Content

- Week in Review

- Winners & Losers

- Celsius Related Events

- Technicals & Order Flow

- Bitcoin

- Ethereum

- Altcoins

- Innovation

- NFTs & Metaverse

- What to Watch

- Insights

- FAQs

- What were the key events in the crypto market during the week of 14th June 2022?

- What issues did the Celsius Network face during this week?

- How did Bitcoin and Ethereum perform during this week?

- What notable events occurred in the altcoin market?

- What is Jack Dorsey's Bitcoin-driven venture, TBD?

- What developments occurred in the NFT and Metaverse space?

- What should investors watch out for in the coming week?

14 Jun, 22

Weekly Crypto Market Wrap, 14th June 2022

- Week in Review

- Winners & Losers

- Celsius Related Events

- Technicals & Order Flow

- Bitcoin

- Ethereum

- Altcoins

- Innovation

- NFTs & Metaverse

- What to Watch

- Insights

- FAQs

- What were the key events in the crypto market during the week of 14th June 2022?

- What issues did the Celsius Network face during this week?

- How did Bitcoin and Ethereum perform during this week?

- What notable events occurred in the altcoin market?

- What is Jack Dorsey's Bitcoin-driven venture, TBD?

- What developments occurred in the NFT and Metaverse space?

- What should investors watch out for in the coming week?

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Note on release date: This week’s Weekly Crypto Market Wrap was released on a Tuesday due to the Queen’s Birthday public holiday in Australia, on the 13th of June.

Week in Review

- US inflation rises rapidly again at 8.6%, with May’s Consumer Price Index (CPI) report.

- European Central Bank to raise interests rates by 25 basis points starting July, also set to end net asset purchases.

- US Senators Cynthia Lummis and Kirsten Gillibrand release bipartisan bill to regulate digital assets – crypto to be labelled as commodities under CFTC authority.

- Leaked copy of a separate US bill shows intention to ban decentralised crypto projects unless they legally register in the United States.

- Celsius Network freezes customer services including withdrawals to “honor […] obligations” amidst market volatility – Binance temporarily paused BTC withdrawals on the Bitcoin Network due to network congestion.

- PayPal enables transfers of any crypto to external wallets.

- Two more spot crypto ETFs launch in Australia.

- IMF recommends eco-friendly CBDCs and non-PoW cryptos for payments.

- New York State releases guidance on how to issue dollar-backed stablecoins.

- MasterCard to allow its 2.9 billion users to make direct NFT purchases without crypto.

- Binance under investigation by US SEC over legitimacy of BNB token following its controversial Reuters piece – Senior Director responds.

- Twitter founder Jack Dorsey and Jay-Z announce Bitcoin Brooklyn Educational Program.

- Terra (LUNA/UST) founder Do Kwon denies allegations of moving $2.7B prior to crash.

Winners & Losers

Macro Environment

- Asset markets took a turn for the worse when US CPI data showed an acceleration in both headline and core price inflation above market expectations. Just when many economists called the peak of inflationary reading to be behind us, and markets had begun to price for stability with the FED in control of the yield curve, the data told a very different story. The bond market led the selling, with 10 yr UST yield last hitting 3.41%. US investment bank JP Morgan also uplifted their call for a 75 bp hike from the upcoming FOMC meeting in the coming week. Stocks, Gold, Japanese YEN, Emerging Market currencies and Cryptocurrency markets went into panic liquidation mode. MSCI’s index of worldwide equity had slumped by 21% YTD, confirming the entry into “Bear” market territory.

- Long-Term Capital Management failed in 1998 due to over-leveraged Delta neutral spread basis trades. Lehman Brothers Inc failed in 2008 due to over-leverage in duration credit trades. Innovation of products assured us that large institutions would not face the same risk time after time. However, the downside risk of over-leverage appears to be the killer blow to major players within the investment industry now and then. This week saw one of the largest liquidity providers in the cryptocurrency space, Celsius, stop the withdrawal of client funds and transfers. The headline generated panic when the rest of the financial markets were already in a risk aversion environment (following the elevated risk central bank policy tightening). One of the speculations leading to Celsius’s troubles was that an over-leveraged maturity mismatch position was generated on their balance sheet. The company had introduced a synthetic ETH (stETH) mechanism where the client deposits ETH for staking purposes (lock up for validation), while still have the flexibility to withdraw their holdings using the stETH anytime. As risk aversion began in the asset markets, Celsius’s clients began to withdraw stETH rapidly. When withdrawal became too fast, too much, Celsius’s own balance sheet could not satisfy the “bank run”. While pausing withdrawal would have been a prudent strategy in terms of risk management, the end effect is similar to shutting the gates during a traditional bank run. Hedge funds in liquidity trouble employed a similar strategy during the GFC of 2008, where a “gate” was closed to the redemption of invested funds. The result was the same in all situations; investors and lenders panicked. The market began to price in the required amount of liquidation of Celsius’s existing cryptocurrency assets to satisfy short-term liabilities. A bottleneck effect spiralled into more selling and more triggering of liquidation requirements across the industry. History has shown us that the loss of confidence created by overleveraged mismatching strategies seldom ends well.

