27 Jan, 21

The Benefits of African Crypto Integration

As Bitcoin (BTC) sits near its all-time high alongside many crypto assets, global focus is being placed on its value as a tradable store of wealth that has immense value to any individual’s portfolio. While this is one key component of BTC’s value and many digital assets’, alternative uses are flourishing in nations across Africa. A region plagued with misfortune and underdeveloped infrastructure is being revitalised on the back of entrepreneurs and visionaries that maximise the utility of digital assets to quash many of the issues holding their nations back. Significant interest from the Chinese government, Twitter founder Jack Dorsey and a host of well-established crypto companies, such as Binance and Huobi, displays the widespread consensus that Africa is set to become one of the most exciting regions in the digital asset space. As the crypto-sphere grows and finds new solutions to an array of inefficiencies in global markets, African crypto integration positioned to capitalise on all that it has to offer.

Africa’s Traditional Systems and Their Struggles

Many of Africa’s economies have been widely regarded as broken for some time, due to several systemic issues such as poor governance, low-quality infrastructure and sparse growth opportunities. The lack of purchasing power in the region is a significant barrier to economic growth, as some nations bear witness to reoccurring double-digit and even triple-digit inflation rates. Figure 1 displays the significant disparity between Sub-Saharan economies and the global average. Even Africa’s largest economies are subject to currency devaluation with the South African Rand (ZAR) losing over 50% of its value against the greenback. A plethora of nations have faced the same troubles, as traditional methods have proven to be of little value against increases in domestic demand and supply shocks, particularly to nations that are overtly subject to destructive weather patterns or have an overreliance on agriculture.

The political instability present through the continent has contributed to the aforementioned inflation and volatile swings in currency value. This impacts international investment and trade drastically, as inconsistent pricing and a high-risk environment scares off long-term investors and burdens exporters. Perhaps the most damaging by-product of these swings is the inconsistent presence of capital controls. Oftentimes, in a bid to accumulate foreign exchange reserves and protect against currency dumps, governments will restrict money flows. Without warning, businesses are losing invested capital. The question of how one might secure or repurpose “captured capital” is becoming increasingly prevalent in the region as governments restrict any company’s ability to circumvent the problem traditionally.

These issues are further exacerbated by a lack of banking infrastructure across the continent. While there is variation from country to country, the basket of contributing factors are similar across the region. Increasing sovereign debt is crowding out private credit in local banks, taking much-needed capital from innovation and development. A decrease in operational viability for international banks and financial legacy institutions has led to withdrawals from the region, further limiting the populace to local banks that are preoccupied with damage control due to the broader economic circumstances. As a result, this situation has created a lack of competition and constricted interbank liquidity, forcing many to look elsewhere for banking services.

This has sparked the rise of mobile banking which has acquired a significant market share over a short period. In 2018, 66% of adults in Sub-Saharan Africa were still bankless. With prices dropping for tech basics such as mobile phones (smartphones in particular), the cost-effective and more reliable nature of mobile banking has captured significant attention from the population. While still imperfect, the success of the mobile banking framework has displayed the result of providing a meaningful solution to a continent’s problems utilising leading technology.

Why African Crypto Integration Is the Solution

While mobile banking deserves significant merit for its strides in Africa, the key issues troubling these nations are not avoided through its use. Mobile money is merely a digital representation of the preexisting cash in circulation. Therefore, the same risk associated with centralisation, private interest and government misconduct are transferable. However, this remarkable shift to transacting digitally has made a large portion of Africans more comfortable with the option of going cashless. As this transition occurs, a paradigm shift in commerce has begun, lending itself to the eventual wide adoption of African crypto integration through digital asset services and use cases.

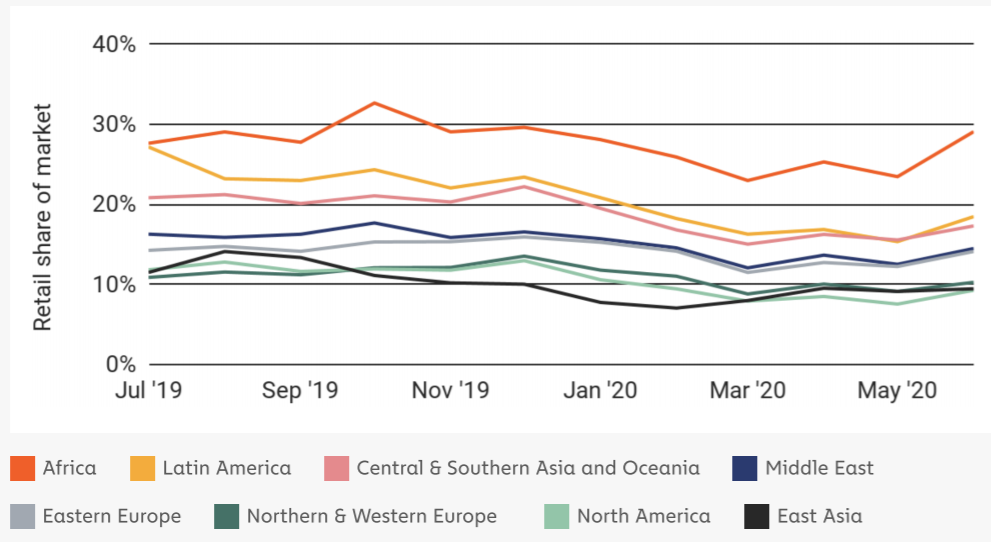

In the western world, the transition to the common use of digital assets has been led by speculative trading and the opportunity for a superior ROI. While this is still a component of its rise in Africa, developing nations are best positioned to display how powerful digital assets and their surrounding infrastructure can be when fully employed – and people in Africa are noticing. Compared globally, retail transactions (<US$10,000) account for almost 30% of Africa’s crypto trade volume, higher than any other region in the world (See Figure 2). This indicates high-use in everyday transactions such as remittances and speaks to the widespread applicability of digital assets that is not comparable in the developed world.

