Content

- One year of Weekly Crypto Market Wrap

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What significant milestones were achieved in the crypto market during the week of 11th October 2021?

- How did Bitcoin perform compared to Ethereum and other digital assets during the week?

- What were the key macroeconomic factors influencing the crypto market during the week?

- What developments occurred in the DeFi and innovation sector in the crypto space?

- What should investors watch for in the coming weeks in the crypto market?

- Disclaimer

11 Oct, 21

Weekly Crypto Market Wrap, 11th October 2021

- One year of Weekly Crypto Market Wrap

- Week in Review

- Winners & Losers

- Macro, Technicals & Order Flow

- Bitcoin

- Ethereum

- DeFi & Innovation

- What to Watch

- FAQs

- What significant milestones were achieved in the crypto market during the week of 11th October 2021?

- How did Bitcoin perform compared to Ethereum and other digital assets during the week?

- What were the key macroeconomic factors influencing the crypto market during the week?

- What developments occurred in the DeFi and innovation sector in the crypto space?

- What should investors watch for in the coming weeks in the crypto market?

- Disclaimer

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

One year of Weekly Crypto Market Wrap

It’s been a whole year since we started writing this weekly newsletter. The crypto market has grown substantially since October of 2020 and so has Zerocap. The team is truly grateful for all subscribers and will continue to provide expert analysis of the ecosystem for many years ahead. Onward!

Week in Review

- Senate votes to raise US debt ceiling until December 3, extending the limit to an extra $480 billion – deferring the risk for a pre-Christmas political showdown.

- The US Jobs report disappoints again, with only 194,000 jobs added in September (against almost 500,000 forecasted). Some blamed calendar miscounting on the 161,000 drop in education employment due to the pandemic. Market still pricing in bond tapering this year.

- US WTI crude price at seven-year high, lack of recent investment in infrastructure the main constraints on supply. Several central banks anticipate a rise in inflationary expectation and normalisation of interest rates between 2022-2023.

- The US Justice Department sets up a National Cryptocurrency Enforcement Team. Senator Elizabeth Warren introduces bill to investigate fiat and crypto roles in ransomware.

- US’ SEC approves ETF that tracks stocks with high exposure to bitcoin, while chair Gary Gensler says the SEC has no intention of banning crypto. Market anticipates a Futures based ETF to be approved soon.

- US Bank launches crypto custody services through partnership with NYDIG.

- George Soros’ fund made an allocation to bitcoin, suggesting the cryptocurrency has long-term potential.

- Amount of ETH held by miners reached its highest level since 2016.

- Bank of America publishes a report with a bullish outlook on the future of cryptocurrencies.

- Institutions buying bitcoin rather than gold as a hedge against inflation according to JPMorgan.

- Crypto transactions in Asia surged 706% over the past year due to institutional adoption.

Winners & Losers

- Equity markets began the week on a positive note as speculation of an official government intervention to bail out Evergrande was on the cards; the EV unit of the embattled property giant rallied 20% on the HK exchange. However, as the week progressed, it was obvious that Evergrande and several other Chinese developers were running into trouble servicing their offshore USD bond repayment. Anticipation for a strong US Non-farm payroll figure was the highlight of the week, as mid-week ADP and initial claims data both emerged above expectations. Stocks end the week off highs, with the NFP employment report missing the mark (194k vs 488k exp), equities still up 0.8% WoW.

- The VIX index remained elevated for most of the week with credit, geopolitical, and inflationary concerns supporting risk aversion, however risk moderated as the week concluded. The index closed just below the 20 level at 18.77 after peaking out at 22.96 earlier.

- Digital assets saw a drop in correlation to traditional markets this week as bitcoin crossed a $1 trillion market cap for the first time since May. With the bitcoin futures premium surging to 12.8% p.a., the move appears to be driven by institutional flows, likely a result of the US’ recent net positive crypto news coverage and the potential for a BTC ETF to be approved in the coming months. Ethereum and the broader crypto market saw mixed returns on the week, boosting BTC dominance. This is likely a result of capital rotation within the sector as well as a divergence in narrative between BTC and the rest of the market (BTC acting as an inflation hedge), while others were broadly treated as tech stocks. Overall, BTC returned 13.44% and ETH 0.07%.