Celsius Related Events

- Celsius is a well-known decentralised finance (DeFi) protocol that offers lending and borrowing. Similar to traditional finance (TradFi), Celsius’ borrowers are overcollateralised. The Celsius app has grown in popularity and possesses over 1.7 million users. As of May 17th, Celsius acclaimed $11.7 billion USD assets under management and noted more than $8 billion USD in loan revenues.

- In the past, Celsius has had problems related to liquidity that arose from losses incurred from DeFi exploits. In May 2021, Celsius lost over 35k ETH, worth about $70 million USD. Further, in December 2021, hackers extracted 896 wBTC from a Celsius MetaMask wallet, valued at $54 million USD. To make matters worse, Celsius had about $500 million USD worth of client deposits in Anchor when LUNA collapsed. Claims have since arisen suggesting that Celsius possesses a lack of liquidity and cannot honour client withdrawals. As a result, these claims imply that Celsius runs the risk of insolvency.

- This week, the price ratio between stETH and ETH fell from 1:1. As the price equivalence deteriorated, entities began exiting positions. In a matter of hours, Alameda Research unloaded nearly 50k of stETH and faced severe slippage upon exit. Subsequently, Celsius, who holds almost 450k stETH worth approximately $1.5 billion USD, entered the spotlight. Utilising the DeFi protocol AAVE, Celsius has previously deposited their stETH as collateral, accumulating over $1.2 billion USD in debt. As stETH began trading for as low as 0.92 ETH, the community began fearing the possibility of Celsius’ liquidation and the potential ramifications this would have on the market.

- Given that Celsius experienced substantial withdrawals during the Luna crash, the participants’ fears of a potential liquidation may have been exaggerated. Notably, Celsius’ assets under management have decreased by approximately 56% in 6 months, with the withdrawal of assets likely contributing to this figure. On June 13th, in order to prevent insolvency and preserve liquidity, Celsius paused all withdrawals, swaps and transfers between accounts. Celsius justified its decision given the extreme market conditions. Subsequent to the withdrawal, the price of Celsius’ CEL token is down

- More recently, Celsius has been accumulating collateral in the form of Wrapped Bitcoin (WBTC). This accumulation is to provide coverage for a loan executed through Maker. The loan, worth $521,837,213.3 at current price levels, has a liquidation price level of $16,852. Whilst the origin and purpose of the loan are unknown, transparency around liquidation levels likely adds to market fear and speculation.

