Content

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What significant events occurred in the crypto market during the week of 15th November 2021?

- Q: How did Bitcoin and Ethereum perform during this week?

- Q: What were the macroeconomic factors affecting the crypto market?

- Q: What developments occurred in the DeFi and Innovation sector?

- Q: What are some key things to watch in the coming week?

- Disclaimer

15 Nov, 21

Weekly Crypto Market Wrap, 15th November 2021

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- Q: What significant events occurred in the crypto market during the week of 15th November 2021?

- Q: How did Bitcoin and Ethereum perform during this week?

- Q: What were the macroeconomic factors affecting the crypto market?

- Q: What developments occurred in the DeFi and Innovation sector?

- Q: What are some key things to watch in the coming week?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Week in Review

- US CPI rises at the fastest inflation pace in three decades, jumping 0.9% last month, while PPI increased by 0.6%.

- Lael Brainard and Jerome Powell interviewed by Biden in the White House regarding the next Fed Chair term – White House doesn’t see Powell’s recent trades as an issue for a second term appointment.

- BItcoin’s “Taproot” upgrade, the first major update in four years, was successfully implemented.

- US Congress plans “demystifying crypto” committee hearing on November 17th.

- European Commission urges members to agree on crypto regulations by year’s end.

- Combined crypto market caps hit three trillion dollars for the first time.

- Grayscale flippens world’s largest gold fund, hits $60B AUM.

- Pew Research Center – 16% of Americans have invested in cryptocurrencies.

- Mastercard partners with crypto companies to launch crypto-linked cards in APAC.

- United Nations Climate Change Conference (COP26) reaches deal for carbon markets – highlights need for sustainable crypto solutions.

- Microsoft’s Decentralized Identity team launches a Digital ID project on the Bitcoin network, set to create key-less blockchain IDs for online identity authentication.

- VanEck’s Bitcoin futures ETF starts trading on Tuesday as XBTF, days after the US SEC rejected their spot BTC ETF application.

- Miami set to hand out bitcoin to residents from the city’s crypto profits.

Winners & Losers

- After a few weeks of mixed performance across the crypto markets, this week saw a resurgence of strength in BTC, overcoming the 63k mark with volume and quickly shooting up to a new high of $68,700 by Tuesday. Inflation data out of the US led to further upside on Wednesday, although the momentum could not be sustained. Following the establishment of a new all-time high at $69,000, the asset tumbled 7% in a matter of hours as late longs were punished with liquidations as stops were hit. The remainder of the week was spent recovering as open interest settled and funding rates reset. ETH followed suit, as did the rest of the market with a minority of assets outperforming on the back of fundamental drivers. Overall, BTC returned 3.49% and ETH returned 0.29% WoW.

- U.S. stocks saw the first week of retracement since early October as inflation concerns weakened consumer sentiment to a decade low. Despite extended negotiations over climate change talks for COP26 in Glasgow, the final draft of conclusive talks failed to deliver a hard move away from fossil fuel reduction by 2030. Commodity and mining shares rallied on the result. Shares of Tesla Inc. initially dropped by 12% following CEO Musk offloading USD 7 billion worth of his shareholding. Evergrande, the world’s most indebted developer, managed to meet the deadline to service the coupon payments of its offshore debt obligations, which led to a rebound on Chinese shares both at home and listing abroad. Shares in JD.com, the second-largest online retailer in China, also rallied following its initiation to employ PBoC’s CBDC in the form of payment options.

- Macroeconomic data concentrated on inflation and consumer sentiment from the US- PPI (8.6% p.a. And 6.8% ex Food & Energy, Same as forecast), CPI (6.2% p.a. Vs 5.9% forecast and 4.6% vs 4.3% forecast ex F&E). The higher inflation data, especially through the consumer end, weighed heavily on the Michigan consumer sentiment report, which fell to a ten year low. Given that the consumer sector contributes to 70% of the US annual GDP output, renewed concern on stagflation emerged, and the bond market took the brunt of the pain.

