways to play a topside squeeze. In-house, we are running bull call spreads to capture cheap calls on the front-end, and cheapening these by selling volatility at the long-end.

Ethereum

- Similarly to Bitcoin, Ethereum set its weekly lows early in the week. The asset fell to 2,900 following market uncertainty from last week’s FEDs minutes before subsequently rebounding. Despite inflation reaching 39-year highs, risk-on assets rallied as CPI data met expectations. Definitely feels like less-bad news is good news at the moment.

- Bullish sentiment built throughout the remainder of the week, marking weekly highs around 3,400. Despite a temporary venture below the 3,000 mark, this level retains relevance alongside 2,550 as key supports. Notably, as ETH rallied it’s implied volatility diminished.

- Several L1 blockchains, including NEAR, FTM, ATOM & ONE experienced significant upside. Key layer 1’s are not only competing with Ethereum, but also offering very distinct value – from bridging blockchains to DeFi to NFTs.

ETH ATM Implied Volatility

- January 2022 has continued to be the best month for NFTs in terms of volume and active traders. In January thus far, OpenSea has averaged $200m+ of daily volume and hit a new all-time-high of 80k unique active daily traders. Whilst crypto asset pricing has broadly remained relatively contained this week, the continued influx of interest in NFTs supports the growing narrative of independent sub-sectors within the space decoupling from each other.

OpenSea Activity (Delphi)

- Following the announcement of a $150m funding round led by Three Arrows Capital, NEAR has continued to form new all-time-highs. NEAR’S bullish sentiment was reinforced by the launch of Aurora, a protocol built on NEAR that bridges ETH protocols to NEAR.

- Despite the recent stagnation of most blockchain ecosystems, Fantom gained over $1.20 billion (+20%) in its TVL over the past week. This growth was largely due to Andre Cronje and Danielle Sestagalli’s recent hints regarding their involvement in the FTM ecosystem. FTM definitely still holds value when compared to other Layer 1 blockchains – the fully-diluted market cap is significantly less than major competitors (SOL, AVAX etc..).

L1 tokens price action (Delphi)

- Open interest out to Mar 25, 2022 depicts heavy weightings at the 15,000 level, with growing interest at the 5,000 and 6,000 levels for calls. Whilst lackluster, some interest grows at the 3,000 and 2,000 levels for puts.

ETH Open Interest by Strike: Mar 25, 2022

- ETHBTC tested traded higher – showing ETH’s prominence when risk-on hits the market.

ETHBTC Daily Chart

- The continued supply expansion on exchanges has been persistent since mid-December, as net inflows continue into 2022. However, these inflows have faded quickly, looking to turn negative again.

Ethereum Exchange Net Position Change

- On aggregate, funding rates trended negatively throughout the week, flipping slightly positive today, implying uncertainty amongst short-term traders – and like BTC, signalling short-interest in a market with growing leverage.

ETH Perpetual Funding Rates

ETH Perpetual Open Interest

- The futures basis curve saw contained volatility throughout the week, suppressed on the back of uncertainty.

ETH Futures Annualised Rolling 1 Mth Basis

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 9,034,930. This represents 7.58% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- In the face of the collective rally of alternative L1 blockchain ecosystems capturing ETH’s market share, there is a sense of urgency to transition to a Proof of Stake system. That said, ETH’s EIP-1559 protocol is still burning ETH and instilling deflationary characteristics – ETH’s total issuance last week was negative, leaning towards supply crunches. Moving forward, ETH’s price action will likely mimic BTC in the short-term as liquidity remains thin and the two major assets follow short-term risk moves. This said, there is a growing possibility of a short-squeeze in BTC and ETH – keep an eye on leverage and implied volatility getting ready to breakout.

DeFi & Innovation

- Jack Dorsey announces a Bitcoin Legal Defense Fund for blockchain developers and lawyers.

- Meta recruits over 100 employees from Microsoft and Apple for its metaverse division.

- Digital yuan wallet tops mobile app store charts in China.

- Disney patents technology for a metaverse theme park.

- Rio de Janeiro’s mayor set to invest 1% of the city’s reserves in crypto.

What to Watch

- Great Britain’s CPI.

- BOE Gov Bailey testifies before Treasury Committee on stability report.

- Australia’s unemployment rate.

FAQs

What were the key inflation figures in the US and Euro zone in December 2022?

US Consumer Prices for December reached 7% inflation, the highest rate in close to 40 years. Euro zone rates hit 5% last December.

What are some notable developments in the crypto space mentioned in the report?

Developments include the formation of a consortium by US FDIC-backed banks to release a new stablecoin, Tesla’s acceptance of Dogecoin for merchandise, and Square’s integration of Bitcoin’s Lightning Network for crypto payments.

How did Bitcoin and Ethereum perform during the week of the report?

Bitcoin set a temporary weekly low below 40,000 before reaching weekly highs around 44,000. Ethereum fell to 2,900 before rebounding to mark weekly highs around 3,400.

What are some key trends and events in the DeFi and Innovation space?

Jack Dorsey announced a Bitcoin Legal Defense Fund, Meta recruited over 100 employees for its metaverse division, and Disney patented technology for a metaverse theme park.

What are some key events to watch for in the future according to the report?

Events to watch include Great Britain’s CPI, BOE Gov Bailey’s testimony before the Treasury Committee, Australia’s unemployment rate, and potential economic slowdown due to central bank tightening of monetary conditions.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 10 Jan. 2022 0:00 UTC to 16 Jan. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Ethereum Smart Contracts: How They Changed Crypto

Ethereum, launched in 2015, revolutionized the digital world by introducing “smart contracts,” self-executing contracts with the terms of the agreement directly written into code. This

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.