Technicals & Order Flow

Bitcoin

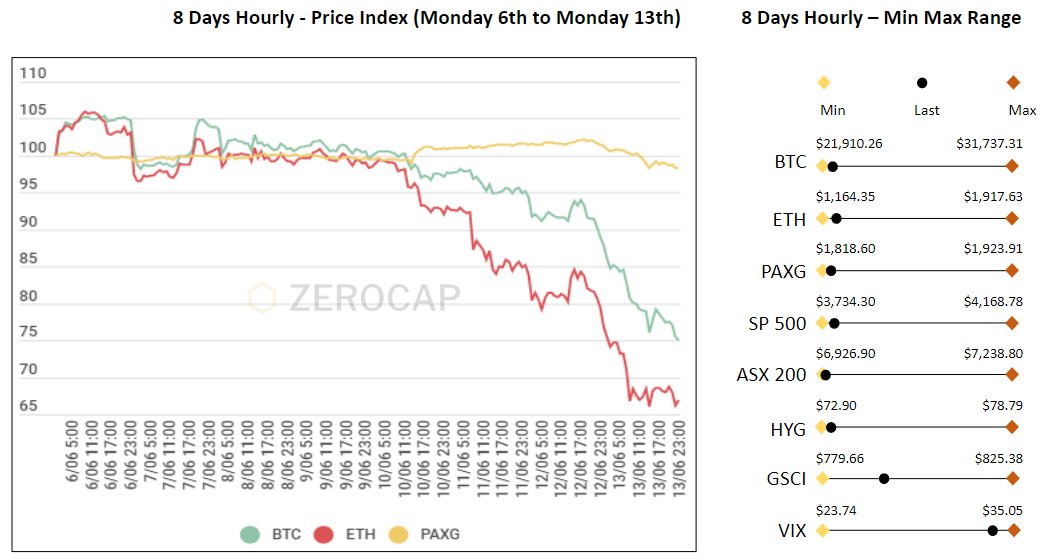

- This week, Bitcoin initially edged higher, breaking above 31,000 before retracing off overhead resistance at 31,500. Action chopped around 30,000 downward momentum forced price below key support at 27,700. A spiral of liquidations followed, causing prices to cascade to levels not seen since December 2020.

- Bitcoin continues to struggle as the Monetary Policy Outlook tightens. The release of CPI data out of the US on Friday, missing expectations, acted as a stimulus for significant de-risking across assets. Bitcoin’s price edged lower following the news.

- Microstrategy, which began accumulating Bitcoin in late 2020, now holds over 120,000 Bitcoin. Acquiring Bitcoin at an average price of approximately 32,000, Microstrategy’s unrealised losses are now estimated to be over $1B. If Microstrategy chooses to liquidate even a portion of these holdings, the price could be significantly affected.

- WoW (06/06 to 12/06), Bitcoin returned -11.10%. Accompanied by over $1b in liquidations on Monday 13th, Bitcoin experienced a further -15.5% drawdown within 24 hours.

- Used as a metric to compare market valuation to the utilisation of its network, Bitcoin’s Entity-Adjusted Dormancy Flows are placed at levels last seen in December 2018. This indicates that market valuation could be undervalued when compared to the time-weighted on-chain transaction volume.

- Looking at derivatives data, it can be seen that since March, Bitcoin’s 25d Skew has edged upward. Depicting the difference between Implied Volatility between puts and calls, greater levels are indicative of relatively greater demand for puts against the risk backdrop.

- Last week, Bitcoin broke a 9-week long downtrend, offering positive returns week on week. This week, we saw the market take these gains back. The release of CPI data, which missed expectations, reaffirmed bearish sentiment. Despite some on-chain metrics continuing to paint a bullish picture, derivatives traders are clearly favouring downside protection. Eyes are now fixated on downside support placed at 19,650, a level that marks the top of the 2017 bull run. As the Monetary Policy Outlook continues to dictate sentiment and action, participants await Thursday’s Interest Rate decision from the Fed. Against all the fear, we will see a bottom at some point – playing implied volatility via Structured Products for accumulation is rational right now when taking a longer-term view.

Ethereum

- Despite the success of the Ropsten Testnet, a simulation of the Ethereum merge, market participants were left unphased and price action, early in the week, reflected this. Following some seesawing action toward the end of the week, Ethereum’s price plummeted. Higher-than-expected CPI numbers forced risk-assets to aggressively sell-off. The previously tested price support of 1,700 gave way, crashing through to close at 1,434. The close marked a 20.6% decline over the week. Fears driven largely by the aforementioned Celsius insolvency concerns, created extreme selling pressures on Monday 13th and the price fell a further 18.59%, closing the day at 1,207.

- Friday’s news, which worsened the macroeconomic backdrop, compounded the already bearish sentiment that has captivated market participants since the beginning of Q1 2022. The collapse of Luna, paired with fears of a similar fallout regarding Celsius, has spooked bullish Ethereum participants who only recently were wagering large bets on the outcome of the merge. With a successful Ropsten merge simulation offering little to no price support, it would be expected that any delays or hiccups in the development team’s preparations will have a significant impact on price.

ETHBTC Daily Chart

- Bitcoin continues to outperform Ethereum during market turmoil. WoW, ETH/BTC dropped 10.8%. Fears, exacerbated by the break of the STETH/ETH ratio, likely placed pressure on large STETH holders to de-risk their portfolios. Within its current range, there is limited support for the pair. Key support is placed at 0.046, painting a bleak outlook for Ethereum. A breakthrough at this level from above could eventuate in another significant move lower.