- The bond market was the pain trade for the week; despite stocks retracing off ATH and ending in the red WoW, bond yields highlighted most of the inflationary concerns from investors. 10 yr UST began the week at 1.43% but closed up 13bp to 1.56%. 30 yr UST are now only 3bp away from the important 2% threshold resistance. The credit market recovered some ground following the confirmation of coupon payment by Evergrande’s offshore USD debt. Still, China will reveal October’s property prices, retail sales and industrial production in the coming week to plot the direction for the economy’s forward momentum.

- The VIX index was subdued despite a weekly fall in the S&P 500. The US Veterans Day holiday on Thursday also shortened the trading week, limiting much of the actions.

- Gold benefited as a function of hedging flows, despite a stronger DXY index following the higher inflation data reports. The market began the week below $1,800 but quickly penetrated the previous resistance level to close the week at $1,865, with the next resistance at the 14th June high of 1877.70. Oil prices weakened from last week’s seven-year high to close lower just above the $80 WTI support level. The continual unwinding of a supply-side squeeze on the positioning was visible in addition to stronger USD reference.

Macro, Technicals & Order Flow

Bitcoin

- We got the break of all-time highs that we forecasted this week, touching 69,000. The inflation data out of the US was concerning – the highest inflation spike since 1990. We saw an initial run, before BTC and the rest of the market began to sell-off. Altcoins took a plunge as the day progressed, with investors selling the fear, and asking questions later. By Asia close, the market was clearly bid again – with equity futures catching a bid, and the risk environment beginning to turn.

- “It’s almost like we are in this period of invincible optimism,” Liz Young, head of investment strategy at SoFi. It does amaze us that we are continuing to bid risk on the back of concerning inflation numbers, but as they say – the market can stay irrational longer than you can stay solvent, so I certainly wouldn’t be shorting risk in any sizable way until we see some real signs of a turning point.

- The fact that the market is bidding BTC at times when gold would normally rally on flights to safety and inflation hedge flows, is indicative of sentiment should we see a meaningful shift in risk trends.

- Technically, price has rejected off support at 63,000, after taking out stops below this level, which coincides with the descending trendline from Oct 20.

- Open interest out to Dec 31 is still dominated by 100,000 calls. With the next two interest levels at 120,000 and 200,000. Some fairly wild speculation here, but a great ‘tell’ on sentiment levels.

OI Interest by Strike – Dec 31, 2021

- Bitcoin supply held by long-term holders is slowing, indicating some profit-taking at these levels by the smart money. There is generally a time lag between moderation in accumulation by these holders and a turn in the market, very similar to the Commitments of Traders (COT) report released by the CFTC in the traditional world, tracking commercials vs speculators. Keep an eye on this metric for longer-term shifts in trend.