- US treasury yield curve bear steepening throughout the week, with the 30 year closing near high of 2.16%, and 10 year at 1.61%. There was a small retracement following the weaker than expected NFP data release, though the market adjusted to price in the expectation of asset tapering as early as next month.

- Gold prices remained range-bound for the week, with a spike towards 1780 as the DXY weakened. However, prices ended the week at 1757; alongside the JP Morgan report that bitcoin has become the preferred alternative to gold as the portfolio inflation hedging tool.

Macro, Technicals & Order Flow

Bitcoin

- We’ve seen bitcoin outperforming against the macro backdrop. The 50,000 level was broken, leading to a clean run to 56,000. Price is looking very bullish here now – a break of the highs at 56,530 (just happened) will likely test 58,000. Price is looking overbought here on the stochastic indicator, however overnight we saw a gap on some feeds to 51,000, leading to some liquidations in derivatives and select spot venues.

- A mixture of low liquidity on Sunday and a big order through on Bitstamp was the culprit here. Stops hit. Market quickly took it back to fair pricing. Exchange volumes across the board spiked as part of the rebalance.

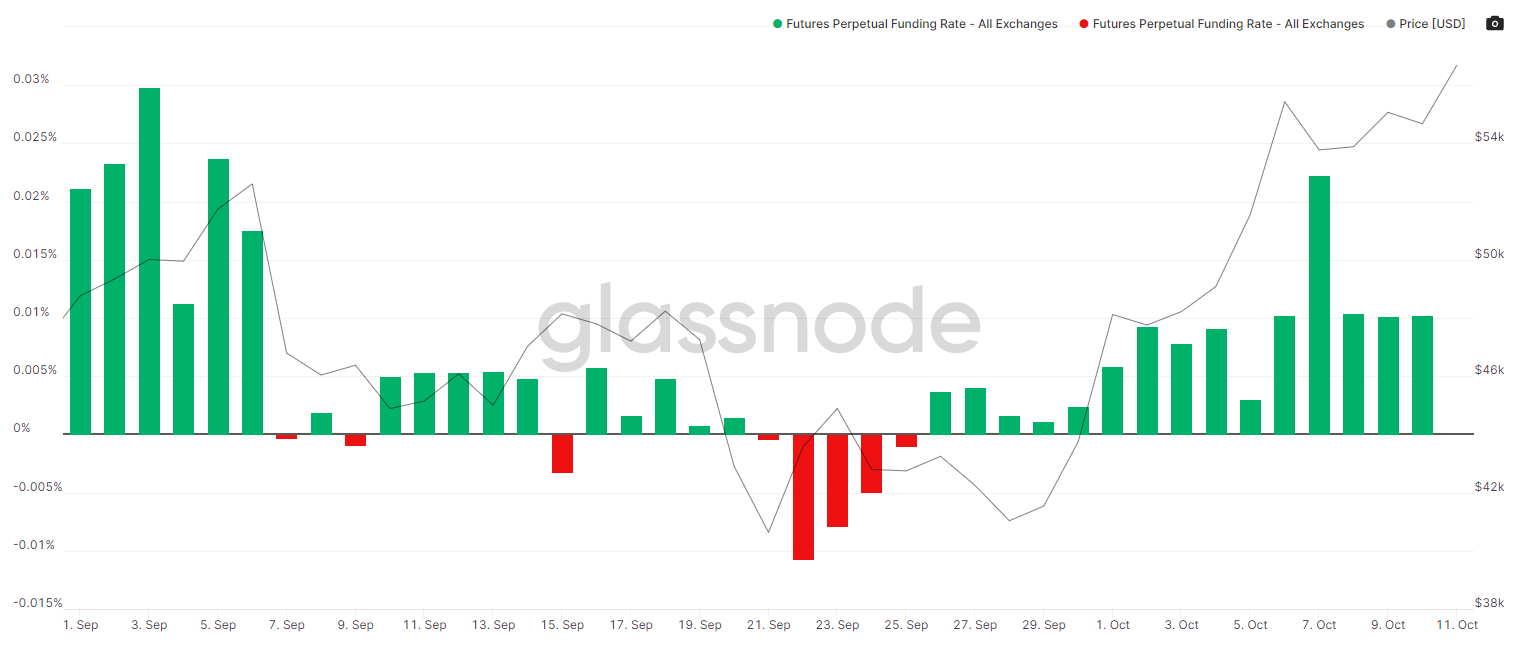

- Perpetual funding rates are positive, but within a manageable range. Open interest is steady and growing. We don’t expect any wild liquidations (beyond unexpected spot orders at Bitstamp!) this week.

BTC Perpetual Swaps Funding

- Notably, the futures leverage ratio is low. This move is clearly driven by spot inflows, and has room to move. Fund flows have been building throughout September and into October, with JP Morgan citing bitcoin as a hedge. Note that we are not close to the fund inflows that we saw before the May sell-off.

Bitcoin Futures Estimated Leverage Ratio

Bitcoin Held By Funds

- Grayscale Trust premium is still negative in the face of these inflows, which does not bode well for this trade. If we see an ETF approved, this may cause continued pressures. Similar to the challenges that we’ve seen around LICs in Australia.

Grayscale BTC Trust Premium

- Long-term holders continue to accumulate.