- Ethereum’s MVRV Z-Score captures ETH’s realised price and compares it to the current spot price, measuring the standard deviations away from its intrinsic value. The current MVRV Z-Score is currently placed below 0. Historically, when this value falls below 0 it has indicated enticing accumulation levels and local market bottoms.

- STETH, a liquid staking derivative of Ethereum obtained through the Lido protocol, traded at a considerable discount over the weekend. Participants were forced to sell their holdings to cover short-term debt obligations. STETH will be redeemable for 1:1 with ETH when withdrawals are enabled post-merge, thus implying that short-term fluctuations in the price of STETH are based on the demand and liquidity for staked ETH.

- Overall, ten consecutive weeks of Ethereum price declines paints a dismal picture of Ethereum YTD performance. In saying this, on-chain data shows signs of capitulation and we are beginning to reach historical levels commonly used to signal accumulation opportunities. With the momentum and hype surrounding the ETH 2.0 merge being outweighed by macro and external factors, longer-term positioning in Ethereum could be attractive at these levels.

Altcoins

- USDD, the native stablecoin of the Tron ecosystem, recently lost its $1 USD peg. Similarly to Luna’s UST, Tron’s stablecoin is algorithmic and backed by tokens like BTC, USDT and USDC as opposed to fiat. This week, USDD reached a low of $0.911 USD. To bolster the peg’s defences, the Tron DAO added 700 million USDC to its reserves. Justin Sun, the founder of Tron, noted that the Tron DAO reserve intends to deploy $2 billion USD into perpetual future contracts to protect TRX by de-incentivising traders to short TRX perpetual contracts. Notably, since USDD’s value fell below $1 USD its value has not returned back to its intended peg and is now sitting at $0.98 USD.

Innovation

- Jack Dorsey’s Bitcoin-driven venture, TBD, has announced its ambitions to create a new decentralised Web platform, named “Web 5”. The former Twitter CEO’s disdain for Web 3 is due to his perception of venture capitalists controlling the space. The name Web 5 comes from the summation of Web 2 and Web 3. This foregrounds TBD’s plans to create a decentralised platform (Web 3) that utilises elements of Web 2. Web 5 will provide users with a decentralised identity that enables them to utilise different applications without repetitively logging in. Further, users will own their data as opposed to third parties.

- Blockchain data analytics platform, Nansen, is partnering with Google Cloud. Moving from BigQuery to Google Cloud’s scalable infrastructure, Nansen plans to stay ahead of its growing user base which has increased by 20 times in the last year. More efficient speeds, via the new infrastructure, should more effectively provide digital asset investors with on-chain data.

NFTs & Metaverse

- Mastercard announced its partnership with a number of NFT marketplaces to enable cardholders to buy these assets with fiat. In its recent study, global payment giant found that 45% of those surveyed had purchased NFTs or considered buying one. Moreover, Mastercard reported that half of the individuals surveyed wanted more flexibility and ease when buying NFTs. The company intends to provide NFT investors similar degrees of protection that they would receive when making transactions online with a Mastercard card.

- After losing his Bored Ape Yacht Club (BAYC) NFT in May, actor Seth Green has been reunited with the asset. Subsequent to the phishing exploit, an NFT investor, DarkWing84, purchased Green’s BAYC. Green and DarkWing84 recently reached an agreement for the resale of the NFT. Blockchain records depict that the actor’s wallet transferred 165 ETH, $297k USD at the time, to DarkWing84 just before the stolen NFT was sent back to Green.

- Neal Stephenson, the author who coined the term ‘metaverse’ in his 1992 science fiction novel, Snow Crash, is creating his own metaverse. The new protocol will be a metaverse-focused layer 1 blockchain named Lamina1. This blockchain will initially be used for a 2D metaverse. Down the line, Lamina1 will be utilised to create a fully immersive 3D open metaverse, akin to that described in Snow Crash.

- In the midst of further attacks from the Russian military, Ukraine will digitise its cultural artefacts as NFTs on the blockchain to preserve this window into the country’s cultural DNA. Ukraine has already used crypto to raise $135 million USD for the financing of its defence against Russia. The announcement was made by NEAR Protocol’s co-founder Illia Polosukhin. NEAR was later revealed to be the first blockchain partner of Ukraine in the digitisation of its art and history.