Bitcoin: Total Supply Held by Long-Term Holders

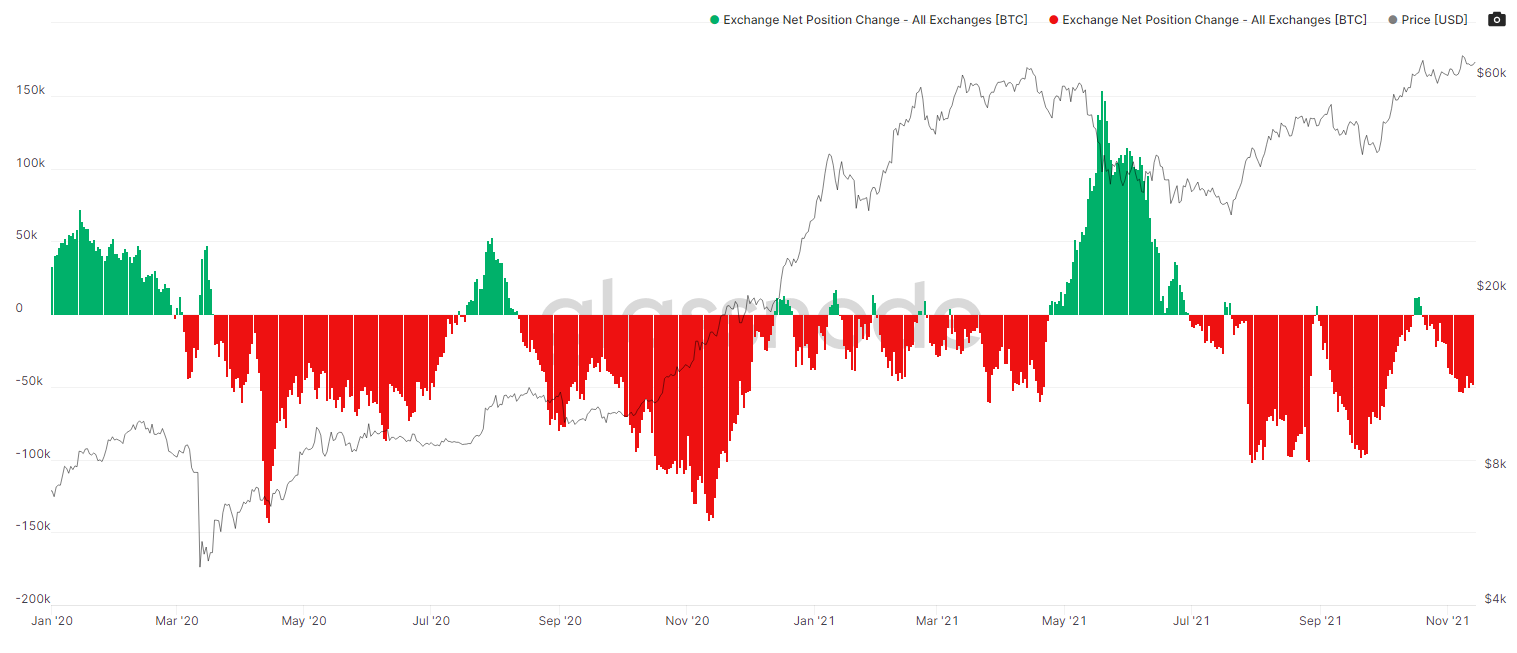

- On-chain data is showing net-outflows from exchanges (indicating a contraction in supply), with velocity slowing. We are still at comparatively moderate levels here, with room to further contain supply.