Bitcoin: Total Supply Held by Long-Term Holders

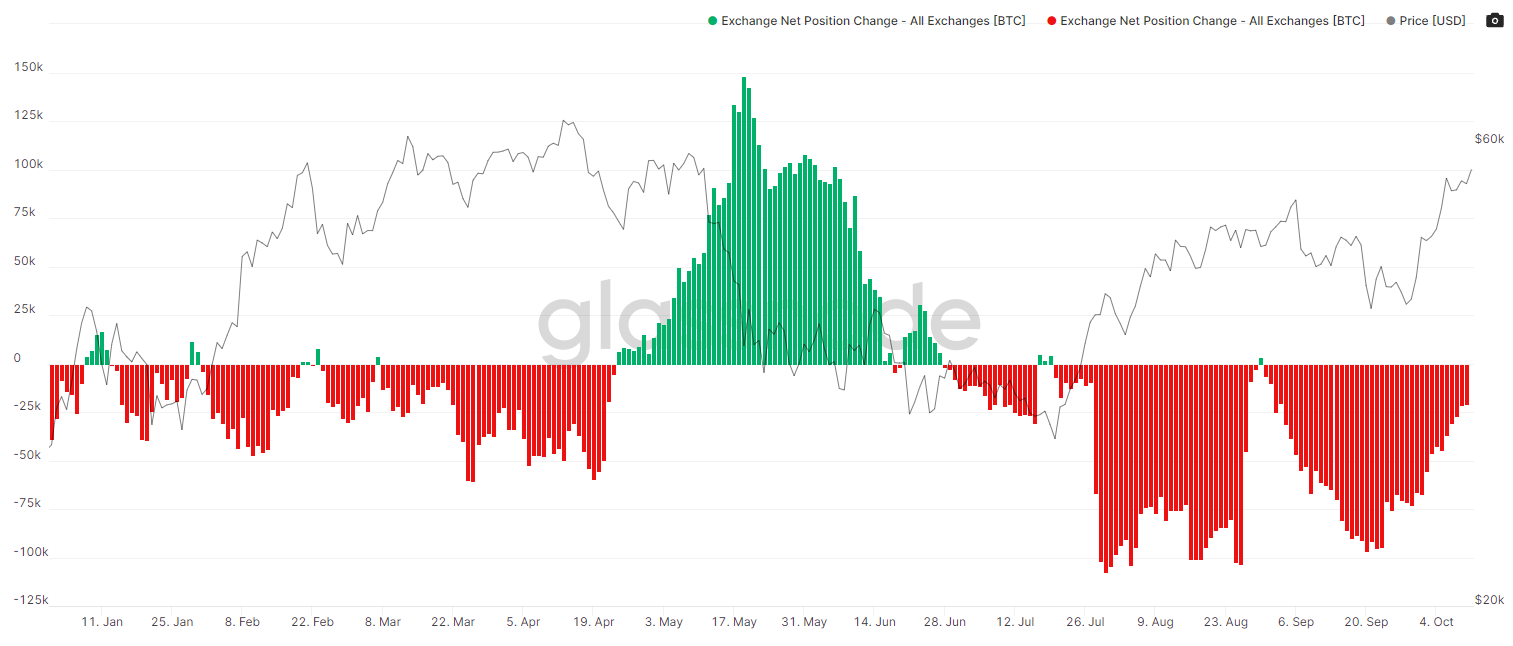

- Net outflows from exchanges are beginning to moderate after weeks of outflows. Despite this, we expect another topside run in the short term, with derivatives leverage increasing before we see a meaningful turn.

Bitcoin Net Position Change

- The futures basis curve continues to expand. Notably, the CME which is usually trading at a discount to crypto derivative exchanges has been trading at a premium this week, spiking above 16% at one point. Another sign of the market structure – institutional and fund driven.

BTC Futures Annualised Rolling 1 Mth Basis

- Seasonality is playing out beautifully this month in “Uptober”. We’ve been looking for market signs that the market could play BTC as a hedge in inflation/stagflation. The early signs are pointing to yes, and given flows into inflationary hedge value stocks, it seems that BTC is playing to the same tune. Keep an eye on exchange outflows, as this is moderating – although we’d like to see this coupled with an extension in price and a leverage spike before calling any meaningful turns in the short-term.

BTC Seasonal Returns

Ethereum

- Ethereum lagging behind bitcoin, recently broken back into the range between 3340 and 3560. We’ve been mentioning the ETH/BTC play after the 2021’s run in ETH. Price is approaching the 200 SMA. and signs are pointing to a break lower against BTC.

- We mentioned last week that we could be in the early stages of hedge vs risk asset playing out. This seems to be the emerging case.