The deflationary nature of bitcoin and various other crypto assets directly combats exposure to the risk that local currencies offer, giving residents the choice to opt for a store of value and medium of exchange that can comfortably hold value long-term. In addition to this, the new-found freedom of choice allows individuals and businesses to circumnavigate the capital controls discussed above.

While assets such as BTC are already in use across the continent (and still set for user growth), the systemic issues impacting the territory have led to an increasing volume of stablecoin demand. However, due to a lack of knowledge and accessibility, the immense value offered by stablecoins such as USDT, PAXG and DAI is yet to be fully utilised across a continent that lacks any form of currency stability. Ultimately, by pegging their asset value to alternate currencies or commodities such as the US dollar or gold, stablecoins limit volatility and currency risk. These digital assets also offer a faster, more cost-effective method to transact via decentralised blockchain networks that limit malicious intervention and are global in nature. As tech adoption continues to grow and the more nuanced digital assets gain increased exposure, we will likely see the benefits of stablecoins flourish in Sub-Saharan Africa.

The global reach of crypto assets is of particular importance to a region that is consistently burdened with capital controls and relies heavily on remittances, not only for the livelihood of its residents but also a sizable contribution of its GDP. According to the World Bank, approximately US$48.7 billion was remitted to Sub-Saharan African bank accounts or 2.76% of the region’s GDP. With average remittance fees sitting at 6.51% per transaction globally and reaching as high as 15% between select African nations, traditional structures make it difficult for individuals to provide the desired support to their families. While there has been a visible effort by organisations such as the G20 and UN to reduce fees, the current system makes it impossible to achieve any real result as there are too many intermediaries involved. The lack of change from service providers and limited care for those that rely on their systems has prompted many to make the transition to digital assets as a means of saving time and money. With models such as the Ethereum network cutting transactional costs and speeds by orders of magnitude, few things hold back those that are not pleased with the current financial model.

Barriers to Success

While African crypto integration rates rank among the highest globally, foundational issues are constricting its potential. The development of the crypto ecosystem is still in its early stages as key components such as mining operations, trade volume, internet access, smartphone adoption and supporting retailers are limited. This is enacting a noticeable slowing effect on African crypto integration. Despite this, there are many entities focused on developing the required infrastructure, from Square to Luno, all to revolutionise the outdated system in place. In turn, making the financial systems in Africa updated and world-leading.

Due to the astronomical rise in usage throughout 2020, some are concerned that stringent regulatory bounds will come into place, further stemming growth. Some nations are already close to finalising legislation on digital assets and their use. South Africa is weeks away from classifying digital assets as financial assets, opening the door for crypto businesses like Luno to register with the Financial Sector Conduct Authority (FSCA), offering legitimacy and a great step forward for the future of innovation in the African crypto-sphere. Similarly, in September last year Nigeria released a paper expressing its views on crypto assets and how it intends to regulate them in the coming years. It states that all digital assets are now viewed as securities unless proven otherwise, suggesting that any crypto-related business will need to apply for licensing should they wish to operate within the country. While major hubs for crypto adoption such as these are leaning towards progressive policies, other nations are taking a back seat approach with the hopes that the results of their more progressive neighbours’ actions will provide clarity on how to approach the space.

As regulation increases and standardised policies such as AML/CTF become widespread, another concern is raised. With an estimated 1 billion people unable to prove their identity due to a lack of documentation, the crucial goal of financial inclusion in Africa is at risk. While regulatory laws surrounding identity are necessary for the protection of all parties involved, it is also imperative for the industry’s reputation. Although there is a long way to ensure that this boundary is lowered for all, organisations such as ID4Africa are making strides to ensure that identity issues are mitigated.

What the Future Holds for Crypto in Africa

As awareness grows and technological barriers are removed, the use of digital assets will grow at unprecedented levels across Africa. Not only will it fundamentally change how money is exchanged and stored, it is likely to impact everyday commerce to a high degree. With newfound ease of access to alternate currencies that do not pose the same centralised challenges, merchants will accept various digital assets for everyday transactions, leading to a freer economy. This will provide immense value for the African economy as individuals, companies and cities are brought onto an even, and some might say superior, playing field compared to the developed world. The economic growth that can occur on the back of the already strong enterprise in this region will change Africa greatly in the coming decades. If government and industry can work together, a world in which blockchain technology and cryptocurrencies fuel entire economies is not improbable, and nowhere is better placed to capitalise on this than Africa.

Zerocap provides digital asset investment and custodial services to forward-thinking investors and institutions globally. Our investment team and Wealth Platform offer frictionless access to digital assets with industry-leading security. To learn more, contact the team at [email protected] or visit our website www.zerocap.com

Like this article? Share

Share

Share  Tweet

Tweet  Post

Post

Latest Insights

Ethereum Smart Contracts: How They Changed Crypto

Ethereum, launched in 2015, revolutionized the digital world by introducing “smart contracts,” self-executing contracts with the terms of the agreement directly written into code. This

Main Crypto Events in the World

The world of cryptocurrencies is dynamic and ever-evolving, with numerous conferences and events held globally to foster innovation, collaboration, and networking among crypto enthusiasts. Here’s

What is Ethena Finance?

Ethena Finance (ENA/USDe) is emerging as a notable player in the cryptocurrency and decentralized finance (DeFi) sectors. Powered by its proprietary stablecoin, USDe, Ethena aims

Receive Our Insights

Subscribe to receive our publications in newsletter format — the best way to stay informed about crypto asset market trends and topics.