Bitcoin Net Position Change

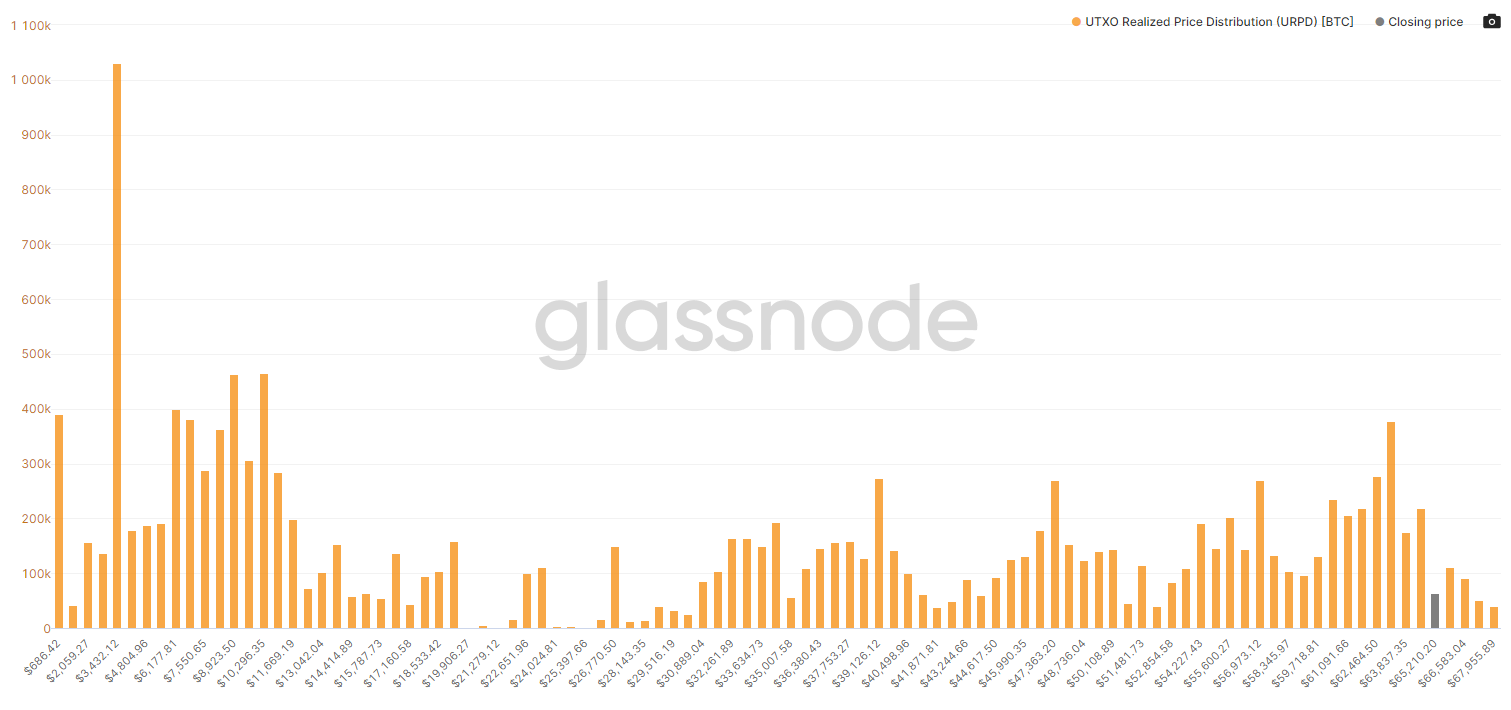

- The on-chain UTXO price distribution shows the depth of bitcoin activity at certain price levels. The prior week saw a clean break higher on the lack of UTXO activity above key levels. We are in a similar position now, with declining activity to the highs. This bodes well for another run higher – the ‘path of least resistance’.

UTXO Realised Price Distribution

- The futures basis curve has compressed over this week on the back of future price uncertainty and arbitrage flows. Open interest levels are elevated, signalling short interest in futures. The basis trade is back – and even with elevated ETF futures buying, compression is floating back into the market.

BTC Futures Annualised Rolling 1 Mth Basis

Bitcoin Futures Open Interest

- Perpetual funding rates have had a few more resets this week. Long interest received a serve on the break higher, whilst short interest felt it on the way back up. We are now sitting at low funding levels on the perps, which like dated futures, could indicate growing short interest at these levels. There is room to run at the current funding rates and levels if we see any bullish stimulus or newsflow.

BTC Perpetual Liquidations 1W

BTC Perpetual Swaps Funding

- The Estimated Leverage Ratio has retraced slightly, diminishing chances of any wild downside liquidations, although volatility is always possible near highs.

Bitcoin Futures Estimated Leverage Ratio

- One last piece of newsflow to note – The Van Eck spot ETF was declined in the US, citing further concerns around pricing manipulation. The fact that BTC held up against this news is encouraging – the question in our minds is whether ASIC in Australia will follow this logic.

- In summary, it looks like a buoyant week ahead for BTC.

Ethereum

- We mentioned that open interest had clearly been focused on the 5,000 psychological level. Our OTC desk was seeing profit-taking between 4,800 and 4,950 with some trades playing the break above 5,000. We got above 4,800, but struggled with momentum. The inflation data led to some fairly hefty repositioning, but price still respected the ascending trendline from early October, albeit with a few false breaks. We now sit at 4,700, playing the bounce higher.

- From the macro view, we still see potential headwinds for ETH in growth rolls over in traditional markets. This said, there are some very interesting structural factors at play. Smart contract growth persists, as supply declines. From late in 2020, the ETH supply on exchanges declined from around 28% to 11% as of earlier this month. Smart contract growth has clearly gone the other direction.

ETH Smart Contract Growth vs Supply (Delphi Digital)

- DeFi and multichain activity continue to accelerate, and we expect this trend to continue in the short to medium-term. Increased on-chain activity and high gas prices led to ETH having its first deflationary week since its inception earlier in November. All of which point to supply constraints.