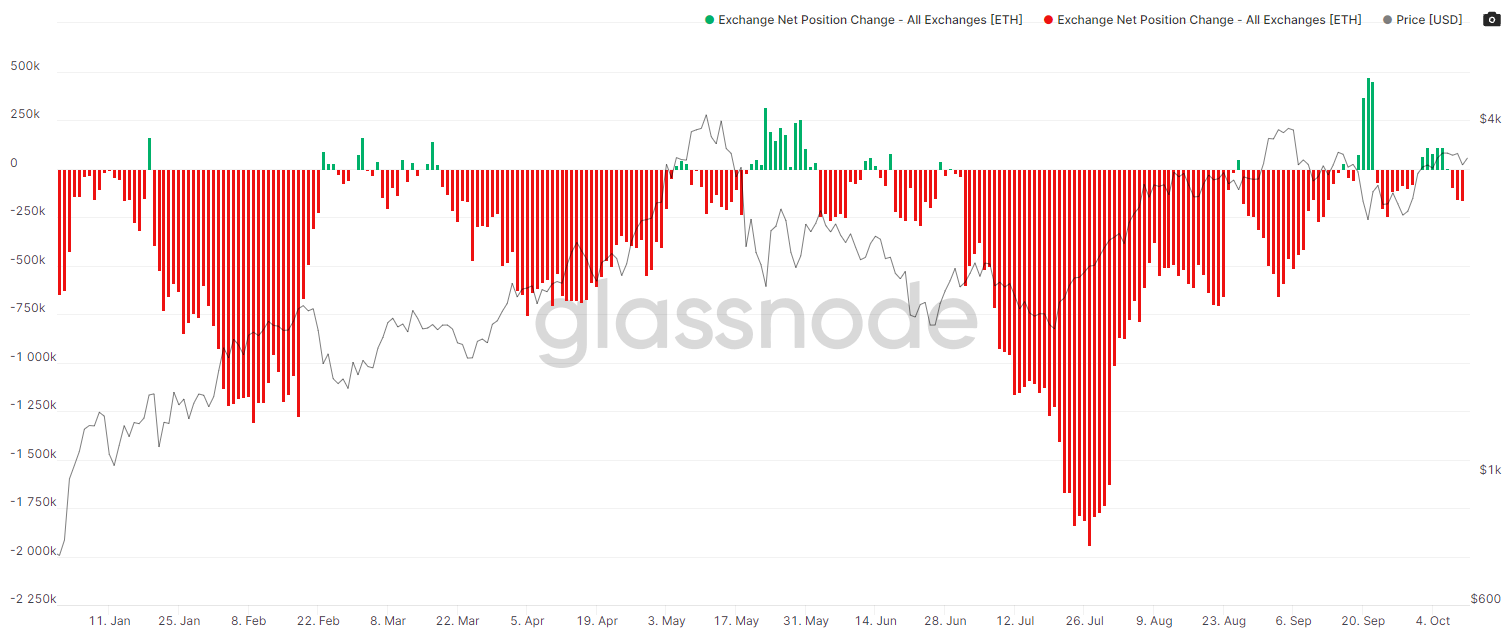

- This said, the market is still looking buoyant against the USD this week. The VIX has dropped back below 20, outflows from exchanges are increasing and the perpetual funding rates and leverage are at manageable levels.

Ethereum Exchange Net Position Change

ETH Perpetual Swaps Funding

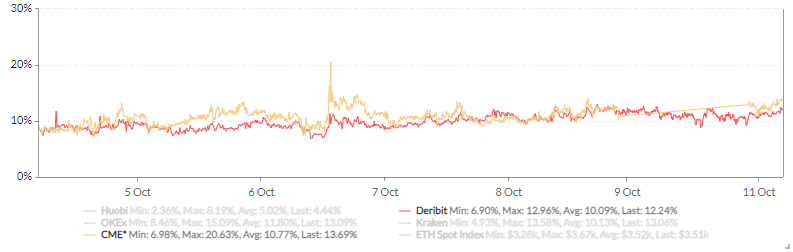

- ETH basis curve is continuing to expand – which is good news for yield hunters, and a bullish sign given growing institutional interest.

ETH Futures Annualised Rolling 1 Mth Basis

- Ethereum staking contracts continue to limit floating supply – the amount of ETH in the ETH 2.0 staking contract currently sits at 7,913,209 . This represents 6.71% of the total supply estimated to remain locked for ~ one year, continuing to slowly constrict supply.

- We’ve seen some positive moves from layer 1s and 2s recently, with a notable shoutout to Fantom that broke highs again over the past week on the back of a new yield farm. Generally, the mad rush into a yield farm never ends well, but Fantom’s tech and relatively low market cap seem to be catching up to other DeFi protocols. (Disclaimer: we own Fantom).