What to Watch

- Federal Reserve’s economic projections, funds rate and a press conference on Wednesday.

- UK’s new monetary policy summary, on Thursday.

- Fed Chair Jerome Powell speaks at an inaugural Washington conference on the international role of the US dollar, on Friday.

Insights

How to access Web 3 – Overview, the Technology and a Case Study on Brave Browser:

Analyst Edward Goldman provides a timely overview of Web 3; how to access it, the technology available and under development with a case study on the Brave browser – currently the most popular access point for Web 3.0.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | SPGSCI | U.S. 10Y |

FAQs

What were the key events in the crypto market during the week of 14th June 2022?

The week was marked by several significant events, including the rise in US inflation, the European Central Bank’s decision to raise interest rates, and the release of a bipartisan bill to regulate digital assets in the US. A leaked copy of a US bill also showed an intention to ban decentralized crypto projects unless they legally register in the US.

What issues did the Celsius Network face during this week?

The Celsius Network had to freeze customer services, including withdrawals, due to market volatility. This was a significant event as it affected the operations of one of the major players in the crypto market.

How did Bitcoin and Ethereum perform during this week?

The article provides a technical analysis of Bitcoin and Ethereum, discussing their performance and market trends. For detailed insights, it’s recommended to read the specific section in the article.

What notable events occurred in the altcoin market?

One of the significant events in the altcoin market was the native stablecoin of the Tron ecosystem, USDD, losing its $1 USD peg. This event had implications for the stability and trust in the altcoin market.

What is Jack Dorsey’s Bitcoin-driven venture, TBD?

TBD is a new venture by Jack Dorsey that aims to create a new decentralized Web platform, named “Web 5”. The project is expected to leverage Bitcoin and blockchain technology to redefine the internet.

What developments occurred in the NFT and Metaverse space?

Mastercard partnered with several NFT marketplaces to enable cardholders to buy these assets with fiat. Additionally, Ukraine decided to digitize its cultural artefacts as NFTs on the blockchain to preserve the country’s cultural DNA.

What should investors watch out for in the coming week?

Investors should keep an eye on the Federal Reserve’s economic projections, funds rate, and a press conference, as well as the UK’s new monetary policy summary. These events could have significant implications for the crypto market.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 6 Jun. 2022 0:00 UTC to 12 Jun. 2022 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

This document is issued by Zerocap Pty Ltd (Zerocap), an Authorised Representative (#001289130) of AFSL 340799. This document is made available to you on the basis that you are a Wholesale or Professional Investor. This document is not intended for retail clients nor should it be distributed to retail investors. This document has been prepared for information purposes only and may not be relied on for any other purpose (including, without limitation, as legal, tax, financial or investment advice). Nothing in this document should be interpreted as an endorsement or recommendation of a particular investment or strategy. Any opinions expressed are general in nature and do not consider the objectives, financial situation or needs of any person. Before making an investment decision you should conduct your own due diligence, consider what is suitable for you and your personal circumstances and obtain your own independent advice. Zerocap Pty Ltd (Zerocap) makes no representation or warranty (express or implied) that any information contained in this document is accurate or complete. Information included in this document is based on matters as they exist as of the date of preparation of this document and will not be updated or otherwise revised. Certain statements reflect Zerocap’s views, estimates, opinions or predictions which may be based on proprietary models and assumptions, and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realised. There are significant uncertainties inherent in the forward-looking statements included in this document. Neither historical returns nor economic, market or other indications of performance should be considered as an indication of future results or performance. Investing in cryptocurrencies and/or digital assets involves a substantial degree of risk and could result in the loss of the entire amount invested. Nothing in this document is intended to imply that investing in cryptocurrencies and/or digital assets may be considered “conservative”, “safe”, “risk free”, or “risk averse”.

You should be aware that dealing in products that are leveraged carries significantly greater risk than non-leveraged products. As such, you could both gain and lose larger amounts. You may even sustain losses well in excess of your initial deposit and also in excess of the margin required to establish and maintain any positions in the leveraged products. Accordingly, you should carefully consider whether leveraged products are appropriate for you in light of your financial circumstances and risk profile.

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Ethereum Smart Contracts: How They Changed Crypto

Ethereum, launched in 2015, revolutionized the digital world by introducing “smart contracts,” self-executing contracts with the terms of the agreement directly written into code. This

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.