- Open interest to Dec 31 in the options markets is gunning for a squeeze, with the 5,000 and 10,000 levels clearly favoured.

ETH Open Interest by Strike: Dec 31, 2021

- Strong outflows from exchanges (indicating contraction in supply) support the derivatives market sentiment. On-chain data is continuing to show larger wallet holders with supply held of 10 to 100 ETH slowing, showing a similar market structure to bitcoin.

Ethereum Exchange Net Position Change

Supply Held by Wallets with Balances of 10-100 ETH

- Perpetual funding rates, like BTC, had a cleanout – and are now at moderate levels.

ETH Perpetual Swaps Funding

- The futures basis curve is also compressing on short interest, similar to BTC.

ETH Futures Annualised Rolling 1 Mth Basis

- Amongst this, institutional interest in ETH continues to grow, with the Grayscale AUM flying.

Ethereum Grayscale AUM

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 8,230,678. This represents 6.95% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- All in all, the risk environment is holding steady – price has been bid across risk against the inflation data out of the US. Combining on-chain and structural factors, we are looking for a healthy week for ETH.

DeFi & Innovation

- Morgan Stanley note; the metaverse is the next big investment theme.

- JPMorgan note says DeFi growth slower than it seems, mostly fueled by a surge in ETH price.

- Twitter launches “Twitter Crypto” task force to explore potential projects for the platform.

- University of Cambridge to launch decentralized carbon-credit marketplace on the Tezos blockchain.

- Elected New York Mayor Eric Adams wants crypto to be taught in schools.

What to Watch

- President Joe Biden and Xi Jinping’s virtual meeting this Monday.

- US retail sales report.

- RBA’s Monetary Policy meeting minutes.

- US Congress “demystifying crypto” committee hearing on Wednesday.

- First network results following the Bitcoin Taproot upgrade.

- VanEck’s bitcoin futures ETF results, starting Tuesday.

FAQs

Q: What significant events occurred in the crypto market during the week of 15th November 2021?

A: The week saw the fastest inflation pace in the US in three decades, Bitcoin’s “Taproot” upgrade was successfully implemented, combined crypto market caps hit three trillion dollars, and the United Nations Climate Change Conference reached a deal for carbon markets. Additionally, Microsoft launched a Digital ID project on the Bitcoin network, and Miami planned to hand out Bitcoin to residents from the city’s crypto profits.

Q: How did Bitcoin and Ethereum perform during this week?

A: Bitcoin broke all-time highs, touching $69,000, but then tumbled 7% before recovering. Overall, BTC returned 3.49%. Ethereum struggled with momentum, reaching above $4,800 but not sustaining it. ETH returned 0.29% for the week.

Q: What were the macroeconomic factors affecting the crypto market?

A: U.S. inflation data, consumer sentiment, bond market trends, and macroeconomic data on inflation and consumer sentiment from the US were key factors. The higher inflation data weighed heavily on consumer sentiment, renewing concerns about stagflation.

Q: What developments occurred in the DeFi and Innovation sector?

A: Morgan Stanley noted the metaverse as the next big investment theme, Twitter launched a “Twitter Crypto” task force, the University of Cambridge planned to launch a decentralized carbon-credit marketplace on the Tezos blockchain, and the elected New York Mayor expressed a desire for crypto to be taught in schools.

Q: What are some key things to watch in the coming week?

A: Key events to watch include President Joe Biden and Xi Jinping’s virtual meeting, the US retail sales report, the RBA’s Monetary Policy meeting minutes, the US Congress “demystifying crypto” committee hearing, the first network results following the Bitcoin Taproot upgrade, and VanEck’s Bitcoin futures ETF results starting Tuesday.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 8 Nov. 2021 0:00 UTC to 14 Nov. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Hong Kong Approves Spot Bitcoin and Ether ETFs

Hong Kong’s recent approval of the first spot Bitcoin and Ether exchange-traded funds (ETFs) marks a significant milestone in the financial industry. These approvals position

Weekly Crypto Market Wrap, 15th April 2024

Download the PDF Zerocap provides digital asset liquidity and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.