New Inflows into Fantom

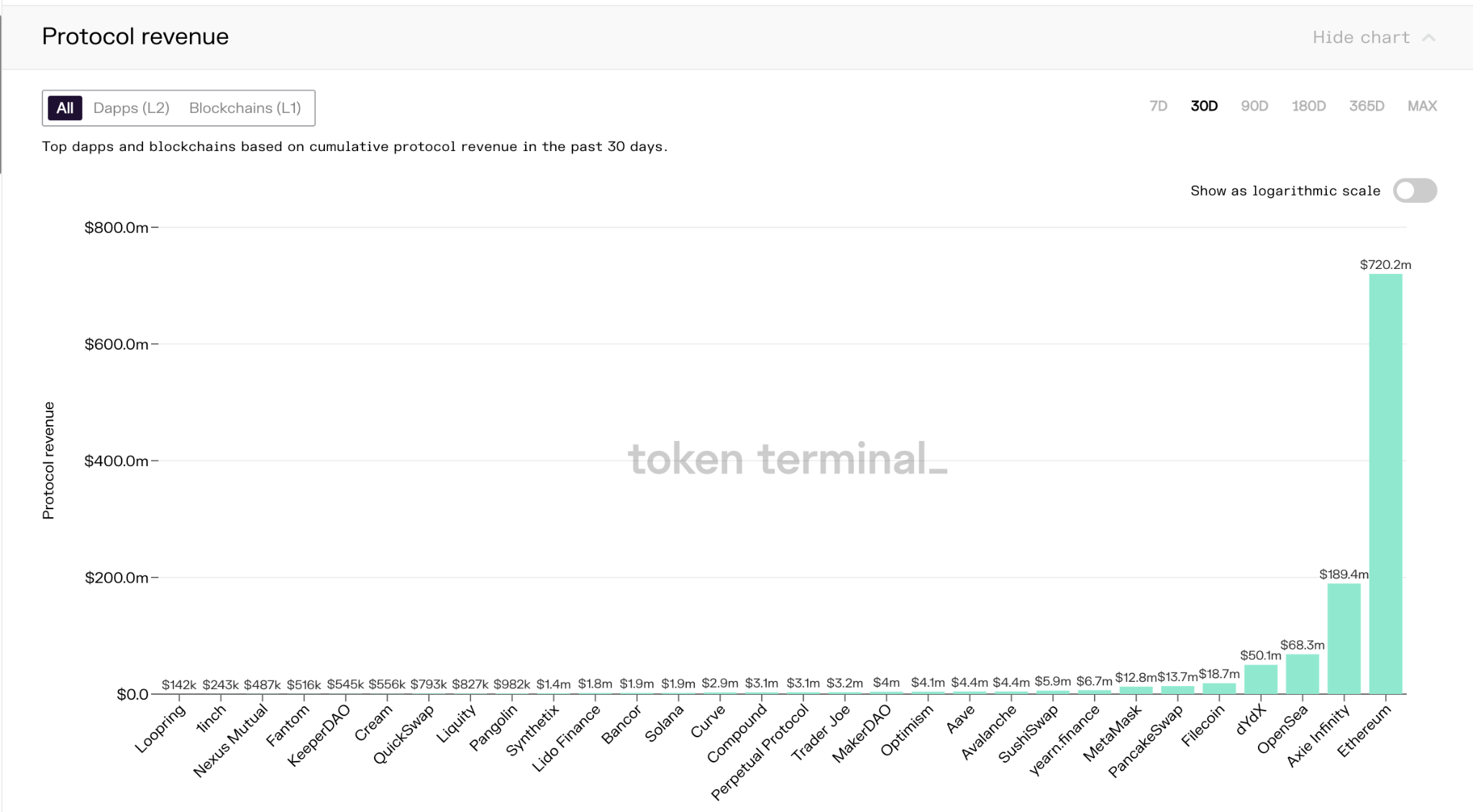

- Nonetheless, keep things in perspective with the ole’ ETH incumbent – it still dominates protocol revenue and perceived safety, despite challenges around speed and fees.

Protocol Revenue

DeFi & Innovation

- Total value locked in DeFi tops $200 billion for the first time.

- AAVE deploys on Avalanche network, deposited assets reach $1 billion in a few hours.

- MakerDAO begins funding to tackle world issues, starting with climate change.

- IMF director says 110 countries are currently working on CBDCs.

- Arab bank set to integrate crypto services using Tezos’ blockchain.

- MetaMask partners with three crypto custodians towards higher institutional adoption.

- El Salvador starts mining bitcoin using volcanic energy.

What to Watch

- Last week, we conjectured that US regulators are taking the crypto wave of innovation seriously instead of bluntly cracking down on the asset class. This week, the SEC approved the first crypto-related ETF, with the SEC having no intentions of banning digital assets. Crypto was also included in a fiat-based bill on ransomware, and a National Cryptocurrency team was created by the Justice Department. The question remains on what departments will ultimately have authority over cryptocurrency legislation, and whether different sectors of the asset class will sit under separate verticals. In any case, the pillars are being built rapidly and we look forward to new developments this upcoming week.

- September’s jobs report disappointed, the debt ceiling raised while inflation continues to reach new targets in the US and across the global economy. Could such factors change the Fed’s tapering plans? Seems unlikely at this point, with November on track for the Reserve to begin reducing bond purchases. Meanwhile, we’ll keep an eye on September’s Consumer Price Index and detailed records of the FOMC’s last meeting, both slated for release next Wednesday, for insights on what to expect in the few weeks ahead.

FAQs

What significant milestones were achieved in the crypto market during the week of 11th October 2021?

The crypto market saw Bitcoin crossing a $1 trillion market cap for the first time since May, driven by institutional flows. The total value locked in DeFi reached $200 billion, and AAVE deployed on the Avalanche network, reaching $1 billion in deposited assets within hours.

How did Bitcoin perform compared to Ethereum and other digital assets during the week?

Bitcoin outperformed, breaking the $50,000 level and reaching $56,000. It returned 13.44% for the week, while Ethereum lagged behind with a return of 0.07%. Bitcoin’s move appeared to be driven by institutional flows, and its dominance increased as it acted as an inflation hedge.

What were the key macroeconomic factors influencing the crypto market during the week?

Several macroeconomic factors influenced the market, including the U.S. Senate’s vote to raise the debt ceiling, disappointing U.S. Jobs report, seven-year high in U.S. WTI crude price, and the U.S. Justice Department’s setup of a National Cryptocurrency Enforcement Team. Additionally, institutions were buying Bitcoin rather than gold as an inflation hedge.

What developments occurred in the DeFi and innovation sector in the crypto space?

In the DeFi sector, AAVE deployed on the Avalanche network, MakerDAO began funding to tackle climate change, and the total value locked in DeFi topped $200 billion. Innovations included El Salvador mining Bitcoin using volcanic energy, MetaMask partnering with crypto custodians for institutional adoption, and Arab bank integrating crypto services using Tezos’ blockchain.

What should investors watch for in the coming weeks in the crypto market?

Investors should watch for developments in U.S. regulations, including potential ETF approvals and the creation of cryptocurrency legislation. They should also monitor global economic factors such as inflation, the Fed’s tapering plans, and the Consumer Price Index. Additionally, the market’s response to recent positive crypto news and the potential approval of a BTC ETF could be significant.

Disclaimer

This document has been prepared by Zerocap Pty Ltd, its directors, employees and agents for information purposes only and by no means constitutes a solicitation to investment or disinvestment. The views expressed in this update reflect the analysts’ personal opinions about the cryptocurrencies. These views may change without notice and are subject to market conditions. All data used in the update are between 27 Sep. 2021 0:00 UTC to 3 Oct. 2021 23:59 UTC from TradingView. Contents presented may be subject to errors. The updates are for personal use only and should not be republished or redistributed. Zerocap Pty Ltd reserves the right of final interpretation for the content herein above.

* Index used:

| Bitcoin | Ethereum | Gold | Equities | High Yield Corporate Bonds | Commodities | TreasuryYields |

| BTC | ETH | PAXG | S&P 500, ASX 200, VT | HYG | CRBQX | U.S. 10Y |

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Bitcoin Mining in the US: Main Challenges

Bitcoin mining in the United States has recently faced a range of challenges, from regulatory hurdles to community and environmental concerns. As a significant hub

Bitcoin Halving: Market Reacts

The 2024 Bitcoin halving, a significant event for the cryptocurrency world, marked a notable shift in the market dynamics of Bitcoin. As the block reward

Weekly Crypto Market Wrap, 22nd April 2024

Download the PDF Zerocap provides digital asset liquidity and digital asset custodial services to forward-thinking investors and institutions globally. For frictionless access to digital assets

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.